In the past few years, hemp transitioned from a Schedule I controlled substance in the United States, to a crop only grown in pilot programs for research purposes, to a legal commodity for commercial production. The newness of the market; the lack of institutional, producer, and processor experience; regulatory and political uncertainties; and a threshold at which the crop becomes illegal all expose hemp markets to risks greater than those for more established sectors of production agriculture. In any market, risks are interrelated. For developing hemp markets the risk of crossing a legal threshold for tetrahydrocannabinol (THC) and becoming classified as marijuana (i.e., legal risk) affects and amplifies the other uncertainties.

Risks associated with production agriculture are well-recognized, with risk management tools and strategies in regular use for most sectors. Sources of risk are numerous and diverse. The Organisation for Economic Co-operation and Development (2009) extensively reviewed risk categories affecting growers (e.g., marketing, legal, production, ecological, personal, institutional, financial, technological). They conclude that an exact classification, while providing a framework for discussion, is not as important as a holistic approach to managing the interrelatedness of the risks. A holistic perspective is particularly important in developing U.S. hemp markets which face not only institutional, production, price, and marketing challenges, but also the amplified financial risks associated with a new industry, and legal risks beyond those typically faced in commercial agriculture that then heighten other uncertainties.

In this article, we examine grower exposure to legal risk in developing hemp markets and how that relates to institutional, production, price, and financial risk and amplifies the corresponding impacts. We discuss some emerging risk management tools that are becoming available to growers.

From 1970 to 2014, all cannabis was considered a Schedule I drug under the U.S. Controlled Substance Act. Schedule I drugs are classified as highly addictive and dangerous, with no accepted medical use (Controlled Substances Act CSA, Public Law 91-513). U.S. cannabis production, including for research purposes, was illegal during this period. The Agricultural Act of 2014, Public Law 113-79 (2014 Farm Bill) allowed institutions of higher education or State Departments of Agriculture to establish pilot programs and produce industrial hemp for research. Industrial hemp was defined as the plant Cannabis sativa L. and any part of that plant with no more than 0.30% delta-9-tetrahydrocannabinol (THC) concentration on a dry-weight basis. Mark et al. (2020) provide a review of the pilot programs established under the 2014 Farm Bill.

The Agricultural Improvement Act of 2018 (Public Law 115-334) (the 2018 Farm Bill) removed hemp from the Schedule I list under the Controlled Substances Act and directed the U.S. Department of Agriculture (USDA) to establish a national regulatory framework for hemp production. The 2018 Farm Bill defines hemp as “the plant Cannabis sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers, whether growing or not, with a delta-9 tetrahydrocannabinol concentration of not more than 0.3% on a dry weight basis.” While the word “industrial” was not included in the 2018 Farm Bill, the definition of the legal crop itself is equivalent under the 2014 and 2018 Farm Bills. However, in practice, the 2018 Farm Bill stipulates testing for “total THC” which requires the addition of a separate cannabinoid, tetrahydrocannabinolic acid (THCA), to the result for delta-9-THC (see Box 1).

The 2018 Bill clarified that delta-9-THC testing should employ a procedure using decarboxylation or similarly reliable methods. Decarboxylation methods, including gas chromatography, convert a different cannabinoid, tetrahydrocannabinolic acid (THCA), into delta-9-THC. The conversion from THCA to delta-9-THC also occurs naturally through heat exposure. The chemical process to convert tetrahydrocannabinolic acid (THCA) into delta-9-THC removes a carboxyl group, releasing carbon dioxide and turning the THCA molecule into a delta-9-THC molecule. To avoid undercounting, the IFR specifies that the total THC, derived by adding delta-9-THC and THCA, must fall below 0.30% (U.S. Department of Agriculture, 2019). Gas chromatography involves heating, which converts THCA into delta-9-THC. Liquid methods do not involve heating, and therefore require mathematical addition of the molecular weights to arrive at total THC. The IFR provides the conversion formula for total THC as the sum of delta-9-THC and 87.70% of THCA. For example, if a hemp plant has 0.24% delta-9-THC content, and a concentration of 0.10% THCA, the total THC is 0.24% + 0.10% x 87.70% = 0.31%. While the delta-9-THC level as found in the plant is below 0.30%, the total THC level is greater than 0.30%, meaning the plant tests over the threshold.

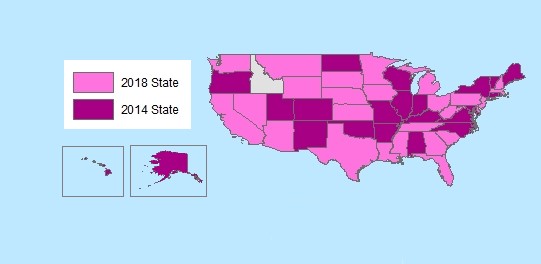

Source: USDA Agricultural Marketing Service. As of

July 17, 2020, Idaho is pending state legislation.

Note: Division of States Under 2014 and 2018 Farm Bills

as of July 2020.

USDA Agricultural Marketing Service (AMS) released the Establishment of a Domestic Hemp Production Program Interim Final Rule (IFR) on October 31, 2019, providing a framework for commercial hemp production in the United States while the Drug Enforcement Agency (DEA) remains the Federal agency that regulates cannabis with THC levels higher than 0.30% (U.S. Department of Agriculture, 2019).1 The IFR incorporates procedures for sampling and testing, and procedures for ensuring the effective disposal of plants that fail to meet the legal threshold. The IFR also allows States to operate programs under the 2014 Farm Bill until October 31, 2020, which some States have opted to do. As of June 2020, 23 states were operating under the 2014 Bill including several with well-established pilot programs, such as Colorado and Kentucky (figure 1). The number of states operating under the pilot program continues to change as states draft plans for USDA approval. The Continuing Appropriations Act, 2021 and Other Extensions Act, passed in early October 2020, allows States to continue operating under 2014 Farm Bill pilot program requirements until September 30, 2021.

The level of legal risk for hemp is unique among agricultural commodities in the United States and amplifies other risks in this emerging sector. Unlike other agricultural commodities, hemp can become illegal based on changes in the chemical composition of the crop. Hemp that tests over a defined level for cannabinoid delta-9-THC is defined as marijuana, still a Schedule I controlled substance which adds legal risk for growers. Only the U.S. Congress can change national statutory law and adjust the THC threshold level (currently set at 0.3%). A lot that tests over the legislatively defined threshold is considered “hot” and cannot be sold. In the IFR, AMS estimated that 20% of lots per year would test high for THC content (U.S. Department of Agriculture, 2019). Compounding the risk, there is no international consensus on acceptable delta-9-THC limits. Most countries in the European Union require a maximum delta-9-THC of 0.20%, while Japan requires zero THC content in the final product (Plain Jane Hemp, 2020). The difference in international threshold levels can cause confusion, limit market access, and make U.S. products illegal overseas.

Under the 2018 Farm Bill, a grower producing hemp must have the hot crop destroyed; this is true even for states in which marijuana production is legal. For states that continue to operate under the 2014 Farm Bill and that have established state-level retail and medical marijuana regulations, a legal option would be to convert a license from industrial hemp to marijuana. However, the transaction costs and market conditions are likely prohibitive. Hemp and marijuana licenses are typically handled by different state agencies and a low (but higher than 0.3%) THC content would be of little or no value in the marijuana market. Some legislators and hemp advocacy groups are promoting a change to the hemp THC threshold; for example, a resolution by the Kentucky House of Representatives is requesting that Congress consider a change to increase the threshold to 1.0% (Kentucky Legislative Research Commission, 2020).

Legal risks for hemp growers were initially exacerbated by a lack of defined sampling and testing procedures for determining THC levels. These were clarified in the 2018 Farm Bill and subsequent IFR (Box 1). However, there is still much to learn about what leads to high THC levels and how growers could ensure their crop will not cross the defined threshold. A meta-analysis by Backer et al. (2019) analyzed the small amount of available literature about impacts from genetic and production methods on yield and cannabinoid profiles, finding that plant density, flowering period, light, and fertilizer affect hemp yield and chemical composition. Various reports contend that stresses such as drought, flooding, and incorrect nutrient mixes can lead to delta-9-THC spikes, increasing legal risk (e.g., Anderson et al., 2019; Blondfield and Dick, 2019; Place, 2019; Pittman, et al. 2019). A recent study identifies genotype as the most important factor in CBD and delta-9-THC level variance, but the study did not specify types of soils or nutrients used (Toth et al., 2020).

Institutional risk relates to the uncertainty faced by growers surrounding changes in government actions and is closely related to legal risk. Multiple U.S. government entities are involved in regulating hemp, including inter alia Congress, USDA, the Food and Drug Administration (FDA), and the DEA. There are many ways in which institutional risk and legal risk interact. The involved agencies have released programs and tools to help and develop the domestic hemp market. However, any program released in the future, such as loans, crop insurance, or marketing assistance, can only be used for a crop testing under the legal threshold.

As one example, the Federal Food, Drug, and Cosmetic (FD&C) Act provides authority to FDA to oversee food, drugs, medical devices, and cosmetics. The 2018 Farm Bill did not alter that authority. The FD&C Act states that if a substance is an active ingredient in an approved drug or has been authorized for substantial clinical research to develop a new drug with research publicly available, then products containing that substance are not included in the definition of a dietary supplement. Half a year prior to the signing of the Farm Bill, the FDA approved a CBD-derived drug. Given the drug approval, and the preapproval clinical investigations, the FDA does not allow CBD to be marketed as a dietary supplement. The FD&C Act allows FDA to make exceptions in adding active drug ingredients to foods or marketing them as dietary supplements, a process that can take three to five years when expedited (U.S. Food and Drug Administration, 2019).

The FDA designated hulled hemp seed, hemp seed protein powder, and hemp seed oil as generally recognized as safe (GRAS) for food consumption (U.S. Food and Drug Administration, 2018). FDA clinical trials showed potential side effects from CBD, including liver injury, adverse interaction with other drugs, and lethargy. Therefore, the FDA has not ruled CBD as safe for human or animal consumption. The agency is investigating differences between CBD isolate, a pure version of the CBD cannabinoid, and broad- and full-spectrum products, which contain other cannabinoids and ingredients. Despite these rules, the FDA has largely avoided intervention in the CBD market, and has instead taken issue only with companies making health claims about CBD. In 2019, the FDA sent 22 cease and desist letters to companies marketing CBD products to treat diseases or claiming other therapeutic benefits of CBD (U.S. Food and Drug Administration, 2020).

The institutional environment of hemp is evolving, which continuously reshapes the uncertainty and risk faced by growers. For example, in February 2020, USDA announced a delay of two IFR requirements for states operating under the 2018 Farm Bill until October 31, 2021 (or until the final rule is finalized, whichever comes first). The first is that all laboratories testing for THC are registered with the DEA. The second is that producers use a DEA-approved reverse distributor (an individual who receives unwanted or unusable controlled substances) or DEA agent to dispose of hot plants. USDA also introduced flexibility on practices to dispose of plants, allowing for common on-farm practices like plowing under, mulching, and disking (U.S. Department of Agriculture, 2020c). These changes allay the risks that bottlenecks could occur if there were a low number of DEA-approved laboratories relative to the number of hemp growers in each state.

Since hemp chemical composition, including THC content, can be impacted by growing conditions, the legal risk of testing hot exacerbates the consequences of production risk. Production risk is pervasive in agriculture and refers to all uncertainties associated with growing a crop, such as weather events, disease, pests, and other factors that can cause yield or quality to drop below expected levels. Each crop thrives under a set of crop-specific optimal conditions. Production risks subvert these optimal conditions. Hemp production risks are amplified both by a dearth of information on optimal planting conditions and by a lack of experience from growers. Vote Hemp estimated that up to 40% of planted acres would not be harvested due in part to crop failures in crop year 2019 (Vote Hemp, 2019). Relative to conventional crops, few research studies exist to define optimal agronomic conditions and genetics for production in the United States that lead to the desired hemp makeup. While research is now underway, it was neglected for decades while commercial growing was prohibited.

Given that hemp is a new crop, options for managing its production risks are limited. The EPA’s Office of Pesticide Program (OPP) regulates the manufacturing of all pesticides and herbicides and establishes the maximum levels of chemical residues for food. Prior to 2019, no pesticides or herbicides were considered legal for use in hemp, which restricted hemp growers’ options for pest and weed control and increased production risk. In December 2019, the OPP approved the use of 10 pesticides for hemp (U.S. Environmental Protection Agency, 2020). While some studies have compared characteristics of hemp cultivars (Piluzza et al., 2013 Vonapartis et al., 2015), extension tests of desired quality by strain are scarce. For example, in 2019 Indiana and Kentucky released total THC tests results for commercially available cultivars, though neither state included accompanying CBD levels for cultivars not testing hot. Many growers are recent market entrants. And at this point, even the most “seasoned” hemp grower could have only been in the market for seven years. For this reason, most growers have not yet established relationships with reputable seedstock suppliers. Only five states (Colorado, North Carolina, North Dakota, Oregon, and Tennessee) have seed certification programs in place, in collaboration with the Association of Official Seed Certifying Agencies (AOSCA). Standardization and transparency in identification and labeling are continuing to develop as the market grows, though progress could stall if researchers and developers perceive that the long-term risk can hamper growth and potential for profits.

Price and market risk relate to uncertainty about input costs and output prices. As an emerging industry, there is a scarcity of reliable, consistently reported information on hemp prices. If a crop goes above the 0.3% THC threshold, the value turns negative as additional costs are incurred for disposal. Legal risk magnifies the downside price risks from lack of data and transparency in emerging markets.

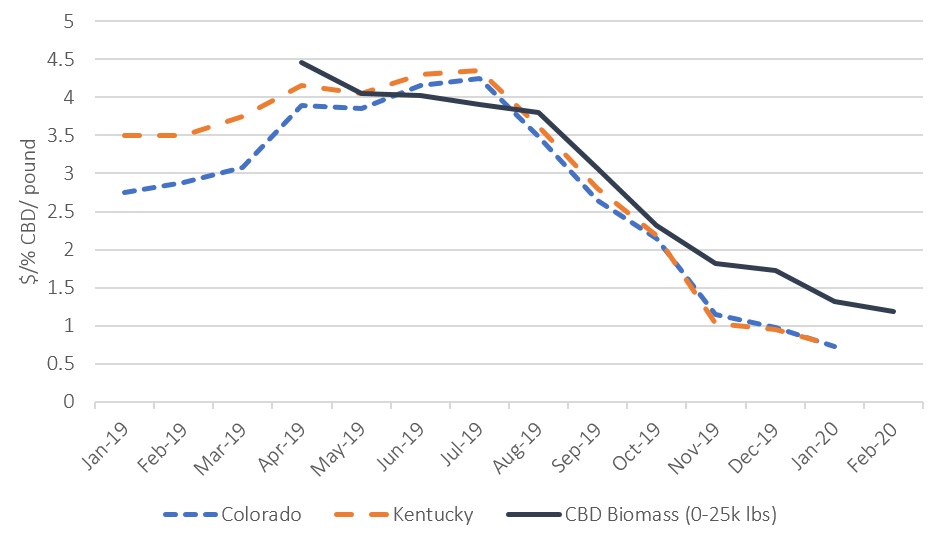

The initial surge in U.S. demand for hemp is being driven by cannabidiol (CBD), a hemp-derived chemical compound used in an expanding number of consumer products, ranging from oils and tinctures to pet treats. CBD has a high value relative to other hemp products which is likely fueling hemp production increases in this category (Schluttenhofer and Yuan, 2017). However, recently returns for CBD have been declining, though prices remain higher than those for seed, grain, or fiber. There is little to no information on demand for hemp-derived products and market risks are exacerbated by lack of transparency and consistency in price reporting.

Notes: Colorado and Kentucky biomass midpoint prices

from PanXchange; average biomass price for 0–25

kilogram sales from Hemp Benchmarks. Both series were

available publicly before changing to paid subscriptions.

At least three sources of proprietary hemp price data exist though none are currently publicly available: PanXchange, Hemp Benchmarks, and The Jacobsen. Data from these sources indicate hemp prices plunged in 2019. For example, in early 2019 CBD isolate in Colorado was priced as high as $7,500 per kilogram. By early 2020, isolate was priced around $2,000 per kilogram. The seed market suffered as well. Growers prefer feminized seeds, treated to produce only female plants which can be genetically or selectively bred to ensure strains with lower THC (Congressional Research Service, 2019). Nonfeminized CBD seeds dropped from around $6,000 per pound to around $1,000 per pound in the same time period, while feminized seeds dropped about 40 cents per seed, or 32%, from mid-2019 to early 2020. CBD biomass (harvested hemp material processed for CBD) prices have declined from a high of over $4 per percentage of CBD content per pound to below $1 (figure 2).

The lack of public price reporting and weak price discovery (the process by which changes in market conditions affect market prices) together mean there is no consistent basis for growers to form price expectations. Just recently, USDA Agriculture Marketing Service Market News began to report advertised retail prices for a limited number of CBD products, but there are still no farm or wholesale prices which are readily available for other crops. Growers typically look at future price expectations, market conditions, and contract terms when making planting decisions but hemp market participants do not have hedging tools to ease price risk.

There are no hemp futures contracts or marketing loans (FSA loans allow farmers to place their crop under loan after harvest, to sell when prices increase later in the season). Hemp growers can instead opt for forward contracting as their main price protection tool. Discussions with industry participants indicate that contracts often allow price to be flexible—i.e., market value at the time of sale, meaning the lack of price transparency poses a high risk to hemp growers. However, growers facing a lack of public data, flexible contract terms, and concerns about processors breaking contracts are left with little information and exposed to additional price risk.

Operating in an emerging industry, growers and hemp businesses often face difficulty in finding a viable partner with whom to transact. Reports have surfaced documenting both buyers and sellers operating without contracts or breaking contracts during the production period. For example, a survey in Indiana indicated that 13% of respondents with unsold inventory had a buyer in place who did not honor the contract (Hemp Benchmarks, 2019). The reasons for contracts being broken include buyers waiting for prices to further drop, growers waiting for prices to trough and start increasing, and bankruptcy (as was the case for GenCanna, one of Kentucky’s largest hemp companies). Additionally, processors will reject any material testing higher than the legal limit in their state, which is either 0.3% delta-9-THC or 0.3% total THC (see Box 1).

Financial risks are associated with borrowing, debt, and the obligation to repay debt. The USDA FSA will provide direct and guaranteed loans for hemp businesses starting in crop year 2020 for eligible operations. Until these loans become available, hemp growers are limited to seeking commercial loans. Banks can lose their licenses or charters if they are shown to be involved in illegal activities and are required by law to submit suspicious activity reports (SARs) after detecting a relevant activity (Federal Deposit Insurance Corporation, 2020). SARs are required when providing financial services to marijuana businesses and, until December 2019, SARs were required for all cannabis-related financing including hemp (Financial Crimes Enforcement Network, 2019).

On December 2019, four federal agencies (the Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, the Financial Crimes Enforcement Network, and the Office of the Comptroller of the Currency) coordinated with the Conference of State Bank Supervisors to issue a statement clarifying that banks are not required to file SARs for borrowers in the hemp market in compliance with the 2018 Farm Bill and its applicable regulations (Financial Crimes Enforcement Network, 2019). In June 2020, the Financial Crimes Enforcement Network updated this guidance to extend to all financial institutions (Financial Crimes Enforcement Network, 2020).

Meanwhile, the Secure and Fair Enforcement (SAFE) Act of 2019, federal legislation aimed at protecting depository institutions serving businesses in the cannabis industry, awaits a vote in the Senate after passing in the House in September 2019. In March 2020, a group of hemp-industry stakeholders including the American Bankers Association, Council of Insurance Agents and Brokers, and the Credit Union National Association, wrote an open letter to the Senate Banking Committee urging support of the SAFE Act. If passed, the Act could increase access to financial markets for hemp growers.

The nascent nature of the market and price volatility hinder banks’ ability to predict cash flow in the hemp market. Legal risks faced by growers add to downside volatility. As a result, hemp growers and businesses have very limited access to credit, translating to increased financial risk. On a larger scale, some States with large production areas, including Kentucky and Colorado, which operate under the 2014 Farm Bill, still require banks to file SARs when financing hemp-related projects. On a granular level, in mid-March 2020, a hemp research, development, and production company called Atalo Holdings filed for bankruptcy, citing an inability to pay back creditors due to failed capital commitment.

Risk management tools for hemp growers are more limited than those for growers in other agricultural sectors. This is in part caused by the lack of futures markets and publicly reported prices. Contracts are a typical tool used to reduce price risk, particularly in thin markets, but growers may be reticent of entering into contracts with processors given the current financial instability among emerging processing companies and reports of broken contracts, unless required for crop insurance purposes. However, tools to reduce some of the risks discussed are beginning to emerge.

USDA has released (or announced) several federal crop insurance tools to help manage production risks (see Box 2). The USDA instruments that help producers with their production risks include the RMA Multi-Peril Crop Insurance (MPCI), the FSA Noninsured Crop Disaster Assistance Program (NAP), RMA Nursery Commodity Insurance, and the Whole-Farm Revenue Protection (WFRP) Program.

RMA Multi-Peril Crop Insurance (MPCI)

MPCI is insurance provided by the Federal Crop Insurance Corporation (FCIC), a government-owned corporation administered by RMA, and sold by private insurance agents. Insurable causes of loss are adverse weather conditions, earthquakes, failure of irrigation water supply, fire, insects and plant disease (unless due to improper disease control measures), wildlife, and volcanic eruption.

Not all hemp growers can purchase MPCI. It is a pilot program for crop year 2020 in certain counties in 21 states. To qualify, growers must have at least one year of hemp-producing history; a contract for the sale of the crop; and minimum of five planted acres if growing for CBD or a minimum of 20 acres if growing for grain and fiber (USDA-RMAa, 2020).

MPCI does not cover losses from non-insurable causes, which includes if THC is in excess of 0.30% on a dry-weight basis; if the grower did not follow the processor contract; if the crop has issues related to mold, yeast, fungus, or other microbial organisms after harvest; or if the grower has damage or loss from an inability to market hemp for any reason other than the insurable causes listed (USDA-RMAb, 2020).

Noninsured Crop Disaster Assistance Program (NAP)

NAP is a financial assistance tool administered by FSA for the Commodity Credit Corporation (CCC), typically available for crops without FCIC insurance. NAP covers loss of yield due to damaging weather and adverse natural occurrences. NAP is available nationally and has a payment limitation of $15,750 (USDA-CCC and USDA-FSA, 2020).

While there are no acreage requirements to qualify for NAP, hemp growers (or the entity applying) must have a contract for the crop and an average adjusted gross income under $900,000. Additionally, first-time growers can only qualify for catastrophic coverage. A producer with at least one year of “successful” production may purchase buy-up coverage. Production is considered successful if yield was at least 50% of the county-expected yield for the intended use, unless losses were due to eligible causes. The same rotation requirements and restrictions for covered losses as MPCI apply.

Whole-Farm Revenue Protection (WFRP)

The WFRP pilot program is a risk management tool provided by FCIC and sold by private insurance agents that protects growers from loss of revenue. The program covers losses for the entire farm from natural causes and declines in market prices. The program is available nationally and is useful for highly diverse farms growing specialty commodities. Growers ensure their revenue, which is equal to the lower of the grower’s current-year expected revenue or historical revenue adjusted for growth at the selected coverage level (USDA-RMAd, 2020).

To qualify, hemp growers must be licensed under the applicable governing authority, whether a state regulator or USDA, by the applicable date (July 15) for WFRP. Only for 2020, this means that growers in states whose plans are not yet approved do not qualify for WFRP. As with MPCI and NAP, the crop must also be grown under contract. Hemp grown without a contract is not insurable, but revenue from noninsured hemp grown on the farm still counts as “revenue to count.”

Nursery Programs

The nursery crop insurance program and Nursery Value Select (NVS) programs are RMA asset-based coverages sold by private insurance agents and will be available for hemp grown in containers. The nursery crop insurance program is available nationwide, while NVS is a pilot that allows nursery producers to select the dollar amount of coverage (USDA-RMAc, 2020). Nursery programs covers losses from adverse weather, failure of irrigation water supply due to an insurable case of loss (like drought), fire (if weeds and undergrowth are controlled), and wildlife.

Similarly to the other programs, hemp can only be insured when in accordance to State, tribe, or USDA regulation, and in accordance to the THC limit. The program also requires growers to use seed or plant cuttings adapted to the intended use (fiber, grain, seed, or processing).

These four federal crop insurance programs do not cover losses from any hemp crop that has tested over 0.30% total THC. Meanwhile, private insurance companies in several states offer hemp crop insurance programs, including hail and weather insurance. Private insurance contracts can be tied to weather events, rendering delta-9-THC or total THC levels irrelevant.

Legal risk is a major hurdle for hemp producers that amplifies the other risks in this emerging industry. Risks in the hemp market are high and rapidly changing, amid increasing knowledge of production and markets and a continually evolving institutional framework. All agricultural commodities face production, price, financial, and institutional risks. Hemp growers also face the legal risk that their crop will pass over a threshold of allowed tetrahydrocannabinol. Federal crop insurance, which is available to hemp producers, cannot insure against illegal conduct. If a grower’s lot tests over the THC threshold, that grower has no viable venue of recouping their production costs and may incur additional costs for disposal. This exacerbates the other uncertainties as the market evolves and new information becomes available.

Anderson, E., D. Baas, M. Thelen, E. Burns, M. Chilvers, K. Thelen, C. DiFonzo, and B. Wilke. 2019. Industrial Hemp Production in Michigan. Ann Arbor, MI: Michigan State University Extension. Available online: https://www.canr.msu.edu/resources/industrial-hemp-production-in-michigan-e3402.

Backer, R., T. Schwinghamer, P. Rosenbaum, V. McCarty, S. Eichhorn Bilodeau, D. Lyu, M.B. Ahmed, G. Robinson, M. Lefsrud, O. Wilkins, and D.L. Smith. “Closing the yield gap for cannabis: a meta-analysis of factors determining cannabis yield.” Frontiers in plant science 10 (2019): 495.

Baxter, J. 2000. Growing Industrial Hemp in Ontario. Agdex no. 153/20. Ontario, Canada: Ministry of Agriculture, Food and Rural Affairs. Available online: http://www.omafra.gov.on.ca/english/crops/facts/00-067.htm

Blondfield, A., and J. Dick. 2019. Hemp in Nevada. Sparks, NV: Nevada Department of Agriculture. Available online: http://agri.nv.gov/uploadedFiles/agrinvgov/Content/Resources/industrial_hemp_faq_update_r5.pdf

Comprehensive Drug Abuse Prevention and Control Act of 1970, Pub.L. 91–513, 84 Stat. 1236 (1970).

Canadian Hemp Trade Alliance. 2020. Production: Seeding Date. Available online: http://www.hemptrade.ca/eguide/production/seeding.

Congressional Research Service. 2019. Defining Hemp: A Fact Sheet. Washington, DC: Congressional Research Service, Report to Congress R44742.

Darby, H., A. Gupta, E. Cummings, L. Ruhl, and S. Ziegler. 2018. 2017 Industrial Grain Hemp Planting Date Trial. Burlington, VT: University of Vermont Extension. Available online: https://www.uvm.edu/sites/default/files/media/2017_Grain_hemp_planting_date_trial.pdf

Kentucky Department of Agriculture. 2020. Hemp Program Summary of Varieties: Including Varieties of Concern and Prohibited Varieties. Frankfort, KY: Kentucky Department of Agriculture. Available online: https://www.kyagr.com/marketing/documents/HEMP_LH_Summary_of_Varieties_List_2019.pdf.

Federal Deposit Insurance Corporation. 2020. Part 1020 Rule for Banks. Available online: https://www.fdic.gov/regulations/laws/rules/8000-1600.html.

Financial Crimes Enforcement Network. 2019. Hemp Guidance. Providing Financial Services to Customers Engaged in Hemp-Related Businesses. Available online: https://www.fincen.gov/sites/default/files/2019-12/Hemp Guidance %28Final 12-3-19%29 FINAL.pdf.

Financial Crimes Enforcement Network. 2020. FinCEN Guidance Regarding Due Diligence Requirements under the Bank Secrecy Act for Hemp-Related Business Customer? Available Online: https://www.fincen.gov/sites/default/files/2020-06/FinCEN_Hemp_Guidance_508_FINAL.pdf.

Heath, R., and M. Hart. 2020. House Concurrent Resolution 57. Bill RN 1417. Frankfort, KY: Kentucky House of Representatives.

Hemp Benchmarks. 2019, December. “U.S. Wholesale Hemp Price Benchmarks. New Leaf Data Services.”

Kentucky Legislative Research Commission. 2020. House Concurrent Resolution 57. 20 RS BR 1417.

Mark, T., J. Shepherd, D. Olson, W. Snell, S. Proper, and S. Thornsbury. 2020. Economic Viability of Industrial Hemp in the United States: A Review of State Pilot Programs. Washington DC: U.S. Department of Agriculture, Economic Research Service, EIB-217, February.

Office of Indiana State Chemist and Seed Commissioner (OISCSC). 2019. 2019 Total THC Test Results by Hemp Variety. Available online: https://purduehemp.org/wp-content/uploads/2019/12/Hemp-THC-Results-by-Variety_update.pdf.

Organisation for Economic Co-operation and Development. 2009. “Risk Management in Agriculture: A Holistic Conceptual Framework.” In Managing Risk in Agriculture: A Holistic Approach. Paris, France: OECD Publishing.

Piluzza, G., G. Delogu, A. Cabras, S. Marceddu, and S. Bullitta. 2013. “Differentiation Between Fiber and Drug Types of Hemp (Cannabis sativa L.) from a Collection of Wild and Domesticated Accessions.” Genetic Resources and Crop Evolution 60(8): 2331–2342.

Pittman, H., and V. Ford. 2019. General Information on Industrial Hemp for Arkansas.” Little Rock, AR: University of Arkansas Division of Agriculture Research and Extension. Available online: https://www.uaex.edu/farm-ranch/crops-commercial-horticulture/industrial_hemp/docs/INFORMATION%20ON%20INDUSTRIAL%20HEMP.pdf.

Place, G. 2019. Hemp Production – Keeping THC Levels Low. Newton, NC: NC Cooperative Extension, Catawba County Center. Available online: https://catawba.ces.ncsu.edu/2018/11/hemp-production-keeping-thc-levels-low/.

Plain Jane Hemp. 2020. Legal Status of CBD around the World. Available online: https://blog.tryplainjane.com/legal-status-of-cbd-around-the-world/.

Potter, D. 2009. “The Propagation, Characterisation and Optimisation of Cannabis sativa L. as a Phytopharmaceutical.” PhD thesis, King's College, London.

Purdue Hemp Project. 2015. Hemp Production. Available online: https://purduehemp.org/hemp-production/.

Schluttenhofer, C., and L. Yuan. 2017. “Challenges towards Revitalizing Hemp: A Multifaceted Crop.” Trends in Plant Science 22(11): 917–929.

Toth, J.A., G.M. Stack, A.R. Cala, C.H. Carlson, R.L. Wilk, J.L. Crawford, D.R. Viands, G. Philippe, C.D. Smart, J.K.C. Rose, and L.B. Smart. 2020. “Development and Validation of Genetic Markers for Sex and Cannabinoid Chemotype in Cannabis sativa L.” GCB Bionergy 12: 213–222.

U.S. Department of Agriculture. 2019. “Establishment of a Domestic Hemp Production Program.” Federal Register 84(211).

U.S. Department of Agriculture. 2020a. Actual Production History Hemp. Washington, DC: U.S. Department of Agriculture, Risk Management Agency, Fact Sheet, February.

U.S. Department of Agriculture. 2020b. Hemp Crop Insurance Standards Handbook. 2020 and Succeeding Crop Years. Washington, DC: U.S. Department of Agriculture, Risk Management Agency, Federal Crop Insurance Corporation, FCIC-20600U (02-2020).

U.S. Department of Agriculture. 2020c. Hemp Disposal Activities. Washington, DC: U.S. Department of Agriculture, Agricultural Marketing Service. Available online: https://www.ams.usda.gov/rules-regulations/hemp/disposal-activities.

U.S. Department of Agriculture. 2020d. “Noninsured Crop Disaster Assistance Program. Final Rule.” Federal Register 85(41).

U.S. Department of Agriculture. 2020e. Nursery Value Select Pilot Crop Insurance Standards Handbook. 2021 and Succeeding Crop Years. Washington, DC: U.S. Department of Agriculture, Risk Management Agency, Federal Crop Insurance Corporation, FCIC-24070 (02-2020)

U.S. Department of Agriculture. 2020f. Whole-Farm Revenue Protection Pilot Handbook. 2020 and Succeeding Policy Years. Washington, DC: U.S. Department of Agriculture, Risk Management Agency, Federal Crop Insurance Corporation, FCIC 18160-1 (03-2020).

U.S. Environmental Protection Agency. 2020. Pesticide Registration: Pesticide Products Registered for Use on Hemp. Available online: https://www.epa.gov/pesticide-registration/pesticide-products-registered-use-hemp

U.S. Food and Drug Administration. 2018. FDA Responds to Three GRAS Notices for Hemp Seed-Derived Ingredients for Use in Human Food. Washington, DC: U.S. Food and Drug Administration. Available online: https://www.fda.gov/food/cfsan-constituent-updates/fda-responds-three-gras-notices-hemp-seed-derived-ingredients-use-human-food.

U.S. Food and Drug Administration. 2019, July 25. Testimony. Hemp Production and the 2018 Farm Bill. Washington, DC: U.S. Food and Drug Administration. Available online: https://www.fda.gov/news-events/congressional-testimony/hemp-production-and-2018-farm-bill-07252019.

U.S. Food and Drug Administration. 2020. Warning Letters and Test Results for Cannabidiol-Related Products. Washington, DC: U.S. Food and Drug Administration. Available online: https://www.fda.gov/news-events/public-health-focus/warning-letters-and-test-results-cannabidiol-related-products.

Vonapartis, E., M. Aubin, P. Seguin, A.F. Musfafa, and J. Charron. 2015. “Seed Composition of Ten Industrial Hemp Cultivars Approved for Production in Canada.” Journal of Food Composition and Analysis 39: 8–12.

Vote Hemp. 2019. U.S. Hemp License Report. Available online: https://www.votehemp.com/wp-content/uploads/2019/09/Vote-Hemp-US-License-Report-2019.pdf.

1 AMS published the Final Rule establishing the Domestic Hemp Production Program on January 19, 2021. The rule was published after this report was written.