Demand for organic food has grown rapidly since the rule establishing the National Organic Program was published in 2000. In 2016, U.S. organic food sales were $43 billion, up 8.4% from the previous year (Organic Trade Association, 2017) and up more than 400% from the 7.8 billion in organic food sales in 2000 (Dimitri and Greene, 2002). Annual growth rates have been in double digits in nearly every year since the early 1990s, exceeding 20% in some years (Greene et al., 2016). The domestic potential to supply organic food, as measured by certified organic acreage, has also grown considerably but not at a comparable rate. In 2000, total U.S. certified organic acreage was 1,776,073 acres. Although there are differences in recent estimates, certified organic acreage had risen to roughly 5 million acres by 2015, slightly less than a 200% increase over the course of 15 years (USDA, 2013b, 2016).

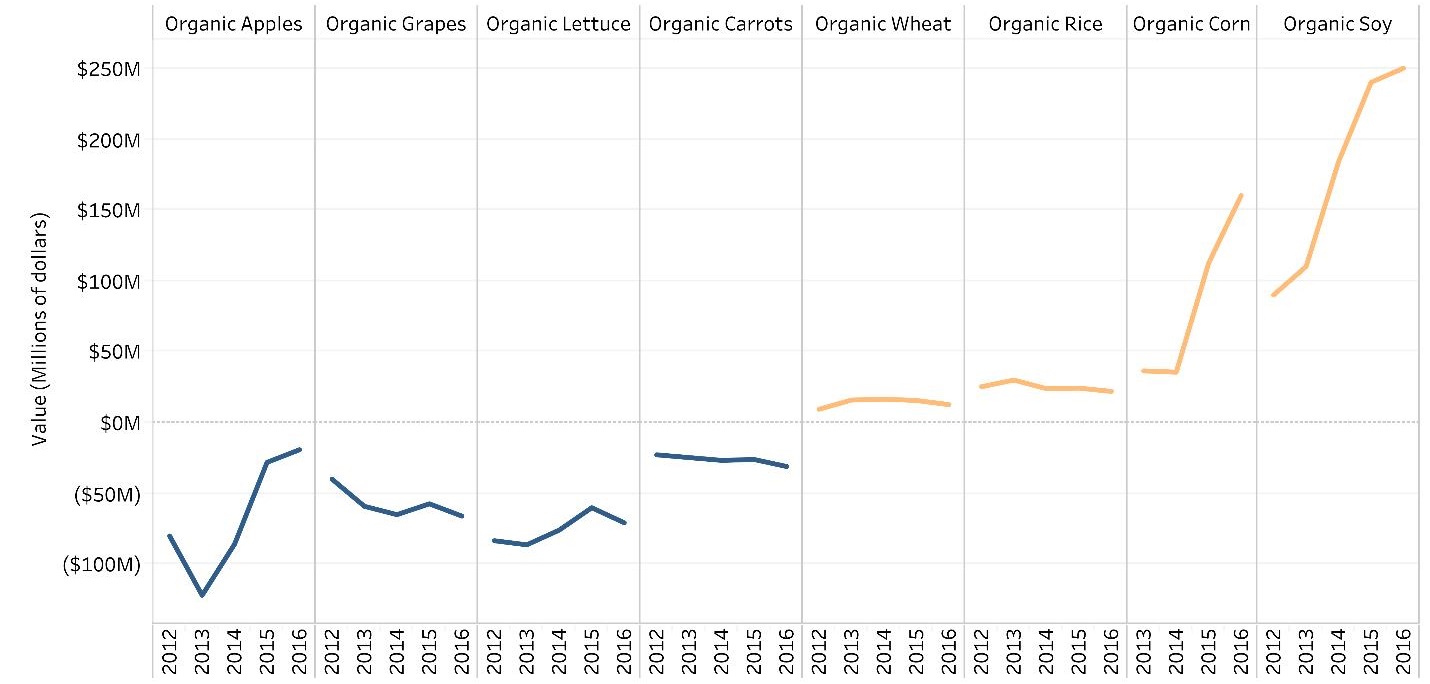

Note: Negative net imports (blue lines) indicate net exports.

Source: The authors, using U.S. Census Bureau trade data

obtained from USDA (2017b).

Production growth has also been uneven across sectors within organic agriculture. While certified cropland for fruits, vegetables, and nuts increased by slightly more than 500% from 2000 to 2015 and certified pasture and rangeland increased by nearly 300%, acreage for field crops such as corn, soybeans, and hay that are used to produce feed for organic livestock grew by only about 140% (USDA, 2013b, 2016).

The United States is a top exporter of conventional corn and soybeans, but there has been a sharp increase in imports of organic corn and soybeans as organic demand growth has exceeded the growth in domestic production. An analysis of U.S. Department of Agriculture (USDA), Foreign Agricultural Service (FAS) data shows that corn imports have grown at an annual rate of 93.7% since 2013, to $160 million, while soybean imports have grown by 36.7% annually since 2011, to over $250 million (USDA, 2017b).

The story is quite different for organic fresh fruit and vegetable markets. Among the specialty crops that are grown in the United States and for which there are organic trade data available, the United States is often a net exporter. Figure 1 shows the dollar value of net imports for organic apples, grapes, lettuce, carrots, wheat, rice, corn, and soy from 2012 to 2016. The fruit and vegetable crops (apples, grapes, lettuce, and carrots; blue lines) are all net exports, while the grain crops (wheat, rice, corn, and soy; orange lines) are all net imports. The sharp increases in imports over the past few years for corn and soybeans are striking, especially compared to the relatively flat lines for most of the other crops pictured.

The relatively slow growth in certified organic field crop acreage is somewhat surprising in light of research findings on the profitability of organic production systems. Organic crop production in the Midwest has been found to be more profitable than the conventional corn-soybean rotation on a per acre basis in experimental trials and through analysis of field-level data (Helmers, Langemeier, and Atwood, 1986; Delate et al., 2003; Pimentel et al., 2005; Chavas, Posner, and Hedtcke, 2009; Delbridge et al., 2011; Center for Farm Financial Management, 2017). At the whole-farm level, Delbridge et al. (2013) accounted for the possibility that conventional systems can be managed on larger farms because of the less intensive management requirements. Nevertheless, they still found expected profits to be higher for the organic system, with a profitability advantage that was greatest for small farms. Delbridge and King (2016) incorporated risk and the cost of transition into a model of the organic adoption decision and found that small farms face lower transition and opportunity costs and are more likely to transition. Expected transition rates of small farms in particular were very high when returns to conventional cropping systems are low.

All of these results suggest that we should be seeing higher transition rates than are actually occurring. The discrepancy suggests that there are significant barriers to transition in the real world that may be affecting producers’ decisions. We identify and discuss these barriers, grouping them into four broad categories: management barriers, policy barriers, cultural barriers, and market uncertainties.

Conventional farmers who want to begin marketing crops or livestock products as “organic” in the United States must first have their cropland or animals certified by a third-party organic certifier. Since 2002, organic certification has been federally defined based on a set of regulations administered and enforced by the USDA National Organic Program (NOP). These national standards include provisions prohibiting the use of transgenic seed and most synthetic fertilizers and pesticides and requiring that animals be provided a certain level of access to pasture. To achieve organic certification, cropland must be managed in accordance with the organic standards for three years prior to certification and animals must be managed according to the organic standards for one year before certification. This period is referred to as the “organic transition period” (USDA, 2013a). During the transition period, most farms achieve lower yields than they did under conventional management. Moreover, crops and livestock products cannot be marketed as organic during this period, often resulting in substantially lower revenues for transitioning farms. There can also be additional transition costs associated with changes in machinery and equipment, navigating regulatory hurdles, and learning to manage an organic system.

The revenue that a farmer expects to earn from selling crops at organic prices and the expected costs to be incurred under organic management are key factors in the decision to pursue organic certification. While many of the costs associated with organic crop and livestock systems are similar in nature to those faced by conventional farmers (for example, machinery costs, purchased inputs) and are easily computable, some management difficulties related to organic production are more subtle and rarely included in published quantitative analyses of organic farm profitability. These production, marketing, and record-keeping challenges can be significant barriers to organic adoption.

Achieving organic certification involves significant paperwork and record keeping not required of conventional growers. This has been termed the “hassle factor,” by Carmen Fernholz, fomer University of Minnesota Organic Coordinator for Research Management and long-time organic crop producer. For example, organic and transitioning farmers must keep detailed records on all inputs applied to their cropland as well as crop rotation information and plans to avoid commingling of organic and conventional crops. Organic farms are required to have annual inspections to maintain organic certification and must report any instances of pesticide drift that might impact certification status (USDA, 2013a). Though difficult to quantify, responses to surveys of conventional, organic, and de-certified organic farmers suggest that navigating the certification process and paperwork are seen as significant challenges and are often cited as a primary cause by farms that surrender their organic certification (Sierra et al., 2008; Farmer et al., 2014; Veldstra, Alexander, and Marshall 2014; Stephenson et al., 2017).

Organic farmers face additional management challenges, including requirements that they source approved inputs (such as certified organic livestock feed and organic seed) and maintain separate crop storage facilities to avoid comingling and contaminating organic products. If the farm includes conventional acreage, machinery must be cleaned thoroughly before it can be used on the farm’s organic crop. In addition to increasing the financial cost of transitioning acreage to organic management, these restrictions limit marketing opportunities and reduce the number of custom operators available for hire by organic growers (Press et al., 2014).

Transitioning to organic production requires the farmer to learn new management techniques that do not rely on synthetic pesticides, develop relationships with new buyers, and identify new input suppliers. The difficulties of making a successful transition to organic production have been compounded by a relatively weak support structure for organic producers. In the years before the NOP was established, there were many fewer organic farms and most university extension programs had little to offer organic growers in terms of technical support (Duram, 2000; Lohr and Park, 2003). Government research funding devoted to organic production methods was limited and some of the most impactful research programs were privately funded. In recent years a more robust group of organic growers has developed and government funding for organic research has increased, but lag times between agricultural research expenditures and the realization of productivity gains are often long. In addition, while conventional growers now receive a large and growing share of their technical support bundled with fertilizer, pesticide, and seed purchases, farm input suppliers have little incentive to provide technical support for organic farmers who do not purchase their products.

The conclusion that a scarcity of available technical information on organic production methods acts as a barrier to organic adoption is supported by recent findings by Marasteanu and Jaenicke (2015), who showed that clusters of certified organic operations are more likely to develop near organic certifiers that conduct outreach activities than near certifiers that do not, suggesting that a lack of access to technical information may make organic adoption more difficult.

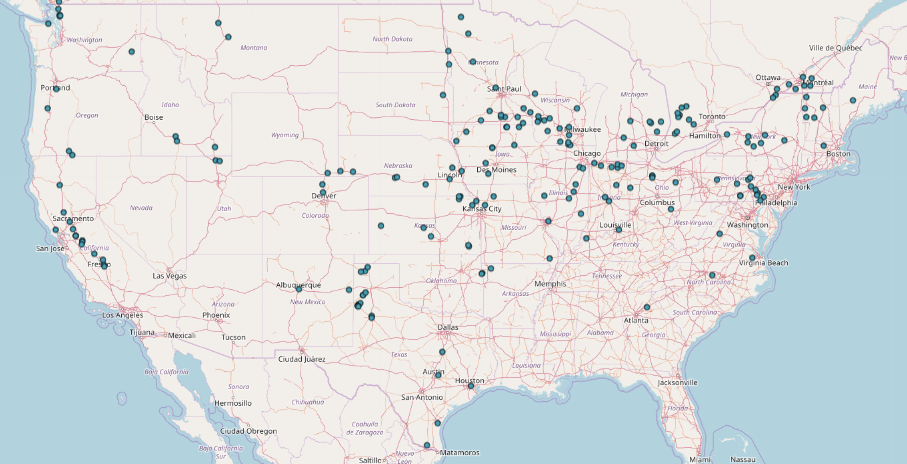

Source: Mercaris (2017).

The lack of a robust physical infrastructure required for efficient marketing and transport of organic commodities can also create barriers to adoption. This includes grain elevators, which are generally the first point of sale for farmers and perform initial post-harvest handling functions like grain storage and cleaning. Similar to organic farming operations, organic grain handlers also must be certified by a third-party verifier. Organic growers cannot sell their grain to conventional elevators. This means that there are far fewer places for organic growers to deliver their grain and implies higher transportation costs. Of 8,783 grain elevators operating nationwide in January of 2014, only 287, or roughly 3%, were certified to handle organic crops (Figure 2; Mercaris, 2017).

Another difficulty faced by producers transitioning to organic production is a lack of price information about the crops they grow and market. While transparent information about conventional agricultural crops is available via both a cash and a futures market, organic agriculture has not had the benefit of these types of price signals. Growers have relied on informal networks (coffee shop talk) or have developed relationships with individual buyers or brokers. The lack of accurate, timely, and precise data on organic crop prices adds risk and cost in a variety of areas and makes risk management tools like crop insurance and forward contracting less effective.

The modern federal crop insurance program serves two objectives. First, crop insurance provides producers with their primary method of managing yield and price risk. Second, as direct payment subsidies have been eliminated and the available amount of insurance coverage has increased, the federal crop insurance program has become the primary source of subsidy transfer for commodity growers (Sherrick and Schnitkey, 2013). Unsurprisingly, the crop insurance program sees nearly full participation for major crops. Over 87% of corn acreage and 88% of soybean acreage were covered by crop insurance in 2014 (USDA, 2014b, 2017c).

Until recently, however, the crop insurance program has not offered organic producers the same risk management options as it has to conventional producers. Before 2011, organic crops could not be insured at organic prices, limiting the risk management benefit provided to organic growers. Furthermore, because organic commodity growers typically use diverse crop rotations, including cover crops and minor crops for which organic insurance products are still not available, organic producers are often unable to insure their entire operation. Partly in response to this policy limitation, the 2014 Farm Bill introduced the Whole Farm Revenue Protection (WFRP) plan, which was designed to improve crop insurance availability for specialty crop growers and diversified farms. While the plan is expected to increase risk management options for some organic producers, achieving adequate risk management during an organic transition remains a challenge (Paggi, 2016).

From a subsidy standpoint, the shift over time from direct payments to the crop insurance program as the primary agricultural subsidy vehicle has likely resulted in less farm program support for organic agriculture than would otherwise have been the case. Under the direct payments regime, organic producers were usually able to receive the same payments as conventional producers. However, since the elimination of the direct payment subsidy in the 2008 Farm Bill was not directly offset by greater insurance options for organic producers, that policy shift has resulted in relatively less subsidy support for organic producers than their conventional counterparts over the past few years.

The 2014 Farm Bill also included several specific organic provisions, including increased funding to help producers and handlers with certification costs, increased funding for organic research and data collection, and the establishment of an option for producers to opt in to an organic promotion program. Certified organic producers also no longer have to pay for conventional commodity programs on their organic production. These measures represent a lowering of some policy barriers to organic transition and may contribute to higher organic adoption and retention rates in the future.

Cultural and ideological factors contribute to a farmer’s decision to adopt an organic production system, just as they contribute to a consumer’s decision to purchase organic foods. While some farmers choose to produce crops or livestock products using organic methods because they believe it to be healthier for them and their families, more environmentally responsible, or for other non-pecuniary reasons, cultural and ideological factors can also act as barriers to organic adoption.

In some cases, the agricultural community in which a prospective organic farmer lives and farms may be hostile to the idea of organic methods, thus discouraging the farmer from pursuing organic certification. Several studies have found through interviews and surveys that prospective and current organic farmers must contend with the beliefs of their families and neighbors that organic farming is not a responsible or efficient way to farm or that it is dependent on misinformed consumers for the price premiums required to maintain profitability in an organic system (Duram, 2000; Brock and Barham, 2013; Press et al., 2014). While these viewpoints are certainly debatable, the social pressure created by organic skeptics within a community can be strong enough to dissuade some farmers who might otherwise consider organic transition. As organic farming becomes more common and there are more visible examples of organic farmers who have experienced sustained success, this barrier has become less significant in some communities, but it continues to play a role in farmers’ transition decisions. Recent quantitative analyses of spatial clustering of organic operations, while not definitive with respect to casual relationships, are consistent with the qualitative research on the importance of social support in the transition decision (Marasteanu and Jaenicke, 2015, 2016).

The ideological beliefs of individual farmers, rather than the beliefs of their community and peers, can also lead to lower organic adoption rates than might otherwise be expected when only analyzing the farm-level profitability of organic systems. Conventional farmers who believe that organic production methods are actually environmentally harmful or that organic price premiums are based solely on deceptive marketing tactics are less likely to consider organic production as a serious option. Among this group, labeled “committed conventional” farmers by Darnhofer, Schneeberger, and Freyer (2005), potential profitability advantages are discounted because they find the “philosophy” of organic farming objectionable. This has been identified as a significant factor in the perceived attractiveness of organic production systems among producers in the United States (Brock and Barham, 2013; Constance and Choi, 2010; Sierra et al., 2008) and Europe (Darnhofer, Schneeberger, and Freyer, 2005; Läpple and Kelley, 2013; Sutherland, 2013). It is unclear whether this ideological barrier is becoming more or less significant as time passes and the organic market develops.

As farmers consider the decision to transition to organic production, they must grapple with significant uncertainty regarding the future profitability of organic systems. Organic markets have developed significantly in recent years, and growers have reported fewer challenges in marketing their products than in the early days of the organic program (Duram, 1999; USDA, 2008, 2014a). However, since the financial success of organic production usually relies on significant price premiums for certified organic crop and livestock products, the transition decision is particularly sensitive to perceived threats to the sustainability of those premiums (Crowder and Reganold, 2015; Delbridge and King, 2016). While the levels of organic price premiums vary by crop, the general strength of the organic brand and the resulting revenues achievable for organic producers are dependent on three major uncertain factors.

First, the degree to which consumers will consider the growing number of alternative food attributes and labeling (such as “GMO free,” “local,” or “certified humane”) as substitutes for organic products is not clear. Some studies have shown that more consumers prefer locally produced food products to organic food products (Greene et al., 2009; Costanigro et al., 2011; Onozaka and McFadden, 2011), and organic premiums have been shown to be much smaller when other grower attributes (such as locality, scale, etc.) are already known (Connolly and Klaiber, 2014). This suggests that some consumers are likely to prefer products with lower prices than certified organic products as long as they hold the attributes that are important to the consumer. With growth in the number of products that carry “sustainable” attribute labels other than the USDA organic certification, there is some uncertainty about the future growth of organic demand.

Second, many growers have reported concerns that the thinness of organic markets leaves them exposed to the risk of a decrease in prices if rates of organic transition increase (Constance and Choi, 2010). Because of the scarcity of organic production and price data, there is little understanding of the price elasticities of supply for organic commodities. In recent years, prices of organic feed grains have been lower than longer-run averages, in part because of large increases in international imports of these commodities (Figure 1; USDA, 2017a,b). While, to our knowledge, no quantitative analysis has been published on the degree to which imports have affected the prices received by domestic organic growers, concerns about the growth in organic supply appear to have been realized for some commodities.

Third, the value of the organic label is dependent on the consumer perception that organic production requirements are rigorously enforced. There have been recent high profile reports of conventional feed grains being fraudulently imported as organic and a large organic dairy producer appearing to not follow organic standards (Whoriskey, 2017a,b). If consumers lose faith that compliance with organic standards is ensured by participation in the NOP, future price premiums are likely to fall and the future profitability of organic systems will be threatened. Producers considering a costly transition to an organic system need to evaluate whether or not they believe enforcement will be sufficient to maintain the integrity of the organic program.

Traditional agricultural policy options are relatively well suited for addressing management and policy barriers to organic transition. USDA is already allocating more funds to organic research, and the 2010 Strategic Plan called for a number of activities that would support a goal of increasing the number of certified organic operations by 25%. This led to the development of USDA–AMS online training modules “Organic 101” and “Organic 201” and the Sound and Sensible Initiative, which focuses on “simplifying and streamlining organic certification and compliance” (McEvoy, 2015). The USDA has maintained the organic certification cost-share program, and several states have initiated similar cost-share programs to support transition to organic certification. As already noted, the USDA also has taken steps to improve crop insurance options for organic producers. All these efforts require fiscal resources, however, and there are many competing demands for the limited resources to be devoted to farm support programs.

Private-sector efforts to encourage transition through price premiums for transition crops coupled with long-term contracts after certification may ultimately be more effective than public policies in stimulating transition to organic production. Food manufacturers and retailers have strong financial incentives to respond to growing consumer demand for organic foods, but this requires reliable access to growing supplies of certified organic crop and livestock ingredients. Stable, long-term supplier–manufacturer relationships, in a manner consistent with the stylized facts for “modern agricultural markets” outlined by Sexton (2013), can be mutually beneficial and adaptable to changing circumstances. As such, these relationships may help address both management barriers and provide more effective risk management options.

Addressing cultural barriers to transition is a more difficult challenge. Philosophical and ideological objections and community resistance to organic agriculture can be slow to change. The USDA has made efforts to increase awareness of the need for conventional and organic agriculture communities to live side by side through the Agricultural Coexistence project (https://www.usda.gov/topics/farming/coexistence). However, awareness of conflicts is only the first step to resolving them. Once again, incentives created by strong consumer demand for organic food products and manufacturer commitment to growing the supply of organic ingredients may have the greatest impact on reducing cultural barriers to transition in the long run. Maintaining the integrity of the organic “brand” will be critical for continued growth in demand and manufacturer commitment to organic, however, and this is a function that is critically supported by public policies.

There are many valuable uses for rigorous, accurate, and timely market data, and its collection and dissemination should be supported. More robust production and sales data would allow improved estimates of supply and demand elasticities, leading to a partial lowering of the market uncertainty barriers discussed earlier. Such data would also inform farm management, including planting and crop mix decisions, crop marketing, and capital planning. Both governmental and private sector organizations currently collect and disseminate market data on organic crops including the USDA Agricultural Marketing Service (AMS); USDA National Agricultural Statistics Service (NASS); and Mercaris (www.mercaris.com). These entities provide different sets of information: the USDA covers farmgate organic spot market prices, acreage reports at intervals ranging from 1 to 5 years, and import/export data. Mercaris tracks delivered cash market prices for organic grains by U.S. and Canadian region, end use, and delivery date. Mercaris also analyzes and interprets USDA organic data on trade flows and acreage. While more information is always needed, these services are a fundamental step to better understanding organic grain markets.

The organic agricultural sector has experienced significant development in recent decades but continues to face challenges. While organic foods are now firmly established in mainstream retail outlets and organic acreage has expanded, the thinness of organic markets and the difficulties and expense associated with achieving certification of cropland have created occasional supply shortfalls. Farmers will continue to face tough decisions on the question of organic adoption and the organic food industry will continue to contend with threats to the organic brand. It remains to be seen whether the organic community—including private industry, policy makers, and certifying bodies—will respond to these barriers in ways that will encourage continued and sustainable growth of organic agriculture in the United States.

Brock, C., and B. Barham. 2013. “‘Milk is Milk’: Organic Dairy Adoption Decisions and Bounded Rationality.” Sustainability 5:5416–5441.

Center for Farm Financial Management. 2017. FINBIN Farm Financial Database. St. Paul, MN: University of Minnesota. Available online: http://www.finbin.umn.edu

Chavas, J.-P., J.L. Posner, and J. L. Hedtcke. 2009. “Organic and conventional Production Systems in the Wisconsin Integrated Cropping Systems Trial: II. Economic and Risk Analysis 1993–2006.” Agronomy Journal 101:288–295.

Connolly, C., and H.A. Klaiber. 2014. “Does Organic Command a Premium When the Food Is Already Local?” American Journal of Agricultural Economics 964:1102–1116.

Constance, D.H., and J.Y. Choi. 2010. “Overcoming the Barriers to Organic Adoption in the United States: A Look at Pragmatic Conventional Producers in Texas.” Sustainability 2:163–188.

Costanigro, M., D.T. McFadden, S. Kroll, and G. Nurse. 2011. “An In-Store Valuation of Local and Organic Apples: The Role of Social Desirability.” Agribusiness 274:456–477.

Crowder, D.W., and J.P. Reganold. 2015. “Financial Competitiveness of Organic Agriculture on a Global Scale.” Proceedings of the National Academy of Sciences 11224:7611–7616.

Darnhofer, I., W. Schneeberger, and B. Freyer. 2005. “Converting or Not Converting to Organic Farming in Austria: Farmer Types and Their Rationale.” Agriculture and Human Values 22:39–52.

Delate, K., M. Duffy, C. Chase, A. Holste, H. Friedrich, and N. Wantate. 2003. “An Economic Comparison of Organic and Conventional Grain Crops in a Long-Term Agroecological Research LTAR Site in Iowa.” American Journal of Alternative Agriculture 18:59–69.

Delbridge, T.A., and R.P. King. 2016. “Transitioning to Organic Crop Production: A Dynamic Programming Approach.” Journal of Agricultural and Resource Economics 413:481–498.

Delbridge, T.A., C. Fernholz, R.P. King, and W. Lazarus. 2013. “A Whole-Farm Profitability Analysis of Organic and Conventional Cropping Systems.” Agricultural Systems 122:1–10.

Delbridge, T.A., J.A. Coulter, R.P. King, C.C. Sheaffer, and D.L. Wyse. 2011. “Economic Performance of Long-Term Organic and Conventional Cropping Systems in Minnesota.” Agronomy Journal 103:1372–1382.

Dimitri, C., and C. Greene. 2002. Recent Growth Patterns in the U.S. Organic Foods Market. Washington, DC: U.S. Department of Agriculture, Economic Research Service, Agriculture Information Bulletin 777, September.

Duram, L. 1999. “Factors in Organic Farmers’ Decisionmaking: Diversity, Challenge, and Obstacles.” American Journal of Alternative Agriculture 14:2–10.

Duram, L. 2000. “Agents’ Perceptions of Structure: How Illinois Organic Farmers View Political, Economic, Social, and Ecological Factors.” Agriculture and Human Values 17:35–48.

Farmer, J.R., G. Epstein, S.L. Watkins, and S.K. Mincey. 2014. “Organic Farming in West Virginia: A Behavioral Approach.” Journal of Agriculture, Food Systems, and Community Development 44:155–171.

Greene, C., C. Dimitri, B.-H. Lin, W. McBride, L. Oberholtzer, and T. Smith. 2009. Emerging Issues in the U.S. Organic Industry. Washington, DC: U.S. Department of Agriculture, Economic Research Service, Economic Information Bulletin 55, June.

Greene, C., S.J. Wechsler, A. Adalja, and J. Hanson. 2016. Economic Issues in the Coesistence of Organic, Genetically Engineered (GE), and Non-GE Crops. Washington, DC: U.S. Department of Agriculture, Economic Research Service, Economic Information Bulletin 149, February.

Helmers, G.A., M.R. Langemeier, and J. Atwood, 1986. “An Economic Analysis of Alternative Cropping Systems for East-Central Nebraska.” American Journal of Alternative Agriculture 1:153–158.

Läpple, D., and H. Kelley. 2013. “Understanding the Uptake of Organic Farming: Accounting for Heterogeneities among Irish Farmers.” Ecological Economics 88:11–19.

Lohr, L., and T.A. Park. 2003. “Improving Extension Effectiveness for Organic Clients: Current Status and Future Directions.” Journal of Agricultural and Resource Economics 283:634–650.

Marasteanu, I.J., and E.C. Jaenicke. 2015. “The Role of US Organic Certifiers in Organic Hotspot Formation.” Renewable Agriculture and Food Systems 453:485–521.

Marasteanu, I.J., and E.C. Jaenicke. 2016. “Hot Spots and Spatial Autocorrelation in Certified Organic Operations in the United States.” Agricultural and Resource Economics Review 453:485–521.

McEvoy, M. 2015. “Sound and Sensible Initiative Projects Simplify Organic Certification.” Washington, DC: U.S Department of Agriculture, October. Available online: https://www.usda.gov/media/blog/2015/10/27/sound-and-sensible-initiative-projects-simplify-organic-certification

Mercaris. 2017. “2016 Organic and Non-GMO Acreage Report.” Silver Spring, MD: Mercaris.

Onozaka, Y., and D.T. McFadden. 2011. “Does Local Labeling Complement or Compete With Other Sustainable Labels? A Conjoint Analysis of Direct and Joint Values for fresh Produce Claims.” American Journal of Agricultural Economics 93:689–702.

Organic Trade Association. 2017. “Robust Organic Sector Stays on Upward Climb, Posts New Records in U.S. Sales.” Available online: https://www.ota.com/news/press-releases/19681

Paggi, M.S. 2016. “The Use of Crop Insurance in Specialty Crop Agriculture.” Choices. Quarter 3. Available online: http://www.choicesmagazine.org/choices-magazine/theme-articles/crop-insurance-in-the-20182019-farm-bill/the-use-of-crop-insurance-in-specialty-crop-agriculture

Pimentel, D.P., J. Hepperly, J. Hanson, D. Doubs, and R. Seidel. 2005. “Environmental, Energetic, and Economic Comparisons of Organic and Conventional Farming Systems.” Bioscience 55:573–582.

Press, M., E.J. Arnould, J.B. Murray, and K. Strand. 2014. “Ideological Challenges to Changing Strategic Orientation in Commodity Agriculture.” Journal of Marketing 78:103–119.

Sexton, R.J. 2013. “Market Power, Misconceptions, and Modern Agricultural Markets.” American Journal of Agricultural Economics, 95(2):209–219.

Sherrick, B.J., and G.D. Schnitkey. 2013, May 30. “Crop Insurance Program Losses in Perspective.” FarmDoc Daily. Available online: http://farmdocdaily.illinois.edu/2013/05/crop-insurance-losses-perspective.html

Sierra, L., K. Klonsky, R. Strochlic, S. Brodt, and R. Molinar. 2008. “Factors Associated with Deregistration among Organic Farmers in California.” Davis, CA: California Institute for Rural Studies.

Stephenson, G., L. Gwin, C. Schreiner, and S. Brown. 2017. “Breaking New Ground: Farmer Perspectives on Organic Transition.” Corvallis, OR: Oregon Tilth and Oregon State University, Center for Small Farms & Community Food Systems, March.

Sutherland, L.A. 2013. “Can Organic Farmers Be Good Farmers? Adding the Taste of Necessity to the Conventionalization Debate.” Agriculture and Human Values 30:429–441.

U.S. Department of Agriculture. 2010. 2007 Census of Agriculture: Organic Production Survey (2008), Volume 3, Special Studies, Part 2. Washington, DC: U.S. Department of Agriculture, National Agricultural Statistics Service, AC-07-SS-2, July. Available online: http://www.agcensus.usda.gov/Publications/2007/Online_Highlights/Organics/ORGANICS.pdf

U.S. Department of Agriculture. 2013a. National Organic Program Regulations. Washington, DC: U.S. Department of Agriculture, Agricultural Marketing Service. Available online: www.ams.usda.gov/nop

U.S. Department of Agriculture. 2013b. “Table 4. Certified Organic Producers, Pasture, and Cropland. Number of Certified Operations, by State, 2000–11. Total Acreage of Certified Organic Pasture and Cropland by State, 1997 and 2000–11.” Organic Production. Washington, DC: U.S. Department of Agriculture, Economic Research Service. Available online: http://www.ers.usda.gov/data-products/organic-production.aspx

U.S. Department of Agriculture. 2014a. 2012 Census of Agriculture: Organic Production Survey (2014), Volume 3, Special Studies, Part 4. Washington, DC: U.S. Department of Agriculture, National Agricultural Statistics Service, AC-12-SS-4, April. Available online: http://www.agcensus.usda.gov/Publications/2012/Online_Resources/Organics/ORGANICS.pdf

U.S. Department of Agriculture. 2014b. Summary of Business Reports and Data. Washington, DC: U.S. Department of Agriculture, Risk Management Agency. Available online: www.rma.usda.gov/data/sob/scc

U.S. Department of Agriculture. 2016. Certified Organic Survey, 2015 Summary. Washington, DC: U.S. Department of Agriculture, National Agricultural Statistics Service, September. Available online: http://usda.mannlib.cornell.edu/usda/nass/OrganicProduction//2010s/2016/OrganicProduction-09-15-2016.pdf

U.S. Department of Agriculture. 2017a. National Organic Grain and Feedstuffs Bi-Weekly Report. Washington, DC: U.S. Department of Agriculture, Agricultural Marketing Service. Available online: https://www.ams.usda.gov/mnreports/lsbnof.pdf

U.S. Department of Agriculture. 2017b. Global Agricultural Trade System. Washington, DC: U.S. Department of Agriculture, Foreign Agricultural Service. Available online: https://apps.fas.usda.gov/gats/default.aspx

U.S. Department of Agriculture. 2017c. Quickstats. Washington, DC: U.S. Department of Agriculture, National Agricultural Statistics Service. Available online: www.nass.usda.gov/Quick_Stats/

Veldstra, M.D., C.E. Alexander, and M.I. Marshall. 2014. “To Certify or Not to Certify? Separating the Organic Production and Certification Decisions.” Food Policy 49:429–436.

Whoriskey, P. 2017a, May 1. “Why Your ‘Organic’ Milk May Not Be Organic.” Washington Post. Available online: https://www.washingtonpost.com/business/economy/why-your-organic-milk-may-not-be-organic/2017/05/01/708ce5bc-ed76-11e6-9662-6eedf1627882_story.html

Whoriskey, P. 2017b, May 12. “The Labels Said ‘Organic.’ But These Massive Imports of Corn and Soybeans Weren’t.” Washington Post. Available online: http://www.washingtonpost.com/business/economy/the-labels-said-organic-but-these-massive-imports-of-corn-and-soybeans-werent/2017/05/12/6d165984-2b76-11e7-a616-d7c8a68c1a66_story.html