Promoting business start-ups and small business activity can stimulate competition and an entrepreneurial spirit within rural communities, which in turn, enhances efficiency, innovation and productivity growth. To succeed, smaller businesses need to be able to adapt to changing environments with flexible production technologies and business strategies. New and small businesses are often a source of experimentation and innovation. By pushing the frontier, they play a vital role in the innovative processes that drive economic growth and development. The importance of business start-ups and a network of smaller businesses to the viability of the local economy has become increasingly recognized by policy makers, as well as rural development researchers and community leaders (Shaffer, Deller, and Marcouiller, 2006; Deller and Goetz, 2009). Several recent studies have found that start-ups are critical to both gross and net job growth (Conroy and Deller, 2015, Haltiwanger and Miranda, 2013, Decker et al., 2014).

Not all start-ups or small businesses are innovative—meaning those that bring a new product, process, or service to market. Many start-ups and small businesses are classified as common or reactionary. Common small businesses are aimed at taking advantage of local market opportunities such as a small grocery or hardware store, residential remodeling business, or accounting business. The owners of these common businesses seldom plan to grow beyond a certain, often modest, size. Some business owners elect to keep their business small because they have a passion for their work or craft and want to spend time on the work that inspired them to start the business rather than managing employees and operations. Reactionary small businesses are those started out of necessity by people who would prefer, but cannot find, wage and salary employment. Often when wage and salary employment becomes available the owner transitions out of self-employment and the business closes.

While community leaders would prefer to foster innovative and high-growth businesses that become a major source of local employment, in rural areas most tend to be characteristically common. Although not necessarily considered as innovative, common and reactionary small businesses can be important to rural communities. Many of these businesses are labor-intensive and, in addition to generating reliable income for the owner herself, may be better positioned to promote modest but sustainable employment growth. They can also draw workers from secondary markets including those with less education or lower skill levels. Because many of these businesses are highly dependent on a small number of employees, there tend to be stronger relationships between workers and managers. In these cases, the owners often view their workers as “family” and have a sense of commitment to their employees minimizing the likelihood of lay-offs. Even if these are not growth businesses they can improve the quality of life by providing stable employment to their employees as well as goods and services that may not otherwise be available in their community. A wider breath of small business activity is important in order to have a critical mass of “potential” firms that could become high-growth firms.

Focusing on new business start-ups as the primary economic growth and development strategy is often met with the concern that many, if not most, start-ups fail during their early years. In rural areas, a small business closure is often quite visible and widely known across the community. Because it is often viewed as a failure, it can create an environment within the community where potential entrepreneurs become risk averse. The local disapproval of failure can discourage risk-taking related to both start-ups and expansion decisions, leading to a stagnant and even declining local economy.

The available research that explores the survival rates of rural businesses is limited in geographic scope. Studies tend to focus on a single or a very small handful of states making generalizations difficult. For example, in a study of rural Arkansas, Maine, and North Dakota, Buss and Lin (1990) found that over the study period start-ups had survival rates of 52%, 89% and 65%, respectively. Yu, Orazem, and Jolly (2011) found rural business six-year survival rates for Iowa and Kansas ranged between 50% to 70% depending on the year the business started.

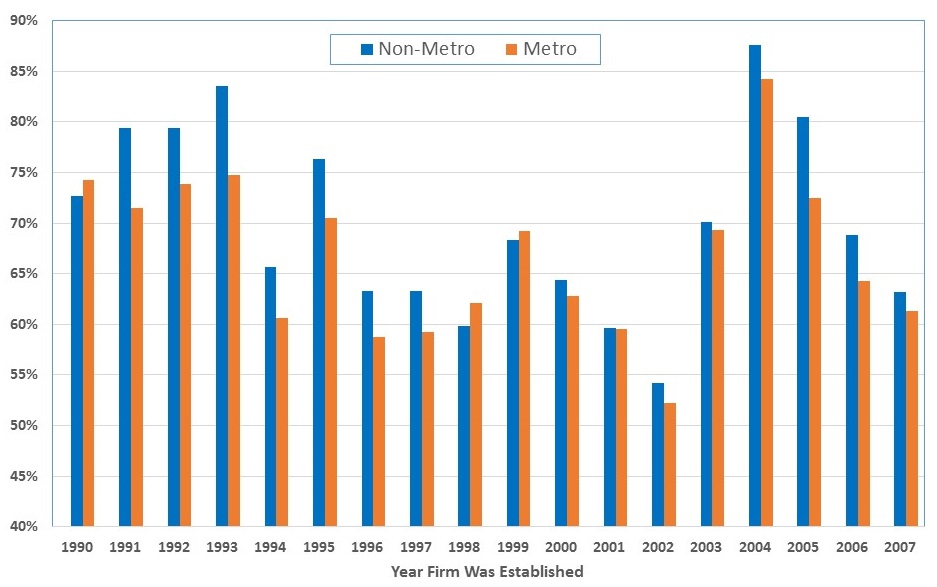

A national perspective of business survival rates is possible by using the whole of the National Establishment Time Series (NETS) database of U.S. establishments (see About the Data Box). Regardless of designation as either a rural or urban county, between 1990 and 2007, businesses in the typical county had a five-year survival rate of 69% (Figure 1). For all counties, firms started in 2004 had a peak of 87% five-year survival rate and for firms started in 2002 a low of 54%—a difference that, based on a set of traditional statistical tests, are statistically significant. This result is largely consistent with much of the economic literature, such as Yu, Orazem, and Jolly (2011), and suggests that macroeconomic trends, particularly the ebbs and flows of the larger economy, can greatly influence survival rates. This is most evident in the period leading up to the Great Recession: businesses started in the years immediately preceding the Great Recession tended to have lower survival rates.

The NETS database is continually updated by Dun & Bradstreet (D&B) in partnership with Walls & Associates. The NETS database is uniquely detailed and includes data for every firm in the United States from 1990 to 2012. In this analysis, new (start-up) firms were track over a five-year period to derive five-year survival rates. These firms were then aggregated to the county level to derive the typical five-year survival rates for business start-ups by birth year for any given county in the U.S. This resulted in over 56,000 county observations.

Source: Calculations based on the National

Establishment Time Series.

Note: For businesses started 1990-2007.

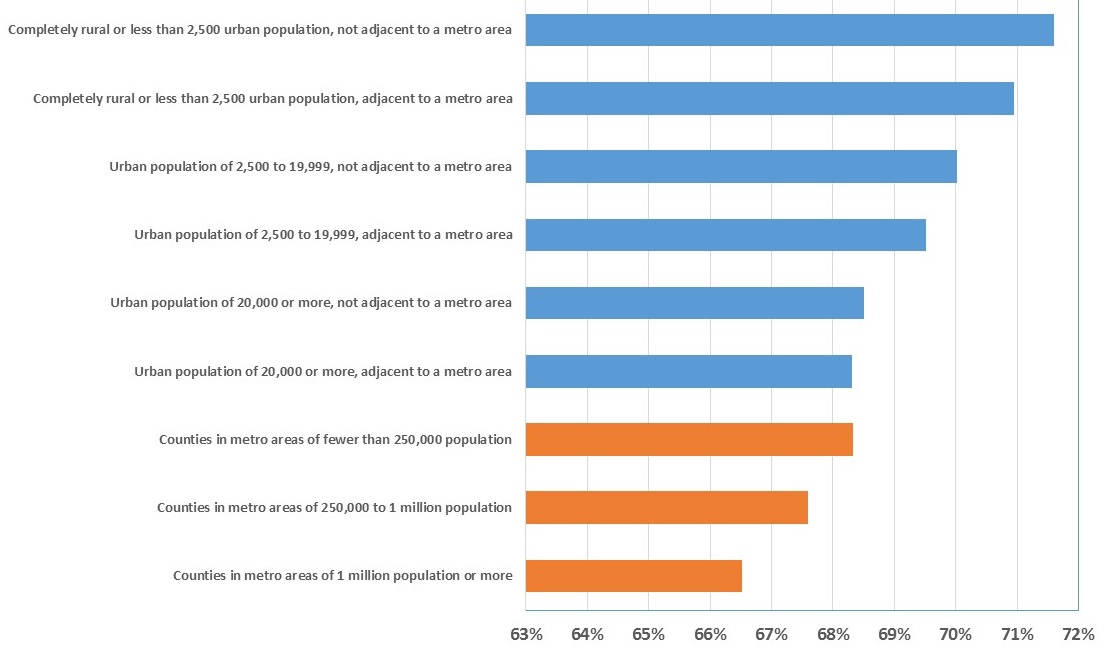

Source: Calculations based on the National

Establishment Time Series.

Across the rural-urban divide the average five-year survival rate across all birth year cohorts for urban (metro) counties was less than for rural (non-metro) counties, 67% and 70%, respectively. This is consistent with the findings of others (Buss and Lin, 1990; Renski, 2009; Yu, Orazem, and Jolly, 2011). If the definitions of rural and urban are refined along a broader spectrum from large urban to remote sparsely populated rural, the relatively high survival rates in rural areas becomes even more pronounced (Figure 2). In fact, the analysis reveals a survival gradient along the rural-urban spectrum. At the extremes, new businesses in remote small rural areas have a five-year survival rate of 72% which is statistically significantly greater than the largest urban areas where the rate is 67%.

There are three lines of reasoning offered to explain why the survival rates are higher in rural communities. First, the number of business start-ups tends to be much lower in rural areas compared to urban. Consequently, the level of competition from other businesses may not be sufficiently high to force less profitable businesses out of the market thus leading to a higher survival rate.

Second, opportunity costs for unprofitable businesses are higher in urban areas when compared to rural areas because there are usually more job and business opportunities in a larger market. Thus, in an urban setting the costs associated with “riding-out” poor business performance is higher: there are more, and likely, better opportunities to move out of one business (exit) and into a new one (start-up) or transition into wage-and-salary employment in urban areas. Rural business owners are more likely to “ride it out” because there are fewer alternatives.

A third element that has not received as much attention within the economic literature is variations in attitudes about risk across rural and urban areas. Existing and potential rural business owners might be more risk averse or conservative in business strategies because there are fewer employment options if their business is not successful. In urban markets, business owners might be willing to take on riskier business ideas because, if it fails, they can easily try another venture or return to the labor market as a wage-earner. Further, in rural communities where business owners are known figures in the community one’s social standing may be at risk if the business is a failure, particularly if bankruptcy is an outcome.

Dynamic local business churn (start-ups and exits) is consistent with a healthy business environment and strong economy. At the local level, there are a number of potential policy levers that can affect these local business dynamics. Support for new business owners, even those that do not yet have employees, will lead to a more dynamic local economy. Support programs need to be crafted to recognize three stages of new business development: the preplanning stage where people are thinking about starting a business, the actual start-up, and the first five years of operation. A potential fourth stage is the growth phase where businesses make the transition from small- to medium-sized. Efforts that are associated with “economic gardening” programs are widely linked to this fourth stage of business development. Support programs that aid start-ups would also need to be present to help businesses especially during their first five years. In addition to networking, mentoring and educational programs, the community may need to review broader community policies such as zoning restrictions on home-based businesses.

Specific strategies vary at the state and local levels due to institutional differences—for example, the ability to alter prevailing laws—and available resources. In essence, the state is in a better position to implement some strategies while individual communities are better positioned to pursue more tailored strategies. Providing educational opportunities for people interested in starting a new business or expanding a relatively young business, for example, can vary significantly at the state and local levels. The state has the resources of public universities and technical colleges to steer formal programs, the types of which local communities cannot offer. Community-level efforts through local institutions, such as chambers of commerce and business associations, can be more flexible and offer more informal, tailored educational workshops and seminars to help local small and new businesses. Ideally, state and local resources are complementary and supportive of each other.

The state also has the authority and resources to create and fund business start-up financing programs such as business planning grants or loan guarantee programs. Local institutions, such as community development corporations and chambers of commerce, among others, can help inform local entrepreneurs about the availability and appropriateness of such financing programs. Local communities can also tap into state resources, including but not limited to university cooperative extension services, to help conduct local economic analyses for the benefit of potential entrepreneurs. Such information can help identify economic strengths, and weaknesses, of the local or regional community as well as the local/regional comparative advantages, or economic clusters, that local entrepreneurs can use to build business opportunities

At the community level, tapping local resources to provide technical and moral support to young businesses and more importantly people who are interested in starting a new business can be an effective strategy. Many communities have recruited local business experts, such as local bank small loan officers, accountants, and information technology experts, to provide mentoring and counseling opportunities. Counseling and mentorship can take place in formal and informal workshops or in local business incubators both built and virtual. Networking opportunities where new business owners, including those thinking of starting a business, can learn from each other as well as more established local business owners are best achieved at the local level.

Communities that network existing business owners with those within the community who are interested in business ownership can help sustain those existing businesses by facilitating succession. For example, Ayres, Leistritz, and Stone (1992) find that many local business owners elect to retire and close the business rather than sell it. Ayres and her colleagues found that in more “successful” communities, existing business owners are networked with those in the community who are interested in going into business for themselves and may be potential buyers for their business.

In the end, the promotion of entrepreneurial activity at all levels is vital for a dynamic and vibrant local economy whether it be a large urban city or a remote rural village. Communities that foster, nurture and support business at the point of start-ups and those all-important first five years of operation through networking, educational, technical and mentoring services will prove to foster stronger local economies and communities.

Ayres, J., L. Leistritz, and K. Stone. 1992. "Rural Retail Business Survival: Implications for Community Developers." Community Development 23(2): 11-21.

Buss, T. F. and X. Lin, X. 1990. ”Business Survival in Rural America: A Three State Study.” Growth and Change, 21 (3), 1–8.

Conroy, T. and S.C. Deller. 2015. “Employment Growth in Wisconsin: Is it Younger or Older Businesses, Smaller or Larger?” Patterns of Economic Growth and Development Study Series No. 3. Department of Agricultural and Applied Economics, University of Wisconsin-Madison/Extension.

Decker, R., J. Haltiwanger, R. Jarmin, and J. Miranda. 2014. “The Role of Entrepreneurship in U.S. Job Creation and Economic Dynamism.” Journal of Economic Perspectives, 28(3), 3–24.

Deller, S.C. and S. Goetz. 2009. “Historical Description of Economic Development Policy.” In S. Goetz, S.C. Deller and T. Harris. (eds). Targeting Regional Economic Development. London: Routledge Publishing.

Haltiwanger, J., R. Jarmin and J. Miranda. 2013. “Who Creates Jobs? Small versus Large versus Young.” Review of Economics and Statistics, XCV(2), 347–361.

Henderson, J. and S. Weiler. 2010. “Entrepreneurs and Job Growth: Probing the Boundaries of Time and Space.” Economic Development Quarterly, 24, 23–32.

Julien, P.A. 2007. A Theory of Local Entrepreneurship in the Knowledge Economy. Edward Elgar: Northhampton, MA.

Low, S. and A. Isserman. 2015. “Where are the Entrepreneurs? Identifying Innovative Industries and Measuring Innovative Entrepreneurship.” International Regional Science Review 38:2 171-201

Renski, H. 2009. “New Firm Entry, Survival, and Growth in the United States: A Comparison of Urban, Suburban and Rural Areas.” Journal of the American Planning Association. 75(1):60-77

Shaffer, R., S. Deller, and D.W. Marcouiller. 2006. “Rethinking Community Economic Development.” Economic Development Quarterly. 20(1):59-74.

Yu, L., P.F. Orazem, and R.W. Jolly. 2011. "Why Do Rural Firms Live Longer?" American Journal of Agricultural Economics 93(3): 669-688.