Nitrogen fertilizer is a critical input for crop production and represents a major variable cost for several U.S. crops (especially corn and wheat). Farmers represent the end users in the fertilizer supply chain, and the prices they pay for fertilizer depend on a number of factors including local demand, product type, retailer markups, transportation costs, and the economics of fertilizer production.

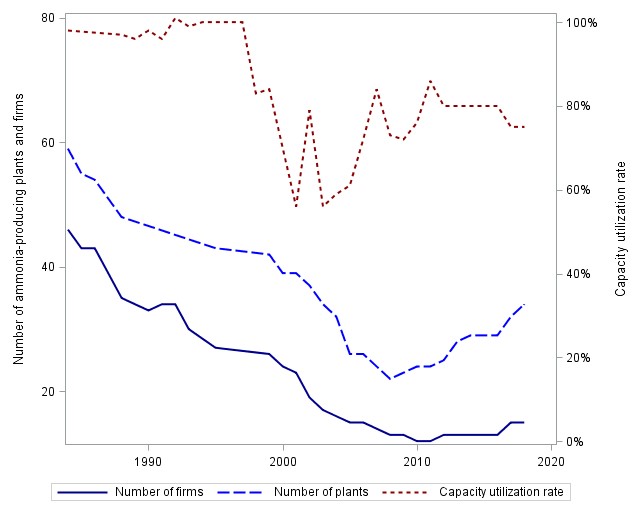

The U.S. nitrogen fertilizer production sector has undergone substantial changes over the past 40–50 years, influenced by a combination of agricultural market conditions, farm and bioenergy policies, and technological innovations for extracting natural gas—the primary input into the production of nitrogen fertilizer. Between the 1980s and mid-2000s, the combination of lower fertilizer demand and higher fertilizer production input costs caused the sector to contract from 59 to 22 production facilities. During the same period, the industry also underwent considerable consolidation, with the number of firms declining from 46 to 13.

In the mid-2000s, biofuel policies increased the demand for corn and, hence, the demand for fertilizer by corn producers while hydraulic fracturing technologies lowered natural gas prices. The combination contributed to a resurgence of U.S. nitrogen fertilizer production. However, despite the renewed growth within this sector, market consolidation continued. In 2019, four firms represented approximately 75% of total domestic nitrogen fertilizer production.

As domestic nitrogen fertilizer production capacity nears the level at which it can fully satisfy U.S. crop production demands, the persistence of market consolidation within the fertilizer production sector may affect market participants across the entire fertilizer supply chain. Hence, it is important to assess these effects, determine whether these effects are market distorting, and, if so, whether policy or market interventions could be used to mediate potential distortions. Understanding the factors that led to the most recent contraction, how markets changed and concentrated during this period, and what effects these changes may have on the evolution of the currently expanding U.S. fertilizer industry is important for assessing the future of a sector that is critical to U.S. food production.

Nitrogen is a component of chlorophyll and amino acids that all plants require and is necessary for the production of protein. Nitrogen availability and timing is critical for plants to achieve their full yield potential. Prior to the twentieth century, farmers used organic animal waste to fertilize crops. The desire to obtain such fertilizer was a primary impetus for the 1864 Spanish–South American War that began with Spain’s occupation of the guano-rich Chincha Islands. However, the use of animal manure could not adequately supply the specificity or quantity of nitrogen needed by the commercial agriculture sector.

In 1898, the British Association for the Advancement of Science encouraged chemistry researchers to develop processes to synthetically manufacture nitrogen fertilizer to help feed growing populations in Great Britain. In 1909, a German scientist, Fritz Haber, discovered the chemical reaction needed to produce ammonia (the basic building block of synthetic nitrogen fertilizer) by combining air and hydrogen. In 1914, German chemist and engineer Carl Bosch developed a commercial-scale ammonia production process. Haber won a Nobel Prize in 1920 for his research; in 1932, Bosch and Frederick Bergius received a Nobel Prize for their development of chemical high-pressure production methods.

The Haber–Bosch process produces ammonia nitrate. The process uses high temperature, pressure, and a catalyst to produce ammonia from the combination of air and hydrogen (derived primarily from natural gas). Industrial-level production also requires large amounts of water. While ammonia contains a high percentage of nitrogen, it is relatively unstable and additional inputs (e.g., carbon dioxide, nitric acid) are used to create more stable nitrogen-containing products such as urea, urea ammonium nitrate (UAN), and anhydrous ammonia. Nitrogen fertilizer is usually measured using product-specific volumes or by converting individual product volumes to total nitrogen (N) using the percentage of nitrogen contained in each product. For example, common fertilizers used for agricultural production include anhydrous ammonia (containing 82% N), ammonium nitrate (35% N), urea (46% N), and UAN (either 28% or 32% N).

The U.S. ammonia industry was initially developed to supply the primary material needed for the production of explosive munitions during World War II. After the war, the output of those plants transitioned into the production of nitrogen fertilizer products. The product output of ammonia plants varies based on specific plant technologies and market conditions. However, 80%–92% of ammonia produced in the United States is transformed into nitrogen-fertilizer products (U.S. Geological Survey, 2019). Hence, market trends in the ammonia industry generally reflect market conditions of the U.S. nitrogen fertilizer sector.

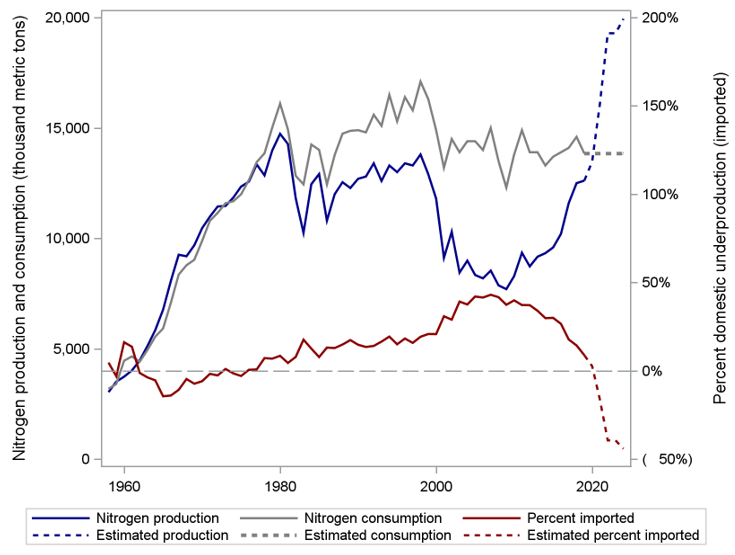

Notes: Percentage imported represents the proportion of nitrogen fertilizer

that would be necessary to fully meet domestic consumption relative to

what is produced domestically.

Figure 1 shows domestic nitrogen fertilizer production, consumption, and net imports data for 1960–2018 and Figure 2 characterizes the number of firms and total production plants for 1980–2018. The figures describe an industry that has undergone a major contraction followed by renewed expansion, but one that is unlikely to return the industry to its original market structure.

Prior to the early 1980s, U.S. nitrogen fertilizer production essentially met or exceeded total domestic demand and consisted of many relatively small firms. However, throughout the 1980s, a combination of domestic and global events prompted significant changes to the U.S. ammonia and fertilizer industries, and increased nitrogen fertilizer imports. The decade was generally characterized by relatively low agricultural commodity prices. Consequently, the U.S. government enacted farm programs in the early 1980s (particularly the Conservation Reserve Program) that, coupled with unfavorable commodity markets, contributed to the removal of one-sixth of U.S. cropland from production. These market and government program changes decreased nitrogen fertilizer demand throughout the 1980s. Figure 1 shows that throughout the decade, U.S. fertilizer use declined by 22% relative to its peak in 1979 and 1980.

In addition to decreased domestic demand for nitrogen fertilizer in the 1980s, the U.S. ammonia industry also experienced substantial increases in the price of its primary input, natural gas (U.S. Energy Information Administration, 2019). Natural gas represents 70%–90% of nitrogen fertilizer variable production costs. Additionally, the development of natural gas fields in Canada, the former Soviet Union, and Trinidad and Tobago in the 1980s and 1990s increased the competitiveness of ammonia and nitrogen imports. Figure 1 shows that one consequence of these competitive pressures was a large increase in nitrogen fertilizer imports, which began to steadily rise throughout the 1980s and peaked in 2007, when the United States imported over 43% of its nitrogen fertilizer.

Because of lower demand and high input costs, the U.S. ammonia and fertilizer sector underwent major changes throughout the 1980s, 1990s, and early 2000s. Figure 2 shows the impacts of these factors on the U.S. domestic ammonia industry. Between 1984 and 2008, the number of active ammonia-producing plants decreased from 59 to 22 (a 63% reduction). Further, Figure 2 shows that plants with continued operations did not operate at full capacity with utilization rates declining to 56%. The figure also shows that this period was characterized by significant consolidation of the domestic industry, perhaps as less efficient firms were forced to exit the sector and other firms expanded to take advantage of scale economies. Between 1984 and 2008, the number of firms decreased from 46 to 13 (a 72% reduction). As of 2018, the four largest U.S. ammonia producers represented 75.3% of total U.S. output.

Just as changes to the U.S. fertilizer industry in the 1980s were prompted by a combination of government policy and market factors, so too was the industry’s renewed transformation that began in the late 2000s and has continued throughout the 2010s. Beckman and Riche (2015) and Bekkerman, Gumbley, and Brester (2020) note two changes that have structurally altered the U.S. nitrogen fertilizer sector: the enactment of a suite of government policies that prompted the rapid expansion of the corn-based biofuels industry and the growth of hydraulic fracturing technologies for natural gas extraction.

A portfolio of U.S. ethanol policies, record world oil prices, and technological changes combined to rapidly expand the U.S. market for corn-based ethanol. Initially, bans on methyl tert-butyl ether (MTBE)—a petroleum-based oxygenate that had been used to replace lead in gasoline as a pollution reduction measure since 1996—around 2006 increased demand for substitute additives, which was primarily corn-based ethanol. The U.S. and various state governments also enacted numerous subsidies for ethanol producers in an attempt to bolster the farm sector while concomitantly establishing ethanol import tariffs to protect the industry (Tyner, 2008). In 2005 and 2007, two renewable fuel standards policies were instituted—the Energy Policy Act and the Energy Independence and Security Act—which mandated a minimum annual use of biofuels. Because of a lack of alternative cost-effective feedstock inputs, corn-based ethanol became the primary product used to meet these mandates. In addition, record world oil prices in 2008 made ethanol an economically viable substitute in blended gasolines and contributed to a major expansion of ethanol production in the United States (Tyner, 2008).

Corn production is particularly dependent on nitrogen fertilizer, which represented 37%–50% of corn production variable costs between 1996 and 2016 and accounted for approximately half of total U.S. nitrogen fertilizer use (USDA Economic Research Service, 2019a). During the mid-2000s, the U.S. corn market experienced a major structural shift. The proportion of corn used for fuel (ethanol) production increased from an average of 11% annually during 2000–2006 to approximately 37% annually during 2007–2018 (USDA Economic Research Service, 2019b). Concurrently, average U.S. corn acreage increased from 79.1 million acres in 2000–2006 to 91 million acres in 2007–2018 and average farm-level corn prices nearly doubled ($2.24 per bushel to $4.30 per bushel). These changes were largely the result of several U.S. energy policies (with many focused on encouraging ethanol production). Abbott (2013, p. 3) notes that these energy policies “helped to create a new, large, and persistent demand for corn,” which increased the level and altered the dynamics of corn prices (Abbott, Hurt, and Tyner, 2011; Condon, Klemick, and Wolverton, 2013).

Notes: Natural gas prices are the Henry Hub natural gas spot price per

million Btu.

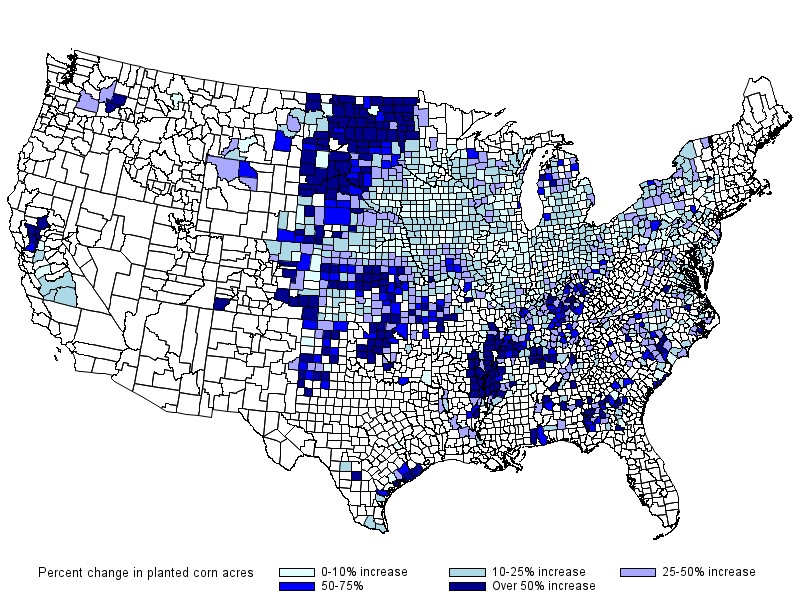

Notes: Percentage increases in each county are defined as changes

between five-year planted acre averages. Values are the percent change in

average planted acres between 2003-2006 and 2011-2015. Using the

average aids in reducing potential influence of nonrepresentative outliers,

such as a single-year increase or decrease. Counties without a color

designation either did not plant corn or had a decrease in planted corn acres.

Figure 3 shows that shortly following the enactment of these policies and subsequent expansion of the U.S. biofuels industry, corn demand and corn prices also experienced structural upward shifts. Naturally, U.S. farmers responded by increasing corn production. Figure 3 shows that between 2007 and 2018, farmers planted, on average, 10 million more acres annually than the average of the preceding two decades.

The expansion of U.S. corn production represented a boon to the fertilizer sector because corn is a nitrogen-intensive crop. Further, increased nitrogen demand may have been further bolstered by two factors. First, the continued development of higher-yielding corn varieties during the 1990s and 2000s meant that larger fertilizer quantities were needed to meet yield potentials. Second, Figure 4 shows that much of the expanded corn acreage occurred in the northern Great Plains, where corn had not previously been a major crop alternative. This was made possible not only by higher corn prices but also by the genetic development of shorter-season corn varieties. In these locations, fertilizer demand growth was relatively larger than in traditional Midwest corn producing areas as corn production displaced other crops (e.g., wheat, barley) that are less nitrogen intensive. The expansion of U.S. corn production after the mid-2000s resulted in stronger causal relationships between corn and ammonia prices (Beckman and Riche, 2015) and nitrogen fertilizer prices (Bekkerman, Gumbley, and Brester, 2020).

In addition to demand-side changes to the U.S. fertilizer market, the late 2000s also experienced a major technological advancement in natural gas production. Hydraulic fracturing and horizontal drilling methods allowed for the development of new oil and natural gas fields in the northern part of the United States as well as increased natural gas output in existing fields in the central and southern Great Plains. These innovations allowed the economical extraction of oil and natural gas from “tight” shale fields. Figure 3 shows the resulting sharp reductions in natural gas prices, which have remained at historically low levels and returned the United States to being one of the lowest-cost natural gas producers in the world.

The concurrent structural changes in the U.S. corn market (including genetic improvements that allowed for corn production outside of the Midwest Corn Belt) and natural gas extraction technologies during the mid- to late 2000s created nearly ideal conditions for the expansion of the U.S. fertilizer industry. Economic theory suggests that when profit opportunities arise, an industry will experience entry. Moreover, in an industry in which the output is a commodity and production technologies are well known (as is the case for the fertilizer industry), entry would likely occur relatively quickly.

Figures 1 and 2 show that, indeed, domestic production of nitrogen fertilizer significantly increased (reducing the difference between domestic consumption and production to 14%) and an additional 12 ammonia plants were added since the low of 22 in 2008. Between 2013 and 2018, six additional plants came online and seven plants expanded, representing approximately 3.14 million metric tons of new nitrogen fertilizer production capacity (Brown, 2018). In addition to producing higher quantities of widely used products such as urea, this expansion probably increased the demand for fertilizer products such as anhydrous ammonia, which is more safely and economically transported domestically relative to imports.

The expansion of production capacity, however, was coincident with increased market concentration. In 2018, the industry’s Herfindahl–Hirschman Index (HHI) was 2,387. The Department of Justice and Federal Trade Commission consider a market to be moderately concentrated if the sector’s HHI is between 1,500 and 2,500, and highly concentrated if an HHI exceeds 2,500 (U.S. Department of Justice, 2010). Governmental concerns about concentrated sectors result from statutory provisions of the 1890 Sherman Act (sections 1 and 2), the 1914 Clayton Act (section 7), and the 1914 Federal Trade Commission Act (section 5).

The assumption is that highly concentrated industries are synonymous with the exercise of market power in which output prices are higher than marginal costs of production and are not representative of competitive equilibria. Of course, the actual exercise of market power depends on many factors and is ultimately an empirical (although difficult to quantify) issue. On the other hand, the contestable markets hypothesis posits that competitive equilibria can occur in such markets if low entry barriers allow for a credible threat of entry (Baumol, Panzar, and Willig, 1983). In the case of nitrogen fertilizer, imports have represented over 40% of U.S. nitrogen use. Hence, one may surmise that global production and low import barriers provide a credible entry threat and help obviate the potential of market power. Nonetheless, consolidated industries certainly provide a higher potential for the use of market power relative to less consolidated sectors.

Nitrogen fertilizer is a critical element of crop production in developed economies. The U.S. fertilizer industry began after World War II as ammonia production was shifted from its use in munitions to commercial fertilizer production. The industry generally produces fertilizer as a commodity and production technologies are well-known. Hence, entry barriers are low and the U.S. supplied almost all its domestic needs for many years. Reductions in the demand for fertilizer, simultaneous increases in domestic natural gas (which is the major variable input into the production of ammonia) prices, and lower natural gas prices in other world regions caused domestic firms to exit the industry. By 2006, 43% of U.S. fertilizer use was sourced from other countries.

The persistent increased demand for corn in the mid-2000s and extraction technologies that lowered natural gas prices caused the domestic industry to rebound so that only about 14% of nitrogen fertilizer is currently being imported. Figure 1 shows that additional capacity expansion announcements, if acted upon, would further increase U.S. nitrogen production capacity. The U.S. could potentially become a net exporter of nitrogen fertilizer. However, given current demands for nitrogen fertilizer, domestic capacity, low natural gas prices, and current degree of market consolidation in the fertilizer production sector, it appears that U.S. agricultural producers should not expect fertilizer prices to substantially decrease in the future.

Abbott, P. 2013. “Biofuels, Binding Constraints and Agricultural Commodity Price Volatility.” Cambridge, MA: National Bureau of Economic Research, Working Paper 18873, March. http://www.nber.org/papers/w18873.

Abbott, P., C. Hurt, and W. Tyner. 2011. “What's Driving Food Prices in 2011?” Oakbrook, IL, Farm Foundation, Report No. 741-2016-51225.

Brown, T., ed. 2018. “Ammonia Capacity in North America.” Ammonia Industry. Available online: https://ammoniaindustry.com/ [Accessed April 24, 2018].

Baumol, W.J., J.C. Panzar, and R.D. Willig. 1983. “Contestable Markets: An Uprising in the Theory of Industry Structure.” American Economic Review 73(3):491–496.

Bekkerman, A., T. Gumbley, and G.W. Brester. 2020. “The Impacts of the Renewable Fuel Standards on Spatial and Vertical Price Relationships in the U.S. Fertilizer Industry.” Applied Economic Perspectives and Policy, forthcoming.

Beckman, J., and S. Riche. 2015. “Changes to the Natural Gas, Corn, and Fertilizer Price Relationships from the Biofuels Era.” Journal of Agricultural and Applied Economics. 47(4): 494–509.

Condon, N., H. Klemick, and A. Wolverton. 2015. “Impacts of Ethanol Policy on Corn Prices: A Review and Meta-Analysis of Recent Evidence.” Food Policy 51: 63–73.

Dutkowsky, M., G.W. Brester, and V.H. Smith. 2014. “International Agricultural Fertilizer Trade.” Bozeman, MT: Agrilcultural Marketing Policy Center, Briefing Paper No. 109, September. Available online: http://www.ampc.montana.edu/briefing.html.

Tyner, W. 2008. “The U.S. Ethanol and Biofuels Boom: Its Origins, Current Status, and Future Prospects.” BioScience 58(7): 646–653.

U.S. Department of Agriculture. 2014. Fertilizer Consumption and Use-By-Year Database. Washington DC: U.S. Department of Agriculture, Economic Research Service. Available online: http://www.ers.usda.gov/ [Accessed May 15, 2017].

U.S. Department of Agriculture, Economic Research Service. Feed Grain Yearbook Tables. Washington DC: U.S. Department of Agriculture, Economic Research Service. Available online: https://www.ers.usda.gov/data-products/feed-grains-database/feed-grains-yearbook-tables/ [Accessed January 20, 2019].

U.S. Department of Justice. 2010. Horizontal Merger Guidelines §5.3. Available online: https://www.justice.gov/atr/horizontal-merger-guidelines-08192010 [Accessed March 27, 2020].

U.S. Energy Information Administration. 2019. U.S. Natural Gas Pipeline and Distribution Use Price. Available online: https://www.eia.gov/dnav/ng/hist/na1480_nus_3a.htm [Accessed May 22, 2019].

U.S. Geological Survey. 2019. “Nitrogen (Fixed)—Ammonia.” Mineral Commodity Summaries. Multiple years. Available online: https://www.usgs.gov/centers/nmic/nitrogen-statistics-and-information [Accessed May 22, 2019].