Telser and Higinbotham (1977) established long ago that commodities that have an organized futures market have more (price) variability than those where such a market is absent. However, this does not automatically imply that futures markets and trading cause greater price variability. Neither theoretical models and literature nor empirical studies provide any consensus on the topic. The theoretical literature on the price stabilizing/destabilizing impact that futures trading has on spot prices of storable commodities is surprisingly inconclusive. Some of the most influential economists have engaged in this debate and could not reach a consensus. Kawai (1983) constructed a rational expectations model of storable commodities in which the existence of a futures market, which facilitates speculation, may destabilize the spot market. Based on his model, this holds even if one rules out speculative bubbles (Tirole, 1985) or market power and irrational behavior (Newbery, 1987). In contrast, Turnovsky and Campbell (1985) presented a rational expectations model in which futures markets always improve the stability of the spot market, supporting the conclusion reached by earlier, less satisfactory, theoretical investigations. In an important theoretical/empirical study, Deaton and Laroque (1996, p. 896) concluded, “Although speculation is capable of increasing the autocorrelation that would otherwise exist in an unmoderated price series, it cannot raise it to the levels that we observe.” In their view, futures markets contribute to a share of observed volatility in spot commodity prices. Most recently, Goetz, Miljkovic, and Barabanov (2021) refined Kawai’s model and reaffirmed his findings that the impact of futures markets on spot price volatility of storable commodities can be either stabilizing or destabilizing, depending on whether the dominant/prevailing disturbance in the commodity market comes from consumption, production, or inventory holding.

Contrary to these economic theory uncertainties, the broadly accepted standard in agricultural economics textbooks regarding the interrelations between futures and spot markets for agricultural commodities is that futures markets allow for price discovery by market participants, smoother allocation of commodities over time, and the transfer of risk from hedgers to speculators. The distribution of products through time, price discovery, and risk transfer are believed to alleviate some of the erratic price movements, or volatility, that are common in commodity markets; hence, futures markets have stabilizing effects on spot market prices for storable commodities (e.g., Tomek and Kaiser, 2014; Ferris, 2005). Comprehensive literature reviews regarding empirical studies to date are provided in, for example, Irwin, Sanders, and Merrin (2009) or, more recently, in Dimpfl, Flad, and Jung (2017). Empirical studies themselves, however, provide much less conclusive and decisive evidence for price stabilizing or destabilizing effects.

These inconsistencies in findings could be nicely illustrated by comparing Brorsen et al. (1989) and Weaver and Banerjee (1990): Brorsen et al. found that live cattle futures increased the volatility in the cash market while Weaver and Banerjee, considering the same time period, found that live cattle futures did not affect the cash market volatility. Most recently, Goetz, Miljkovic, and Barabanov (2021) found destabilizing impacts of futures markets on corn spot prices and stabilizing impacts on oil spot prices in the United States. Their theoretical model predicted that when production (supply side) is the dominant disturbance, the spot price is destabilized in the short run by futures markets but may or may not be stabilized in the long run. Agricultural commodity markets, including corn markets, are subject to various production disturbances such as weather events (e.g., drought, flood, hail) or pest infestations (Tomek and Kaiser, 2014). Moreover, legislation on ethanol subsidies in recent decades further stimulated corn production within and outside the Corn Belt, adding to the list of supply (and demand) side disturbances on corn prices (e.g., McPhail and Babcock, 2012; Miljkovic, Ripplinger, and Shaik, 2016). Their empirical results indicate a large impact from futures markets on spot price volatility of corn in both the short and long run, which is consistent with the theoretical model. A companion paper (Miljkovic and Goetz, 2020a) analyzing the North American hard red spring wheat market and prices came to similar conclusions. In the national oil markets, demand (consumption) side disturbances were dominant during the period considered, hence a small and stabilizing impact of futures prices on spot oil prices in the United States. This finding is reinforced in the companion paper (Miljkovic and Goetz, 2020b) that considered US regional oil markets. Hence, their empirical results are consistent with their model predictions. In terms of sophistication, previous studies move from those using simple Granger causality (Irwin, Sanders, and Merrin, 2009) to Hasbrouck’s (1995) more complex information share methodology, used by Dimpfl, Flad, and Jung (2017), or causal analysis using directed acyclic graphs theory, as in Miljkovic and Goetz (2020a,b).

Unsurprisingly, this lack of consensus in both the theoretical and empirical literature only furthered one of the recurring arguments made against futures markets that, by encouraging or facilitating speculation, they give rise to price instability. This argument, in various versions, has been made throughout many past congressional hearings going back to the 1960s and 1970s and as recently as 2009 (Commodity Futures Trading Commission, 2009). Thus, there is a duality: The mainstream agricultural economics narrative, as recorded in textbooks, emphasizes the price-stabilizing role of futures markets, while the popular belief of different interest groups points to futures markets’ destabilizing impact, a belief that is partially supported by theoretical and some empirical research.

Price stability matters because that price stability versus volatility has different implications for the welfare of different groups (i.e., producers, consumers, and taxpayers) and social welfare overall. Hence, commodity price stabilization has been and continues to be a subject of keen interest to policy makers, where the role of stockholding is the key to the discussion in providing stability (e.g., Oi, 1961; Samuelson, 1972; Newbery and Stiglitz, 1981; Schmitz, 2018a,b). Note that most of these studies focused on price stabilization policies and their impacts, while ignoring the role of price risk management institutions such as futures markets. The general conclusion within the context of welfare economics is that price stabilization brought about through stockholding activities leads to a net welfare improvement to society (Massell, 1969), even though there are gainers and losers from price-stabilization policies (e.g., Waugh, 1944; Oi, 1961; Williams and Wright, 2005). Specifically, from Samuelson (1972) on, we do know that price stabilization benefits consumers, while price instability benefits producers (e.g., Schmitz, 2018b).

The recent Russian invasion of Ukraine provides an opportunity to observe the interaction of cash and futures markets in near real-time for a variety of key agricultural commodities. An event study that traces the responses of cash and futures markets may provide additional contextual insights which can guide future theoretical and empirical analysis. This example focuses on spring wheat, corn, and soybean cash market price responses at selected locations in North Dakota. Similar observations can be made for other locations in other states.

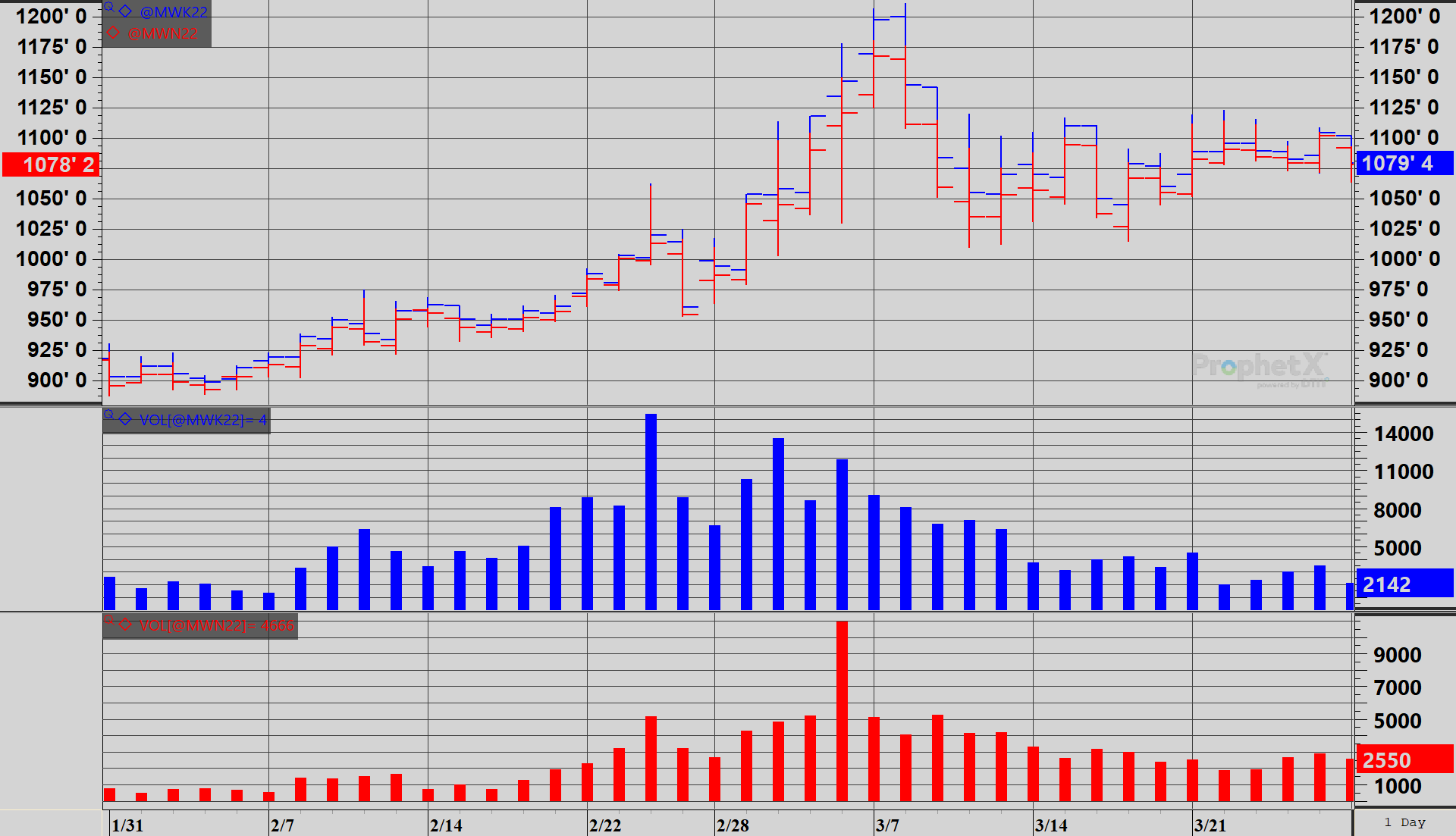

Notes: May futures contract prices and trading volumes are

blue. July futures contract prices and trading volumes are red.

Source: DTN ProphetX.

At approximately 9:00 pm Central Standard Time on February 23, 2022, Russian President Vladimir Putin announced a special military operation and launched a coordinated military attack on Ukraine. While the Russian military buildup along Ukraine’s eastern and southern borders had been escalating since October 2021, the invasion surprised the global grain markets. The U.S. corn, wheat, soybean oil and soybean futures markets responded quickly to the invasion news, but the full implications would not be felt for several weeks. Based upon the March USDA World Agricultural Supply and Demand Estimates (WASDE), Russia is the second largest global wheat exporter, behind the European Union, second largest sunflower oil, and fourth largest feed barley exporter. Ukraine is the world’s largest sunflower oil exporter, third largest feed barley and rapeseed oil exporter, and fourth largest corn and wheat exporter.

| 2-15-22 | 2-25-22 | 2-28-22 | 3-1-22 | 3-2-22 | 3-3-22 | 3-4-22 | 3-7-22 | |

| Hard red spring wheat; March delivery | ||||||||

| Futures month | March | May | May | May | May | July | July | July |

| Future price | 9.53 | 9.50 | 9.94 | 10.53 | 10.58 | 10.90 | 11.00 | 11.68 |

| Basis | -0.35 | -0.55 | -0.55 | -0.40 | -0.40 | -0.40 | -0.45 | -0.50 |

| Cash price | 9.18 | 8.95 | 9.39 | 10.13 | 10.18 | 10.50 | 10.55 | 11.18 |

| Corn, March delivery | ||||||||

| Futures month | March | May | May | May | May | July | July | July |

| Futures price | 6.38 | 6.55 | 6.90 | 7.25 | 7.25 | 7.47 | 7.21 | 7.27 |

| Basis | -0.15 | -0.25 | -0.20 | -0.20 | -0.20 | -0.45 | -0.15 | -0.15 |

| Cash price | 6.23 | 6.30 | 6.70 | 7.05 | 7.05 | 7.02 | 7.06 | 7.12 |

| Soybean, March delivery | ||||||||

| Futures month | March | May | May | May | May | July | July | July |

| Futures price | 15.51 | 15.84 | 16.36 | 16.90 | 16.63 | 16.67 | 16.33 | 16.34 |

| Basis | -0.55 | -0.65 | -0.65 | -0.65 | -0.65 | -0.75 | -0.55 | -0.55 |

| Cash price | 14.96 | 15.19 | 15.71 | 16.25 | 15.98 | 15.92 | 15.78 | 15.79 |

As the invasion began, the Ukrainian government announced that their Black Sea ports would be closed until further notice and Russia stopped commercial ships leaving the Azov Sea. The shipping disruptions raised concerns about short-term availability for wheat, feed grains, and vegetable oils and opened the potential for declaration of force majeure on existing cash market contracts. By March 3, 2022, news reports of significant wheat tenders or purchases by Bangladesh, China, Algeria, and Turkey had reached the market. Global buyers began to realize that current agricultural exports from Ukraine and Russia would be delayed or cancelled, and future supplies would likely be unavailable for an extended time. Even though the United States might not be the source of the alternative wheat, corn, or soybean oil export sales, United States futures and cash markets responded to the changing global supply chain concerns.

Rising price levels, wider daily trading ranges, higher trading volumes, and increasing price volatility attracted the attention of futures market speculators, including managed hedge funds and index funds. While these fund-based speculators have different trading strategies than more traditional spread traders, their participation in a broad base of commodities added to the fever pitch of trading. On Friday, March 4, 2022, the May Chicago Board of Trade wheat futures contracts opened at the limit up of $0.75/bushel. On Monday, March 7, the May contract once again opened at the limit up of $0.85/bushel. At this point, domestic wheat merchandizers—like local elevators, multinational traders, and wheat millers—were recognizing a separation developing between the near-by May futures contract prices and domestic and international spot market cash prices. A similar disconnect between spot cash and near-by futures was being recognized in corn and soybean cash markets.

News reports and anecdotal stories began to appear that local elevators and multinational traders were not purchasing spot market grain from farm managers because of uncertainty regarding the ability to resell the cash grain at profitable levels and the decreasing effectiveness of hedging in the near-by futures contracts. To compensate for this trend, elevators purchasing in the spot market for wheat, corn, and soybeans began shifting their pricing and hedging activities from May futures market contracts to July contracts (please see Figure 1 and Table 1). This shift in futures market contracts improved the correlation between spot market cash prices and futures market prices, resulting in more effective price risk management from hedging and allowing more time for current cash market purchases to be resold in an inverted market.

The general recommendation for effective hedging is to use the futures market contract that best matches the final cash market transaction. For farm managers, this is when the cash grain will be delivered and sold in the cash market to an elevator or end user. For local elevators or export terminals, this is when cash grain previously purchased is resold and delivered. For end users, this is when the cash grain is purchased and received for further processing or consumption. Some cash market participants will modify this hedging strategy and use the near-by futures contract to price cash transactions that will be delivered or used several months in the future. These hedgers, typically grain sellers and merchandizers, are attempting to capture a “carry” in the market and realize a gain from rolling their hedges into a forward contract when the nearby contract is close to expiration. A carry in the market results when futures market prices in the distant contract months are higher than the nearby contract. This provides an incentive to store grain and deliver or use the grain in the future. A futures market carry also incentivizes buyers, like processors or end users, to purchase now rather than wait. However, when Russia invaded Ukraine, the futures market for corn, soybeans, and wheat went from a carry, or slight inverse, to a strong inverse. In an inverted market, the nearby futures prices are higher than deferred contracts, resulting in a disincentive to store grain or sell later. An inverted market signals that there is more buying interest today than there will be in the future.

The primary functions of agricultural commodity futures markets are price discovery for a commodity into the future and risk transfer between hedgers and speculators. The futures markets trade predefined contracts in which price is the only contract term that is negotiable. Product quantity, quality, premiums and discounts, time of delivery, and delivery location are fixed in the contract and nonnegotiable. Futures markets help producers and consumers allocate storable agricultural commodities over time. In contrast, all of the contract trading terms for cash market transactions for agricultural products are negotiable.

Basis is the price difference between the cash market price at a specific location with a specific delivery period and the corresponding futures market contract. Basis levels can vary significantly across time and location but are typically less variable than the price of the underlying commodity. Hedging becomes more effective as a risk management tool when cash and futures market prices are highly correlated, or basis levels are stable. This does not mean that cash market participants will not hedge if price correlations weaken, but trading volumes in the cash market may slow and risk premiums (margins) for merchandizers will increase.

Economic theory tends to focus on current spot market transactions. However, actual trading of agricultural commodities is a blend of spot market and contract-based transactions. Empirical analysis that evaluates the stabilizing or destabilizing effects of futures markets on cash markets follows theory and focuses on spot market prices, using near-by futures and spot market cash market bids. These studies also tend to use weekly, monthly, or quarterly average prices. Unfortunately, every time an average is used, some of the variability is removed. Using average prices may hide some of the stabilizing or destabilizing effects of utilizing futures markets.

The planning horizon for most cash market participants ranges from a few days to several months. In addition, as hedgers in the futures markets, most cash market participants monitor daily futures market price movements. Many speculators monitor and trade price movements that range from less than a second to several hours.

This difference in time perspective among economic theory, empirical analysis, cash market participants, and futures market speculators raises some interesting questions. During times of stable prices, the differences in planning horizons and trading objectives may not be obvious. The interaction of futures markets and cash markets seems to work smoothly. However, during times of extreme uncertainty, like the Russian invasion of Ukraine, differences in planning horizons, trading objectives, and availability of information result in different response times. In other words, the implications of new information on futures market prices, where planning horizons can be short and there is high liquidity of standardized contracts, can be different than cash market prices, where planning horizons are longer, liquidity is lower, and contracts are fully negotiated. These differences can lead to lower price correlations between cash and futures market prices.

Agricultural commodity markets continue to evolve and become more complex. The integration of U.S. agricultural products into the global economy—combined with competing uses for food, feed, fiber, and fuel—have increased the number, frequency, and impact of exogenous shocks to agricultural commodity markets. Traditional theoretical models suggest that price stabilization attained through stockholding activities leads to a net welfare improvement to society, but there are gainers and losers from price stabilization policies. Moreover, the effectiveness and cost of alternative price stabilizing systems—like domestic and international policies, inventory management practices, and supply chain coordination—have not been fully explored. To ensure more credible and testable theory, more complex theoretical models reflecting new realities in commodity trading, including relevant technological developments (e.g., algorithmic trading or order filling algorithms), institutional factors (e.g., impacts of USDA or other scheduled reports), and changed philosophy of farm policy relevant to commodity markets are needed. Extreme price shocks can lead to irreversible negative welfare shocks when existing coping mechanisms are diminished or fail (Tröster, 2018). In combination, this can set in motion a downward spiral of rising vulnerability, with fragile systems and actors (e.g., farmers in food systems) most affected. Therefore, policies to cope with commodity price volatility, such as direct price controls or mitigation of consequences, can have critical stabilizing functions supporting farmers’ welfare and regional (rural) development (Goetz, Miljkovic, and Barabanov, 2021).

Empirical analysis of the role futures markets play in cash market price stabilization or destabilization is also not definitive. Access to quality cash market datasets and accurate inventory levels is always a challenge, but private data sources for cash market price bids are becoming more accessible. A focus on not only spot market but also on forward pricing opportunities in both cash and futures markets may provide additional insights regarding the ability of cash market participants to manage price risk and adjust to changing conditions in an efficient way. And finally, combining modern empirical analysis with event studies of extreme market shocks may provide a more robust analysis of how market participants, both producers and consumers, adjust to price instability.

Brorsen, B.W., C.M. Oellermann, and P.L. Farris, P. L. 1989. “The Live Cattle Futures Market and Daily Cash Price Movements.” Journal of Futures Markets 9(4): 273–282.

Commodity Futures Trading Commission. 2009. Energy Position Limits and Hedge Exemptions, Alexandria, VA: CFTC. Available online: https://www.cftc.gov/sites/default/files/idc/groups/public/@newsroom/documents/file/transcript072909.pdf

Deaton, A., and G. and Laroque. 1996. “Competitive Storage and Commodity Price Dynamics.” Journal of Political Economy 104(5): 896–923.

Dimpfl, T., M. Flad, and R.C. Jung. 2017. “Price Discovery in Agricultural Commodity Markets in the Presence of Futures Speculation.” Journal of Commodity Markets 5(1): 50–62.

Ferris, J.N. 2005. Agricultural Prices and Commodity Market Analysis. East Lansing, MI: Michigan State University Press.

Goetz, C., D. Miljkovic, and N. Barabanov. 2021. “New Empirical Evidence in Support of the Theory of Price Volatility of Storable Commodities under Rational Expectations in Spot and Futures Markets.” Energy Economics 100: 105375.

Hasbrouck, J. 1995. “One Security, Many Markets: Determining the Contributions to Price Discovery.” Journal of Finance 50(4): 1175–1199.

Irwin, S.H., D.R. Sanders, and R.P. Merrin. 2009. “Devil or Angel? the Role of Speculation in the Recent Commodity Price Boom (and Bust).” Journal of Agricultural and Applied Economics 41(2): 377–391.

Kawai, M. 1983. “Price Volatility of Storable Commodities under Rational Expectations in Spot and Futures Markets.” International Economic Review 24(2): 435–459.

Massell, B.F. 1969. “Price Stabilization and Welfare.” Quarterly Journal of Economics 83(2): 284–298.

McPhail, L.L., and B.A. Babcock. 2012. “Impact of US Biofuel Policy on US Corn and Gasoline Price Variability.” Energy 37(1): 505–513.

Miljkovic, D., and C. Goetz. 2020a. “Destabilizing Role of Futures Markets on North American Hard Red Spring Wheat Spot Prices.” Agricultural Economics 51(6): 887–897.

———. 2020b. “The Effects of Futures Markets on Oil Spot Price Volatility in Regional US Markets.” Applied Energy 273: 115288.

Miljkovic, D., D. Ripplinger, and S. Shaik. 2016. “Impact of Biofuel Policies on the Use of Land and Energy in US Agriculture.” Journal of Policy Modeling 38(6): 1089–1098.

Newbery, D.M. 1987. “When Do Futures Destabilize Spot Prices?” International Economic Review 28(2): 291–297.

Newbery, D.M., and J. Stiglitz. 1981. The Theory of Commodity Price Stabilization. New York, Clarendon.

Oi, W.Y. 1961. “The Desirability of Price Instability under Perfect Competition.” Econometrica 29(1): 58–64.

Samuelson, P.A. 1972. “The Consumer Does Benefit from Feasible Price Stability.” Quarterly Journal of Economics 86(3): 476–493.

Schmitz, A. 2018a. “Commodity Price Stabilization under Unattainable Stocks.” Theoretical Economics Letters 8(5): 861–865.

Schmitz, A. 2018b. “Producers’ Preference for Price Instability?” Theoretical Economics Letters 8(10): 1746.

Telser, L.G., and H.N. Higinbotham. 1977. “Organized Futures Markets: Costs and Benefits.” Journal of Political Economy 85(5): 969–1000.

Tirole, J. 1985. “Asset Bubbles and Overlapping Generations.” Econometrica 53(6): 1499–1528.

Tomek, W.G., and H.M. Kaiser. 2014. Agricultural Product Prices. Ithaca, NY: Cornell University Press.

Tröster, B. 2018. Commodity Price Stabilization: The Need for a Policy Mix that Breaks the Vicious Cycle of Commodity Dependence and Price Volatility. ÖFSE Policy Note No. 20/2018, Austrian Foundation for Development Research (ÖFSE), Vienna, Austria.

Turnovsky, S.J., and R.B. Campbell. 1985. “The Stabilizing and Welfare Properties of Futures Markets: A Simulation Approach.” International Economic Review 26(2): 277–303.

Waugh, F.V. 1944. “Does the Consumer Benefit from Price Instability?” Quarterly Journal of Economics 58(4): 602–614.

Weaver, R.D., and A. Banerjee. 1990. “Does Futures Trading Destabilize Cash Prices? Evidence for US Live Beef Cattle.” Journal of Futures Markets 10(1): 41.

Williams, J.C., and B.D. Wright. 2005. Storage and Commodity Markets. Cambridge, UK: Cambridge University Press.

Wright, B.D. 2011. “The Economics of Grain Price Volatility.” Applied Economic Perspectives and Policy 33(1): 32–58.