Having done research on various aspects of ethanol production and policy for several years, we decided to take stock of what we have learned so far for this paper. Of course, our research has benefitted from the work of many others, and we will try to capture some of that work as well. An assessment of where we are now is particularly important because so many changes have occurred in agriculture that are affected by ethanol growth and policy. Furthermore, the U.S. ethanol subsidy is set to expire in 2010, so Congressional action will be taken in 2009 to determine what form future U.S. ethanol policy will take. We will group the items under the following general categories: linkages between energy and agriculture, biofuels and commodity prices, policy analysis, the blending wall, cellulosic ethanol issues, and global biofuels impacts. We have done our research using firm level models, as well as partial and general equilibrium analysis.

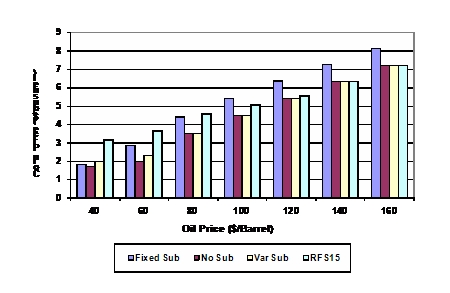

Historically, the correlation between energy product and agricultural product prices has been quite low (Tyner and Taheripour, 2008a and 2008b). The forces determining crude oil and other energy product prices have largely been different from those determining agricultural commodity prices. However, today, with agriculture being called upon to produce not only food, feed, and fiber, but also fuel, that is all changing. We have shown that in the future, corn and crude oil prices can be expected to move together. Previously, we demonstrated that with break–even analysis at the firm level (Tyner and Taheripour, 2008c), and more recently with partial equilibrium analysis (Tyner and Taheripour, 2008a and 2008b). The Iowa State group among others reach similar conclusions (Elobeid et al., 2007; Tolgoz et al., 2007; McPhail and Babcock, 2008a and 2008b). Figure 1 illustrates the combination of corn and crude oil prices which maintain the U.S. ethanol industry at the break–even condition under alternative policy options. Policy options in this figure are: 45 cent fixed subsidy effective January 2009 (Fixed Sub); no ethanol subsidy (No Sub), a subsidy which varies with the price of curde oil (Var Sub), and the 15 billion gallon ethanol Renewable Fuel Standard (RFS) (U.S. Congress, 2007). The fixed blender’s credit was changed in the 2008 Farm Bill (U.S. Congress, 2008) from 51 to 45 cents for corn ethanol. In addition, for cellulosic ethanol, there is now an additional production tax credit of 46 cents, a small producer credit of 10 cents and the standard blender’s credit of 45 cents bringing the total cellulose credit to $1.01.

Figure 1 shows that the crude and corn prices move up together under all alternative policy options. We have called this a revolution in American and global agriculture. Since ethanol is a near perfect substitute for gasoline, higher gasoline price means more demand for ethanol and induces investment in ethanol plants. More ethanol plants and production means more demand for corn, which, in turn, means higher corn prices. The same is true going in the downward direction. If oil price were to fall, less ethanol would be demanded, corn would be freed up for other uses, and corn price would fall.

There is no doubt that ethanol production in the United States has contributed to higher corn prices. A large portion of the growth in corn demand is associated with growth in ethanol production. In the European Union (EU), the same is true for biodiesel and vegetable oils. Between 2004 and earlier in 2008, crude oil went from $40 to $120. Over that same time period, corn went from about $2 to about $6. With the results from our prior work (Tyner and Taheripour, 2008a, 2008b, and 2008c) one can partition the $4 corn price increase into two parts: price increase due to the U.S. ethanol subsidy and price increase due to the demand pull of higher crude oil price. The result is that about $1 of the increase is due to the US subsidy and $3 to the crude oil price increase. The crude oil price increased due to many factors such as higher demand for crude oil, devaluation of the U.S. dollar, political instability in the Middle East, and many other factors. So the crude oil price is the major driver in corn price increases, and the U.S. ethanol subsidy less so. Of course that was not the case before the surge in crude oil prices. Prior to 2005, the ethanol industry would not have existed without the subsidy. In our earlier work (Tyner and Taheripour, 2007), we estimated that with corn around $2 and no subsidy, $60 oil would be required for profitable ethanol production. Oil did not reach $60 until 2006, so the whole development of the ethanol industry was enabled by the subsidy. Today, the oil price is the larger driver.

In addition to the subsidy, the United States has other policies in effect as well—a renewable fuel standard (RFS) and a tariff on imported ethanol. The RFS (U.S. Congress, 2007) has to date not been binding; that is, the market plus the subsidy have always produced a higher amount than the level of the RFS. Our analysis indicates that if oil stays above $120, the mandate will not become binding under normal circumstances. The market would produce more than the amount dictated by the mandate. Of course, if weather events such as the 2008 flood occurred, the mandate could become binding in any given year. However, the EPA administrator has authority to waive or reduce the RFS under that type of circumstance. The major qualification to this conclusion would be a continuation of very high corn production input prices such that the market would be unwilling to produce enough corn to meet the ethanol, food, feed, and export demands without substantially higher corn prices. Under that condition, especially if oil prices were relatively lower, ethanol plants would bring production down to the mandate level, and the mandate would become binding.

Another U.S. policy is the import tariff. The import tariff originally was established to offset the U.S. ethanol subsidy, which applies to both domestic and imported ethanol. Clearly, Congress wanted to subsidize domestic but not imported ethanol, so the tariff accomplished that objective. Early on, the specific tariff was equal to the domestic subsidy of 54 cents per gallon. However, since then the subsidy was reduced to 51 cents and will be reduced again in January 2009 to 45 cents per gallon. In addition to the specific tariff of 54 cents per gallon, there is also an ad valorem tariff of 2.5%. The total tariff today for an import price of $2/gal. is 59 cents/gal., quite a bit more than the 45 cent U.S. subsidy. Brazilian sugarcane based ethanol is much cheaper to produce than U.S. corn ethanol, especially at today’s corn prices. Three years ago, Brazilian ethanol was in the range of $1.10–$1.20, but with depreciation of the U.S. dollar, it is now about $1.70 even though the Brazilian domestic cost has changed little. Adding transport cost and the tariff to that cost figure makes Brazilian ethanol not generally competitive in the U.S. market today. Imports in 2008 to date are far below the 2006 level. However, if the tariff were reduced significantly or eliminated, there could be substantial imports of Brazilian and Central American ethanol. If that were to happen, it would likely reduce pressure on corn prices. Thus, the import tariff is an important policy instrument.

The blending wall refers to the maximum amount of ethanol that could be blended at the current national blending level of 10%. Since we consume about 140 billion gallons of gasoline annually, the theoretical maximum amount of ethanol that could be blended as E10 is 14 billion gallons. The practical limit, at least in the near term, is more like 12 billion gallons (Tyner, Dooley, Hurt, and Quear, 2008). We already have in place or under construction 13 billion gallons of ethanol capacity. At present E85 is tiny, and it would take quite a while to build that market. There are only about 1,700 E85 pumps in the nation and few of the flex–fuel vehicles that are required to consume the fuel. We would need a massive investment to make E85 pumps readily available for all consumers, and a huge switch to flex–fuel vehicle manufacture and sale to grow this market. Without strong government intervention, it will not happen.

What options exist? The most popular among the ethanol industry is switching to E15 or E20 instead of E10. The major problem is that automobile manufacturers believe the existing fleet is not suitable for anything over E10. Switching to a higher blend would void warranties on the existing fleet and potentially pose problems for older vehicles not under warranty. In the United States, the automobile fleet turns over in about 14 years, so it is a long term process. We could not add yet another pump for E15 or E20. The costs would be huge. So the blending wall in the near term is an effective barrier to growth of the ethanol industry. Without a breakthrough (such as cost effective butanol production), the EPA administrator will be forced to cap the RFS far below the planned levels—to the levels that can be blended at E10 plus whatever can be sold as E85.

Cellulosic ethanol development is fraught with risks. There are at least four categories of risks: oil price uncertainty, technological uncertainty, RFS implementation uncertainty, and raw material supply and contracting uncertainty. A 100 million gallon cellulosic ethanol plant is expected to have a capital cost of at least $400 million at current prices. It is unlikely investment will occur without policies aimed at addressing these uncertainties. We will discuss each in turn.

Cellulosic ethanol is likely to be economic at oil prices of $140 and higher. However, there is absolutely no assurance oil price will remain that high. Indeed, at this writing it is substantially below that level. A policy, such as a variable subsidy, could help alleviate the oil price uncertainty risk. Investment is unlikely without some change in policy. There are no commercial ethanol plants today. The increase in the cellulose subsidy described above is set to expire in 2012, before cellulosic production will occur, so it will not provide an incentive to invest unless promptly extended. Many companies and universities are doing path–breaking work to develop viable technologies. However, moving from laboratory or even demonstration scale to commercial scale is quite a leap. It is difficult for government policy options to provide protection against technical risk. Over time, the market will accomplish that with firms which are able to produce economically being the survivors.

The third risk is RFS implementation. Each year, EPA in consultation with DOE and USDA must decide the level of the RFS for the next year for cellulosic ethanol (and the other categories included in the RFS). It is unclear how this will be done. Given the rules of the RFS, it appears if the level is set high enough to absorb all cellulosic ethanol produced, the firms would be able to market the ethanol at a price a bit higher than energy equivalent gasoline, but not substantially higher. There is an option for blenders to pay 25 cents per gallon for a Renewable Fuel Identification Number (RIN) in lieu of actually blending the fuel. Again, it is not clear how this will be implemented. The bottom line is that there is considerable policy uncertainty, and that uncertainty also will impede investment.

Finally, there will be difficulties securing raw material supply. It is likely that potential cellulosic investors will want to be assured raw material supply before sinking steel and laying concrete. Cellulosic ethanol plants will have to source locally, unlike corn ethanol plants. Two potential sources are corn stover and switchgrass. They are quite different in many ways. First, according to our analysis (Brechbill and Tyner, 2008) corn stover is substantially cheaper that switchgrass. It costs about $40 per dry ton compared with $60 for switchgrass. This cost includes fertilizer replacement but does not place a value on soil carbon reduction. The literature on this topic is not consistent, but our reading is that most scientists who have worked on the issue conclude that one–third to one–half of the residue could be removed without subsequent adverse yield effects (Barber, 1979; Benoit and Lindstrom, 1987; Karlen, Hurt, and Campbell, 1984; Linden, Clapp and Dowby, 2000; and Lindstrom, 1986). Second, corn stover and other residues or waste products clearly and unequivocally reduce GHG emissions (because there is little or no direct or indirect land use change). It might be argued that the additional revenue stream from corn stover would induce more corn planting. There might be a very small effect, but we argue that the incremental net revenue would not be sufficient to cause a significant area shift.

Third, corn (and thus corn stover) is an annual crop, whereas switchgrass and similar crops are perennials, meaning in this case that they are planted and harvested over a period of about 10 years. Ethanol plants will want to contract with farmers for supply of raw materials. It should be easier to come up with contracting and risk sharing mechanisms for corn stover than for a crop like switchgrass that will require long–term contracts. This will be new territory for farmers and ethanol producers alike. And unlike corn ethanol, all the raw material must be sourced locally—normally within 50 miles of the plant. Therefore, we must develop new contracting and risk sharing mechanisms to protect both farmers and ethanol producers.

The 2008 Farm Bill contains a provision providing incentives for farmers to plant and grow cellulosic feedstock. It is sort of a plant it, and they will come provision. In our view, it is ill–conceived in that it will not ensure the supply for a plant. The only way dedicated cellulose crops will get off the ground is if adequate private contracting mechanisms are developed. The University of Tennessee is doing good work on this issue.

We will need to deal with all these issues to successfully launch a cellulose ethanol industry. In terms of policy, perhaps a variable subsidy would be first choice since that is the main mechanism for reducing oil price risk at low cost. Extension services might be used to help bring farmers and ethanol producers together to hammer out acceptable contract terms for raw material supply. Consideration might be given to providing better information on RFS implementation for cellulosic ethanol to help reduce the government policy uncertainty.

Many countries have announced and implemented plans and programs to increase production and use of biofuels renewable energy. In both the United States and the EU programs are already in effect that either require or provide incentives for significant production of bioenergy. China, India, Indonesia, and Malaysia, among others, also have announced and implemented biofuels initiatives. More than 13 billion gallons of bio–ethanol and about 2 billion gallons of biodiesel were produced globally in 2007. The ethanol production is driven by a combination of high oil prices and government support. Biodiesel production is driven mainly by government support, as it is further from being economic without policy support (OECD, 2008).

This large–scale global implementation of bioenergy production causes global economic, environmental, and social consequences. It can affect the global economy in several ways. In addition, it induces major land use changes across the whole globe which may lead to significant environmental impacts. To assess the global impacts of biofuel production, a computational general equilibrium (CGE) framework has been developed. This framework builds upon the standard Global Trade Analysis Project (GTAP) database and modeling framework and modifies it in several ways. Three types of biofuels (ethanol from sugarcane, ethanol from crops, and biodiesel from oilseed) and their byproducts - distillers dried grains with soluble (DDGS) and biodiesel byproducts (BDBP) - are explicitly introduced into the standard GTAP model. The new framework has been used in several research activities to examine global impacts of biofuel production. In this short paper we address some key findings of these research activities. In particular, we report some results from Hertel, Tyner, and Birur (2008), and Taheripour et al. (2008).

Hertel, Tyner, and Birur (2008) have examined the implications of U.S. and EU biofuel mandate policies for the world economy during the time period of 2006–2015. According to this paper, biofuel mandates sharply increase the production of coarse grains (mainly corn) in the United States and production of oilseeds in the United States, EU and Brazil. The United States and EU would use a large portion of their corn and oilseed outputs to meet their biofuel mandates for 2015. In the United States, the share of corn used in ethanol production could increase from 12.7% in 2006 to 29.9% in 2015, while the share of oilseeds going to biodiesel in the EU could increase from 23.3% in 2006 to 69.2% in 2015. The United States and EU mandates policies interact, and the most dramatic interaction between these policies is for the U.S. oilseed production. While, the U.S. mandates alone would reduce U.S. oilseed production, the combination of both the U.S. and EU mandates would increase oilseed production in the United States. In general, about one–third of the growth in the U.S. crop cover is attributed to the EU mandates. The U.S.–EU mandates affect the rest of the world as well. The combined policies have a much greater impact than just the United States or just the EU policies alone, with crop cover rising sharply in Latin America, Africa and Oceania as a result of the combined U.S.– EU biofuel mandates. These increases in crop cover come at the expense of pasture (first and foremost) as well as commercial forest.

Taheripour et al. (2008) have revealed the importance of incorporating biofuel byproducts into the economic analysis of biofuels policies. The model with byproducts reveals that production of DDGS and BDBP would grow sharply in the United States and EU. For example, the U.S. production of DDGS would grow from 12.5 million metric tons in 2006 to 34 million metric tons in 2015. A major portion of this byproduct would be used within the United States, and the rest would be exported to other regions such as Canada, the EU, Mexico, China, Africa and Asia.. On the other hand, the EU production of BDBP would grow from about 6.1 million metric tons in 2006 to 32.5 million metric tons in 2015. The EU production of BDBP would be mainly used within the region.

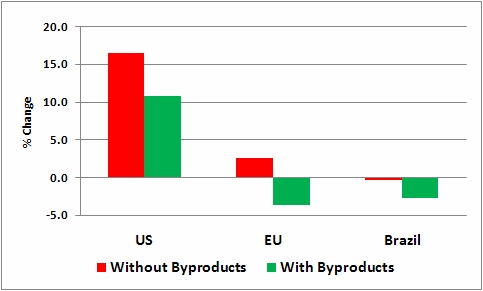

The CGE models with and without byproducts tell quite different stories regarding the economic impacts of the United States and EU biofuel mandates for the world economy in 2015. While both models demonstrate significant changes in the agricultural production pattern across the world, the model with byproducts shows smaller changes in the production of cereal grains and larger changes for oilseeds products in the United States and EU, and the reverse for Brazil. For example, as shown in Figure 2, the U.S. production of cereal grains increases by 10.8% and 16.4% with and without byproducts, respectively. The difference between these two numbers corresponds to 646 million bushels of corn which could be used to produce about 1.7 billion gallons of ethanol. This is really a big number to ignore and disregard in the economic analyses of biofuel production.

With byproducts included in the model, prices change less due to the mandate policies. For example, the model with no byproducts predicts that the price of cereal grains grows 22.7% in the United States during the time period of 2006 to 2015. The corresponding number for the model with byproducts is 14%. Introducing byproducts into the model alters the trade effects of the U.S.–EU mandate policies as well. For example, the model with no byproducts estimates that the U.S. exports of coarse grains to the EU, Brazil, and the Latin American region would drop sharply by –4.8%, –25.5%, and –12.7%, respectively. The corresponding figures for the model with byproducts are –2.1%, –15.7%, and –7.9%.

We have learned a lot in the economic analysis done to date, but there is much more work needed. Our next step is to improve the data and models such that we will be able to estimate global land use changes induced by national biofuels programs. Land use changes are important in estimating greenhouse gas emissions changes associated with biofuels.

Barber, S.A. (1979). Corn Residue Management and Soil Organic Matter. Agronomy Journal 71 (1979): 625–627.

Benoit, G.R. & Lindstrom, M.J. (1987). Interpreting Tillage–Residue Management Effects. Journal of Soil and Water Conservation March–April (1987): 87–90.

Brechbill, S. & Tyner, W. (2008). The Economics of Renewable Energy: Corn Stover and Switchgrass. Department of Agricultural Economics, Purdue University.

Elobeid, A., Tokgoz, S., Hayes, D.J., Babcock, B.A., & Hart, C.E. (2007). The Long–Run Impact of Corn–Based Ethanol on the Grain, Oilseed, and Livestock Sectors with Implications for Biotech Crops. AgBioForum, 10(1): 11–18.

Hertel, T., Tyner, W., & Birur, D. 2008. Biofuels for all? Understanding the Global Impacts of Multinational Mandates. GTAP Working Paper No. 51, Center for Global Trade Analysis, Department of Agricultural Economics, Purdue University.

Karlen, D.L., Hunt, P.G. & Campbell, R.B.. (1984). Crop Residue Removal Effects on Corn Yield and Fertility of a Norfolk Sandy Loam. Soil Science Society of America Journal 48 : 868–872.

Linden, D.R., Clapp, C.E., & Dowdy, R.H. (2000). Long–Term Corn Grain and Stover Yields as a Function of Tillage and Residue Removal in East Central Minnesota. Soil and Tillage Research 56, no. 3–4 : 167–174.

Lindstrom, L.J. (1986). Effects of Residue Harvesting on Water Runoff, Soil Erosion and Nutrient Loss. Agriculture, Ecosystems and Environment 16: 103–112.

McPhail, L.L. & Babcock, B.A. (2008a). Short–Run Price and Welfare Impacts of Federal Ethanol Policies. Staff General Research Papers 12943, Iowa State University, Department of Economics.

McPhail, L.L. & Babcock B.A. (2008b). Ethanol, Mandates, and Drought: Insights from a Stochastic Equilibrium Model of the U.S. Corn Market. Staff General Research Papers 12878, Iowa State University, Department of Economics.

Organization for Economic Cooperation and Development (OECD). (2008). Economic Assessment of Biofuel Support Policies (http://www.oecd.org/dataoecd/19/62/41007840.pdf).

Taheripour, F., Hertel, T., Tyner, W., Beckman, J., and Dileep, K. 2008. Biofuels and their By–Products: Global Economic and Environmental Implications. Presented at the 11th GTAP Conference, June 12–14 2008, Helsinki, Finland and at the 2008 American Agricultural Economics Association meeting in Orlando Florida.

Tokgoz, S., Elobeid, A., Fabiosa, J., Hayes, D., Babcock, B., Yu, T–H., Dong, F., Hart, C.E., Beghin, J.C. 2007. Emerging Biofuels: Outlook of Effects on U.S. Grain, Oilseed and Livestock Markets. Staff report 07–SR 101 Iowa State University (www.card.iastate.edu)

Tyner, W., Dooley, F., Hurt, C., and Quear, J. (2008). Ethanol Pricing Issues for 2008. Industrial Fuels and Power: 50–57.

Tyner, W. & Taheripour, F. (2008a). Policy Options for Integrated Energy and Agricultural Markets. Presented at the Allied Social Science Association meeting in New Orleans, January 2007, and published in the Review of Agricultural Economics, Vol. 30 No.3.

Tyner, W. & Taheripour, F. (2008b). Policy Analysis for Integrated Energy and Agricultural Markets in a Partial Equilibrium Framework. Paper Presented at the Transition to a Bio–Economy: Integration of Agricultural and Energy Systems conference on February 12–13, 2008 at the Westin Atlanta Airport planned by the Farm Foundation.

Tyner, W. & Taheripour, F. (2008c). Future Biofuels Policy Alternatives. In Joe Outlaw, James Duffield, and Ernstes (eds), Biofuel, Food & Feed Tradeoffs, Proceeding of a conference held by the Farm Foundation/USDA, at St. Louis, Missouri, April 12–13 2007, Farm Foundation, Oak Brook, IL, 2008, 10–18.

Tyner, W. & Taheripour, F. (2007). Renewable Energy Policy Alternatives for the Future. American Journal of Agricultural Economics, 89(5): 1303–1310.

University of Tennessee Institute of Agriculture. Guideline Switchgrass Establishment and Annual Production Budgets Over Three, Six, and Ten Year Planning Horizons. October 2007.

U.S. Congress (2007). Energy Independence and Security Act of 2007. H.R. 6, 110 Congress, 1st session.

U.S. Congress (2008). 2008 Farm Bill. H. R. 6124 (P.L. 110–246).