Over the last decade, American consumers fueled a fast-growing market for organic food and U.S. farmers flocked to genetically engineered (GE) varieties of several major U.S. crops. The potential for GE crop production to impose costs on organic production, via accidental pollination and other mechanisms, underscores the problem of coexistence between GE and organic crops. Here we review evidence that consumer demand has led to markets for products differentiated on some basis of GE status, and that maintaining the integrity of those differentiated product markets relies on interventions such as physical distancing or product segregation. Further, at present, the costs required to support the coexistence of all markets is borne disproportionately by producers and consumers of organic food in the United States.

Demand for organic food and other products in the United States has steadily increased since the late 1990s, providing market incentives for U.S. farmers across a broad range of products to grow organic. Although the market in the United States is relatively small, it is quite strong and has realized double-digit annual growth rates over the last decade. In 2010, sales of organic food continue growing much faster than in the overall food market. Congress passed the Organic Foods Production Act of 1990 to establish national standards for organically produced commodities, and USDA’s subsequent national organic program (http://www.ams.usda.gov/nop/) regulations and certified organic label played important roles in providing consumer assurance, most likely contributing to the growth in the U.S. organic market. U.S. sales of organic products were $23 billion in 2009—about 3.5% of total at-home food sales—and will reach $25 billion in 2010, according to the Nutrition Business Journal.

USDA’s national organic standards are process-based. They address the methods, practices, and substances used in producing and handling crops, livestock, and processed agricultural products that can be certified as organic. These requirements apply to the way the product is created, not to measurable properties of the product itself. USDA regulations specify that organically produced food cannot be produced using genetically engineered materials. While these regulations are process-based and do not set a threshold limit for the accidental presence of GE materials in organic products, organic buyers in the United States and elsewhere have set thresholds and are increasingly requiring testing and other compliance measures. During the USDA’s final rule-making process, organic consumers unequivocally stated their preference that genetic engineering technologies be excluded from organic production and processing. This was recently reconfirmed in the context of animal cloning.

Although not regulated by the Federal government, there is evidence that firms in the United States can capitalize on consumer preferences by labeling food as having been grown without the use of genetic engineering. For example, WhiteWave Foods (www.whitewave.com/) sells Silk brand organic soymilk, which meets all USDA organic production and processing standards, including the prohibition on the use of genetic engineering, as well as Silk soymilk that is produced from non-genetically modified crops. WhiteWave has its own testing protocols to ensure that genetically modified crops are not present in these products: soybean seeds are tested and only approved seeds are planted; samples are pulled and tested as beans are harvested before entering a storage silo; and composite samples are taken and tested as sacks are prepared for delivery. The product commands a premium price to cover the costs of such a program—and consumers are paying it. According to industry estimates, packaged food containing a non-genetically modified organism (GMO) label claim accounted for nearly $787 million in sales in the United States between April 2009 and April 2010.

In the United States, the private sector has taken the lead in setting product-based standards to minimize the risk of contamination of non-GE products. Individual companies have used a patchwork of non-GMO standards and label claims over the past decade. Spurred by organic and natural food companies needing a consistent, verifiable and reliable standard, a nonprofit group, the Non-GMO Project, emerged recently with an independent verification system for products made according to best practices for GMO avoidance, including testing of risky ingredients—for example, soybeans. The “Non-GMO Project Verified” label claim is based on non-GE product traceability, segregation, action thresholds and other practices for GMO avoidance. Action thresholds are set for high-risk inputs and products, such as corn and soybeans, and are set at 0.9% for food grains, for example. The Non-GMO Project avoids legally and scientifically indefensible claims that products are 100% GE-free. A broad set of U.S. organic and natural food companies have already joined the non-GMO Project to use its non-GE testing and labeling protocol—including Eden, Hodgson Mill, Lundberg’s Family Farms, Nature’s Path Organic, Organic Valley, Rice Select, Snyder’s of Hanover, Straus Family Creamery, and many others. Whole Foods Market, the largest natural foods supermarket chain in the United States, is also partnering with the Non-GMO Project to use their non-GE testing and labeling protocol for its private label products.

Many important foreign markets have regulatory requirements for non-GE products, and buyers may also set more stringent private standards in these countries. The European Union, (EU) for example, has mandatory GE labeling and coexistence policies. All products marketed in the EU for which the content of a product exceeds 0.9% GE ingredients must be so labeled. This policy places a labeling cost on GE crop producers. Yet, results from public polls in the United States and elsewhere show “overwhelming support for labeling of genetically modified food” ( Onyango, Nayga, and Govindasamy, 2006). Consumer preference for non-genetically engineered food is not as well documented.

There is ample opportunity for U.S. crop producers to take advantage of the many production benefits that GE crops provide. The vast majority of U.S. soybean, cotton and corn producers plant genetically engineered varieties, attesting to GE crops’ commercial production appeal. Although recent industry surveys indicate that a majority of U.S. consumers buy organic products at least occasionally, food purchase data suggest that a majority of U.S. consumers are either unaware of or indifferent to the presence of GE ingredients, or are unable to afford the prices that organic and non-GE foods command.

Clearly we have a largely GE-indifferent mainstream food market, a well established and growing market for foods differentiated by the organic label, and evidence in the United States and abroad of another market for products specifically differentiated by their lack of GE ingredients. The coexistence of these markets is threatened by the possibilities of transgene flow, GE-induced resistance of pests to pest control products, product comingling, and other externalities. We note that this is the case not just for organic markets and GE crop production, but also for commodities differentiated in other ways. For example, in the United Kingdom, two differentiated varieties of non-GE rapeseed are produced for oil–one for edible oil, the other for an industrial grade product that is prohibited for human consumption. The different markets rely on strategies that assure coexistence without interference with one another.

Contamination of differentiated products can occur at many different stages in the production and processing chain. Gene flow from genetically-altered crops, even those approved for food uses, is a particular issue for farmers that target organic food markets, but other modes of contamination may also occur. For example, in 2002 transgenic corn plants engineered to express a vaccine were found to have “volunteered” in an otherwise normal corn planting. This discovery led to incineration of plants, both corn and soybean, across a wide acreage and fines on the firm that produced the transgenic variety. In 2000, StarLink, a gene-altered corn approved only as animal feed, was found in corn chips and other food products throughout the United States, prompting product recalls. StarLink corn was commingled with other corn after it was harvested.

Failure to manage biological confinement can lead to disruption of domestic and international markets for organic products since international and USDA organic regulations prohibit the use of genetically modified organisms in organic crop production. Markets for organic food differ in their tolerance levels for the adventitious presence of genetically modified organisms, with some countries and buyers setting a zero tolerance, and others allowing small amounts, generally under 1%. The tolerance level that organic farmers must meet has largely been market driven, rather than regulatory driven in the United States.

It is no surprise that organic farmers perceive contamination as a big issue. The University of Maryland in cooperation with a research team from USDA's Economic Research Service conducted a set of focus groups across the United States to explore the risks faced by organic farmers, how they are managed, and needs for risk management assistance. Participants in these sessions included operators of about 60 farms, producing many different organic crops in various parts of the country. Contamination of organic production from genetically engineered crops was seen as a major risk, particularly by grain, soybean, and cotton farmers. Organic farmers at all the focus group sessions expressed considerable concern about risks from the use of genetically engineered crops by conventional farmers. Contamination from pollen drift from genetically engineered crops was seen as a particularly serious risk, one that the participants felt is now resulting in lost organic sales.

Organic farmers also pointed out that genetically engineered varieties may destroy the effectiveness of natural pest controls. For example, many organic farmers use Bt-based foliar pesticides, which are approved for organic use, to control insects. In recent years, transgenic varieties of corn containing the Bt protein have been developed, and organic farmers worry that their widespread use will hasten development of Bt resistance by insects and limit the usefulness of Bt organic pesticides.

Many of the organic farmers expressed a broad complaint about responsibility for transgenic crop varieties. They explained that companies developing genetically engineered crop varieties provide a technology that is useless to organic farmers, while at the same time exposing organic producers to substantial risks.

The coexistence of organic and GE crops relies on management practices, segregation and identity preservation measures at every step in the food chain, from seed production through food or feed processing and transportation.

Organic farmers use numerous management strategies—buffer zones, careful timing for crop planting, crop monitoring—to minimize to possibility of accidental contamination. One way of managing the risk of transgenic contamination is to plant the organic crop one to two weeks later than nearby conventional farmers plant so that the organic crops would not pollinate at the same time as the predominant genetically engineered varieties. This strategy has only been modestly successful because cool and wet spring weather can delay plant growth such that corn plants pollinate at about the same time regardless of planting date. Some U.S. producers and processors have grown organic corn for seed in countries with less widespread adoption of GE crops in order to have a two-mile buffer zone. In addition to adding or increasing the size of buffers, adjusting the timing of crop planting, and changing crop location, additional risk management strategies that organic farmers may use to mitigate the risk of transgenic contamination include altering cropping patterns or crops produced and discontinuing the use of inputs at risk for contamination. The use of any of these risk management strategies may increase the costs of producing organic and non-GE crops.

Growers of GE crops that have pesticidal properties, such as Bt corn and cotton, also take steps to maintain susceptibility of the pest population. They are required to set aside refuge areas—areas planted to conventional varieties of the same crop—so that the pest population includes genes of pests that are not likely to become resistant. The strategy’s success relies on the cooperation of GE variety producers and EPA enforcement of the practice. Set-asides are not costless but GE producers, as well as non-GE producers, benefit from their success.

Post-harvest preservation of the organic or non-GE trait is accomplished by segregating the organic crops and their downstream products from GE crops. Segregation is exceptionally costly. Segregating organic from GE crops requires substantially larger investment in infrastructure for handling the crop commodity and the intermediate and final products. Harvesting equipment, sorting processes, on-farm or elevator storage facilities, containers and other transportation vessels, storage at point of shipment, and processing facilities essentially have to be distinct for organic and for GE. In some cases, facilities used to process GE crops may also be used for organic crops by cleaning the facility first. For example, a cotton gin is cleaned by putting an initial load of organic cotton through the gin and treating that load as conventional product and forgoing the organic price premium on it.

A major organic producer organization in the United States, the Organic Farmers Agency for Relationship Marketing (OFARM), recently adopted its own protocol for minimizing GMO contamination. Member groups, including the top organic grain marketing cooperatives in the Midwest, have agreed to the detailed set of GMO avoidance practices, including product testing for seeds and feeds, and a sampling protocol for products.

Despite producer efforts to avoid GE contamination, one of the top organic and non-GE grain wholesalers in the United States reports that it’s rejecting an increasing percentage of the arriving loads because they test higher than 0.9% for genetically engineered material. When a load is rejected, a producer loses their organic or non-GE price premium for the product, incurs additional trucking costs for transportation to a buyer who purchases GE grain, and may have other losses. According to Lynn Clarkson, of Clarkson Grain, several factors explain their recent rise in rejected loads. First, the Non-GMO Project has sensitized many food processors regarding GMOs, and the numerous food processors that have joined this project are now demanding Non-GMO Project Verified ingredients. Also, more organic buyers are contracting for grain with non-GMO verification as well as organic certification. Clarkson Grain is conducting more GMO testing to comply with their clients’ wishes. In addition, a major tool for identifying GE contamination—the visual distinction of yellow GE corn kernels and white non-GE kernels—was lost several years ago when major non-GE white corn buyers also starting purchasing white corn from producers using GE crops.

Coexistence Problems Affect Producers’ and Consumers’ Welfare

Moschini, Bulut, and Cembalo (2005) have demonstrated that the segregation and identity preservation costs imposed on the organic sector by the introduction of a GE innovation can be so high that they overwhelm the welfare gains, or economic benefits, from the GE innovation itself. This finding relies on the existence of a non-GE differentiated market, like organic, at the time of the GE introduction.

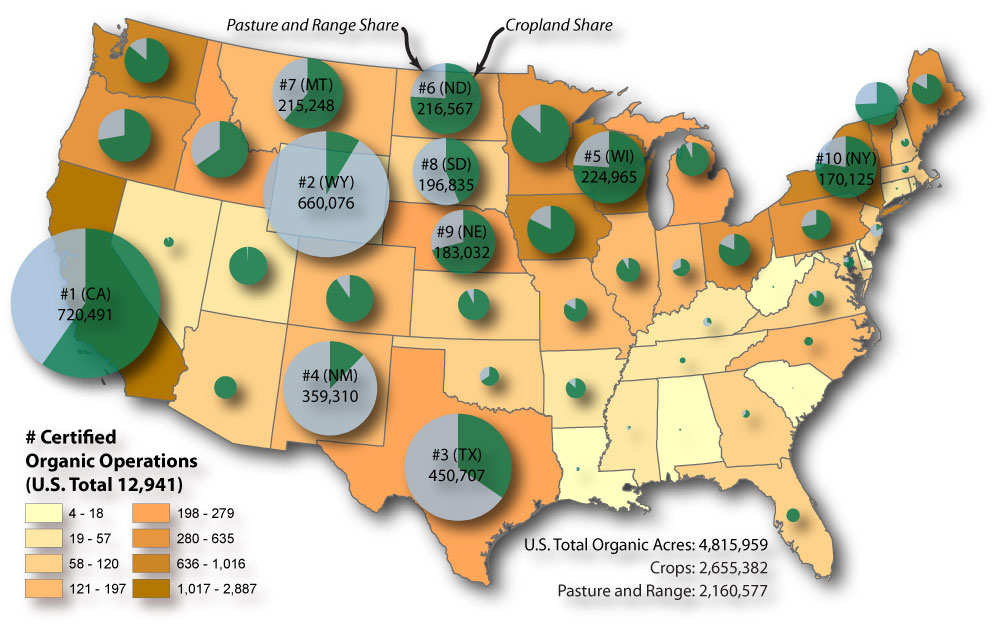

We hypothesize for field crop producers in the United States that the widespread use of genetically modified crops may also play a significant role in dampening the adoption of organic farming systems. U.S. producers dedicated approximately 4.8 million acres of farmland—2.7 million acres of cropland and 2.1 million acres of rangeland and pasture—to organic production systems in 2008. California remains the leading State in certified organic cropland, with over 430,000 acres, over 40% of which is used for fruit and vegetable production. Other top states for certified organic cropland include Wisconsin, North Dakota, Minnesota, and Montana. However, for the crops for which adoption of GE technology is greatest, organic production is low. Only a small percentage of the top U.S. field crops—corn (0.2%), soybeans (0.2%), and wheat (0.7%)—were grown under certified organic farming systems, compared with vegetables (7%) and fruits (3%). U.S. organic soybean acreage has remained relatively flat since the early 2000s despite increasing demand for organic feed grains and consumer products such as soymilk, and U.S. feed grain distributors and soy product manufacturers report sourcing organic soybeans from other countries. Meeting government and private standards for non-GE crops is easier for farmers in many countries outside the United States where adoption of GE crops is low.

Who Pays for Coexistence?

Depending upon the regulatory or technological fix employed, and/or liability assignment, organic producers and consumers and/or GE seed developers and users can end up paying to assure coexistence. In the EU, mandatory labels for GE products shift some of the cost of coexistence to GE product processors and sellers. The European Commission published guidelines for developing national strategies and practices to ensure a fair balance between the interests of GE and non-GE farmers in July 2003, and recently determined that Member States had made significant progress in developing national strategies for coexistence. The coexistence approach in a number of these countries is to require GE producers to use buffers and other prevention strategies and to make them liable for economic damages to non-GE producers. Another coexistence strategy that is being examined in Europe is the use of insurance markets to help compensate for the economic losses experienced by organic and other non-GE producers (Koch).

In the United States, an alternative approach has been used, implicitly allocating risks and costs to non-GE producers. Organic and other non-GE products are labeled, and the non-GE producers assume the full costs and liability of accidental contamination from GE crops. By 2002, 8% of respondents to a national organic producer survey reported having direct costs or damages, such as testing costs and loss of organic sales or markets, related to GE crop production. The open-ended economic risk to non-GE producers from accidental contamination by GE crops may dampen prospects for growth in the domestic organic farm sector, particularly as GE technology spreads to the food crops that dominate the organic sector.

Moving toward a more level playing field for organic and non-GE producers in the United States could involve a mix of strategies. For example, U.S. organic and non-GE producers might continue to incur some of the extra costs associated with GE production, such as the costs of GE testing, but have access to compensation if their crop loses organic or non-GE status, and attendant price premiums, due to GE contamination. Or, the private sector could step in by, for example, stacking a trait for unusual seed color or shape to avoid comingling. A public/private partnership may enhance coexistence and make organic, non-GE and GE production more sustainable in the United States.

Hanson, J., Dismukes, R., Chambers, W., Greene, C. and Kremen, A. (2004). Risk and risk management in organic agriculture: Views of organic farmers. Renewable Agriculture and Food Systems: 19 (4), p. 218-227.

Koch, B. A. (2007). Liability and Compensation Schemes for Damage Resulting from the Presence of Genetically Modified Organisms in Non-GM Crops. European Centre of Tort and Insurance Law, Contract 30-CE-0063869/00-28.

Moschini, G., Bulut, H. and Cembalo, L. (2005) On the Segregation of Genetically Modified, Conventional and Organic Products in European Agriculture: A Multi-market Equilibrium Analysis. Journal of Agricultural Economics, 56 (3) pp 347–372.

Moschini, G. (2008). Biotechnology and the Development of FoodM: Retrospect and Prospects. European Review of Agricultural Economics: 35 (3) pp. 331-355.

Murphy, D. (2007). Plant Breeding and Biotechnology: Social Context and the Future of Agriculture. Cambridge, UK: Cambridge University Press.

Non-GMO project. (2010). Non-GMO project working standard, version 6, June 7, 40 p. Available online: http://www.nongmoproject.org/.

Onyango, B., Nayga, R.M., Jr., and Govindasamy, R. (2006). U.S. Consumers’ Willingness to Pay for Food Labeled ‘Genetically Modified’, Agricultural and Resource Economics Review, 35 (2) pp. 299-310.

On-farm practices:

Product loading and shipment practices:Producer responsibilities:

Driver responsibilities:

|

*OFARM coordinates marketing for member groups:

Buckwheat Growers Association of Minnesota

Kansas Organic Producers Association

Midwest Organic Farmers Co-op

Montana Organic Producers Co-op

NFOrganics

Organic Bean and Grain

Wisconsin Organic Marketing Alliance

The views expressed in this article are the views of the authors and not necessarily the views of the United States Department of Agriculture.