The U.S. fuel ethanol industry has experienced phenomenal growth in recent years, with roughly a 3.6-fold increase in ethanol production since 2005 (RFA, 2012). A fuel blender’s credit (the Volumetric Ethanol Excise Tax Credit), a secondary tariff on imported ethanol, and mandatory use of renewable fuels supported the development of the industry. However, two of these three policy instruments—the federal tax credit and the secondary tariff—were allowed to lapse at the end of 2011. The Renewable Fuels Standard (RFS)—which sets annual mandates for renewable transportation fuels sold in the United States—has been maintained and currently requires 15.2 billion gallons of renewable fuel, an increase of roughly 9% from last year, to be contained in motor vehicle fuels in 2012 (EPA, 2011).

In an earlier assessment of U.S. biofuels policies (Yano, Blandford and Surry, 2010), we argued that the mix of policies did not make economic sense, particularly in terms of their impact on international trade. In this article we examine whether things have changed and focus on the key issue of whether the RFS should continue to be applied.

U.S. demand for ethanol is topping out. Most of the vehicles on the road can use gasoline with a maximum ethanol share of 10% (E10) or 15% (E15). Higher blends may cause damage to the engine and other fuel system components. The use of E15 in cars and pickups built since 2001 was recently approved by the U.S. Environmental Protection Agency (EPA) in order to increase the maximum amount of ethanol consumed domestically. With E10, a maximum of 12.5-13.5 billion gallons of ethanol can be used—this constitutes a so-called “blend wall” (RFA, 2010).

The ethanol industry is pinning its hopes on the rapid adoption of E15 to increase domestic consumption to around 17.5 billion gallons (RFA news release, 2011), which is higher than the amount required under the RFS for 2012—15.2 billion gallons including at least 1 billion gallons of biodiesel. Unfortunately, the EPA decision is unlikely to have much immediate impact on the domestic market for ethanol. To sell E15 alongside E10, the owners of service stations typically have to add additional expensive equipment and may face legal problems if consumers use the wrong fuel in their vehicles (Wisner, 2012). Since the EPA cannot force retailers to sell E15, many may choose not to adopt the product until the fleet becomes dominated by suitable vehicles. Consequently, the use of E15 is expected to spread slowly. This, in combination with the limited prevalence of flex fuel vehicles capable of using higher amounts of ethanol, means that the demand for the product is likely to remain constrained.

A compounding factor is declining gasoline consumption nationwide. As fuel has become more expensive, consumers have been shifting to more energy efficient vehicles (EV) and driving less. Higher Corporate Average Fuel Economy (CAFE) standards—which penalize automakers if new vehicles do not achieve a mandated fleet-wide fuel economy standard—are also stimulating reductions in consumption. If current trends continue, declining demand for blended fuels will reduce the maximum volume of ethanol that can be consumed domestically and further strengthen the effect of the blend wall.

These market trends are a big issue for the ethanol industry. Under the RFS the volume of renewable fuels which must be used is scheduled to increase annually from 15.2 billion gallons in 2012 to 36 billion gallons in 2020. The legislation does not establish a specific mandate for corn-based ethanol—which is classified as “conventional” biofuel; but to meet the nonadvanced portion of the RFS, blenders are likely to use domestic corn-based ethanol and/or imported sugarcane-based ethanol because cheaper alternatives do not exist. Biodiesel—which has a mandate of at least 1 billion gallons (ethanol equivalent volume of 1.5 billion gallons)—qualifies as an advanced biofuel under the RFS and can be used to meet the overall mandate, but to increase consumption beyond 1 billion gallons the United States would need to rely on imports or to use feedstocks other than soybean and develop new biodiesel conversion processes. It is highly likely that mandated increases in the RFS will exceed potential domestic consumption of biofuels, due to weaker fuel demand and the impact of the blend wall. If blenders comply with the RFS, we are likely to see an imbalance in the domestic market with an excess supply of blended fuel.

Accumulated stocks of Renewable Identification Numbers (RINs) can be used to meet part of the RFS for a few years, but this year’s drought is likely to reduce such stocks significantly because the EPA denied requests for waiver of the RFS for 2012-2013 in November 2012 (EPA, 2012). If drought and/or other weather conditions continue to cause lower corn yields, an imbalance in the domestic ethanol market will be more likely to occur.

Traditionally the United States has been a small importer of ethanol mainly from Caribbean countries and Brazil. However, in early 2009 exports surged due to high world sugar prices, which meant tighter global supplies of sugar-based ethanol from Brazil, and the effect of the blend wall in the domestic market. The U.S. industry also benefited from cost reductions in corn ethanol production due to improved technology, and the effect of Federal and state subsidies and import protection through tariffs. Last year U.S. ethanol exports reached 1.19 billion gallons, more than triple the 2010 volume of 396 million gallons.

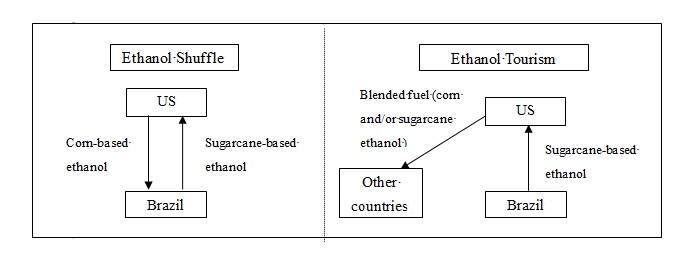

Despite this, the United States still needed to import sugarcane-based ethanol from Brazil to comply with the mandate for what are classified as “advanced biofuels” under the RFS and the California Low Carbon Fuels Standard (LCFS) because cellulosic biofuels that also qualify are not economically viable. Corn-based ethanol could not be used to meet those mandates. So, U.S. fuel blenders had to use expensive Brazilian ethanol, while cheaper corn-based ethanol was being shipped to Brazil and other countries. Vice president of Research and Analysis at the Renewable Fuels Association, Geoff Cooper called this practice the “ethanol shuffle” (Cooper, 2011).

The shuffle demonstrated that the RFS does not make sense economically in the presence of the blend wall. The advanced biofuels mandate, which is part of the overall RFS mandate, and the LCFS increase the amount of corn-based ethanol that needs to be exported when domestic consumption of ethanol is constrained. The EPA and the California Air Resource Board (CARB) argue that producing ethanol from sugarcane results in fewer lifecycle GHG emissions than producing ethanol from corn. However, Geoff Cooper questions whether ethanol shuffle makes sense in terms of environmental impact. Although the United States might be able to reduce its GHG emissions by using sugarcane-based ethanol instead of domestic corn-based ethanol, the impact on global atmospheric CO2 levels is no different wherever sugarcane-based ethanol is consumed. Rather, shipping that product from Brazil to the United States is actually worse for the climate due to additional emissions from transportation.

If the ethanol shuffle created by the RFS was not bad enough, we could be heading for something worse—ethanol tourism—in which imported sugarcane-based ethanol is subsequently reexported rather than being used domestically. To see why this might happen we need to examine the market for ethanol under the RFS with a blend wall from the perspective of blenders.

The elimination of the tax credit means that blenders face higher costs in complying with the RFS, holding other factors unchanged. At the same time, the imposition of higher levels of ethanol use through the RFS puts upward pressure on the demand for ethanol. The removal of the supplementary tariff on ethanol and falling world sugar prices due to increased global supplies of sugar would make Brazilian ethanol increasingly price-competitive in the U.S. market. Consequently, the United States could import a larger amount of sugarcane-based ethanol. Although Brazilian ethanol is currently more expensive than U.S. ethanol, theoretically the volume of imported ethanol could exceed the volume required by the advanced biofuels mandate. This is because blenders can replace corn-based ethanol with sugarcane-based ethanol to comply with the overall mandate, if, for example, the corn-based product becomes more expensive due to drought as is the case this year. Sugar-based ethanol qualifies not only for the advanced biofuels mandate in the RFS but also the overall renewable fuels mandate. Therefore, blenders’ demand for domestic corn-based ethanol is likely to fall if world sugar prices fall.

With overall domestic demand for ethanol constrained by weakening demand for fuel and the blend wall, the likely effect will be that excess supplies of mixed fuels generated by the RFS will be exported. Exports are possible because once ethanol is mixed with gasoline, the Renewable Identification Numbers (RINs) are no longer required to remain with renewable fuels and mixed fuels can be delivered anywhere. This could result in U.S. exports of mixed fuels containing sugar-based ethanol—imported Brazilian ethanol used to meet RFS mandates would not be used domestically, but rather re-exported in the form of blended fuel, that is—ethanol tourism. While other countries may benefit from discounted prices for mixed fuel that could result from this practice, it hardly makes sense on the grounds of U.S. energy security or reductions in GHG emissions. Ethanol tourism would be a perverse outcome of the command and control approach of the RFS.

The elimination of a tax credit and a secondary tariff for ethanol could have reduced distortions in the domestic market for transportation fuel, if the RFS had not remained in place. However, the continued application of the RFS, under which the volume of ethanol required to be used by fuel blenders is to be progressively increased, is likely to lead to further market distortions.

We have already witnessed an ethanol shuffle—in which Brazilian ethanol is imported and U.S. corn-based ethanol is exported—due to constrained domestic demand for mixed fuel. This could be replaced by ethanol tourism—in which Brazilian ethanol imported to meet the RFS is subsequently re-exported in the form of mixed fuel. With lower world sugar prices, continued low corn yields, and an increasing ethanol mandate under the RFS, the prospect would be for increased imports of sugar-based ethanol and exports of blended fuels. If the RFS is to remain, rather than being eliminated, the mandated volume of renewable fuels should not exceed the volume which can be consumed domestically so that exports of mixed fuel are not artificially encouraged. The sub-mandates, such as that for advanced biofuels which have already led to trade distortions, would need to be abandoned.

Cooper, G. (2011). The ethanol shuffle. The E-Xchange blog. Washington, DC: Renewable Fuels Association (RFA). Available online: http://www.ethanolrfa.org/exchange/entry/the-ethanol-shuffle/

McPhail, L., P. Westcott and H. Lutman. (2011). The renewable identification number system and U.S. biofuel mandates. Outlook BIO-03. Washington, DC: ERS, USDA. Available online: http://www.ers.usda.gov/media/138383/bio03.pdf

Renewable Fuels Association (RFA). (2010). The paradox of rising U.S. ethanol exports: Increased market opportunities at the expense of enhanced national energy security? Washington, D.C. Available online: http://ethanolrfa.3cdn.net/650a769ab9c9a94c36_r9m6iviy6.pdf

Renewable Fuels Association (RFA) news release. (2011). E15 decision opens blend to 2 out of 3 vehicles; More work yet to be done. Available online: http://www.ethanolrfa.org/news/entry/e15-decision-opens-blend-to-2-out-of-3-vehicles-more-work-yet-to-be-done/

Renewable Fuels Association (RFA). (2012). 2012 Ethanol industry outlook: Accelerating industry innovation. Washington D.C. Available online: http://ethanolrfa.3cdn.net/d4ad995ffb7ae8fbfe_1vm62ypzd.pdf

U.S. Environmental Protection Agency. (2011). EPA finalizes 2012 Renewable Fuel Standards. EPA-420-F-11-04. Washington, DC: Office of Transportation and Air Quality. Available online: http://www.epa.gov/otaq/fuels/renewablefuels/documents/420f11044.pdf

U.S. Environmental Protection Agency. (2012). EPA Decision to Deny Requests for Waiver of the Renewable Fuel Standard. Washington , DC: Office of Transportation and Air Quality. EPA-420-F-12-075. Available online: http://www.epa.gov/otaq/fuels/renewablefuels/documents/420f12075.pdf

Wisner, R. (2012). Ethanol exports: A way to scale the blend wall. Renewable Energy Newsletter. Ames, Iowa: Agricultural Marketing Resource Center.

Yano, Y., Blandford, D. and Surry, Y. (2010). Do Current U.S. Ethanol Policies Make Sense? Choices, Policy Issues, 10. Agriculture and Applied Economics Association. Available online: www.aaea.org/publications/policy-issues/