A strong view has emerged this past year from many farm groups that crop insurance should play a pivotal role in the 2012 Farm Bill and beyond. Meanwhile, some have questioned the near-consensus support for crop insurance. This article addresses why crop insurance has taken on a primary position among farm support programs and examines alternative paths that crop insurance could take in the future, including some ways it could assume an even larger role.

The use of crop insurance by U.S. farmers has grown sharply, increasing from 45 million insured acres in 1981 to 262 million in 2011 (Figure 1). Insured liability shows a sharper increase, rising from $6 billion in 1981 to more than $113 billion in 2011. More acreage, higher crop prices, and increased coverage levels explain the dramatic rise in liability.

Several factors explain greater use of crop insurance by farmers.Today’s insurance program structure began with the Federal Crop Insurance Act of 1980, which required crop insurance to be sold and serviced by the private sector. With private sector compensation based on the volume of premium sold, companies and agents had a strong incentive to bring crop insurance to producers. Increases in premium subsidies and government payment of insurance company delivery costs made crop insurance increasingly affordable over time, boosting participation and coverage levels.

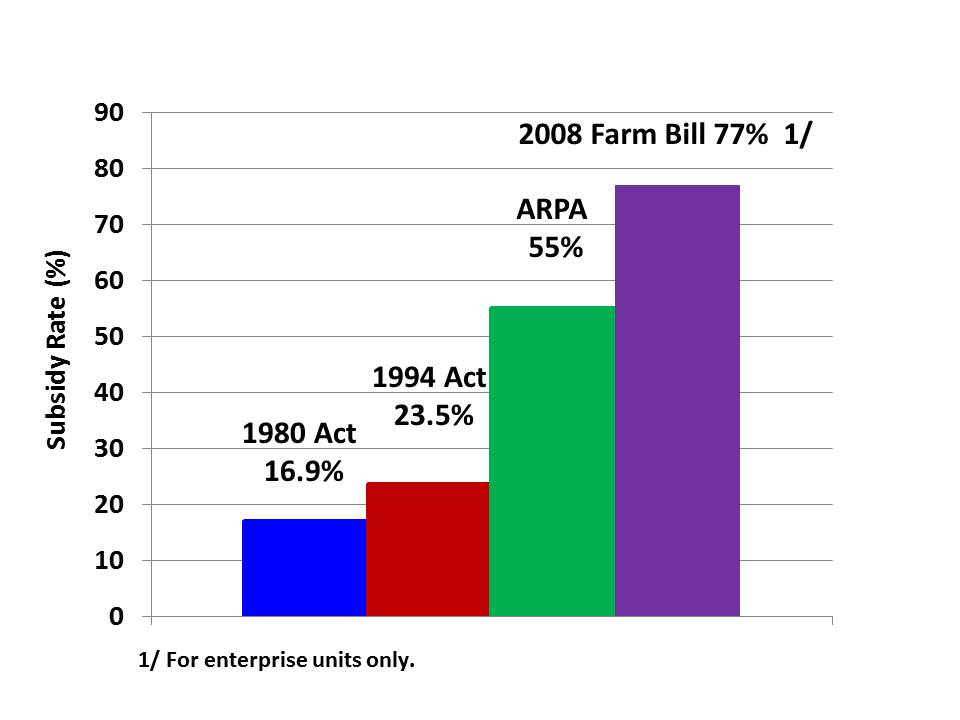

Figure 2 illustrates the share of premium subsidized by the Federal government for an individual policy at the 75% coverage level. The 1980 Act set the premium subsidy at 16.9% for a policy with 75% coverage. Despite the subsidy, demand remained limited by reliance on other programs such as ad hoc disaster assistance, target price coverage, and commodity loan programs. The subsidy rate was increased slightly by the Federal Crop Insurance Act of 1994. Temporary economic loss assistance in the late 1990s provided a premium discount, which continued until a permanent increase was provided in the Agricultural Risk Protection Act of 2002 (ARPA). ARPA raised subsidies, particularly at the higher coverage levels, with the 75% coverage level subsidy more than doubling. The 2008 Farm Bill did not change subsidy rates for individual insurance plans but increased subsidy rates for enterprise and whole farm units to 77% for a policy with 75% coverage on an enterprise unit.

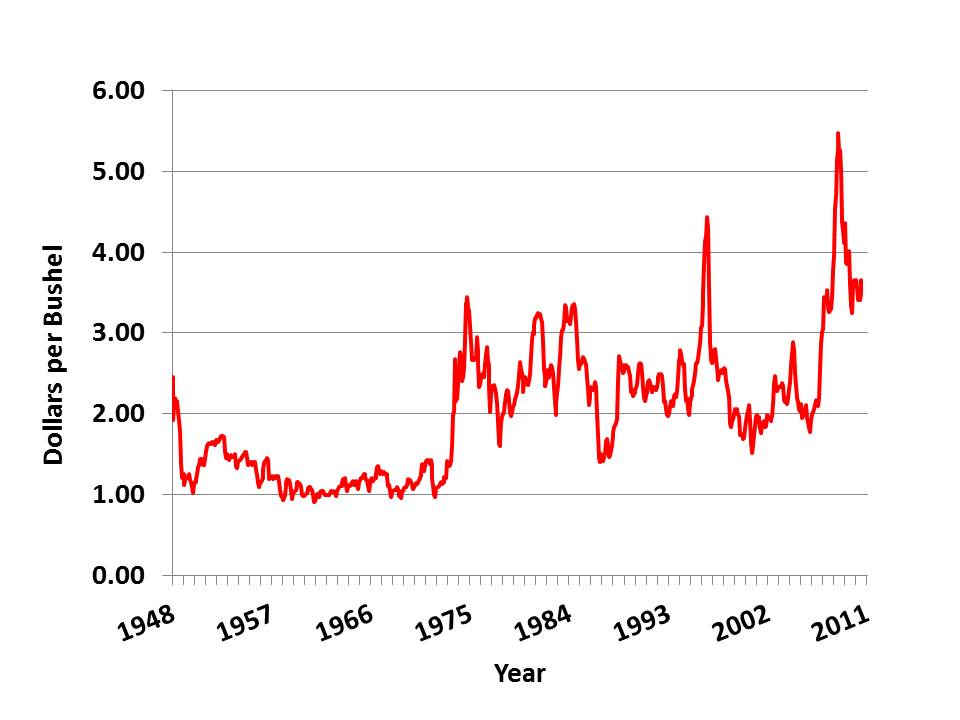

Other factors also contributed to higher demand for coverage. The Federal Crop Insurance Reform Act of 1994 required producers to have crop insurance to be eligible for farm program benefits. While short lived, this requirement introduced many producers to crop insurance. Reductions in the level of protection provided by farm programs and requirements to have crop insurance in order to be eligible for the receipt of ad hoc disaster payments encouraged participation and higher coverage levels. Greater volatility in commodity markets (Figure 3) and efforts to acquaint producers with risk management strategies may have also increased insurance demand. Program improvements have attracted additional producer participation. These improvements, introduced during the late 1990’s, included more appropriate premium rates for some crops; reduction of waste, fraud, and abuse; and new and better plans of insurance, such as revenue plans.

Farm programs have evolved from very market intervening programs to those that let market forces operate more fully, with producers shouldering greater responsibility to manage risks. In line with this evolution, the crop insurance program has a number of appealing features (NCIS, 2011). A producer must consciously elect to manage risks, can design a program to fit individual farm risks, and must share in the program cost, reducing public costs and aiding accountability.

The private sector delivers the crop insurance program as part of a public and private partnership, providing producer choice, and promoting competition in service quality and efficiency and effectiveness in delivery. Through the private sector, producer losses are adjusted and indemnities paid promptly. Congress has enabled the program to largely govern itself—with the USDA responsible for setting premium rates, underwriting and loss adjustment standards, and enforcing compliance. Thus many program provisions can be quickly changed to correct program parameters and reduce costs and inefficiencies. Premium rate changes and a reduction in payments to companies negotiated in the 2011 Standard Reinsurance Agreement (SRA) are examples of such discretionary actions. Little found that the program operates with fraud and abuse levels far below other lines of property and casualty insurance (Review of the Integrity and Efficacy of the Federal Crop Insurance Program, 2007). Crop insurance also allows many producers to secure credit, as an insurance policy serves as collateral, and aids forward marketing by providing resources to meet delivery obligations in the event of a production loss.

While the aforementioned factors help explain the program’s attraction, there are concerns. U.S. loss ratios —indemnities divided by premiums—have been well below the statutory maximum of 1.0 for many years and vary sharply among regions, raising questions about whether the rating system suitably accounts for program improvements over time, changing production technology, and the probabilities of catastrophes. A premium rate review was conducted by the Risk Management Agency (RMA) in 2010 and a major revision in rating methods is now being implemented. Recently, low losses and high crop prices have resulted in higher-than-expected company underwriting gains and delivery payments. Although some argue they remain excessive, the 2011 SRA and the recent rating changes have reduced the expected value of private insurance company underwriting gains and delivery payments, and the long-term average net income of crop insurance companies remains below that in the overall property and casualty industry (Grant Thornton, LLP, 2011). Many producers are concerned that crop insurance yields lag expected yields or reduce coverage after successive years of yield shortfalls, as required by most crop insurance plans. An adjustment to reflect yield trends, recently approved for sale for 2012, may partly address this issue. Another concern is whether the portfolio of insurance plans can be improved for small producers, socially disadvantaged producers, specialty crops and other crops that may not be covered or have atypical or specific risks or lack transparent pricing.

While there now appears to be much agreement that crop insurance will continue to be the primary program in the future farm safety net, there are alternative views on how to address program concerns and how crop insurance should evolve, including the extent to which it should be integrated with existing or new farm programs. These approaches are summarized next.

I—Reduce or Eliminate Subsidies. Reflecting higher participation, coverage levels, and commodity prices, the expected public cost of the program is now about $8 billion per year, raising criticism of underwriting gains, delivery costs, and premium subsidies—the components of program costs (Babcock, 2011; Smith, 2011). While the 2011 SRA and recent premium rate reductions at least partly address the first two cost components, premium subsidy rates are set in statute. One option to cut costs is to retain the current program structure but reduce premium subsidies. Premium subsidies are a fixed percentage of premiums which makes the dollar value of subsidies higher for higher risk producers of a particular crop, other things equal. High subsidy levels may encourage the purchase of insurance for the purpose of earning a return, rather than just protecting against a risky outcome. Record-high farm income and the need to cut Federal spending motivate suggestions to cut or end subsidies.

One suggestion, around for a while, has been to distribute limited premium subsidies through vouchers (for example, Glauber, 2004). Another idea would simply cap subsidies per farm (Smith, 2011) or impose eligibility criteria on subsidies. Another approach is to reduce subsidies for certain plans of insurance, such as charging premium rates for Catastrophic Coverage (CAT) rather than the current administrative fee or eliminating subsidies for the price component of revenue policies (Babcock, 2011). Other ideas include further reducing payments to companies. Proponents of lower subsidies argue such changes would help meet World Trade Organization (WTO) obligations, reduce the deficit, improve market orientation, and better reflect farm household well-being relative to nonfarm households.

The downside of reducing or ending crop insurance subsidies would be a likely reduction in participation and coverage levels, depending on the type of changes made to the program. Lower coverage levels would expose producers to more price, yield, and quality risk and could encourage the government to provide ad hoc payments in the event of a widespread declared disaster. Sharp cuts in premium subsidies, delivery cost payments to companies, and Federal reinsurance would likely generate significant opposition from producers, companies, and farm suppliers. For example, loss of subsidies for price protection in revenue insurance would likely limit producers’ ability to forward market, adding to risk exposure. In the extreme, with full privatization of the program, including loss of Federal reinsurance, premium rates would rise sharply and would have to include a delivery cost load, leading to much smaller sales and a contraction in delivery infrastructure with fewer companies and agents. Companies would no longer be required to sell to all farmers who want a policy, and in some cases, coverage may not even be offered to some producers and some areas. A possible response to avoid such outcomes could be a push for a Federal program, such as described in the next two sections. However, creating a free Federal program to substitute for crop insurance is simply a continuation of subsidies, but in a different form.

II—Wrap individual crop insurance around index plans of insurance. One idea is to provide a base level of coverage to program crop producers in the form of a free Federal area or another type of index plan of protection, with privately delivered insurance purchased by producers to cover added individual risks (Coble and Barnett, 2008; Babcock, 2010; Smith, 2011; Zulauf, 2011a). This wrapped, privately delivered insurance may be subsidized or not. The idea is that an index plan, based on area yields, revenues, vegetation conditions, or weather variables, would have low administrative costs and limited moral hazard—actions by the producer that increase the likelihood and severity of a loss. Such index plans are not currently integrated with individual plans, but could be integrated. For example, a Federal area revenue program that covers all area losses in excess of 15% could be provided free to cover more widespread correlated risks, with private insurance companies being left on their own to sell policies to cover other farm risks. Another approach would be to use payments made under a Federal index plan to offset indemnities paid under the current individual crop insurance policies, thus reducing crop insurance net indemnities. This concept was most recently proposed by the American Farm Bureau Federation (2011). Such options reduce program duplication, crop insurance program costs, and premium rates. Also, an index plan requiring a 30% loss to trigger a payment could potentially be exempt from penalties under the WTO.

The downside of wrapped approaches is that index plans work better the more highly related the producer’s loss is with the index’s loss. This means to be effective the index insurance would have to apply on a more local scale like the county or another small geographic area, which increases program cost and complexity.

Individual insurance does a better job of protecting against risk than index plans and is preferred by most producers (Bulut, Collins, and Zacharias, 2011). Index plans are unlikely to be effective for producers in regions that are very heterogeneous in terms of topography, climate, soil type, etc. Another issue is that, depending on the structure of the product, the index plan may just substitute for production or revenue currently covered by crop insurance, adding little to the overall risk reduction of the farm, although lower premium rates may encourage participation and higher coverage levels on individual policies. Greater reliance on crop insurance wrapped around index products that substitute for some of the risk protection now provided by crop insurance would likely require a rerating and a new SRA. Crop insurance companies would likely bear less risk and provide less risk protection, as Federal assumption of risk increased, with the likely effect of a smaller private crop insurance industry over time.

III—Expand farm programs to cover uninsured production and possibly enhance income. Some proposals maintain crop insurance as is, but supplement its coverage with free farm programs to reduce uninsured losses which occur due to the policy’s deductible and farm insurance yields being below expected yields. The Average Crop Revenue Election (ACRE) and the Supplemental Revenue Assistance Payments (SURE) programs are examples. The now-expired SURE program raised coverage levels of the underlying policies on an individual whole-farm basis and subtracted indemnities from SURE payments. The ACRE program tries to effectively raise a producer’s coverage levels using an area revenue guarantee of 90% of expected state revenue. Indemnities are not subtracted from the ACRE payment, but a maximum ACRE payment rate of 25% of the state revenue guarantee reduces the overlap with crop insurance indemnities (Zulauf, Schnitkey and Langemeier, 2010).

A range of farm revenue programs that would supplement crop insurance proposals have been discussed for the 2012 Farm Bill (for example, Zulauf, 2011b). They would essentially replace ACRE and include area plans with guarantees as high as 95% of revenue but with a maximum payment rate as low as 10% of the guarantee to better target the deductible on most insurance policies and limit overlap with crop insurance. There are also plans based on individual farm losses. Overall risk protection would be increased as the plans supplement crop insurance. Multiyear protection and enhanced farm income are provided when the price component of the guarantee is set to exceed expected prices in low price years.

These supplemental plans have several disadvantages. Guarantees set at high levels to supplement crop insurance rather than replace it may generate WTO issues, encourage more risk taking and production, and thus impede production response in excess supply periods. This may be especially true for individual farm plans, which also have moral hazard. The area plans suffer from basis risk, or imperfect correlation between farm and area yields, potentially paying when a farm has little to no loss and not paying when a farm has a loss. Also, the more the supplemental coverage band overlaps higher levels of crop insurance coverage, the more the supplemental plan will reduce crop insurance demand at the higher coverage levels.

IV—Expand crop insurance to cover uninsured production and possibly enhance income. Another approach is to have no supplementary free farm programs and rely on the delivery assets and benefits of the crop insurance program. Unlike the supplemental farm program plans, crop insurance covers far more crops. As the sole program, there may be interest in expanding crop insurance features to address currently uninsured production for all crops, with coverage enhancements subsidized at alternative levels. Subsidies on existing underlying policies could be retained or reduced as budget and policy objectives require. A number of the following options could be used.

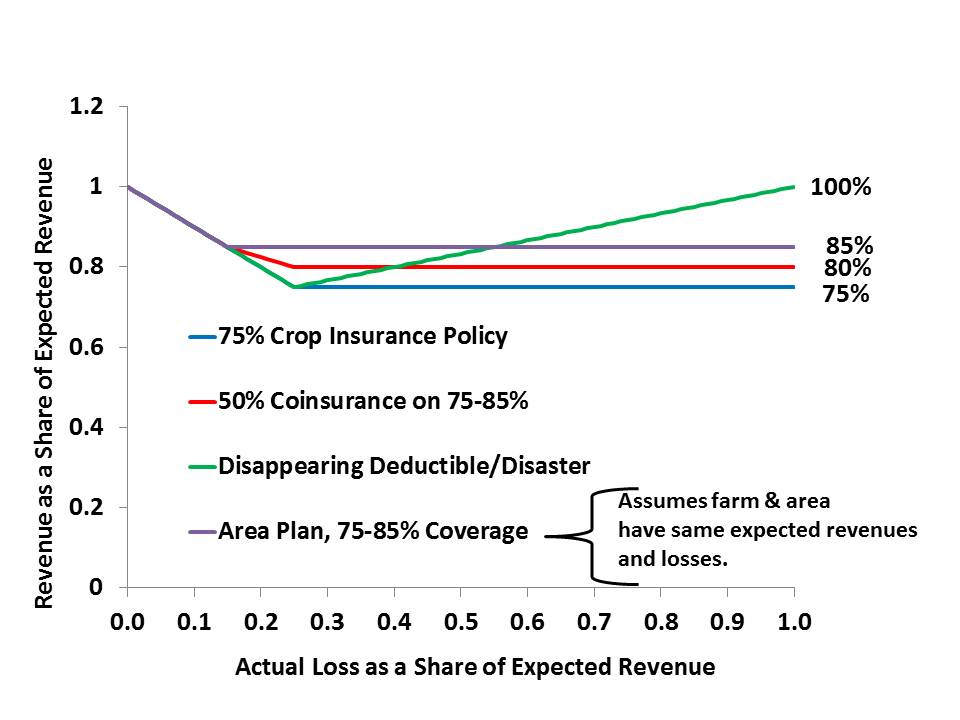

Figure 4 illustrates how coinsurance, a supplemental crop insurance area plan, disappearing deductible, and a disaster payment might work to augment income with a 75% crop insurance policy. The line for the supplemental disaster payment assumes a 33% payment rate so it is coincident with the disappearing deductible. The area plan line depends on how the producer’s loss compares with the area’s loss. As drawn, the area plan covers 75% to 85% of the expected area revenue and is assumed to perfectly supplement the individual plan and provide protection up to 85%—assuming the farm and area have exactly the same expected revenue and losses. In reality, that would be the best case and highly improbable. The other extreme would be that the area plan never triggers when the producer has a loss. In that case the relevant line is the 75% crop insurance policy and the area plan is ineffective, again an improbable case.

As Federal spending on traditional farm programs diminishes while that for crop insurance expands, crop insurance has drawn increasing scrutiny from critics of farm subsidies and those wanting agriculture to contribute to deficit reduction. At the same time, many want to continue or strengthen the current program for its risk management benefits for producers, while still retaining some Federal farm program support. These views have led to different proposals for future farm safety net programs fashioned around risk management objectives. From a crop insurance perspective, these proposals may be viewed as either reducing crop insurance subsidies, substituting a free farm program for part of the risk that crop insurance now covers, augmenting crop insurance with a new free farm program that covers losses crop insurance does not cover, and expanding crop insurance to replace farm programs.

The 2012 Farm Bill proposal of the House and Senate Agriculture Committee chairs, submitted to the Joint Committee on Deficit Reduction in the fall of 2011, incorporated several of the options discussed here, including a supplemental revenue farm program based on individual farm losses and supplemental area revenue plans sold by the crop insurance industry (Stabenow, 2011). While the area plans would likely expand crop insurance coverage, the supplemental individual farm revenue program would likely displace some crop insurance sales at high coverage levels. While the fate of this proposal is unknown, it illustrates key choices that have to be made, including government versus private delivery, government versus private risk bearing, and the extent of deductible, or shallow loss, coverage. Whatever structure emerges, the debate over farm and crop insurance subsidies is likely to continue. With deficit reduction in prospect for years to come and insurance so fundamental to risk management in all economic areas, the long-term most sustainable safety net program for farmers may be enhanced crop insurance—but likely with more restricted subsidization.

American Farm Bureau Federation. (2011). Systemic Risk Reduction Program. Available online: http://www.fb.org/newsroom/nr/nr2011/10-21-11/AFBF_SRRP_Proposal.pdf.

Babcock, B.A. (2010). Costs and Benefits of Moving to a County ACRE Program (CARD Policy Brief 10-PB 2). Ames, Iowa: Iowa State University Center for Agricultural and Rural Development. Available online: http://www.card.iastate.edu/publications/synopsis.aspx?id=1128.

Babcock, A. B. (2011). The Revenue Insurance Boondoggle: A Taxpayer-Paid Windfall for Industry. Washington, DC: Environmental Working Group. Available online: http://static.ewg.org/pdf/Crop_Insurance.pdf.

Barnaby, G.A. (2011). Improved Farm Financial Safety Net Based on Revenue Insurance. Presented at the 2011 Annual Meeting of the Agricultural and Applied Economics Association, Pittsburgh, PA.

Bulut, H., K. Collins, and T. Zacharias. (2011). Optimal Coverage Demand with Individual and Area Plans of Insurance.Presented at the 2011 Annual Meeting of the Agricultural and Applied Economics Association, Pittsburgh, PA.

Coble, K.H. and B.J. Barnett. (2008). Implications of Integrated Commodity Programs and Crop

Insurance. Journal of Agricultural and Applied Economics, 40(2), 431-442.

Glauber, J. W. (2004). Crop Insurance Reconsidered. American Journal of Agricultural Economics, 86(5), 1179-1195.

Grant Thornton, LLP. (2011). Federal Crop Insurance Program, Profitability and Effectiveness Analysis, 2010 Update. Overland Park, KS: National Crop Insurance Services. Available online: http://www.ag-risk.org/NCISPUBS/SpecRPTS/GrantThornton/Grant_Thornton_Report-2010_FINAL.pdf.

Review of the Integrity and Efficacy of the Federal Crop Insurance Program: Hearing before the Subcommittee on General Farm Commodities and Risk Management of the House Committee on Agriculture(Serial 100-25), 110th Cong. 10 (2007) (testimony of Bert Little, Ph.D.).

National Cotton Council. (2011, November 18). NCC Welcomes Farm Bill Proposal [Press release]. Available online: http://www.cotton.org/news/releases/2011/11farmprop.cfm.

National Crop Insurance Services. (2011, February). The Essential Strengths of Crop Insurance. Crop Insurance TODAY, 44(1), 4-6. Available online:http://www.ag-risk.org/NCISPUBS/Today/2011/Today02-11.pdf.

Smith, H.V. (2011). Premium Payments: Why Crop Insurance Costs Too Much. Washington, DC: American Enterprise Institute. Available online: http://www.aei.org/paper/economics/fiscal-policy/federal-budget/premium-payments-why-crop-insurance-costs-too-much/.

Stabenow, D. (2011). Recommendations to the Joint Select Committee on Deficit Reduction. Unpublished manuscript. Washington, DC: U.S. Senate Committee on Agriculture, Nutrition, and Forestry. Available online: http://www.hagstromreport.com/assets/112111_SenAgRecommendations.pdf.

United States Department of Agriculture National Agricultural Statistics Service. (2011). Acreage. Available online: http://usda01.library.cornell.edu/usda/current/Acre/Acre-06-30-2011.pdf.

Zulauf, C. (2011a). A Coordinated Framework for a 21st Century Farm Safety Net. Presented at the 2011 Annual Meeting of the Agricultural and Applied Economics Association, Pittsburgh, PA.

Zulauf, C. (2011b). Assessment and Comparison of Farm Safety Net Proposals.Washington, DC: American Farmland Trust. Available online: http://www.farmland.org/documents/AssessmentandComparisonofFarmSafetyNetProposals.pdf.

Zulauf, C., G. Schnitkey, and M. Langemeier. (2010). Average Crop Revenue Election, Crop Insurance, and Supplemental Revenue Assistance: Interactions and Overlap for Illinois and Kansas Farm Program Crops. Journal of Agricultural and Applied Economics, 42(3), 501-515.