Though U.S. consumers have experienced many dramatic pivots in food availability, perhaps none caused as much difficulty for families as the infant formula crisis of 2022. Store shelves across the United States were sometimes barren, inducing panic among parents and generating clamor for policy reform. The infant formula shortage reveals shortcomings in the U.S. system, emphasizing critical inequities in food and nutrition access.

Reliable access to formula plays an important role in infant nutrition. Despite this importance, economic issues stemming from the pandemic (disrupted supply chains and labor shortages) have resulted in infant formula being in short supply in recent years (Paris, 2022). Shortages were further exacerbated in February 2022, when Abbott Nutrition—the largest infant formula manufacturer in the country—voluntarily closed its Sturgis, Michigan facility and recalled several lines of powdered formula in response to concerns over bacterial contamination at the facility and reports of four infant hospitalizations and two infant deaths (White House, 2022a). Abbott voluntarily recalled some Similac, EleCare, and Alimentum product lines produced at its Sturgis facility, and the U.S. Food and Drug Administration (FDA) further announced a recall of Similac PM 60/40, Abbott’s specialized low-mineral infant formula. By late spring 2022, reported out-of-stock rates were over 30% nationwide and as high as 40% in some states (Paris, 2022).

While the popular press has thoroughly detailed how the crisis emerged, fewer reports have focused on linkages between the industry structure and federal policies that might have contributed to recent shortages or limited U.S. capacity to expand production and imports. This article discusses the U.S. infant formula market structure, the role that U.S. import policies and regulations might play in constraining supply, and the USDA's Special Supplemental Nutrition Program for Women, Infants, and Children (WIC), which purchasesmuch of the infant formula consumed in the United States. By considering market structure, import policies, and WIC, our overall goal is to highlight issues ripe for qualitative and empirical analysis from agricultural and applied economists.

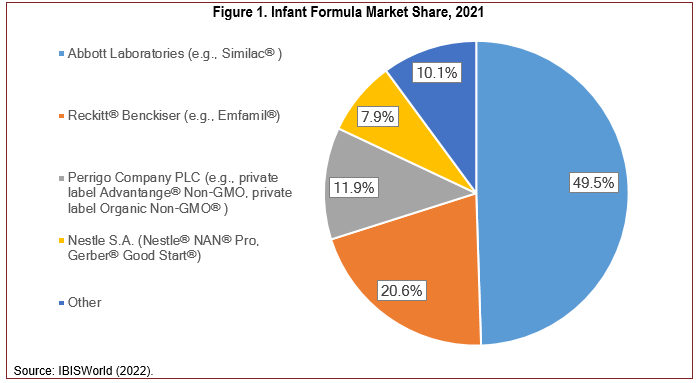

Figure 1. Infant Formula Market Share, 2021

U.S. infant formula production is highly concentrated, generating annual revenues of $2.1 billion in 2021 (IBISWorld, 2022). In 2021, the four largest companies accounted for about 90% of industry sales. Figure 1 shows the major companies, the brands they sell, and their estimated 2021 market shares. Market concentration has been common in the industry for some time, as the three largest infant formula companies accounted for 98% of all formula sales in 2008 (Oliveira, 2011). In addition to this intense market concentration, there are currently only 21 infant formula manufacturing facilities in the United States (IBISWorld, 2022). While there may be economies of scale gained by a few large production facilities, the concentration also creates concerns about the resiliency of the supply chain. This risk was highlighted in the winter of 2022, when Abbott Laboratories voluntarily closed their facility in Sturgis, Michigan. This exacerbated ongoing supply chain strains caused by the COVID-19 pandemic, inducing a well-documented infant formula shortage. Reckitt’s market share has since climbed dramatically through 2022 and is now estimated to be as high as 60% of the infant formula market, with Abbott’s share declining to 20% (Creswell and Corkery, 2022). Abbott resumed production at its Michigan plant in August 2022 and will likely recapture some of its lost market share (Oxenden, 2022).

It is important to note that all four major infant formula companies are large multinational companies with diverse product portfolios. Abbott is headquartered in Illinois and is publicly traded on the New York Stock Exchange (NYSE) (ABT). In 2021, Abbott had $43.1 billion in worldwide sales and sold products ranging from medical devices to pharmaceuticals, including over-the-counter COVID-19 tests (Abbott, 2021). Reckitt is headquartered in England and is publicly traded on the London Stock Exchange (RKT). In 2021, Reckitt had approximately $15 billion in annual revenues and products spanning the lifecycle from Durex healthcare products to infant and adult nutrition products (Reckitt, 2021). Perrigo is headquartered in Ireland for tax purposes and Michigan for operations, is publicly traded on the NYSE (PRGO), and has net sales of approximately $4 billion (Perrigo, 2021). They primarily specialize in private label over-the-counter pharmaceuticals (e.g., cold medicines, pain medicine, digestive health). Nestlé® is headquartered in Switzerland, trades on the Swiss Exchange (NESN), and had approximately $90 billion in revenue in 2021 from sales of a diverse assortment of products from powdered and liquid beverages to pet care, ice cream and confectionary, water, and nutrition and health science related products. Thus, the four dominant U.S. infant formula manufacturers provide a wide range of products within their multibillion-dollar portfolios.

U.S. infant formula makers may be unlikely to devote additional resources to expanding or enhancing their facilities and products. Infant formula sales have been relatively stagnant over the past decade as breastfeeding rates have increased alongside a declining U.S. birthrate (IBISWorld, 2022). Furthermore, the Federal Food, Drug, and Cosmetics Act (FFDCA), which is primarily enforced by the FDA, includes regulations specific to infant formulas regarding nutritional content and labeling and requires manufacturers to notify the FDA prior to marketing new products. These regulations apply not only todomestically produced formula but also imports (Sheikh et al., 2022). Consequently, U.S. companies are less likely to invest in new infant formulas, particularly when other products in their portfolio are more profitable and experience fewer regulatory hurdles.

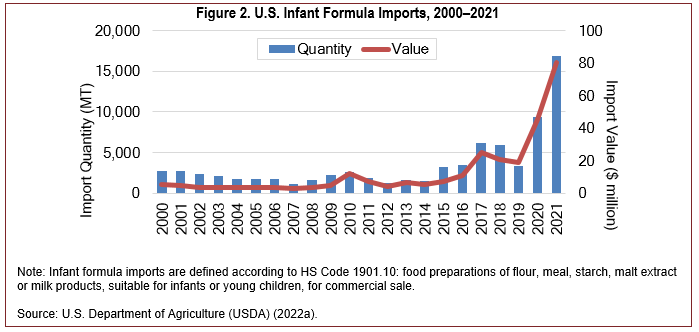

Note: Infant formula imports are defined according

to HS Code 1901.10: food preparations of flour,

meal, starch, malt extract or milk products, suitable

for infants or young children, for commercial sale.

Source: U.S. Department of Agriculture (USDA)

(2022a).

The FDA plays a critical role in ensuring that infant formula in the United States is safe and nutritionally adequate. By design, the statutory and regulatory requirements enforced by FDA make it difficult for new products, foreign or domestic, to be introduced to the market. Given the recent shortage, however, FDA issued new guidance that allowed for

“case-by-case determinations about whether to exercise enforcement discretion to allow the introduction into interstate commerce (including importation) of infant formula that is safe and nutritionally adequate, but that may not comply with all statutory and regulatory requirements.” (FDA, 2022a)

This enforcement discretion policy is clearly designed to increase the supply of infant formula and suggests a more favorable policy toward imports, at least during the current period of relative short supplies.

The data reported in this section suggest that the statutory and regulatory requirements enforced by the FDA makes importing infant formula prohibitive. This is, in part, evidenced by domestic production accounting for more than 98% of total demand (FDA, 2022b). During the last decade, U.S. production averaged 524,000 metric tons (MT) annually, while imports averaged only 5,000 MT (Casey, 2022).[1] What is interesting, however, is that U.S. regulations actually allow for imported infant formula so long as products meet nutritional and labeling standards and the foreign facilities that produce, store, or handle products are registered with the FDA and provide the FDA with prior notice of incoming shipments (FDA, 2022c). Very few domestic companies, to say nothing of foreign companies, have been given FDA approval.

The easing of statutory and regulatory procedures raises concerns about the role of imports in satisfying current and future demand. From 2000 to 2009, U.S. infant formula imports averaged less than $4 million annually, or less than 2,000 MT (see Figure 2). It has only been within the last 5 years that imports have significantly increased. Record years occurred in 2020 and 2021, when imports increased by $26 million and $35 million, respectively, reaching a high of $80.2 million (nearly 17,000 MT). This represents a 2,000% increase compared to imports during the previous decade. A more detailed examination of the data reveals that the increase in 2021 was primarily due to unprecedented imports from Mexico, valued at $50 million (USDA, 2022a). Since the child population in the United States (ages 0–5) has been relatively steady at 25 million children over the last 2 decades (2000–2021) (U.S. Census Bureau, 2021), this increase is likely due to factors other than increased demand.

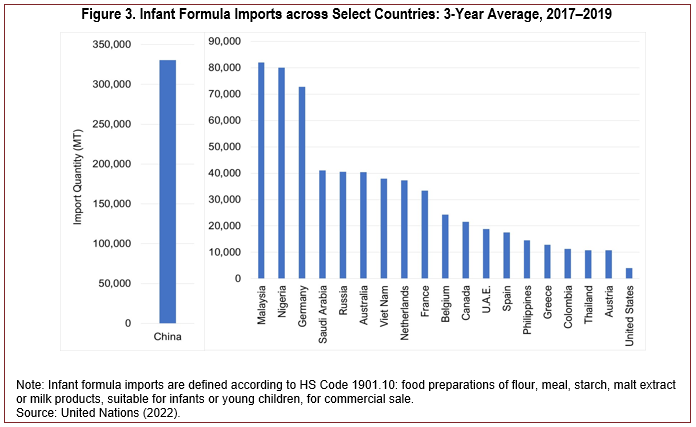

A comparison of imports across countries supports the claim that U.S. markets are relatively restricted. Figure 3 shows infant formula imports across select countriesprior to the pandemic. Note how small U.S. imports are(only 4,000 MT) compared to many countries around the world. During 2017–2019, China imported over 300,000 MT per year on average, whereas countries like Malaysia and Nigeria averaged over 80,000 MT, and Russia 41,000 MT. Even comparable high-income countries in the EU averaged significantly more imports than the United States: Germany, 73,000 MT; the Netherlands, 37,000 MT; and France, 33,000 MT. Despite Australia having less than one-tenth of the U.S. population, it imported 10 times more infant formula than the United States (40,000 MT). Year-to-date imports (January–July) in 2022 ($132 million, 20,000 MT) suggest that recent actions by the FDA may have resulted in increased imports; as of July 2022, imports were up by 182% compared to the previous year (USDA, 2022a). This places the United States on pace to import as much as Australia and other high-income countries. However, the recent increase is still relatively small by comparison on a per capita basis.

Note: Infant formula imports are defined according to

HS Code 1901.10: food preparations of flour, meal,

starch, malt extract or milk products, suitable for infants

or young children, for commercial sale.

Source: United Nations (2022).

The Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) is a targeted nutrition assistance program that provides specialized food packages to participating women, infants, and children as well as nutrition education services, including breastfeeding promotion (Aussenberg, 2017). The WIC program reports that it serves half of all infants born in the United States (USDA, 2022b). Thus, the program plays an important role in infant nutrition, which in the first year of life comes predominantly from breast milk or infant formula.

WIC eligibility is determined based on financial, categorical, and nutritional risk criteria (Aussenberg, 2017). Financial eligibility is based upon the household’s income, which can be at most 185% of the federal poverty line (FPL). In 2020, however, 64.3% of participants had incomes at or below the poverty line (Kline et al., 2022). There are five major types of nutrition risk recognized by the program that fall into two broad categories capturing medically based risk and diet-based risk. Nutrition risk is determined by a competent professional authority—such as a physician, nutritionist, or nurse—during the application process (Aussenberg, 2017). Finally, participants must belong to one of the following categories: pregnant, postpartum, and breastfeeding women; infants; or children under the age of five.

The quantity of infant formula available to WIC families depends on the age of the infant and level of breastfeeding and is set by the federal government. However, state agencies have discretion in determining specific brands, types, and sizes allowed in WIC food packages, including the discretion to issue infant formula in concentrated liquid or powdered form. This discretion is an important tool for cost containment, which has been required by federal law since the 1989 Child Nutrition and WIC Reauthorization Act. Competitive bidding for WIC infant formula contracts has been the primary method through which states, or alliances of states, manage infant formula costs (Aussenberg, 2017; Oliveira and Frazao, 2015). In this process, infant formula manufacturers submit a sealed bid to states, or state alliances, with the rebate, expressed as apercentage of the wholesale price, and the contract is awarded to the manufacturer with the lowest monthly net price, calculated as wholesale price less rebate (Oliveira and Frazao, 2015). WIC participants may redeem their benefits at WIC-authorized retailers only on the state’s contracted brand; WIC then reimburses food retailers for the retail price of the infant formula and the infant formula manufacturer with the state contract reimburses WIC based on the agreed-upon rebate. Thus, the cost of infant formula to WIC is the net price plus any retail markup. Historically, WIC has been able to obtain infant formula below retail prices, with rebates that can exceed 90% of the wholesale price (Oliveira and Frazao, 2015). Although the competitive bidding process is an effective tool for cost containment, it also limits WIC participants’ ability to substitute between brands and package sizing during shortages.

Considering the effect of the WIC program on the infant formula market more broadly, there is substantial evidence documenting the effects of state contracting on the market share of an infant formula manufacturer within a state (Oliveira and Frazao, 2015). Choi et al. (2020) found that 1 year following a contract change, the volume of sales of WIC infant formula for the new brand increased by 322%. They also found a significant increase in sales of the new brand for non-WIC eligible products, suggesting spillover effects. Prior research suggests that these spillover effects may occur because the new brand receives more shelf space at supermarkets or because consumers interpret the WIC-approved label on the WIC brand as a signal of government endorsement (Oliveira and Frazao, 2015).

The WIC program may also result in higher prices for infant formula (Rojas and Wei, 2019; Oliveira and Frazao, 2015). There are two potential mechanisms through which the WIC program could increase infant formula prices. First, since the WIC program provides free infant formula to the most price-sensitive consumers in the marketplace, it may allow manufacturers and retailers to charge higher prices to remaining consumers (Oliveira and Frazao, 2015). Second, awarding a state contract to a single manufacturer increases market power, resulting in higher prices for the entire market. Some early evidence suggested that WIC increased both wholesale prices and retail markups, resulting in higher prices for both WIC and non-WIC participants (Oliveira and Frazao, 2015). Rojas and Wei (2019) more recently found that both the winning manufacturer and losing manufacture increased prices after a change in a state’s contract.

To increase infant formula supply, the Biden administration has implemented policies to address the underlying issues that have contributed to the shortage. Industry concentration is a major reason why the closure of a single manufacturing could be so disruptive. To address this issue, the USDA has provided states additional flexibility to expand the brands and sizes of infant formula available to WIC participants (Sheikh et al., 2022). For instance, the USDA has added flexibility to waive rules that limit WIC participants from purchasing competing brands during supply chain disruptions (White House, 2022b). The FDA is also limiting red tape and regulatory hurdles to increase imports. However, recent import increases mostly include foreign affiliates of the companies mentioned in this report (e.g., Reckitt, Nestlé’s, Abbott).

The current shortage has also resulted in calls to either lower or abolish the tariffs on imports (Casey, 2022). However, non-tariff barriers (i.e., statutory and regulatory requirements) are far more likely to discourage foreign producers since tariffs are relatively low: The most-favored-nation (MFN) tariff rate for infant formula ranges from 14.9% to 17.5% depending on content. Beyond a certain import threshold, tariffs on most infant formulas increase to $1.04/kg plus the 14.9% tariff, and some lower priced formulas could be subject to additional tariffs. Overall, the average effective tariff rate on infant formula is around 25%, which is by no means prohibitive (Casey, 2022). While abolishing the tariff could make it easier for foreign companies with FDA approval, it appears that the FDA approval process is far more restrictive.

Calls for policy changes emphasize the need for additional empirical research in an area as important as infant nutrition. For instance, there is a clear need to better understand the degree to which trade policy (tariffs or otherwise) affects firm participation, product availability, and prices. Additionally, it would be informative to compare regulatory policies globally, ranking the relatively restrictiveness of the U.S. market. Finally, empirical analyses of industry concentration, either examining the policy-induced causes or impacts on output and supply risk would be informative in guiding policies and the structure of the WIC program.

Abbott. 2021. 2021 Annual Report. Available online: https://www.abbottinvestor.com/static-files/28e5aeb5-7a6c-48a7-9c4c-2847a4f0bb1a

Aussenberg, R. 2017. A Primer on WIC: The Special Supplemental Nutrition Program for Women, Infants, and Children. Washington. DC: Congressional Research Service, Report R44115.

Casey, C.A. 2022. Tariffs and the Infant Formula Shortage. Washington, DC: Congressional Research Service, Report IN11932.

Choi, Y., A. Ludwig, T. Andreyeva, and J. Harris. 2020. “Effects of United States WIC Infant Formula Contracts on Brand Sales of Infant Formula and Toddler Milks.” Journal of Public Health Policy 41(3):303–320.

Creswell, J., and M. Corkery. 2022, September 19. “Store Shelves Are No Longer Bare, but Baby Formula Remains in Short Supply.” New York Times. Available online: https://www.nytimes.com/2022/09/12/business/baby-formula-shortages.html

IBISWorld. 2022. Infant Formula Manufacturing. Industry Report OD4287.

Kline, N., P. Zvavitch, K. Wroblewska, M. Worden, B. Mwombela, B. Thorn, and D. Cassar-Uhl. 2022. WIC Participant and Program Characteristics 2020. U.S. Department of Agriculture, Food and Nutrition Service. Available online https://www.fns.usda.gov/wic/participant-program-characteristics-2020

Nestlé. 2021. Annual Review 2021. Available online: https://www.nestle.com/investors/annual-report

Oliveira, V. 2011. “Winner Takes (Almost) All: How WIC Affects the Infant Formula Market.” Amber Waves. Available online: https://www.ers.usda.gov/amber-waves/2011/september/infant-formula-market/

Oliveira, V., and E. Frazao. 2015. The WIC Program: Background Trends, and Economic Issues, 2015 Edition. Washington, DC: U.S. Department of Agriculture, Economic Research Service, Economic Information Bulletin EIB-134.

Oxenden. M. 2022, August 27. “Abbott to Restart Production of Similac Baby Formula.” New York Times. Available online: https://www.nytimes.com/2022/08/27/business/abott-baby-formula-similac.html

Paris, M. 2022, July 15. “Why the Baby Formula Shortage Continues in the US.” Washington Post. Available online: https://www.washingtonpost.com/business/why-the-baby-formula-shortage-continues-in-the-us/2022/07/15/090cfac8-0461-11ed-8beb-2b4e481b1500_story.html

Perrigo. 2021. Annual Report. Available online: https://investor.perrigo.com/index.php?s=62&cat=21

Reckitt. 2021. Annual Report 2021. Available online: https://www.reckitt.com/investors/annual-report-2021/

Rojas, C., and H. Wei. 2019. “Spillover Mechanisms in the WIC Infant Formula Rebate Program.” Journal of Agricultural and Food Industrial Organization 17(2):20180019.

Sheikh, H., R.A. Aussenberg, A. Nair, and H. Peters. 2022. Infant Formula Shortage: FDA Regulation and Federal Response. Washington, DC: Congressional Research Service, Report IF12123.

United Nations. 2022. UN Comtrade Database. https://comtradeplus.un.org/

U.S. Census Bureau. 2022. Child Stats. Available online: https://www.childstats.gov/americaschildren/tables/pop1.asp

U.S. Customs and Border Protection. 2022. “Requirements for Importing Baby Formula.” Article 000001151. Available online: https://help.cbp.gov/s/article/Article-392

U.S. Department of Agriculture (USDA). 2022a. Global Agricultural Trade System. Washington. DC: USDA, Foreign Agricultural Service.

———. 2022b. Special Supplemental Nutrition Program for Women, Infants, and Children (WIC). Washington. DC: USDA, Food and Nutrition Service. Available online: https://www.fns.usda.gov/wic

U.S. Food & Drug Administration (FDA). 2022a. Guidance for Industry: Infant Formula Enforcement Discretion Policy. FDA-2022-D-0814. Center for Food Safety and Applied Nutrition. Available online: https://www.fda.gov/regulatory- information/search-fda-guidance-documents/guidance-industry-infant-formula-enforcement-discretion-policy

———. 2022b. “FDA Encourages Importation of Safe Infant Formula and Other Flexibilities to Further Increase Availability.” FDA News Release. Available online: https://www.fda.gov/news-events/press-announcements/fda- encourages-importation-safe-infant-formula-and-other-flexibilities-further-increase-availability.

———. 2022c. “Importing Food Products into the United States.” Available online: https://www.fda.gov/food/food-imports-exports/importing-food-products-united-states

White House. 2022a. Fact Sheet: President Biden Announces Additional Steps to Address Infant Formula Shortage. Washington, DC: White House Briefing Room, Statements and Releases. Available online: https://www.whitehouse.gov/briefing-room/statements-releases/2022/05/12/fact-sheet-president-biden-announces-additional-steps-to-address-infant-formula-shortage/

———. 2022b. Addressing the Infant Formula Shortage. Available online: https://www.whitehouse.gov/formula/

[1] Infant formula imports are defined according to HS Code 1901.10: food preparations of flour, meal, starch, malt extract or milk products, suitable for infants or young children, for commercial sale. While mostly infant formula, this subcategory also includes formula for toddlers. This subcategory is used throughout the article.