The 2014 farm bill, formally known as the Agricultural Act of 2014, fundamentally reduced the level of agricultural subsidies for all the program crops, and the bill changed the way that subsides are calculated by eliminating the Direct Payments, Countercyclical Payments, and Average Crop Revenue Election Payments and substituting revenue insurance programs, including the Stacked Income Protection Plan (STAX) for upland cotton—almost all cotton in the world is classified as upland.

Farm bills are products of diverse influences, including policy objectives, political pressures and budget limitations. The 2014 farm bill was uniquely influenced by an additional factor, the legal ramifications of the Brazil cotton case in the World Trade Organization (WTO).

In WTO parlance, upland cotton was treated “specifically” and “ambitiously,” within the 2014 farm bill, and such treatment would never have happened but for the legal pressure brought by Brazil under the Dispute Settlement Mechanism within the World Trade Organization (WTO), augmented by the force of moral suasion brought by African countries and their supporters within the Talks on Agriculture in the Doha Development Agenda (the Doha Round).

U.S. cotton exports nearly quadrupled from 4 million bales in crop year 1998/1999 to 17 million in 2005/2006. Yields rose from around 650 pounds per acre in the 1990s to 830 in 2005/2006, and production rose from 14 million bales to 24 million.

In addition, domestic use of cotton (mill use) dropped from 10 million bales in 1998/1999 to 6 million in 2005/2006 in response to competitive pressures from textile and apparel imports. With production rising while mill use was dropping, the amount of cotton available for export grew, and shipments naturally expanded.

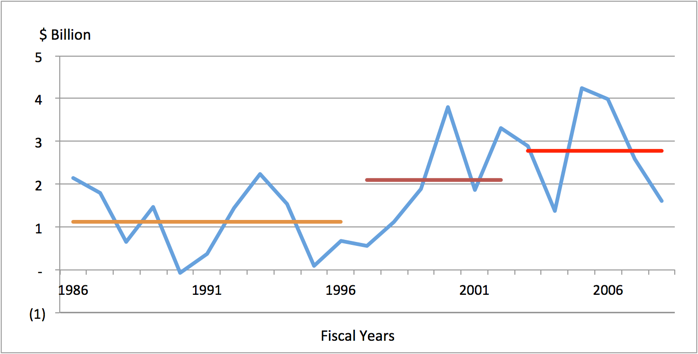

Source: Presidents’ Budget, 2014, Table 35.

CCC Net Outlays by Commodity and

Function.

However, there was another factor that seemed to drive U.S. production and exports to higher levels: subsidies. In the early 1990s, Commodity Credit Corporation (CCC) outlays for upland cotton averaged $900 million per year. Between 1997 and 2002 under the 1996 farm bill, outlays rose to an average of $2.1 billion per year, and between 2003 and 2008 under the 2002 farm bill, outlays for upland cotton rose to an average of $2.8 billion per year. To competing exporters, the correlation between U.S. cotton shipments and subsidies seemed too strong to be coincidence; they believed that subsidies caused the rise in shipments.

The increase in CCC outlays for cotton also drew attention from U.S. domestic critics of agricultural subsidies. The farm value of U.S. upland cotton production averaged $4.4 billion per year between 1998 and 2005. Using data from the U.S. Department of Agriculture, Economic Research Service (USDA-ERS) on the cost of production, the resource cost of producing that value averaged $6.1 billion, suggesting that the U.S. cotton industry was destroying around $2 billion in economic value each year and remained competitive among world exporters only because of subsides. Various critics of agricultural subsidies, such as the Environmental Working Group, Oxfam, and others, began to focus on cotton in their efforts to change U.S. farm legislation.

Brazil cotton production began expanding in the mid-1990s as large producers in central Brazilian states such as Matto Grosso learned that cotton made an excellent addition to their crop rotations with soybeans and maize. By the early 2000s, Brazil was emerging as a major cotton exporter, and cotton had become a big industry characterized by operations with thousands of hectares run by people with economic power and political savvy. Under the auspices of the Brazilian national cotton growers’ association (ABRAPA), cotton producers went to the government of Brazil and offered to pay the fees to hire lawyers and experts to challenge U.S. upland cotton subsidies in the WTO. With the private sector willing to pay the legal fees, the Brazilian government agreed to mount a challenge to U.S. cotton subsidies.

Following WTO protocol, Brazil requested consultations with the United States in September of 2002, contending that the subsidies paid to upland cotton growers between 1999 and 2002 violated the commitments made by the United States in the Uruguay Round Agreement on Agriculture (AoA) and the Agreement on Subsidies and Countervailing Measures (SCM).

The Dispute Settlement Body established a Panel in March 2003 (WTO, 2014). The Panel report was circulated in September, 2004, and the major findings were that agricultural export credit guarantees and several other subsides provided to upland cotton producers were prohibited under WTO rules. The United States appealed the Panel report, and the report of the Appellate Body was circulated in March 2005, essentially upholding the findings of the Panel that marketing loan payments, Step 2 payments—to exporters and users of upland cotton based on the difference between U.S. and non-U.S. cotton prices—market loss assistance payments and counter-cyclical payments caused “serious prejudice” to Brazilian exports of upland cotton by causing “significant price suppression” on the world market.

The U.S. government eliminated Step 2 payments administratively in July, 2006. However, the 2002 and 2008 farm bills mandated the counter cyclical, marketing loan, and market loss assistance payments, and they could not be eliminated or adjusted administratively. The United States exercised its rights to appeal, and at the end of the WTO process when those appeals had been lost, the United States concluded a Framework Agreement with Brazil in June 2010 and agreed to just pay Brazil $147.3 million per year to not exercise its right to retaliate against U.S. exports until new farm legislation could be passed.

And then there were the Africans, specifically the governments of Benin, Burkina Faso, Chad, and Mali, collectively known as the C4.

Cotton has been called a “litmus test” of the commitment of developed countries to the Development Round, and a “poster” for the Doha Development Agenda. It was not always so. The Doha Round was launched in 2001 with most countries eschewing sectoral specific initiatives, and if you were to have picked a commodity to serve as the poster for development within the Round, it would probably not have been cotton. The gross value of world cotton production is smaller than for other major crops. For example, the gross value of world cotton production in 2001 when the Doha Round was launched was about $30 billion. In contrast, maize was $87 billion, soybeans $49 billion, sugar cane as well as beets were $52 billion, and wheat was $93 billion (FAO, 2015). Additionally, cotton is primarily a fiber crop, not a food crop, which means it is not usually associated with food security, a traditional focus of government concern.

Cotton rose to prominence in the Doha Round because the President of Burkina Faso attended a WTO meeting in 2003 (it is unusual for a head of state to attend such a meeting) and demanded that cotton be addressed specifically. Speaking on behalf of the C4 and all developing country cotton exporters, he noted that cotton is the only good of any significant value exported by the C4, and he asserted that subsidies in developed countries depressed world prices thus hindering efforts at income generation and economic development in developing countries. He stated simply that the C4 could not support completion of the Round unless the cotton issue was resolved, an ominous threat in an institution that requires unanimity.

The prominence of cotton became official in 2005 at a WTO meeting in Hong Kong, when member governments agreed to treat cotton ambitiously, specifically, and expeditiously within the talks on agriculture in the Doha Development Agenda, the only commodity singled out for specific treatment. From then on, at every WTO meeting in which agriculture was discussed, cotton was a prominent part of each conversation. At every opportunity, the C4 and its allies hammered away at the United States, and to a smaller degree the European Union (EU), for subsidies provided to cotton growers. U.S. representatives to WTO meetings were always on the defensive.

The U.S. position in the WTO regarding cotton was further weakened in 2006 when the European Union revised its program for cotton under the Common Agriculture Policy (CAP) to substantially reduce production aid and substitute decoupled payments. While the EU is not a large producer of cotton, the change to the CAP had a positive demonstration effect from the perspective of those opposed to agricultural subsidies and further isolated the United States on the cotton issue.

By the mid-2000s, a perfect storm of legal pressure brought by Brazil, moral pressure brought by the Africans and their supporters, political pressure brought by various U.S. interest groups opposed to farm subsidies, and budget pressures affecting all federal government outlays was building against the U.S. cotton industry and the cotton program. And, because the programs for the other covered crops were similar to the program for cotton, the programs for all the covered commodities implicitly faced the same pressures.

To its credit, the National Cotton Council of America (NCC), the umbrella organization representing all segments of the U.S. cotton value chain, responded proactively to these pressures by developing the proposal revenue insurance that was eventually adopted, rather than waiting to be overwhelmed by the pressures for change.

According to USDA, STAX addresses U.S. obligations under the WTO (USDA ERS - Agricultural Act of 2014: Highlights and Implications: Crop Insurance). After some rhetorical chest beating, the government of Brazil agreed. In October 2014, the government of Brazil signed an agreement with the United States effectively ending the cotton case.

STAX provides revenue insurance to producers of upland cotton. Indemnities will be calculated as the difference between projected prices at planting time multiplied by historical yields in each county and actual prices at harvest multiplied by actual yields in each county.

Under STAX, if revenue in a county falls below 90% of the estimated revenue at planting time, upland cotton farmers in that county who have paid the premiums to buy STAX insurance will receive indemnity payments equal to the difference but no more than 20% of expected revenue. STAX will be available for purchase on all acres planted to upland cotton.

Crucially, STAX will not provide insurance against declines in cotton prices from one season to the next. STAX is essentially, a government-operated and subsidized program to assist cotton producers in hedging their crop for five or six months between planting and harvesting each season. Farmers participating in STAX will be able to pledge to a bank any resulting indemnities as collateral against production loans, and therefore banks will more readily make such loans for cotton production.

The premiums for STAX will be calculated on an actuarially sound basis, which means that over several seasons, indemnities are expected to equal premiums. However, the government will pay 80% of the premiums, and the government will cover all administrative costs, which will be substantial, given that there are about 9,000 upland cotton farmers in the United States; operating about 250,000 separate cotton farms in about 700 counties, and separate calculations must be made in each county.

The upland cotton marketing loan program will continue, just as it has since 1986. However, under the 2014 farm bill, the national average loan rate can range between $0.45 cents and $0.52 cents, depending on a simple two-year moving average of the adjusted world price (AWP). The loan rate for upland cotton was previously fixed at $0.52 cents per pound.

In addition, the program known as Economic Assistance to Mills will continue. This program provides $0.03 cents per pound in direct subsidy to U.S. textile mills using upland cotton.

| If the 2008 farm bill were still in effect: | ||||

|---|---|---|---|---|

| Target Price | $/Lb. | 0.71 | ||

| Farm Price, est. 1/ | $/Lb. | 0.60 | ||

| Direct Payment | $/Lb. | 0.06 | ||

| Deficiency Payment | $/Lb. | 0.04 | ||

| Total Support per pound | $/Lb. | 0.10 | ||

| Average Yield | Lbs./Acre | 800 | ||

| Support per Acre | $/Acre | 80.00 | ||

| Under the 2014 farm bill: | ||||

| Projected Price Dec (ICE futures, Jan 2015) | $/Lb. | 0.63 | ||

| 5-year Avg County Yield, typical county | Lbs./Acre | 800 | ||

| Expected County Revenue | $/Acre | 504 | ||

| 90% | $/Acre | 454 | ||

| 70% | $/Acre | 353 | ||

| Actual Price (December ICE futures, Oct 2015) 2/ | $/Lb. | 0.65 | ||

| Actual County Yield, assumed | Lbs./Acre | 800 | ||

| Actual County Revenue | $/Acre | 520 | ||

| Indemnity | $/Lb. | 0 | ||

| STAX Premium | $/Acre | -$10 | ||

Source: Congressional Budget Office’s March 2015 Baseline for Farm Programs

Because the 2014 farm bill was enacted after the deadline by which the new provisions could have been implemented for 2014, STAX was not available until 2015, for the 2015/2016 (August/July) season. The impact of the 2014 farm bill is shown by comparing the payments that would have been expected by upland cotton producers during 2015/2016 if the provisions of the 2008 farm bill were still in place to the indemnities that are likely to be collected during 2015/2016 under STAX.

Under the provisions of the 2008 farm bill, the cotton target price was $0.7125 cents per pound. Current projections for the 2015/2016 average cotton farm price by USDA are a range between $0.50 and $0.70 cents per pound with a mid-point of $0.60 cents. Assuming the projection of $0.60 cents per pound proves to be correct, owners of upland cotton base area would expect to receive direct payments of approximately $0.06 cents per pound and producers would receive deficiency payments of about $0.05 cents per pound on 85% of the their base acres. Total support to the sector would be about $0.10 cents per pound or around $80 per acre at average yields.

In contrast, under STAX, premiums may exceed indemnities in 2015/2016. Premiums average about $10 per acre. The average closing value of the December 2015 Intercontinental Exchange (ICE) cotton futures contract was about $0.63 cents per pound from mid-January to mid-February 2015. As of mid-June 2015, the December contract has risen a bit to around $0.65 cents per pound. If the December 2015 contract remains near this level through October, there would need to be a drop of 10% in yields below average levels before participating farmers would be eligible for any indemnity.

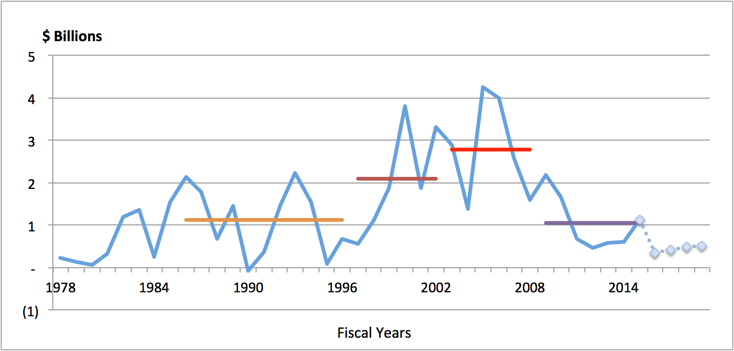

During the eight fiscal years ending in September 2003 through September 2008, corresponding to the 2002 farm bill, average CCC expenditures on upland cotton were $2.8 billion per year.

During the seven fiscal years ending in September 2009 to September 2015, corresponding to the provisions of the 2008 farm bill with the transition payments for 2014/2015, expenditures on upland cotton are estimated to average $1 billion per year.

Based on USDA estimates of average farm prices and production during the life of the 2014 farm bill, the Congressional Budget Office estimates that CCC outlays for upland cotton including: Net Lending, Loan Deficiency Payments, and Economic Assistance to Mills, will average just $450 million per year during fiscal years 2016 through 2019, corresponding to crop years 2015/2016 through 2018/2019 (Congressional Budget Office, 2015).

Thus, expenditures under the 2014 farm bill are estimated at about one-sixth of CCC expenditures under the 2002 farm bill and about two-fifths of expenditures under the 2008 farm bill.

Many farmers view program support as an entitlement in a world in which other countries also subsidize their products, and U.S. cotton farmers are bitter that they have been singled out for attention within the WTO. Many farmers blame Brazil and the WTO for having attacked “their” program. And, after crops are marketed and bank balances reconciled following the 2015 harvest and farmers experience the reality of a program that no longer provides either Direct Payments or Counter Cyclical Payments when world prices have fallen, there is likely to be more anger.

It is ironic that cotton producers, who are dependent on exports for approximately three-fourths of total commodity disappearance, are deeply disenchanted with U.S. membership in the WTO. Multiply the cotton experience across many sectors of the U.S. economy, and you begin to understand why President Barack Obama is having difficulty garnering support for current trade negotiations.

The U.S. cotton industry, dominant in the world market for decades, has become inefficient under the regimen of subsidies provided during the 1980s, 1990s, and 2000s, destroying billions of dollars in wealth every year. Because of the disciplines to domestic support brought by the rules-based multilateral trading system, some farmers will leave cotton, either for retirement or to produce other crops with higher net returns. Eventually, the U.S. cotton industry will shrink, but surviving producers will be more efficient than those who left.

Another irony of the Brazil cotton case and the efforts by the C4 in the Doha Round is that neither Brazil nor Africa is likely to benefit much from reduced exports of cotton from the United States. Soybeans and corn are the dominant crops in rotations in Brazil, and with grain and oilseed prices supported by biofuel mandates, Brazilian producers are de-emphasizing cotton. African producers remain hobbled by poor infrastructure, weak institutions, and low levels of technology adoption, and cotton production is not likely to climb substantially, whether there are opportunities for export or not.

The changes imbedded in the 2014 farm bill represented a belated acknowledgement by the United States of legal obligations agreed under the Uruguay Round of trade negotiations within the General Agreement on Tariffs and Trade (GATT) completed in 1994. The 2014 farm bill with the provision of STAX for upland cotton proves that the multilateral trading system has concrete and substantial power, even though the Doha Round has not been completed after more than a decade of negotiations.

Congressional Budget Office. https://www.cbo.gov/sites/default/files/cbofiles/attachments/44202-2015-03-USDA.pdf

United Nations Food and Agriculture Organization (FAO). 2015. FAOSTAT Data. Available online: http://faostat3.fao.org/home/E.

World Trade Organization (WTO). 2014. “United States – Subsidies on Upland Cotton.” Available online: https://www.wto.org/english/tratop_e/dispu_e/cases_e/ds267_e.htm.

National Cotton Council of America. 2013. Brazil WTO Case Framework Agreement Summary/Background. Available online: http://www.cotton.org/issues/2013/brazframe.cfm.

United States Department of Agriculture, Economic Research Service. 2014. Agricultural Act of 2014: Highlights and Implications: Crop Insurance. Available online: http://www.ers.usda.gov/agricultural-act-of-2014-highlights-and-implications/crop-insurance.aspx#.U0_hol54X1o.