The COVID-19 pandemic gripped the United States beginning in early March 2020 and quickly caused widespread economic impacts. Closures of businesses—such as theaters, restaurants, and bars—across large parts of the nation led to a spike in the unemployment rate, which reached 14.7% in April 2020; as of June 2020, the unemployment rate had only declined to 11.1%, a stark contrast to the previous year’s steady unemployment, which hovered around 4% (U.S. Bureau of Labor Statistics, 2020). Initially issued in March and April 2020, shelter-in-place “lockdown” and curfew orders enacted in many counties and states (Raifman et al., 2020) further reduced economic activity in an effort to prioritize human health and safety. However, the measures taken to reduce disease transmission had significant costs as many American families found themselves low on or without any remaining emergency funds to weather the coronavirus crisis—a precarious situation in the midst of a global pandemic. Altogether, the challenging times faced by U.S. families led to the federal government intervening with financial assistance, which resulted in measurable changes in spending and purchasing behaviors. We investigated the effects of the pandemic and relief package herein.

The Coronavirus Aid, Relief, and Economic Security Act (CARES)—signed into law by the president on March 27, 2020—extended economic impact payments (EIP) to U.S. households. This bill helped individuals, families, and businesses affected by the 2020 coronavirus pandemic. According to the Internal Revenue Service, disbursement of the first wave of EIP began on April 15, 2020. For many U.S. citizens, CARES represented a significant cash supplement that was meant to help get them through the economic recession resulting from the pandemic.

As widely reported in the news and on social media, daily activities for many individuals, families, and businesses changed drastically because of the coronavirus pandemic. Warnings about meat processing facilities shutting down sent consumers into a panic-buying mode (Maclas, 2020). Prices for many goods increased as demand rapidly increased while production shuddered to a halt (Gallagher and Kirkland, 2020). Across the United States, restaurants, cafes, and bars drastically limited occupancy or completely shut down due to social distancing ordinances (Wida, 2020). Meanwhile, layoffs and furloughs increased (Bomey, 2020) and forced many Americans to consider where their next paycheck would come from while trying to manage bills coming due (Arnold, 2020). Many Americans found themselves quickly transitioning toward prioritizing human health and reducing disease transmission. All these changes drew attention to the fragile nature of a highly complex food system.

This article sheds light on more subtle changes in household purchasing behaviors in response to COVID-19 and the ways in which U.S. households utilized their EIP. We also investigate changes in spending patterns among food-retail formats, how the pandemic changed the different types of foods households purchased, and the attributes of food products deemed most important during the COVID-19 pandemic. To examine these issues, we conducted a nationwide survey in May 2020, which was administered online through a survey management company that ensured proportional representativeness of the sample across gender, age, and income using the 2018 American Community Survey 1-Year Estimates. The questions in the survey spanned respondent and household demographics, issues surrounding COVID-19, receipt of an EIP, and food shopping and consumption behaviors.

A total of 972 respondents, 18 years or older, completed the survey. At the time of the survey, about 46% of respondents were employed full-time, nearly 42% were employed part-time, and nearly 12% were unemployed. Approximately 57% of respondents reported no change in income during COVID-19, while another 38% reported experiencing an income decrease averaging 44% as a result of the pandemic. The most commonly cited reasons for the reduction in total household income due to COVID-19 for those experiencing decreased income were reduced hours (45%), layoffs (34%), and directly reduced pay by employers (18%). The remaining respondents, about 5% of the sample, reported an increase in income averaging approximately 41%.

As stated in the bill, the purpose of the CARES Act was “to provide emergency assistance and health care response for individuals, families, and businesses affected by the 2020 coronavirus pandemic” (McConnell et al., 2020). The 2020 CARES Act authorized stimulus payments (EIP) to U.S. taxpayers of up to $1,200 per individual ($2,400 for married couples) and up to $500 for qualified dependents (Pub. L. 116-136) (116th Congress, 2020). Eligibility was based on household income levels below $75,000 for single filers and $150,000 for married couples. For households with incomes over these levels, their EIP was reduced by $5 for every $100 of income over the threshold. The goal of the EIP was to ensure that Americans saw direct and fast relief in the wake of the coronavirus pandemic (U.S. Department of the Treasury, 2020). For some households, the EIP replaced lost wages, while for others it was an unanticipated increase in income. The 2020 EIP provides individuals and couples with payments approximately twice as large as those provided under 2008 U.S. stimulus payment program (U.S. Internal Revenue Service, 2008).

While the amount of the EIP that households expected to receive was clearly established in the CARES Act, there was significant variation in the timing of when households received these payments because the payments were processed in batches starting in mid-April. During our survey period—May 15–25, 2020—67.9% of respondents indicated that they had already received the EIP, 14.9% anticipated receiving the EIP, and 17.2% did not anticipate receiving any payment. We focus on the households who indicated that they had either received or anticipated receiving the EIP in this analysis. Of these households, the median EIP reported was $2,000, and 67.0% of households received/anticipated an EIP for either one ($1,200) or two ($2,400) eligible adults.

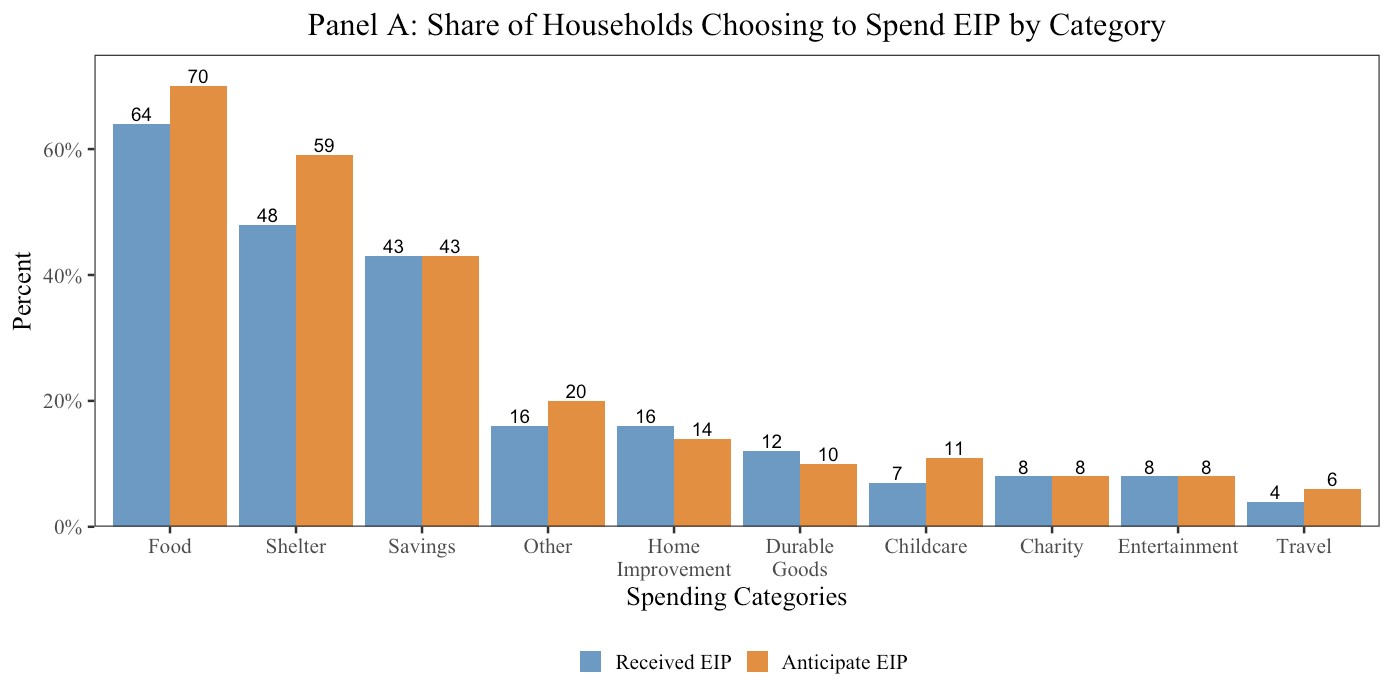

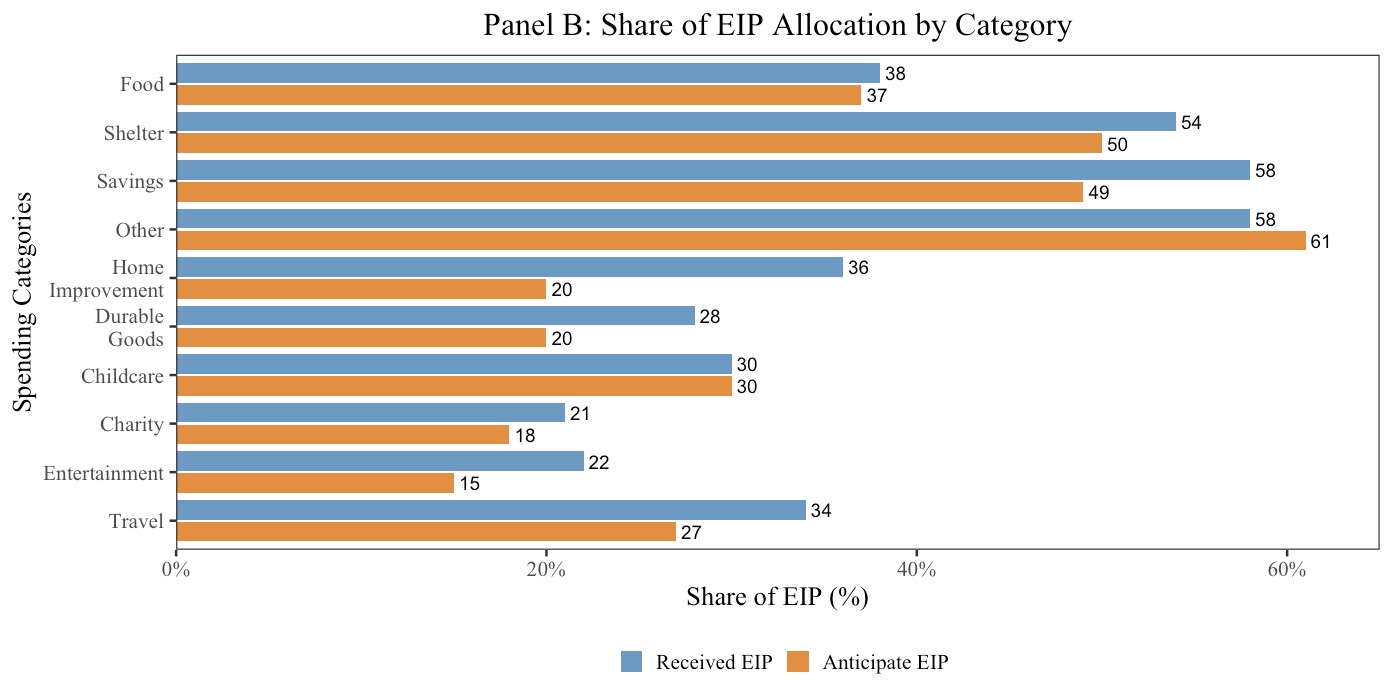

We asked respondents about their intent to spend their EIP across ten categories, building on the approach taken by Shapiro and Slemrod (2009) who examined how U.S. households intended to spend their 2008 tax rebates. Figure 1 presents side-by-side comparisons for respondents who have already received an EIP and those who were expecting to receive an EIP. Panel A of Figure 1 illustrates the proportion of respondents that have spent or plan to spend at least some of their EIP on a given category for each of the possible spending categories posed in the survey. Panel B of Figure 1 illustrates the average share of the respondents’ EIP allocated to each category for respondents who indicated spending at least some of their EIP on that particular spending category.

Considering the ten possible spending categories, more respondents indicated allocating at least part of their EIP to food, shelter, and savings than the other spending category alternatives. These categories largely reflect basic necessities during the pandemic plus increasing savings in fear of continued uncertainty. To the extent that recipients planned to spend their payments on necessities, like food and shelter, it could be argued that the CARES met its stated purpose of providing immediate economic relief to Americans. Sixty-four percent of the respondents who had received the EIP allocated at least some of the payment to purchase food, spending an average of 38% of their stimulus check on food. Similarly, 70% of the households anticipating the EIP planned to allocate an average of 37% of the payment toward food. We find that 59% of households anticipating the EIP planned to allocate part of the payment to immediate rent or mortgage payments, compared to 48% of households that had already received the funds. Less than 10% of respondents in either group reported allocating EIP funds toward travel or entertainment; these findings are consistent with industries/sectors that were closed during the COVID-19 pandemic.

Taking both those households that had already received their EIP and those that anticipated receiving an EIP, among households allocating EIP money to food consumption, 98% indicated they would use their payment to purchase food from grocery stores, 44% indicated they would purchase food delivered to their home, and 21% would purchase food locally (e.g., farmers’ market and community supported agriculture). These findings indicate that EIP spending mostly benefits traditional grocery retailers. Local food producers who supply products to grocery retailers (e.g., “Fresh from Florida”) or food delivery services that have partnerships with grocery stores may also benefit from the increased spending at the grocery store.

Our results show that households allocated the largest shares of their stimulus payment toward nondurable goods, especially food, during the COVID-19 pandemic. Notably, previous research on the 2008 stimulus checks received during the 2007–2009 recession found that during the three-month window when payments were disbursed, U.S. consumers spent 12%–30% of their payments on nondurable goods and services as a category; however, spending on food only represented 2% of the payment (Parker et al., 2013). One justification for recipients spending a higher proportion of their stimulus checks on food in the current environment is the concerns over supply chain constraints due to COVID that were not present in 2008. Allocating the EIP to stock up on food may have been a hedge against future shortages.

The COVID-19 pandemic resulted in disruptions to food supply chains that changed both where consumers obtained food and what products were available to purchase. However, consistent with previous economic downturns, we see significant shares of people allocating a large portion of their EIP to cover immediate shelter needs and savings. Our findings also suggest consumers may have been concerned about the food supply chain and future food availability.

In this study, we do not have the data to investigate whether households are treating the EIP as they would a pure income transfer. If the EIP is fully fungible (a perfect substitute for income), we would expect a household to allocate one additional dollar of the EIP in the same manner it would allocate one dollar of income. However, since the EIP replaced lost income for some households that suffered income losses due to COIVD-19 and was an additional source of income for those households that had not lost income, it is likely that the income effects associated with receiving the EIP affected the allocation of funds to the various spending categories. Further, for households that lost income due to the pandemic, the EIP may have mitigated or partially mitigated prior income effects. Alternatively, if the EIP is not fully fungible, households may allocate the EIP rather differently than they would allocate other sources of income, resulting in significantly different purchasing behavior than when the EIP is fully fungible. For example, previous research has found that households spend a higher share of funds on food when using SNAP benefits (Levedahl, 1995; Breunig and Dasgupta, 2002, 2005) and that fungibility can vary based on household characteristics like shopping behaviors and poverty (Smith et al., 2016). While this study is unable to determine if the EIP caused behavior to differ from a change in household income, this is an important area for future research to understand the effects of stimulus and emergency payments.

The EIP was a fast-acting financial booster injected into the budgets of many American households at a time when many households were facing uncertainty regarding the length of shelter-in-place orders and other restrictions and concerns about the food supply chain. Thus, we also examine whether respondents shifted their food purchasing patterns.

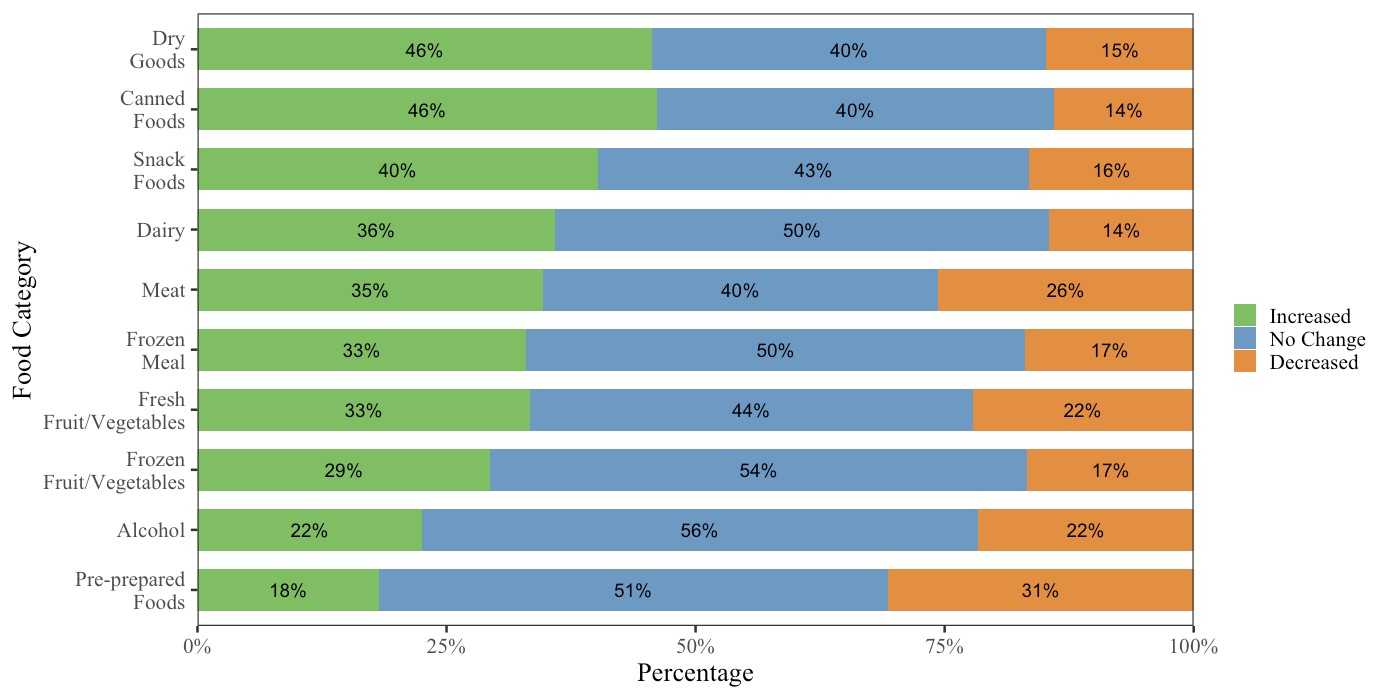

Consistent with prolonged shelter-in-place orders, we find that households most frequently reported increasing their purchases of shelf-stable items—including canned foods, dry goods (e.g., rice, pasta, beans), and snack foods—compared to other categories during the COVID-19 pandemic. For example, 46% of households sampled reported increasing their purchases of canned foods and dry foods. The largest reduction in food purchasing occurred in the pre-prepared foods category, in which 31% of households reported scaling down purchases, followed by meat (26%).

In addition to changes in individual behavior, some of these reductions may have been due to shortages and disruptions in the food supply chain. We find that 52% of consumers experienced shortages of meat, 40% experienced shortages of dry goods, 30% experienced shortages of produce, and 30% experienced shortages of fruit and vegetables.

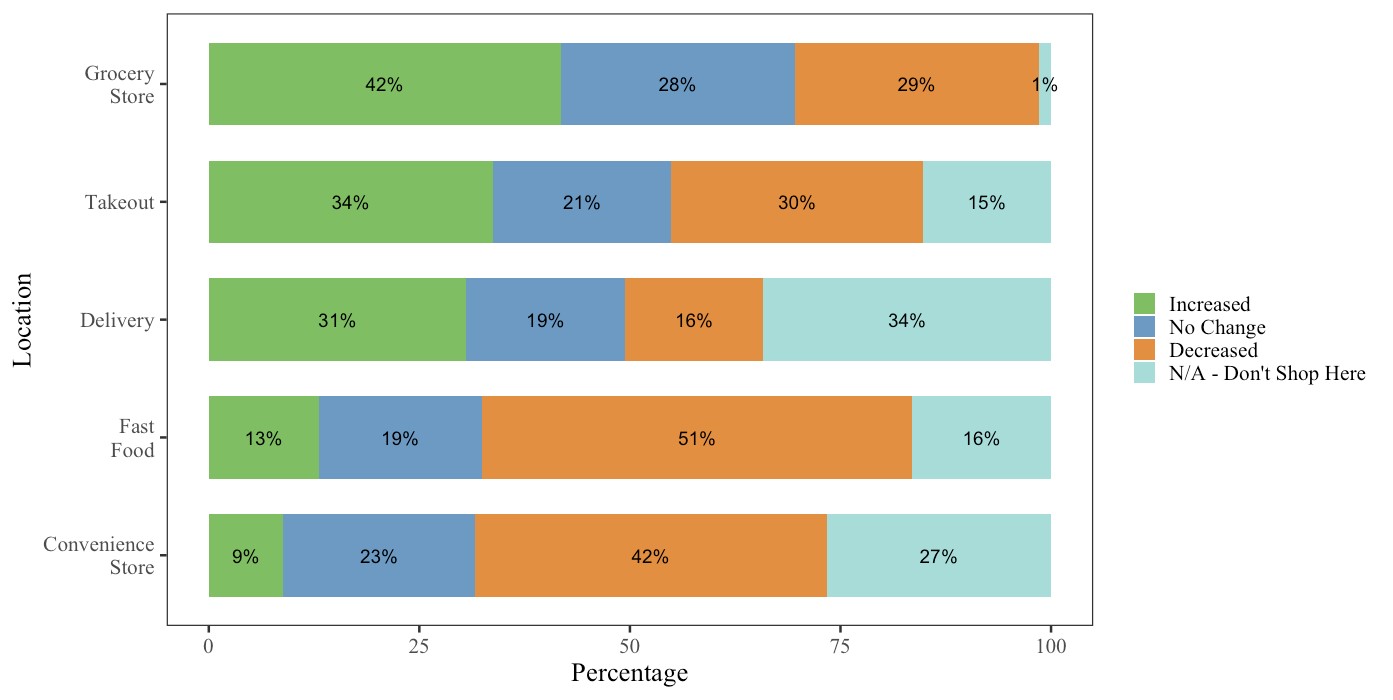

Figure 3 presents how the COVID-19 pandemic altered where people spent money on food. Overall, 42% of the respondents reported increasing their spending at the grocery store because of the COVID-19 pandemic. On average, households in our sample took 5.6 trips to the grocery store in the month prior to taking the survey. In comparison, 34% and 31% of the respondents indicated increasing their spending on takeout and delivery, respectively. On the other end of the spectrum, convenience stores and fast food stores had a marked decrease in patronage; 42% and 51% of respondents reported purchasing less food at these locations, respectively. These results provide evidence that during the pandemic, a shift occurred in shopping locations.

Another noticeable layer in consumer behavior changes is the increased concentration of spending (or lack thereof) among different types of places where food can be obtained quickly. During the COVID-19 pandemic, shopping for household necessities like food was important. Many traditional food retail establishments that consumers frequented were inundated by shoppers forming long, socially distant lines along storefronts, while others experienced marked decreases in foot traffic.

In addition, concerns regarding how to shop safely and avoid contracting COVID-19 while shopping was an additional challenge that households had to consider. Many food retail businesses implemented safety measures. Popular grocery store chains, like Kroger and Walmart, took actions such as limiting customer capacity in stores, asking customers to maintain six feet of distance from one another, and encouraging customers to wear masks (Kroger Co., 2020; Walmart, 2020). Some stores reserved access for particularly vulnerable groups, like senior citizens, during special hours of operation (Kassraie, 2020). In many cases, limiting store occupancy resulted in longer lines and wait times in storefronts (Telford and Bhattarai, 2020).

Freshness and cost were ranked by the respondents as the most important product attributes when shopping during the COVID-19 pandemic. This likely resulted from a large portion of consumers preparing to shelter at home for an unknown amount of time. Further, respondents indicated that they were less focused on production-oriented attributes—including organic, sustainable, and locally produced—or the brand name of products. Given the overall supply constraints and quota limits implemented at many retailers (Aaron, 2020; Halkias, 2020), this reduced focus on production-orientation may be due to fewer products on the shelves to choose from and consumers attempting to acquire any supplies still available. Nutrition, nonperishable/shelf stable, and convenience were also deemed important attributes, ranking above production characteristics.

Our findings have implications for the food supply chain, which are important to understand as Congress considers a second round of stimulus payments. EIP recipients who spend a significant portion of their stimulus payment on food do so primarily at grocery stores. Our survey results also indicate that consumers have increased their spending at grocery stores, and thus most of the benefits of increased spending on food and spending related to the EIP are accruing to traditional grocery retailers. We expect many EIP recipients to continue to spend a larger share of their payments on nondurable consumption goods and to continue to spend more at grocery stores than they did prior to the pandemic while COVID-related closures and restrictions remain in place. Food processing and manufacturing can try to cash in on the increased patronage at grocery stores by identifying consumers’ changing needs. For example, the Campbell Soup Company (2020a,b) has proactively started rebuilding inventory, expecting prolonged shelter-in-place orders. While this can help traditional grocery stores keep shelves stocked with food items, grocery stores can take advantage of increased patronage by offering a larger assortment of goods not traditionally found in the retail format—similar to the partnership between Kroger and Walgreens, which combines health and beauty products with food-related items (Japsen, 2019). Groceries may also benefit from increased sales of store brands as we find that our respondents deem branding to be less important than other product attributes. In addition, situations in which grocery stores or other channels experience stockouts presents a potentially unique opportunity for convenience stores, such as for the snack foods category (Mulloy, 2020), as consumers seek to satisfy their indulgences. However, easing shelter-in-place orders and other restrictions across several states in the United States will likely stimulate higher consumer spending and patronage at other food outlets, including restaurants, thus potentially spreading the benefits of the payments to a larger share of stakeholders in the food supply chain. Additionally, with the food supply chain adapting and more direct-to-consumer options becoming available (e.g., drive-through farmers’ markets), it is possible that more of these economic benefits could flow directly to farmers.

As policy makers debate whether a second round of pandemic-related stimulus checks is needed (Konish, 2020), this article provides evidence that consumers have directed a significant share of their EIP toward essential food and shelter needs. This article also highlights the potential benefits realized through this form of government aid and its crucial role in alleviating part of the burden created by this unprecedented public health crisis. A second round of EIP could allow Americans, especially for those without (or running low on) emergency funds, to find relief as they try to stretch their dollars further.

116th Congress. 2020. H.R.748: CARES Act. Available online: https://www.congress.gov/bill/ 116th-congress/house-bill/748 [Accessed August 5, 2020].

Aaron, R. 2020, May 5. “Some Grocery Stores Limit Meat Purchases during COVID-19 Related Shortage.” ABC4. Available online: https://www.abc4.com/coronavirus/some-grocery-stores-limit-meat-purchases-during-covid-19-related-shortage/ [Accessed July 9, 2020].

Arnold, C. 2020, June 3. “Millions of Americans Skip Payments as Tidal Wave of Defaults and Evictions Looms.” NPR. Available online: https://www.npr.org/2020/06/03/867856602/ millions-of-americans-skipping-payments-as-tidal-wave-of-defaults-and-evictions- [Accessed July 2, 2020].

Bomey, N. 2020, March 17. “COVID-19 Job Cuts: Layoffs Accelerate as Coronavirus Disrupts American Economy.” USA Today. Available online: https://www.usatoday.com/story/ money/2020/03/17/covid-19-job-cuts-layoffs-coronavirus-economy/5068695002/ [Accessed July 2, 2020].

Breunig, R. V., and I. Dasgupta. 2002. “A Theoretical and Empirical Evaluation of the Functional Forms Used to Estimate the Food Expenditure Equation of Food Stamp Recipients: Comment.” American Journal of Agricultural Economics 84(4): 1156–1160.

Breunig, R., and I. Dasgupta. 2005. “Do Intra-Household Effects Generate the Food Stamp Cash-out Puzzle?” American Journal of Agricultural Economics 87(3): 552–568.

Campbell Soup Company. 2020a, April 2. “Our Response to COVID-19.” Available online: https://campbells55.wpengine.com/csc-2/newsroom/news/2020/04/02/our-response-to-covid-19/ [Accessed July 24, 2020].

Campbell Soup Company. 2020b, April 3. “The Strength of our Supply Chain.” Available online: https://www.campbellsoupcompany.com/newsroom/news/2020/04/03/the-strength-of-our-supply-chain/ [Accessed July 24, 2020].

Gallagher, D., and P. Kirkland. 2020, April 27. “Meat Processing Plants across the US Are Closing Due to the Pandemic. Will Consumers Feel the Impact?” CNN. Available online: https://www.cnn.com/2020/04/26/business/meat-processing-plants-coronavirus/ index.html [Accessed July 2, 2020].

Halkias, M. 2020, March 27. “Grocery Shopping Remains a Challenge with Eggs Added to the (Empty Shelf) List.” Dallas News. Available online: https://www.dallasnews.com/ business/retail/2020/03/27/grocery-shopping-remains-a-challenge-with-eggs-added-to-the-empty-shelf-list/ [Accessed July 9, 2020].

Japsen, B. 2019, August 19. “Walgreens Expands Kroger Grocery to More Drugstores.” Forbes. Available online: https://www.forbes.com/sites/brucejapsen/2019/08/19/walgreens-expands-kroger-grocery-to-more-drugstores/ [Accessed August 5, 2020].

Kassraie, A. 2020, April 22. “Supermarkets Offer Senior Hours Due to Coronavirus.” AARP. Available online: http://www.aarp.org/home-family/your-home/info-2020/coronavirus-supermarkets.html [Accessed July 3, 2020].

Konish, L. 2020, July 20. “Will There Be a Second $1,200 Stimulus Check? Here’s What We Know.” CNBC. Available online: https://www.cnbc.com/2020/07/20/will-there-be-a-second-1200-stimulus-check-heres-what-we-know.html [Accessed July 24, 2020].

Kroger Co. 2020. “Kroger - COVID-19 FAQs”. Available online: https://www.kroger.com/hc/ help/faqs/covid-19/general [Accessed July 3, 2020)\].

Levedahl, J. W. 1995. “A Theoretical and Empirical Evaluation of the Functional Forms Used to Estimate the Food Expenditure Equation of Food Stamp Recipients.” American Journal of Agricultural Economics 77(4): 960–968.

Maclas, C. 2020, June 25. “Is the Food Supply Strong Enough to Weather the COVID-19 Pandemic?” Available online: https://www.ucdavis.edu/food/news/is-food-supply-strong-enough-to-weather-covid-19-pandemic [Accessed July 2, 2020].

McConnell, M., M. Rubio, R. Shelby, and R. Wicker. ‘IN THE SENATE OF THE UNITED STATES’ (March 2020):247.

Mulloy, T. 2020, May 20. “Snacking Soars as C-Stores Vie for Sales.” CStore Decisions. Available online: https://cstoredecisions.com/2020/05/20/snacking-soars-as-c-stores-vie-for-sales/ [Accessed July 25, 2020].

Parker, J. A., N. S. Souleles, D. S. Johnson, and R. McClelland. 2013. “Consumer Spending and the Economic Stimulus Payments of 2008.” American Economic Review 103(6): 2530–2553.

Raifman, J., K. Nocka, D. Jones, S. K. Lipson, and P. Chan. 2020 July 14. “COVID-19 US State Policy Database (CUSP).” Available online: www.tinyurl.com/statepolicies [Accessed July 22, 2020].

Shapiro, M. D., and J. Slemrod. 2009. “Did the 2008 Tax Rebates Stimulate Spending?” American Economic Review 99(2): 374–379.

Smith, T. A., J. P. Berning, X. Yang, G. Colson, and J. H. Dorfman. 2016. “The Effects of Benefit Timing and Income Fungibility on Food Purchasing Decisions among Supplemental Nutrition Assistance Program Households.” American Journal of Agricultural Economics 98(2): 564–580.

Telford, T., and A. Bhattarai. 2020, March 2. “Long Lines, Low Supplies: Coronavirus Chaos Sends Shoppers into Panic-Buying Mode’. Washington Post. Available online: https://www.washingtonpost.com/business/2020/03/02/grocery-stores-coronavirus-panic-buying/ [Accessed July 3, 2020].

U.S. Bureau of Labor Statistics. 2020, July. “June 2020.” Employment Situation 42. Available online: https://www.bls.gov/bls/news-release/empsit.htm.

U.S. Department of the Treasury. 2020. “The CARES Act Works for All Americans.” Available online: https://home.treasury.gov/policy-issues/cares [Accessed August 5, 2020].

U.S. Internal Revenue Service. 2020, July 18. “Basic Information on the Stimulus Payments.” Available online: https://www.irs.gov/newsroom/basic-information-on-the-stimulus-payments [Accessed July 9, 2020].

Walmart. 2020, March 27. “Answering Your Questions”. Available online: https://corporate.walmart.com/answering-your-questions [Accessed July 19, 2020].

Walmart. 2020. “How We’re Responding to COVID-19.” Available online: https://corporate.walmart.com/here-for-you [Accessed July 3, 2020].

Wida, E. 2020, March 16. “Which States Have Closed Restaurants and Bars Due to Coronavirus?” Today. Available online: https://www.today.com/food/which-states-have-closed-restaurants-bars-due-coronavirus-t176039 [Accessed July 2, 2020].