Source: Environmental Conservation Online System (ECOS)

https://ecos.fws.gov/ecp/species-reports [Accessed December 7, 2018].

The Endangered Species Act (ESA) is America’s flagship conservation law and also one of its most contentious. The ESA was created in 1973 under President Nixon to prevent threatened and endangered plant and animal species from reaching extinction. The U.S. Department of the Interior’s Fish and Wildlife Service (FWS) and the Department of Commerce’s National Marine Fisheries Service (NMFS) are responsible for classifying terrestrial and aquatic species as endangered and threatened, developing management plans that ensure species protection and recovery, and determining when recovery has been achieved. Classifying a species as “endangered” means that the species is susceptible to extinction throughout the entirety or the majority of its rangelands, while “threatened” indicates a species that is likely to become endangered in the near future.

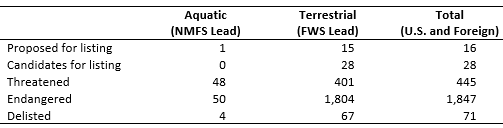

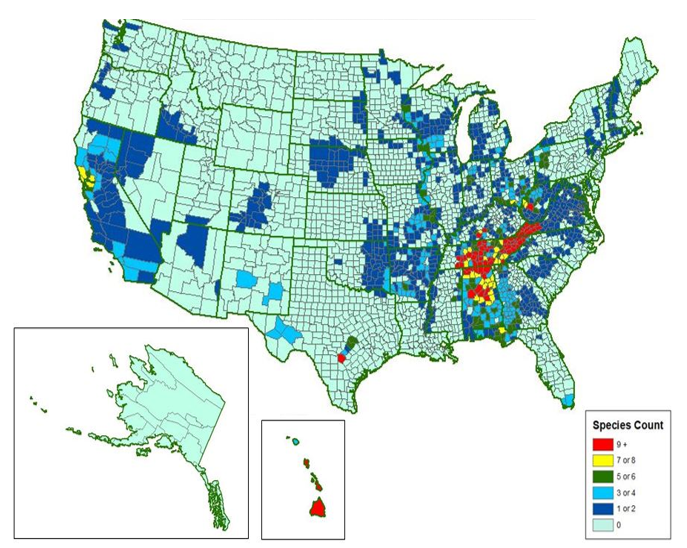

Since passage of the ESA in 1973, 2,363 species have been listed as either endangered or threatened, 71 of which were eventually delisted. Only 45 species have been delisted because of satisfactory recovery of the species. Currently, 2,336 species of plants and animals are listed as endangered or threatened or are currently under review (see Table 1). This includes those species proposed for listing as well as other candidate species. High concentrations of endangered vertebrate species are found in Arizona, California, Hawaii, and the southern tip of Florida, while high concentrations of endangered invertebrates are found in southern and central Appalachia (Figure 1).

On July 19, 2018, the FWS and NMFS proposed changes to the regulations implementing the ESA. While some of the proposed rules undo Obama-era regulatory revisions, several of the proposals represent watershed changes that would significantly change how key provisions of the ESA are implemented. The most dramatic and controversial of the recent proposed changes to the ESA involves the regulations surrounding listing and delisting species. We draw on past economic analyses to provide intuition about the potential consequences of several proposed changes to listing/delisting policy. To consider what these changes might mean, we pose three questions: (i) How might economic considerations influence the listing decision? (ii) What does “foreseeable future” mean and how does it influence listing decisions? and (iii) How should we gauge success?

Much of the debate concerning the ESA surrounds the role of economics, which plays an obvious role in determining the congressional budget allocations used to administer and implement the ESA. The ESA faces well-documented funding shortfalls (Miller et al., 2002; Stokstad, 2005), which may undermine the effectiveness of ESA recovery efforts (Ferraro, McIntosh, and Ospino, 2007) and have caused the number of species proposed for listing to outpace listing decisions, leading to backlogs (Stokstad, 2005).

But most of the recent debate over the role of economics in the ESA has focused on prioritizing species for protection and defining recovery. When enacting the ESA in 1973, Congress noted that decisions concerning the listing of species as endangered or threatened must be based solely on “the best available scientific information” with a prohibition on economic criteria. This “science only” mandate for listing decisions presents two challenges for the ESA. First, it limits the ability to manage how nonscientific variables such as public opinion and the physical appearance of the species indirectly influence the probability of listing (Metrick and Weitzman, 1996; Ando, 1999; Ferraro, McIntosh, and Ospino, 2007). Second, the “science only” mandate makes it harder to define clear criteria to guide listing decisions, which creates uncertainty and confusion for landowners and leaves considerable discretion in the hands of agency officials. Assessments of the likelihood of future impacts on a particular species or the habitat on which it relies must be made in the face of considerable uncertainties. To deal with this uncertainty, the statutory language that guides listing decisions adopts a precautionary principle approach (Prato, 2005). While this precautionary principle approach correctly acknowledges the need to act before uncertainty is completely resolved, it is difficult to define when precaution should be exercised.

The FWS and NMFS recently proposed deleting regulatory language that expressly prohibited “reference” to economic impacts in a listing decision. The FWS and NMFS (2018) are quick to assure that this would only allow for references to economic impacts in listing decisions but would not allow economic impacts to be considered in listing decisions. However, it is unclear whether economic impacts refer to both the benefits and the costs of listing a species. Even with a comprehensive economic analysis that includes both the costs and benefits, it is unclear why costly economic analyses should be undertaken if the insights gained from these analyses cannot be used in the listing decision. This proposal would almost certainly exacerbate ESA’s funding shortfalls and add to the current backlog of candidate species that have not received a final listing decision.

Source: Loomis and White (1996)

It is also unclear how reference to economic impacts in a listing decision would not suggest improper consideration of economic impacts. Thus, a logical question in response to these recent proposed changes is how economic considerations might influence the listing decision. While economic considerations would almost certainly change the composition of species deemed threatened and endangered, they may influence listing decisions through multiple channels, which makes predicting the influence of economic considerations on listing decisions challenging.

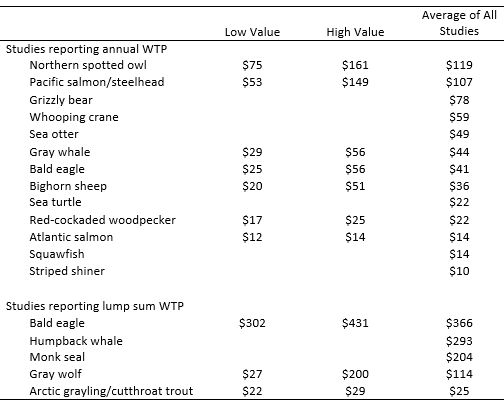

First, economic considerations could quantify the values people hold for endangered species, which would go a long way to quantifying the benefits of listing an at-risk species. Loomis and White (1996) estimate willingness to pay (WTP) for 18 species based on 20 studies (see Table 2). In this context, WTP is the amount individuals are willing to pay to protect at-risk species and is the conceptually correct measure of the benefits of species protection. If these types of economic values were considered in listing decisions, the endangered species list would become increasingly skewed toward charismatic megafauna (such as the northern spotted owl and bald eagle) instead of less well-known species like the striped shiner. But it is unlikely that WTP estimates will capture all of the monetary benefits of listing at-risk species. At-risk species may provide valuable ecosystem services that are not fully understood or may support other species that society values through complex food webs (Allen and Loomis, 2006). Indeed, quantifying the monetary benefits of protecting at-risk species is an enormous hurdle to effectively incorporating economic analyses into listing decisions (Kotchen and Reiling, 1998; Bulte and Van Kooten, 1999).

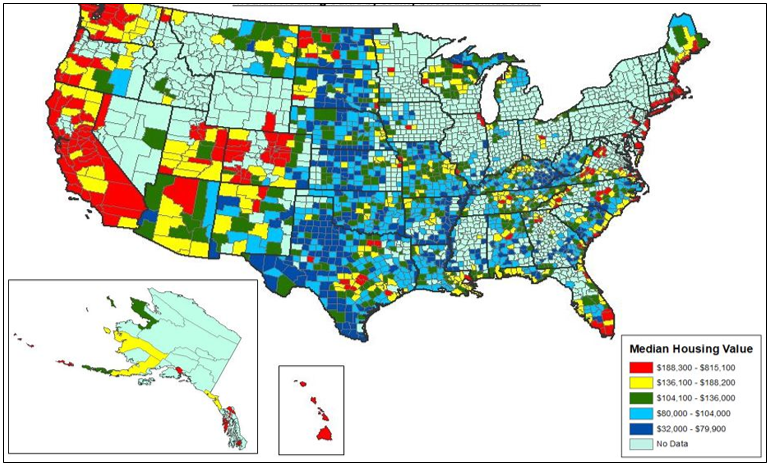

Second, economic considerations could help quantify the costs of ESA protections. To illustrate, Figure 2 shows the median housing value in each county in the United States. High median housing values tend to signal greater land development pressure and loss of wildlife habitat. As expected, an informal comparison of Figures 1 and 2 shows high concentrations of endangered vertebrate species, which often rely on large contiguous habitats, in areas with higher housing values, such as California, Arizona, and Hawaii. Because protecting species means protecting their habitat from development, areas with higher housing values will also tend to be where conservation is most costly. These economic considerations in the listing decision would make protecting species in California, Arizona, and Hawaii (and the habitats on which they depend) relatively more expensive than protecting endangered species in the upper Missouri River Basin or the Ohio River Valley. Economic considerations are also critical for determining how decreases in production and employment in one region due to species protection are offset by increases in production and employment in other regions. Transfer of economic activity is not a cost of protecting species.

In addition to quantifying the costs, economic considerations can also be used to identify strategies that help minimize the cost of ESA protections. Incentive programs can be more effective at protecting at-risk species than the traditional regulatory approach employed by the ESA (Langpap, 2006; Kamal, Grodzińska-Jurczak, and Brown, 2015). The cost savings achieved by many of these incentive programs depend on the terms of the conservation easement (Boyd, Caballero, and Simpson, 2000), threat of regulation (Langpap and Wu, 2004), their ability to create contiguous habitat (Parkhurst et al., 2002), and whether incentives are predicated on actions or outcomes (Hanley et al., 2012). Specifically, improvements in the design of conservation agreements have been pivotal in mitigating the cost of endangered species protection in the agriculture sector and ensuring consistent food production.

Economic considerations can also be used to establish how to weigh the benefits and costs of conservation to set conservation priorities. One approach is the cost-effectiveness criterion, which attempts to maximize returns from public conservation investments (Weitzman. 1993, 1998). But cost-effectiveness criteria have been criticized for overly simplifying extinction risk and the uncertainty in species benefits. An alternative strategy is to make listing decisions that minimize the maximum possible losses from species extinction (Bishop, 1978; Ready and Bishop, 1991). But evaluation criteria for listing decisions based on these min–max rules would be difficult to quantify and thus do not help us address the persistent debates over current hard-to-quantify listing decisions.

Sims et al. (2017) introduce a bioeconomic criterion for listing at-risk species, based on a real options approach, which treats listing as a risky public conservation investment. The bioeconomic criterion is a clearly defined critical species population threshold for efficient listing that captures (i) fundamental population dynamics (growth rate, carrying capacity), (ii) source of extinction risk, (iii) anthropogenic impacts on the population, (iv) various costs associated with listing, and (v) values people hold from hunting/harvesting the species and leaving the species in place. The criterion assumes a species with a population reduced through hunting or harvesting, which can be eliminated by listing the species. Listing the species requires a one-time investment (sunk cost) and initiates a stream of costs associated with protection and recovery. Treating listing as an investment is not incongruous. The General Accounting Office reported that the total cost of listing 34 species is approximately $700 million, ranging from a 1994 cost of $145,000 for the White River spinedace to a 1991 estimate of $154 million for the green sea turtle and loggerhead turtle (Shogren and Hayward, 1997). The median cost of preparing and publishing various listing documents alone ranges from $39,276 for a 90-day finding to $345,000 for a proposed rule with critical habitat (U.S. Department of the Interior, Fish and Wildlife Service, 2010).

The bioeconomic criterion balances two forms of regret. The most common form of regret is inaction—fear that in not listing a species or in listing too late it will become extinct. The bioeconomic criterion suggests hastening any listing decisions to minimize this form of regret. The second form of regret is the fear of failure—fear that conservation decisions will be deemed incorrect as new information arrives (Meek et al., 2015). Fear of failure can avoid costly conservation mistakes, but it also creates incentives to delay actions that could help at-risk species.

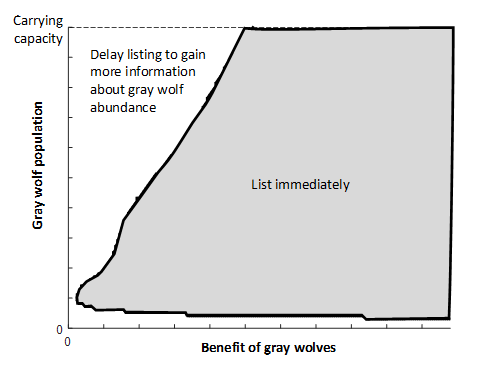

As an example, consider the case of the gray wolf, which was added to the endangered species list in 1973. Figure 3 shows the bioeconomic criteria for listing the gray wolf (Sims et al. 2017). Listing is only economically justified when the population is in the shaded region. Provided that society has some value for gray wolves, a declining wolf population (downward movement along the y-axis) will eventually cross into the shaded region and trigger listing. Increases in the economic benefits of the gray wolf (movement along the x-axis) increase the critical listing threshold (movement along the y-axis) and justify listing at a higher population threshold. Increases in the costs associated with listing a species shift the threshold down, thereby necessitating a lower population to justify listing.

The possibility of the gray wolf unexpectedly going extinct leads to a lower boundary on the shaded region. A declining wolf population will eventually justify listing, but an extremely small population would not. The lower boundary reflects those instances when the gray wolf population is low enough that they are likely to go extinct even if listed and given the considerable protections afforded by the ESA. This high possibility of extinction would make FWS reluctant to commit funds to list the gray wolf. Thus, economic considerations can lead to a strong case for protecting at-risk species if listing decisions are made before a population becomes severely impacted. However, ensuring the greatest amount of species conservation from a fixed budget means that species with small populations with a very uncertain future (those most in need of ESA protection) would be passed over in favor of more stable species that provide a more certain outcome.

Due to the various ways in which economic considerations influence listing decisions, it is difficult to draw definitive conclusions about the impact of introducing economic considerations in the listing decision. It is also important to remember that the FWS and NMFS proposals would only allow for references to economic impacts and would not allow economic impacts to be considered in listing decisions. However, it is clear that the efficiency gains achieved through economic considerations would alter the candidate species that would eventually be listed. The relative merits of this tradeoff depend on how one defines the ESA’s objectives. Similar debates over the role of economics in prioritizing conservation efforts are even playing out in the conservation biology community (Game, Kareiva, and Possingham, 2013; Brown et al., 2015; Jenkins et al., 2015a,b).

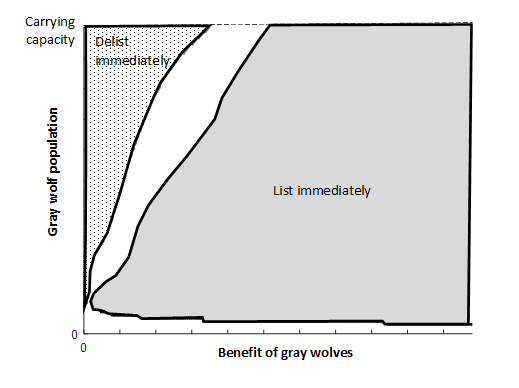

The ESA defines a “threatened species” as one that is “likely to become endangered within the foreseeable future throughout all or a significant part of its range.” Defining “foreseeable future” has been a contentious issue, especially for listings motivated by climate change. The new rule would define “foreseeable future” as “only so far into the future as the Services can reasonably determine that the conditions potentially posing a danger of extinction in the foreseeable future are probable.” This proposed rule change, which largely codifies agency guidance during the Obama administration, means that future potential threats to species that cannot be reliably predicted without speculation (e.g., climate change impacts) would not be considered in listing decisions. Forecasting extinction risk poses several challenges and is subject to considerable uncertainty (Thuiller et al., 2004; Araújo et al., 2005; Regan et al., 2005). This would lower the perceived risk of extinction for some species, which would reduce the case for listing. However, it would also make an investment in listing less risky, which increases the incentive to list these species.

To illustrate, Figure 4 shows the bioeconomic criteria for listing when the listing agency’s perceived risk of extinction for a species is reduced relative to the perceived risk of extinction in Figure 3. The reduced risk of extinction in Figure 4 would reflect the effect of limiting what is considered the “foreseeable future.” As expected, lower risk of extinction does reduce the case for listing (lower listing threshold), but only when the benefit of gray wolves is small. If the benefit of gray wolves is larger, the lower risk of extinction effectively eliminates the lower boundary on the shaded region. In short, lowering the perceived risk of extinction by limiting the definition of foreseeable future makes listing gray wolves seem like a safer investment. With this new definition of “foreseeable future,” economic considerations could provide a stronger argument for listing than the current “science only” mandate allows.

The goal of moving listed species to a recovered state is appealing and is often identified as a metric of the ESA’s success. Critics of the ESA cite the small number of delistings as proof of the legislation’s ineffectiveness (Doremus and Pagel, 2001). Proponents counter that many listed species would have gone extinct without the protections afforded by the ESA. The FWS defines “recovery” as “the process by which the decline of an endangered or threatened species is arrested and reversed, and threats removed or reduced so that the species’ survival in the wild can be ensured”. However, using this definition of recovery as a metric for ESA success is problematic. First, while population counts can help determine whether species decline has been reversed, determining whether threats have been removed or reduced is more difficult. The threat of relisting the species should mitigate, in part, any remaining threats, but this deterrent is untested since no species have been relisted following recovery. Second, for many species, reaching a recovered status is not possible due to an inability to alleviate threats to their habitat. For these species, success is marked by preventing extinction, not by removing the species from the endangered or threatened list.

The current standards for delisting a species are more restrictive than the standards that would dictate listing. Even with these more restrictive delisting standards, the number of species delisted has increased in recent years. The recent proposed rule changes would make the standards for delisting more similar to those for listing. Specifically, under the proposed changes, a species can be delisted if (i) it is extinct, (ii) it no longer meets the definitions of threatened or endangered (e.g., recovered to the extent that it no longer meets the statutory definitions), or (iii) the listed entity does not meet the statutory definition of a species. These changes would give the FWS and the NMFS more flexibility when delisting a species, which should, at the very least, continue the recent increase in species delisting.

Like debates over listing, recent debates over delisting species are driven by a lack of definitive criteria to guide delisting decisions. One advantage of the bioeconomic criteria in Sims et al. (2017) is its ability to identify delisting criteria that incorporate the initial listing criteria. For example, factors that increase the sunk cost of listing a species (e.g., costly interest group opposition to a candidate species listing) makes subsequent delisting more difficult to justify. Figure 5 shows that the efficient delisting criteria for the gray wolf are not the same as the criteria that define efficient listing. A listed species may recover to the point that the initial listing would appear unwarranted. But this is not sufficient evidence that the species should be delisted. When economic considerations are extended to the delisting decision, criteria that define “recovery” may be substantially more restrictive than criteria that define “endangered.” Thus, economic considerations lend some support to the current regulations surrounding delisting instead of the proposed rule changes.

Many of the changes to the ESA proposed by the FWS and NMFS represent efforts to codify existing agency practices or guidance or undo Obama-era regulatory revisions. However, many of the proposals would represent the most dramatic changes to the ESA since the early 1980s. Using the framework in Sims et al. (2017), we speculate what the proposed changes could do to listing and delisting decisions. Because of the intense scrutiny on additions and removals from the list, these proposed changes will likely generate the most controversy.

Our conclusions are based on two critical assumptions: First, including economic considerations in listing decisions will not result in decreases in Congressional budget allocations to the agencies that administer the ESA. Second, by “economic considerations,” we mean efforts to increase the efficiency of conservation activities provided by the ESA and not a veiled attempt to ignore the benefits that species conservation provides. Focusing on the ESA’s costs while ignoring its benefits is not an economic argument.

These proposed changes are unlikely to change people’s views of the ESA. Farrell (2015) finds that the opposition to gray wolf protection has more to do with culture and perceptions of morality than economics and science. It is also important to note recent efforts to increase protections for at risk species outside of the traditional workings of the ESA. There have been increasing calls for partnerships between public and private sectors to work together toward conserving endangered, threatened, and candidate species. Many of these partnerships focus on recovery (Groves, Klein, and Breden, 1995; Fox and Nino-Murcia, 2005; Conde et al., 2011), with few examples of private support for the listing process itself (though see Hanson, Wiles, and Gaydos, 2016). Partnerships have also recently developed to manage at-risk species proactively and avoid the need for endangered species listing (e.g., the FWS Candidate Conservation Agreements and Assurances and FWS Partners for Fish and Wildlife Program). Proactive, voluntary conservation can be in the private sector’s interest, particularly when it reduces the probability or cost of future compliance obligations (Langpap and Wu, 2004; Langpap, 2006; Boyd and Epanchin-Niell, 2017). One recent example is the response of petroleum companies to ESA regulations put in place to protect the lesser prairie chicken (Melstrom, 2017).

Allen, B.P., and J.B. Loomis. 2006. “Deriving Values for the Ecological Support Function of Wildlife: An Indirect Valuation Approach.” Ecological Economics 56(1):49–57.

Ando, A.W. 1999. “Waiting to Be Protected under the Endangered Species Act: The Political Economy of Regulatory Delay.” Journal of Law and Economics 42(1):29–60.

Araújo, M.B., R.J. Whittaker, R.J. Ladle, and M. Erhard. 2005. “Reducing Uncertainty in Projections of Extinction Risk from Climate Change.” Global Ecology and Biogeography 14(6):529–538.

Bishop, R.C. 1978. “Endangered Species and Uncertainty: The Economics of a Safe Minimum Standard.” American Journal of Agricultural Economics 60(1):10–18.

Boyd, J., K. Caballero, and R. D. Simpson. 2000. “The Law and Economics of Habitat Conservation: Lessons from an Analysis of Easement Acquisitions.” Stanford Environmental Law Journal 19:209.

Boyd, J., and R.S. Epanchin-Niell. 2017. Private Sector Conservation Investments under the Endangered Species Act: A Guide to Return on Investment Analysis. Washington, DC: Resources for the Future, RFF DP 17-11.

Brown, C.J., M. Bode, O. Venter, M.D. Barnes, J. McGowan, C.A. Runge, J.E. Watson, and H.P. Possingham. 2015. “Effective Conservation Requires Clear Objectives and Prioritizing Actions, Not Places or Species.” Proceedings of the National Academy of Sciences 112(32):E4342–E4342.

Bulte, E.H., and G.C. Van Kooten. 1999. “Marginal Valuation of Charismatic Species: Implications for Conservation.” Environmental and Resource Economics 14(1):119–130.

Conde, D.A., N. Flesness, F. Colchero, O.R. Jones, and A. Scheuerlein. 2011. “An Emerging Role of Zoos to Conserve Biodiversity.” Science 331(6023):1390–1391.

Doremus, H., and J.E. Pagel. 2001. “Why Listing May Be Forever: Perspectives on Delisting under the U.S. Endangered Species Act.” Conservation Biology 15(5):1258–1268.

Farrell, J. 2015. The Battle for Yellowstone: Morality and the Sacred Roots of Environmental Conflict: Morality and the Sacred Roots of Environmental Conflict. Princeton, NJ: Princeton University Press.

Ferraro, P.J., C. McIntosh, and M. Ospina. 2007. “The Effectiveness of the US Endangered Species Act: An Econometric Analysis Using Matching Methods.” Journal of Environmental Economics and Management 54(3):245–261.

Fox, J., and A. Nino-Murcia. 2005. “Status of Species Conservation Banking in the United States.” Conservation Biology 19(4):996–1007.

Game, E.T., P. Kareiva, and H.P. Possingham. 2013. “Six Common Mistakes in Conservation Priority Setting.” Conservation Biology 27(3):480–485.

Groves, C.R., M.L. Klein, and T.F. Breden. 1995. “Natural Heritage Programs: Public-Private Partnerships for Biodiversity Conservation.” Wildlife Society Bulletin 23(4):784–790.

Hanley, N., S. Banerjee, G.D. Lennox, and P.R. Armsworth. 2012. “How Should We Incentivize Private Landowners to ‘Produce’ More Biodiversity?” Oxford Review of Economic Policy 28(1):93–113.

Hanson, T., G.J. Wiles, and J.K. Gaydos. 2016. “A Novel Public–Private Partnership Model for Improving the Listing of Endangered Species.” Biodiversity and Conservation 25(1):193–198.

Jenkins, C.N., K.S. Van Houtan, S.L. Pimm, and J.O. Sexton. 2015a. “Reply to Brown et al.: Species and Places Are the Priorities for Conservation, Not Economic Efficiency.” Proceedings of the National Academy of Sciences 112(32):E4343–E4343.

Jenkins, C.N., K.S. Van Houtan, S.L. Pimm, and J.O. Sexton. 2015b. “US Protected Lands Mismatch Biodiversity Priorities.” Proceedings of the National Academy of Sciences 112(16):5081–5086.

Kamal, S., M. GrodziÅ„ska-Jurczak, and G. Brown. 2015. “Conservation on Private Land: A Review of Global Strategies with a Proposed Classification System.” Journal of Environmental Planning and Management 58(4):576–597.

Kotchen, M.J., and S.D. Reiling. 1998. “Estimating and Questioning Economic Values for Endangered Species: An Application and Discussion.” Endangered Species Update 15(5):77–83.

Langpap, C. 2006. “Conservation Of Endangered Species: Can Incentives Work for Private Landowners?” Ecological Economics 57(4):558–572.

Langpap, C., and J. Wu. 2004. “Voluntary Conservation of Endangered Species: When Does No Regulatory Assurance Mean No Conservation?” Journal of Environmental Economics and Management 47(3):435–457.

Loomis, J.B., and D.S. White. 1996. “Economic Benefits of Rare and Endangered Species: Summary and Meta-Analysis.” Ecological Economics 18(3):197–206.

Meek, M.H., C. Wells, K.M. Tomalty, J. Ashander, E.M. Cole, D.A. Gille, B.J. Putman, J.P. Rose, M.S. Savoca, L. Yamane, J.M. Hull, D.L. Rogers, E.B. Rosenblum, J.F. Shogren, R.R. Swaisgood, and B. May. 2015. “Fear of Failure in Conservation: The Problem and Potential Solutions to Aid Conservation of Extremely Small Populations.” Biological Conservation 184:209–217.

Melstrom, R.T. 2017. “Where to Drill? The Petroleum Industry's Response to an Endangered Species Listing.” Energy Economics 66:320–327.

Metrick, A., and M.L. Weitzman. 1996. “Patterns of Behavior in Endangered Species Preservation.” Land Economics 72(1): 1–16.

Miller, J.K., M.J. Scott, C.R. Miller, and L.P. Waits. 2002. “The Endangered Species Act: Dollars and Sense?” AIBS Bulletin 52(2):163–168.

Parkhurst, G.M., J.F. Shogren, C. Bastian, P. Kivi, J. Donner, and R.B. Smith. 2002. “Agglomeration Bonus: An Incentive Mechanism to Reunite Fragmented Habitat for Biodiversity Conservation.” Ecological Economics 41(2):305–328.

Prato, T. 2005. “Accounting for Uncertainty in Making Species Protection Decisions.” Conservation Biology 19(3):806–814.

Ready, R.C., and R.C. Bishop. 1991. “Endangered Species and the Safe Minimum Standard.” American Journal of Agricultural Economics 73(2):309–312.

Regan, T.J., M.A. Burgman, M.A. McCarthy, L.L. Master, D.A. Keith, G.M. Mace, and S.J. Andelman. 2005. “The Consistency of Extinction Risk Classification Protocols.” Conservation Biology 19(6):1969–1977.

Shogren, J.F., and P.H. Hayward. 1997. “Biological Effectiveness and Economic Impacts of the Endangered Species Act.” Land & Water Land Review 32:531–550.

Sims, C., D. Finnoff, A. Hastings, and J. Hochard. 2017. “Listing and Delisting Thresholds under the Endangered Species Act.” American Journal of Agricultural Economics 99(3):549–570.

Stokstad, E. 2005. “What's Wrong with the Endangered Species Act?” Science 309(5744):2150–2152.

Thuiller, W., M.B. Araújo, R.G. Pearson, R.J. Whittaker, L. Brotons, and S. Lavorel 2004. “Biodiversity Conservation: Uncertainty in Predictions of Extinction Risk.” Nature 430(6995): 1.

U.S. Fish and Widlife Service and National Oceanic and Atmospheric Administration. 2010. “Endangered and Threatened Wildlife and Plants; Review of Native Species That Are Candidates for Listing as Endangerd or Threatened; Annual Notice of Findings on Resubmitted Petitions; Annual Description of Progress on Listing Actions.” Federal Register 75(217). Rep. 50 CFR Part 17.

U.S. Fish and Widlife Service and National Oceanic and Atmospheric Administration. 2018. “Endangered and Threatened Widlife and Plants; Revisions of the Regulations for Listing Species and Designating Critical Habitat.” Federal Register 83(143):35193–35201.

Weitzman, M.L. 1993. “What to Preserve? An Application of Diversity Theory to Crane Conservation.” Quarterly Journal of Economics 108(1):157–183.

Weitzman, M.L. 1998. “The Noah’s Ark Problem.” Econometrica 66(6):1279–1298.

Link to academic journal article: https://academic.oup.com/ajae/article/99/3/549/2961784