Agricultural production is one of the few remaining examples of a “nearly” perfectly competitive industry, where products are largely homogeneous and firms are price-takers. However, due to the rapid consolidation of farms, even the agricultural production industry is at risk of market-power imbalances which have impacted other industries. Two market forces, economies of scope and economies of scale, could be behind the increase in consolidation.

Farms increase production levels and diversify product mix to exploit scale and scope economies. As a result, they increase in size, creating the potential for the largest farms to exercise market power and adversely affect consumers. Industry consolidation also has potential for negative side effects relating to the environment, especially in confined animal operations.

To anticipate the likely extent of further consolidation, we examine recent growth and diversification trends to analyze whether Washington farms of different sizes have experienced scale and/or scope economies. Scale or scope economies occur, respectively, if average cost decreases with output level or number of outputs produced. We identify and compare scale and scope characteristics for four major agricultural production industries, both for firms existing in 1992 and for firms that entered the industry by 2002. We also compare scale and scope characteristics and trends for Washington State to national trends.

We examined data from the U.S. Census of Agriculture for Washington wheat, apple, beef, and dairy producers. Value of production from each of these industries consistently ranks them among the top five agricultural commodities in the state (USDA 2006). Our data came from the three most recent agricultural censuses—1992, 1997, and 2002. We included all firms in the 1992 census that produced at least one of these commodities and for which the operator selected “farming” as the main occupation. This data sample was comprehensive and only omitted hobby, recreational, and retired farmers. However, this one exclusion removed slightly more than half of all dairy and wheat farms, 2/3 of apple farms, and 4/5 of beef farms.

Firms were ordered by size based on their 1992 agricultural sales, excluding government payments and subsidies. They were divided into nonoverlapping deciles, or cohorts, with cohort one containing the smallest 10% of farms and cohort 10 contained the largest 10%. See Table 1 for mean sales by cohort. Farms retained their original cohort assignment across censuses, regardless of whether they grew, shrank, or otherwise changed over time. This preservation of cohort assignment permitted measurement of cohort-specific growth, a key factor for determining which farm size grew the fastest, and facilitated comparison and analysis across census periods. Each cohort initially had the same number of farms, but those that stopped being farmed caused these numbers to shrink unevenly across censuses.

To assess scale economies and calculate commodity-specific growth tendencies, compound growth rates were calculated for the mean of each cohort in each industry. These growth rates measured the rate at which real sales, a proxy for output, increased. To measure scope economies and calculate diversification tendencies, farms in each cohort were divided into five sales categories based on the percent of total agricultural sales obtained from the sale of the main commodity group: (1) 90% or greater, (2) 75–89.9%, (3) 50–74.9%, (4) 25–49.9%, and (5) less than 25%. For example, if a wheat farm in our sample derived 65% of its sales from grain and oilseeds and 35% of its sales from other products/services, this farm fell into diversification category three. A specialization index was created as a weighted sum of the share of farms in each diversification category, with the mean sales percent for the category used as the weight. This index ranges from zero to one, with a score of one indicating complete specialization and a score of zero indicating complete diversification to other agricultural products/services.

A graphical depiction of cohort growth rates for each of the four Washington industries is presented in Figure 1. Growth rates are included for two periods: 1992–1997 and 1992–2002. From the graphs, it is apparent that there was a negative correlation between initial farm size and growth rate in both periods for three of the industries—wheat, apples, and beef. The statistical correlation coefficients documented this observation; for the 10-year period, they were -0.83, -0.64, and -0.63 respectively. The dairy industry was the exception to this pattern; its 10-year correlation coefficient was positive and strong, 0.82.

Wheat farms had the strongest negative correlation between farm size and growth rate. They were also the only industry to have positive growth rates in all cohorts. For this industry, smallest farms grew the fastest, and largest farms were among the slowest-growing.

In both the wheat and apple industries, the smallest cohort of farms set the bar for growth. In the apple industry, only the growth rates of the smallest two cohorts were substantially different from the others for the 10-year period (see Panel B of Figure 1). In fact, growth rate in this industry was not strongly related to initial farm size for mid-to-large cohorts. While the correlation between growth rates and farm size was also negative for beef farms, the cohort pattern was quite different—cohort four had nearly three times the growth rate of any other cohort.

The growth pattern for dairy farms differed in even more important ways from the other industries. Besides a strong positive correlation between farm size and growth rate, surviving farms in the smallest cohort shrank by 4%. Nearly all growth of farms in this industry occurred in the largest three cohorts.

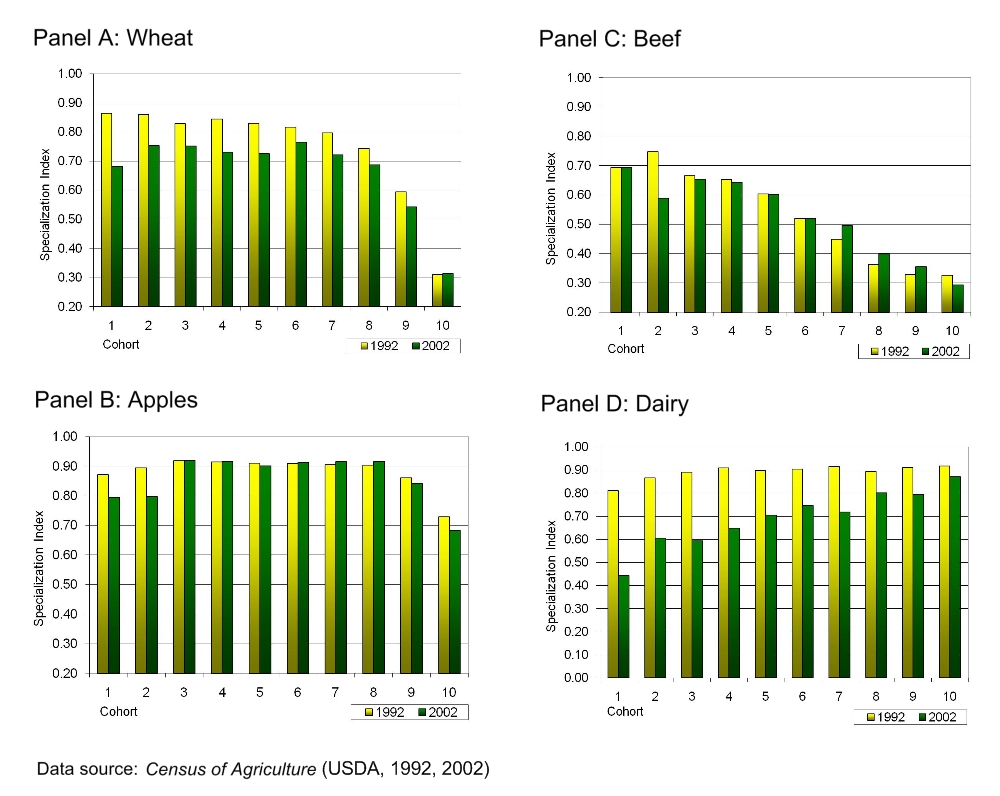

As was the case with growth patterns, Washington wheat, apple, and beef farms followed a specialization pattern that contrasted sharply with the pattern exhibited by dairy farms. For wheat farms, the level of specialization was negatively related to farm size in all censuses, and the correlation decreased in strength over time (see Panel A of Figure 2). While the largest cohorts were the most diversified, the smallest cohorts tended to diversify more rapidly over time. The specialization scores in 1992 ranged from 0.86 for cohort one to 0.31 for cohort 10, with an average specialization score of 0.75. In successive censuses, all but the largest cohort became more diversified. The average score dropped to 0.67 by 2002.

Apple farms also exhibited a negative relationship between farm size and specialization level in each census, but the correlation was not as strong as for wheat farms (Panel B of Figure 2). The specialization scores in 1992 ranged from 0.92 for the third cohort to 0.73 for the tenth, with an average of 0.88, so apple farms were more specialized than wheat farms. They also remained more specialized. Only the smallest two cohorts and the largest cohort became much more diversified by 2002, and the average specialization score dropped only by 0.02 to 0.86.

Beef farms showed the strongest negative correlation between size and level of specialization. Panel C of Figure 2 shows a near-linear relationship between cohorts three–ten and the specialization score. In addition to having the strongest correlation between farm size and index score, beef farms had the lowest levels of specialization with average index scores close to 0.50 in both years. On average, beef farms showed a trivial reduction in average specialization score between 1992 and 2002.

Specialization levels in the dairy industry contrasted sharply to those of the other three industries. Whereas specialization index scores were negatively correlated with cohort size in the wheat, apple, and beef industries, they were positively correlated in the dairy industry (Panel D of Figure 2). Thus, among the four industries examined, dairy is the only one in which specialization increases with farm size. Also, on average, the dairy industry was the most specialized industry in the sample in 1992 but diversified more rapidly than any of the others. It experienced an average drop in specialization index score of 23% from 1992 to 2002.

One important insight gleaned from these results is that, in all industries, higher levels of specialization were generally associated with higher growth rates. Consequently, we infer that economies of scale, rather than economies of scope, appear to have driven farm growth.

Most farms that entered the wheat, apple, and beef industries were comparable in size to farms in the smallest incumbent cohorts. In the dairy industry, however, entrants were bimodally distributed between smallest and largest incumbent cohorts, with relatively few comparable in size to mid-level cohorts. New farms in all industries entered with specialization levels higher than the average incumbent farm. Thus, while many farm entrants failed to fully capture either economies of scale or economies of scope at the time of entry, they entered at sizes for which evidence for the existence of economies of scale and/or scope was the strongest. In all but the beef industry, new farms tended to diversify at a more rapid rate than incumbent farms, which implies they quickly recognized and captured economies of scope after entering the industry.

Overall, trends in Washington growth rates were similar to national growth rates in each of these industries (Melhim, O’Donoghue, and Shumway 2009). While similarities were greatest between wheat, apple, and beef farms, the national patterns reflected stronger negative correlations between farm size and growth rate for these industries. Growth rate patterns of Washington dairy farms also generally followed the trends of national dairy farms. One exception is that the smallest cohort, which grew by 5% nationally, shrank by 4% in Washington. Washington diversification trends were also similar to national trends for all but the beef industry. However, in all industries, Washington farms were generally more specialized.

The most striking difference between Washington and national trends dealt with the size of entrants in the wheat, apple, and beef industries. Average sizes of national entrants exceeded the average size of their incumbent counterparts while average sizes of Washington entrants were smaller than incumbents. In addition, farms entering the dairy industry nationwide were much larger than the average incumbent and did not follow the bimodal distribution of new entrants in Washington. In contrast, diversification patterns of new entrants in most national industries did not differ much from the pattern seen in Washington, i.e., farms entered the industry at a more specialized level than incumbents and they diversified more rapidly over time.

Census-documented changes between 1992 and 2002 imply that the wheat, apple, and beef industries in Washington may, in one sense, be converging toward equilibrium farm sizes. While farms in all size cohorts are growing, the largest cohorts are growing at slower rates. This finding, which also applies to the nation, could be the result of the largest farms facing diseconomies of scale, or at least diminishing economies of scale, as output expands. However, in the dairy industry, the largest farms are among the fastest growing—evidence that strong economies of scale persist. This finding suggests that further consolidation of dairy farms is probable, which could, in the long run, ultimately distort the near perfectly-competitive nature of this industry, increase the potential adverse environmental impacts from large confined animal operations, and put the economic welfare of some small agriculturally-based communities at risk. Of the four studied, it is this industry that warrants most attention. Further, to address each of these three concerns, policymakers could focus on policies that facilitate the growth and/or diversification of small and medium-sized dairies.

With the exception of the apple industry, the more highly specialized farms have higher growth rates. This fact suggests that economies of scale rather than economies of scope drive farm growth in the wheat, beef, and dairy industries. Therefore, policies aimed at increasing output of the primary commodity on small and medium-sized farms are expected to have a greater effect on farm growth than policies oriented toward increasing diversification.

Washington trends are generally comparable to national trends, especially where firm growth is concerned, and imply similar conclusions with respect to future consolidation, growth, diversification, and policy. One exception is that the average new entrant at the national level is larger than the average of incumbent farms, whereas, except for the dairy industry, the average new entrant in Washington is smaller. Diversification trends are mostly similar, but Washington farms are more specialized on average. Another notable exception is that at the national level, beef farms become more specialized over time, a trend not followed by Washington beef farms. Despite all the similarities, the few differences between Washington and national trends document an important fact. National trends are not always the trends of individual regions and states, so policies designed to achieve a specific goal in all areas may need local adjustment.

Melhim, A. O’Donoghue, E.J., and Shumway, C.R.. (2009). What Does Initial Farm Size Imply about Growth and Diversification? Journal of Agricultural and Applied Economics: forthcoming.

United States Department of Agriculture, National Agricultural Statistical Service. (1992, 1997, 2002). Census of Agriculture. Washington, DC.

United States Department of Agriculture, National Agricultural Statistical Service. (2006). Washington 2006 Annual Bulletin. Washington, DC.

| Cohort | Wheat | Apples | Beef | Dairy |

| 1 | $36,103 | $18,266 | $4,625 | $51,792 |

| 2 | $71,660 | $49,064 | $10,023 | $125,373 |

| 3 | $100,467 | $79,769 | $16,111 | $186,526 |

| 4 | $129,508 | $118,030 | $25,816 | $243,091 |

| 5 | $161,862 | $157,320 | $41,236 | $300,511 |

| 6 | $200,432 | $205,417 | $63,855 | $370,424 |

| 7 | $247,485 | $275,739 | $96,656 | $447,275 |

| 8 | $315,726 | $374,317 | $149,266 | $591,559 |

| 9 | $442,826 | $558,835 | $237,295 | $867,413 |

| 10 | $1,562,813 | $2,085,375 | $934,075 | $1,968,144 |

Source: Census of Agriculture (USDA, 1992)

We are indebted to the anonymous reviewers for their constructive comments. The views expressed are those of the authors and do not necessarily correspond to the views or policies of the Economic Research Service or the U.S. Department of Agriculture.