Source: IRS tax filing data, calculations by the authors.

As America ages, households and local economies are becoming more dependent on pensions as a source of income. In 1990, 15.8% of all households filing income tax returns declared some pension income, and in 2014 that share increased to 20.7% (Figure 1). Households with pension income, however, tend to have additional sources of income, such as dividend and interest payments on private savings, social security allotments, or even wage and salary income. In 1990, only 6.2% of total Adjusted Gross Income (AGI, from IRS data) came from pension payments, but that share increased to 11.2% in 2014. Nationally, the average nominal pension payment went from $11,940 in 1990 to $19,999 in 2014. These trends, however, do not come without significant risks: Pension funds, both private and public, are under pressure.

Many pension plans have been underfunded, with both private employers and state and local governments deferring payments. At the same time, the lingering effects of the Great Recession and record low interest rates have contributed to pension funds being unable to meet their obligations (USGAO, 2013). The past standard for projecting pension fund balances assumed unrealistic growth rates of 7.6%, while actual realized annual returns averaged only 4.1% between 2000 and 2017 (Damodaran, 2017). The U.S. multiemployer pension funds had $1.8 billion in total assets against $44.2 billion in total discounted liabilities as of September 30, 2014 (PBGC, 2016).

Approximately 10 million workers and retirees are covered by multiemployer pension plans, and approximately 10% of them have plans that could run out of money in the next 20 years (Marte, 2016). An analysis of 124 multiemployer funds found an average funding ratio of only 47% in 2014, a ratio that has deteriorated (Moody’s Investors Service, 2016). Plan bankruptcy could also bankrupt the fund that guarantees multiemployer pensions, the Pension Beneficiary Guarantee Corporation (Fletcher, 2014; Horowitz, 2015; Marte, 2016). Moody’s found that the Pension Beneficiary Guarantee Corporation fund had assets of only $2 billion against liabilities of $54 billion in fiscal year 2015.

The risk of pension fund bankruptcies is a cause for concern. As an example, the Central States Pension Fund—a multiemployer fund with a main body of pensioners in Michigan, Wisconsin, Minnesota, Missouri, Texas and New York—was on the brink of declaring insolvency. Several companies that paid into this multiemployer fund on behalf of their teamster employees cut back on payments or went bankrupt, forcing the fund to pay out $2 billion more annually in benefits than it receives in contributions. Because of this, it was expected to run out of money in 10–15 years (Marte, 2016). Under 2014 legislation that allows multiemployer plans to reduce benefits to improve solvency, Central States Pensions applied to reduce benefits by an average of 23% for the 407,000 individuals covered by the plan. This legislation is a major change from 40 years of shielding workers’ pensions (Fletcher, 2014).

While 13% of Americans were 65 and over in 2010, outside of metropolitan and micropolitan areas they account for 17.2% of the population (Werner, 2011). Thus, the most rural areas are more exposed to changes in sources of retirement income. Furthermore, since rural earnings lag urban earnings, retirees in rural communities are already strained by lower retirement incomes (USDA, 2016b). Relatively high unemployment and underemployment in rural areas also mean fewer informal and formal work opportunities for those facing pension cuts (USDA, 2016c). While many rural employees are not covered by private pensions, government provides 20% of earnings in nonmetropolitan areas, compared with 16% in metropolitan areas (USDA, 2016a; USDC-BEA, 2016). This increases nonmetropolitan dependence on public pensions, which in many cases are also underfunded. The risks to personal incomes because of the higher percentage of retirees, generally lower retirement incomes, and fewer economic opportunities, may in turn pose disproportionate risks to rural economies.

The limited available research focuses exclusively on the impacts of pension reductions on households; this study focuses on the impacts of pension reductions on local economies. Using pension and annuity income data from the Internal Revenue Service, we are able to provide more detailed insights into rural America’s exposure to pension risks. We use a post-recession, four-year average (2011–2014) to minimize the influence of year-to-year fluctuations and achieve a more stable representation.

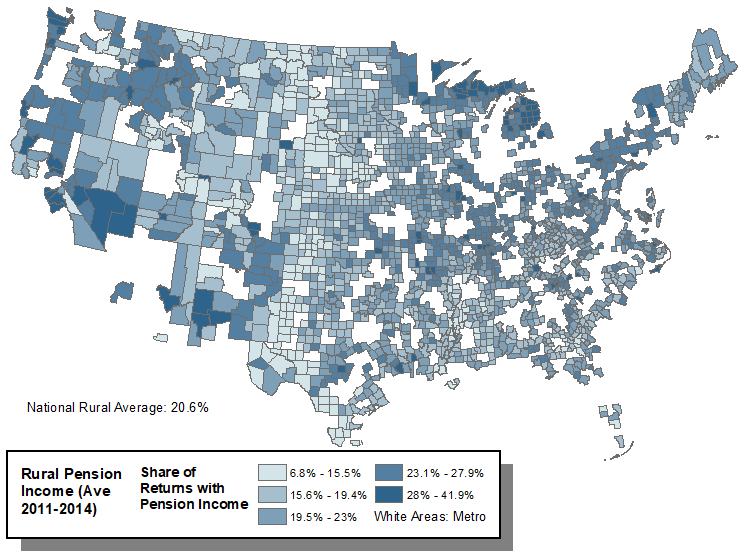

Notes: Metro areas removed from map.

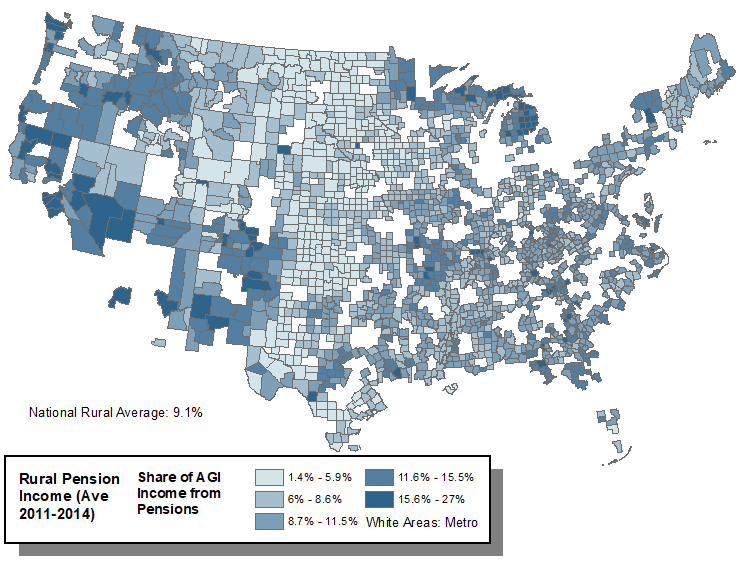

Notes: Metro areas removed from map.

Notes: Metro areas removed from map.

Consider first the share of federal tax returns that declare some pension income across rural (nonmetropolitan) counties (Figure 2). In a typical rural county, 20.6% of all returns declare some pension income, with a range of 6.8%–41.9%. It is important to note that not all pensioners are solely dependent on pensions for income. The share of AGI from pensions averages 9.1% across rural America, with a range of 1.4%–27% (Figure 3). The income flowing into households from pensions, however, can be significant. The average pension income per tax return that declared pensions was $19,042, with a range of $9,118–$56,807 (Figure 4).

A visual analysis of the spatial patterns for these simple measures of dependence on pensions, coupled with a range of spatial clustering tools (for example, the Getis-Ord and Local Moran statistics), suggests that three parts of the rural United States are particularly dependent on pensions for income: the traditional manufacturing belt from southern New England to Minnesota, the Pacific Coast, and smaller pockets in the south that are traditionally thought of as retirement destinations. The Great Plains, much of the South (other than a few pockets along the coasts), and the Mountain West are less dependent on pensions. The general spatial patterns of dependence on pensions for income tells us that, despite some parts of rural America being more at risk of pension fund reductions or defaults, this is not a regional but rather a national issue that needs to be addressed at the national level.

To gain a finer understanding of the dependence of rural communities on pension income, we group U.S. counties using three different USDA (2016a) classifications: the urban-rural spectrum, economic base, and sociodemographics. In the urban-rural spectrum analysis, we classify counties as metropolitan, nonmetropolitan adjacent, and nonmetropolitan remote (nonadjacent, nonmetropolitan). The third set of comparisons is across retirement destination counties, low education, and persistent poverty, among others. These latter classifications are often referred to as “policy codes.”

Metropolitan counties have the highest average pension income ($21,558), and remote counties have the lowest ($18,628). However, the share of AGI from pensions is slightly higher in adjacent nonmetropolitan counties (9.1%) than in metropolitan and remote counties (8.5%), and the differences are statistically significant (based on an F-test of the differences). The percentage change in average pension income from 2011 to 2014 is not significantly different for the three areas.

Looking across different industry bases, we find that rural counties dependent on farming (391 of 444 are nonmetropolitan counties), mining (183 of 219 are nonmetropolitan counties), and manufacturing (351 of 506 are nonmetropolitan counties) have the lowest share of AGI from pensions and lowest average per pension payment. This is not surprising given that farmers tend to be self-employed and farm workers are generally not covered by pensions. While we commonly think of mining as coal or oil, which tend to be large operations, there are many types of smaller operations in rural areas, such as quarrying. Many of these workers may not have a pension. The same is true of many small and mid-sized manufacturing firms in rural areas.

Recreation counties (288 of 332 are nonmetropolitan counties) are the highest on the measures of pension dependence, followed by federal and state government (351 of 506 nonmetropolitan counties) and nonspecialized counties (585 of 1,237 are nonmetropolitan counties). These differences among the county economic types are statistically significant. Recreation counties likely have a high percentage of well-off retirees who have moved into the area, contributing to the importance of pensions. The importance of public pensions in rural areas is demonstrated by their importance in counties that are dependent on federal and state governments.

We also compare counties with specific sociodemographic characteristics to all other counties (nonmetropolitan and metropolitan). The USDA (2016a) defines retirement destination counties (193 of 442 are nonmetropolitan counties) as those where net in-migration caused the population of individuals age 60 and older to grow 15% or more from 2000 to 2010. Based on the concentration of retirees, it would be expected that these counties would have higher dependence on pension income than other counties. By all of the measures, retirement counties are significantly more dependent on pension income than all other counties. It should be noted that there is some overlap of retirement counties with recreation-dependent counties, discussed above, which are the most pension dependent. Average pensions, pensions as a share of AGI, and the share of filings with pensions all appear higher in the recreation than in the retirement counties. This may suggest that counties with the highest recreation amenities attract retirees with higher incomes because there are likely premiums, such as higher housing prices, for living near these amenities.

In low-education counties, 20% or more of the population age 25–64 lack a high school diploma or GED based on the 2008–2012 five-year average (USDA, 2016a). Of these counties, 367 of 467 are non-metropolitan.. Low-education counties have significantly lower dependence on pension income than other counties, but the difference in pension income change is not statistically significant. Given that average education rates change slowly, it is likely that these counties have had low education levels for many years and that those with lower skills are less likely to have jobs covered by pensions.

Low-employment counties (720 of 906 are nonmetropolitan counties) are defined based on a five-year 2008–2012 average. In these counties, less than 65% of the population of prime working age, 25–64, were employed. These counties have a higher share of filings with pension income. Pensions make up a higher share of AGI in these counties, and the average pension per return with a pension is also significantly higher than for all other counties. In tandem, this suggests that these counties are relatively more dependent on pension income, but overall income levels are still low. These counties may be particularly exposed to the risks of underfunded pension funds.

In counties with persistent poverty (301 of 353 are nonmetropolitan counties), at least 20% of the population lives below the poverty line, based on the 1980–2000 decennial censuses and the American Community Survey 2007–2011 five-year average. These counties have a significantly lower share of filings with pension income and lower pension income per return with pension income than all other counties. On the other hand, in these counties, a significantly higher share of AGI is pension income. With pensions contributing a higher share of AGI, decline in pension income in a persistent-poverty county can have a notable negative impact at the margin. There is overlap between the low-education, low-employment, and persistent-poverty counties. In low-employment and persistent-poverty counties, the share of AGI from pensions is significantly higher than in other counties, suggesting that families in these counties may be more sensitive to changes in pension income than those in other counties.

Population-loss counties (467 of 529 are nonmetropolitan) have had declining populations in each decennial census, 1990–2010. These counties are concentrated in the Great Plains states and show a statistically significant lower dependence on pensions than all other counties. There is substantial overlap between population-loss and farming counties. As noted above, many farmers and farm workers do not have pensions. It is also possible that those with pensions leave the county at retirement, contributing to the population loss.

Taken together, these results suggest that rural counties across the United States are exposed to pension system failures. Geographic pockets of higher dependence correspond with our testing across different types of counties. Rural areas that are traditionally dependent on farming are at less risk to pension failures, but higher amenity areas that have promoted recreation and retirement migration may be at greater risk. This raises the question of what the potential economic impact might be if pensions fail or are forced to make significant reductions in payments.

We ask a simple question: What would be the economic impact of a 50% reduction in pension income? To answer this question, we use a family of regional input-output models (IMPLAN) for states in the North Central region and a handful of representative counties. Again, we use the IRS pension and annuity income data to build our scenarios. For example, consider Iowa, which had over $5.3 billion in pension payments to individuals in 2014. Of all federal income tax returns, 20.8% reported pension income and 6.4% of AGI income came from pensions. The average pension payment was $17,823. A 50% reduction in pensions, about $2.65 billion, would cost Iowa 20,830 jobs, $4.1 billion in total income, and $164.9 million in state and local government revenue. The results of this analysis for the 12 North Central states are provided in Table 1. It is clear that while the largest states—such as Illinois, Michigan and Ohio—are at risk of experiencing the largest economic impacts, even smaller states are at risk. In South Dakota, a loss of some $760 million from a 50% reduction in pension payments would cost the state 6,410 jobs, $1.2 billion in total income, and $46.3 million in state and local government revenues.

To further refine the potential impact of at-risk pensions, we select nine representative rural (nonmetropolitan) counties from Michigan, Minnesota, Missouri, and Wisconsin. We use two criteria: i) a mix of rural counties adjacent to metropolitan counties and nonadjacent (remote) and ii) a mix of counties with small (population less than 40,000) and medium population. These counties include Newaygo and Roscommon in Michigan, Meeker and Winona in Minnesota, Adair and Johnson in Missouri, and Clark, Grant, and Marinette in Wisconsin (see appendix Table A1 for descriptive statistics). A simple summary of the effects of a hypothetical 50% reduction in pension income on these counties’ economies is provided in Table 2.

Johnson County, Missouri, has the largest potential loss of pension income: A 50% reduction would be just over $58 million and result in a loss of 308 jobs and about $77.9 million in total income. The least exposed county is Clark County, Wisconsin, where a 50% reduction in pension income would results in 81 jobs being lost and a total of $24.5 million in total income. This 50% loss represents a loss of 4.4% of total personal income for Johnson County but only 1.9% for Clark County. Roscommon County would see the largest negative percentage impact of a 50% loss of pension income, experiencing a total loss of 8.2% of total personal income. The implicit income multipliers range from 1.278 for Clark County, Wisconsin, to 1.422 for Adair County, Missouri. That means that for every dollar of pension income lost, an additional 28–42 cents in total income would be lost to the county through the multiplier effect.

Rural pensioners may be hit hard by any reduction to income from public pensions and single- or multiemployer private pension shortfalls. Due to overly optimistic outlooks on revenue growth and declining contributions, an increasing number of pension funds are at risk of insolvency. If pension funds become insolvent, pensioners are forced to absorb significant reductions in payments. In an effort to retain solvency of the Pension Benefit Guaranty Corporation’s Multiemployer Program, the Multiemployer Pension Reform Act of 2014 authorizes such plan administrators to petition contributors for reduced benefits if fund insolvency is deemed inevitable. Despite higher PBGC rates per participant, the PBGC has $2 billion in assets to cover $54 billion in future liabilities (Moody’s Investor Services, 2016).

We find that pension benefits are highest in urban areas, while rural-adjacent counties tend to exhibit higher shares of adjusted gross income made up of pensions. Rural counties steeped in farming, mining, and manufacturing are less dependent on pension incomes. This may reflect the smaller-scale businesses with no or few pension offerings that operate in rural counties. Alternatively, recreational counties and those with significant dependence on state and local government tend to be more dependent on pension incomes, where recreation counties likely exhibit a pattern of retiree migration to amenity-rich communities. This is evident when looking at both USDA-designated rural and metropolitan retirement destinations.

The findings highlight the importance of retirement income not just to the individual retiree but also to the local economy and local government. Of the counties selected in this study, the share of income tax returns with pension or annuity incomes ranged from 16% to 40%, comprising 6%–23% of total household adjusted gross income. As rural communities continue to grey, America’s heartlands will increasingly rely on pension incomes to drive their economies. The loss of 50% of pension income could cost our sample of rural counties from 81 (Clark County, WI) to 308 jobs (Johnson County, MO). For rural communities that are struggling to rebuild their economies in the wake of the Great Recession, these job losses would be significant.

Rural policy makers need to be aware of the exposure that many of their communities face with the serious pension risks across the United States. If pension funds default on their payments or are forced to make significant reductions in benefit payments to remain solvent, many rural communities will feel the impacts. Rural policy makers need to understand the extent of their communities’ exposure and think through strategies to help mitigate the fallout of potential pension reductions.

Damodaran, A. 2017. Historical Returns: Stocks, T.Bonds & T.Bills with Premiums: 1928–Current. Available online: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

Fletcher, M. 2014, December 14. “Congressional Leaders Hammer Out Deal to Allow Pension Plans to Cut Benefits.” The Washington Post.

Horowitz, C. 2015, October 19. “Teamsters Central States Pension Fund Puts PBGC in Jeopardy.” National Legal and Policy Center. Available online: http://nlpc.org/2015/10/19/teamsters-multiemployer-pension-fund-pbgc-jeopardy/

Internal Revenue Service (IRS). 2016. Tax Statistics. Washington, DC. Available online: https://www.irs.gov/statistics

Marte, J. 2016, April 20. “One of the Nation’s Largest Pension Funds May Soon Cut Retiree’s Benefits.” The Washington Post.

Moody’s Investors Service. 2016, July 13. Multiemployer Pensions Remain Substantially Underfunded, Stressing Sponsors, Agencies. Available online: https://www.moodys.com/research/Moodys-Multiemployer-pensions-remain-substantially-underfunded-stressing-sponsors-agencies--PR_352064

Pension Benefit Guaranty Corporation (PBGC). 2016, March. “PBGC Insurance of Multiemployer Pension Plans: A Five Year Report.” Washington, DC. Available online: http://pbgc.gov/documents/Five-Year-Report-2016.pdf

U.S. Department of Agriculture (USDA). 2016a. County Typology Codes. Economic Research Service, Washington, DC. Available online: https://www.ers.usda.gov/data-products/county-typology-codes/

U.S. Department of Agriculture (USDA). 2016b. Rural America at a Glance, 2016 Edition. Economic Research Service, Washington, DC. Available online: https://www.ers.usda.gov/webdocs/publications/eib162/eib-162.pdf

U.S. Department of Agriculture (USDA). 2016c. Rural Employment and Unemployment. Economic Research Service, Washington, DC. Available online: https://www.ers.usda.gov/topics/rural-economy-population/employment-education/rural-employment-and-unemployment/

U.S. Department of Commerce, Bureau of Economic Analysis (USDC-BEA). 2016. Regional Economic Accounts. Washington, DC. Available online: https://www.bea.gov/regional/

U.S. Government Accountability Office (USGAO). 2013. Private Pensions: Timely Action Needed to Address Impending Multiemployer Plan Insolvencies. Washington, DC. Available online: http://www.gao.gov/products/GAO-13-240

Werner, C.A. 2011. The Older Population: 2010. Washington, DC: U.S. Department of Commerce, Bureau of the Census, 2010 Census Briefs, C2010BR-09. Available online: https://www.census.gov/prod/cen2010/briefs/c2010br-09.pdf