The problem of poor profits in American agriculture is not new or a secret, but it is not well known to most Americans, including most policy makers, even though the problem threatens an entire sector of our national economy. As such, the problem should be understood by policy makers at all levels of American government. Yet after more than 80 years of government policy interventions in agriculture, the problem remains: Farm income for 2018 is forecast to fall to its lowest real-dollar level in nearly two decades (USDA, 20018c). This failure indicates there must be a fundamental flaw in policy makers’ understanding of the profit problem. Therefore, this article i) presents a summary of research findings that outlines the problem and ii) offers guidelines to policy makers and agricultural industry participants who, as a team, may hold the only workable solutions to this old problem.

The agricultural profit problem has been around for a long time, and this is not the first time it has been the focus of serious warnings and calls for action. In 1933, newly elected President Franklin D. Roosevelt was well aware of the huge economic impact it was having on the country, as summarized by Egan (2006, p. 133): “America had produced more food than any country in history, and farmers were being run off the land, penniless, while the cities couldn’t feed themselves. The average farmer was earning three hundred dollars a year—an 80 percent drop in income from a decade earlier.” Now, 85 years later, the problem is generally much the same: The dismal economics of commodity markets punish, rather than reward, American agricultural producers for being so good at their jobs. However, the specifics of the problem have changed over the past five decades.

My own research into the profit problem was spurred by the agricultural industry and its questions: “What is happening?” and “Why?” As an agricultural economist, I sought to identify economic trends that could shed some light on the nature of the problem and its potential solution. My two most significant efforts to address agriculture’s two questions took the form of books, aimed at a different audiences, but with the same goal: to raise the level of awareness and discussion of the economic factors and trends creating the profit problem so that the problem might be resolved. In 1998, The End of Agriculture in the American Portfolio was published. It was a “call to action” aimed at a general audience of Americans who cared about agriculture. I believed that was the audience who was most likely to find workable solutions to the problem.

However, my research on the economic factors underlying the problem convinced me that the complexity of the issues involved would require a team effort, including agricultural economists and government policy makers in support of the agricultural industry. Thus, in 2008, The Economics of American Agriculture: Evolution and Global Development was published, with those groups as its audience. It reported much of the empirical data that described the economic trends to partially answer the question “What is happening?” It also summarized much historical research—as well as my own recently published work—on the economic factors that explain “Why?”

A summary of some key results in those books follows:

In the remainder of this article, I outline how the specifics of the profit problem have changed over the past five decades, present some updated empirical data that show that the key economic trends reported in Blank (2008) have continued and still support the results summarized above (despite another decade of market shocks), then suggest alternative themes for future government policies. Along the way, I offer some simple new analysis and comments on how my suggested policy theme is aimed more directly at the real problem of agriculture and is therefore more likely to improve the sector’s profit situation over the long term.

As explained in Blank (2008, chapters 6 and 7), since the 1970s the profit problem has been driven by technological innovations that have increased commodity production and competition across what have become global markets:

Profits to U.S. agricultural producers are being squeezed because for an increasing number of commodities, price is global, production cost is local. That means the markets and prices of commodities have become global in scope, while production costs remain local. Thus, profits vary by location. With a single competitive ‘world price’ ceiling affecting producers of a global commodity, it means that local costs determine the profit per unit for producers dispersed across the globe and, therefore, costs determine which producers will survive in the long term. (pp. 121–122)

The profit squeeze leads individual agricultural producers to seek ways to increase their output per acre by adopting more, and more advanced, technology in their commodity production operations. In 1958, Cochrane developed the theory explaining this technological treadmill, which Levins and Cochrane (1996) summarize as follows:

The theory was first introduced as a ‘product price’ treadmill in which farmers constantly strive to improve their incomes by adopting new technologies. ‘Early adopters’ make profits for a short while because of their low unit production costs. As more farmers adopt the technology, however, production goes up, prices go down, and profits are no longer possible even with the lower production costs. Average farmers are nonetheless forced by lower product prices to adopt the technology and lower their production costs if they are to survive at all. The ‘laggard’ farmers who do not adopt new technologies are lost in the price squeeze and leave room for their more successful neighbors to expand. (p. 550)

The treadmill theory clearly links the investment decisions of individual agricultural producers to the profit results they generate. Therefore, American government needs to be more focused on the needs of individuals, rather than on regions, when designing programs intended to improve agriculture’s profit problem. Unfortunately, Weber et al. (2015) found that policy makers still often justify agricultural subsidies by stressing that agriculture is the engine of the rural economy, but those macro-targeted policies are often so general in their design that “cuts to agricultural subsidies are therefore likely to have little effect on the broader rural economy in regions like the Heartland.” (p. 459)

The profit problem does not include just issues of total profit levels, but also of profit variability over time for different groups of agricultural producers. For example, Key, Prager, and Burns (2018, p. 215) found that “the income of commercial farm households is substantially more volatile than that of all U.S. households….” In an assessment of recent government efforts to reduce income risks faced by producers, they also showed that government interventions do not impact all producers equally, noting that the farm income of producers “specializing in program crops (the commodities associated with the bulk of agricultural program payments) saw a significantly greater decline in variability than those not specializing in program crops” (p. 238). In other words, government programs are selective, not general, in their targets, meaning many people in agriculture are left out, forced to seek their own solutions to the profit problem.

In summary, American agriculture’s profit problem derives from its structural problem. The theory underlying the economic field of industrial organization says that an industry’s structure determines its conduct which, in conjunction with its structure, determines that industry’s performance. In agriculture, a high number of firms produce identical outputs (i.e., a commodity), resulting in the price of each commodity being determined by a competitive bidding process involving buyers and sellers, with no seller having any significant influence on the market price. In other words, agricultural producers are “price takers.” Over time, such a “perfectly competitive” market structure pushes prices down to a level at which the average profit of the industry is zero (profits earned by some firms are offset by losses from other firms). Historically, analysts of American agriculture have focused on its performance. However, all this has done is identify trends that illustrate the long-term nature of the problem.

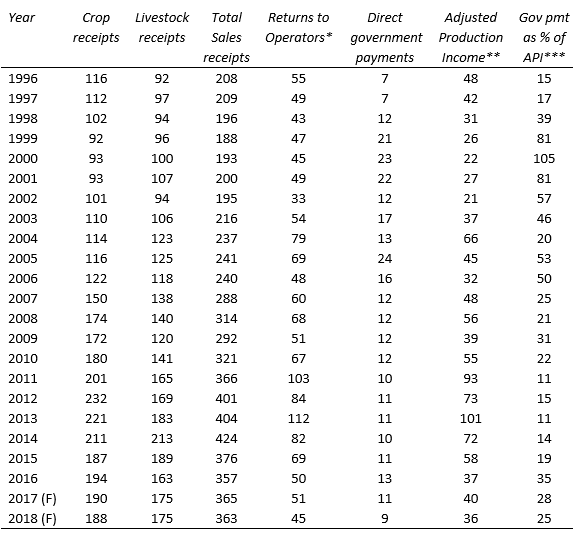

The most recent data available to me when I was doing research for Blank (2008) was for 2003 (see Table 6.1 in the book), which appeared to be the first up-tick after down-trends in both real agricultural sales since the 1970s and income since the 1940s. (Both of the historical down-trends are illustrated in Figure 2.3 of Blank, 2008.) So, have the trends reversed over the last 15 years?

To assess that question, I revisited Table 6.1 of Blank (2008), as shown in Table 1 of this article. Even without adjusting the data into “real” terms, it is easy to answer the question: No. Although nominal sales receipts started increasing in 2003 and continued with just a couple exceptions through 2014, they fell over the last four years, 2015–2018. Arguably, that pattern reflects volatility but not a reversal of the long-term trend. However, the more important trend is the one in income. The nominal totals for income are shown in Table 1 in the column labeled “Returns to Operators.” In that data, it is easy to see the high level of volatility over the 2003–2018 period and that, clearly, the long-term down-trend did not reverse; the nominal totals for returns in years 2016–2018 are each lower than the total was in 2003… and 1996! A second argument against the point that profitability may have improved over the last 15 years is the fact that the average gross profit margin (approximated by dividing total operator returns by total sales receipts) was 25% in 2003 and is forecast to be about half that (12%) in 2018. But returns to operators include direct government payments to owners of farms and ranches, thus inflating the profit margin. Therefore, I removed government payments from returns—just as I did in Blank (2008)—to get “Adjusted Production Income” (API) to better reflect owners’ gains from production operations. By inspecting the data in the API column of Table 1, it is even clearer that the long-term down-trend in agricultural income has not reversed. The nominal (i.e., unadjusted for inflation) API expected for 2018 is about the same as that reported for 2003 and below the total for 1996.

What would the income picture be if the data were adjusted into real terms? For the current year, the USDA (2018c) reports that “in inflation-adjusted (real) 2018 dollars, net farm income is forecast to decline… [I]f realized, this would be the lowest real-dollar level since 2002.” Therefore, the income down-trend has not reversed, even after a volatile period of higher prices that improved the picture for several years.

Turning to the role of direct government payments in determining returns to operators, there appears to be a relationship that implies the government’s effective policy goal. Government payments are generally higher during the early decade reported in Table 1—when returns to operators were generally lower—and the reverse during the later decade shown in the table. For example, the highest amount of payments occurred in 2000 (when payments represented over half of returns that year), whereas during 2013, the year that returns were the highest, government payments represented only about 10% of returns to operators. This seems to indicate that the government is trying to respond to commodity market conditions. If true, that would create a negative correlation between the data on returns to operators and government payments. In fact, the correlation coefficient for those data is −0.23. However, a more precise reflection of the importance of government payments to operators is generated by focusing on API, rather than on returns to operators, and by expressing payments as a percentage of API, as I have done in the far right column of Table 1. The correlation between returns to operators and government payments as a percentage of API is −0.57. This much stronger relationship is consistent with the hypothesis that the goal of government policies is to provide an income base (i.e., a “minimum wage”) for agricultural operators. However, the relatively low degree of correlation implies that the government is not very good at it, most likely because current programs are aimed at only a few “program commodities.”

Has anything changed since my books appeared? Government policies have increased their focus on risk management (through use of crop insurance), but those efforts have still been limited in their coverage to a subset of crops: Not all crops are covered by crop insurance. In other words, low-value grain crops grown in the Midwest still get lots of attention—and money—while producers in other regions and markets get little help. Hence, it is not surprising that long-term income trends have not really changed over the past two decades. So, have changes in government policies changed any of the non-income trends in American agriculture?

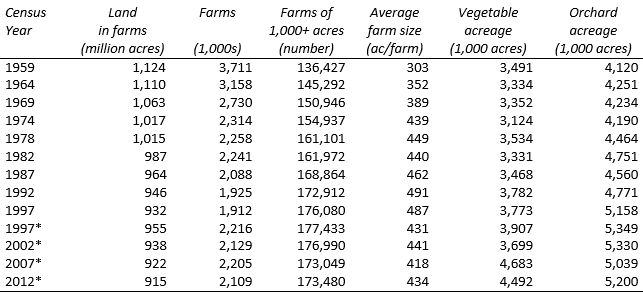

Table 2 shows that structural trends remain the same, indicating that there has been no change in agricultural producers’ expectations: Farmland and farms continue to leave agriculture and producers are still looking for tools other than the government’s risk programs to improve their profit problem. However, the data in Table 2 may reveal some early signs of change in the pace of decline in American agriculture. For example, the growth in numbers of very large farms (1,000+ acres) has slowed, if not stabilized, over the last two decades, and the shift of acreage into high-value, high-risk vegetable and orchard crops also seems to have slowed. Of course, these changes may be results from many factors, but they clearly have implications for agricultural policy.

A theme for government policy was created during the Great Depression in response to the Midwest’s Dust Bowl period of drought that brought economic collapse to a large section of the High Plains. The policy theme was part of the report of the Great Plains Drought Area Committee delivered to President Roosevelt on August 27, 1936. The report concluded that “the situation is so serious that the Nation, for its own sake, cannot afford to allow the farmer to fail.… We endanger our democracy if we allow the Great Plains, or any other section of the country, to become an economic desert” (reported in Egan, 2006, p. 269). In other words, the recommended theme was to have policies that focused on the economic viability of agricultural operators across the country.

In 2006, Egan summarized how the theme of government farm policies had changed since the Dust Bowl. He observed (p. 310)

The government props up the heartland, ensuring that the most politically connected farms will remain profitable. But huge sections of mid-America no longer function as working, living communities. The subsidy system that was started in the New Deal to help people… stay on the land has become something entirely different: a payoff to corporate farms growing crops that are already in oversupply, pushing small operators out of business.

The message got muddled over time, most likely due to politics. Originally, government programs in agriculture were general, trying to help everyone in the industry (i.e., provide a “safety net”), but now they are specific to a limited number of commodities, making them a poor investment for the country. For example, we now use U.S. tax dollars to subsidize corn and wheat production, a large part of which is exported and consumed by people in other countries.

America needs to invest in regions and commodity markets that have a better, competitive-market-derived return and to let an unconstrained market deal with the Midwest. Of course, this would require much more restraint on the part of policy makers than is likely to materialize; without government subsidies to grain and some other agricultural commodities, prices would fall, and that reduction in expected revenue per acre would reduce farmland values if alternative crops or land uses were not available. With 83.5% of farm sector assets held in farmland in 2018 (USDA, 2018a), such a policy shift would amount to a government-induced reduction to the economic security net of agricultural producers of subsidized commodities. No politician wants to be a part of that. Thus, it appears program commodities are now “too big to fail.” But is it fair (or good policy) to reward industries for being a bad investment? Government policy effects artificially inflated farmland prices in areas dominated by the production of program crops, so shouldn’t the government fix that problem?

The profit problem could be improved by adjusting the current policy theme, but it could be solved by adopting a possible new policy theme that may be better received by the agricultural industry itself. In the current policy theme, an improvement might be possible by dropping the commodity focus of programs. The goal could be to provide a real minimum wage and/or economic security net to all agricultural producers, not just a subset, by dropping all links to what commodity is produced when determining eligibility for assistance. Instead, the focus could be on the amount of money invested per acre in production operations, with program eligibility and benefits both determined by some threshold amount. Such a goal would be consistent with the policy theme from the Great Depression.

A second, and new, policy theme could be to help agricultural producers become integrated firms that can influence their own profit margins. The profit problem exists for operators that are producers of only commodities, so a new policy approach could facilitate producers’ shift to being integrated firms with outputs that include branded and/or value-added products. Such a policy shift would attack the economic basis of the profit problem itself rather than trying to manage markets. The goal would be to change agriculture’s industry structure by giving industry participants the tools to make the change themselves. The resulting long-term shift in industry structure, from being “perfectly competitive” to a “monopolistic competition” form, leads to more agricultural firms that can use their value-adding skills to improve their profit margins. That type of firm has a market advantage coming from American technological advantages and, therefore, will be a leading competitor profiting in global markets.

Since over 80 years of government programs have not been able to solve the profit performance problem, it is time to focus policies on agriculture’s structure. However, the people employed in agriculture know their industries best, thus, they should be engaged with government in any discussions of how to solve the profit problem. Programs that get more buy-in are more likely to succeed than programs focusing on buy-outs.

Blank, S.C. 1998. The End of Agriculture in the American Portfolio. Westport, CT: Quorum.

———. 2008. The Economics of American Agriculture: Evolution and Global Development. Armonk, NY: M.E. Sharpe.

Cochrane, W.W. 1958. Farm Prices: Myth and Reality. St. Paul, MN: University of Minnesota.

Egan, T. 2006. The Worst Hard Time: The Untold Story of Those Who Survived the Great American Dust Bowl. Boston, MA: Houghton Mifflin.

Key, N., D. Prager, and C. Burns. 2018. “The Income Volatility of U.S. Commercial Farm Households.” Applied Economic Perspectives and Policy 40(2):215–239.

Levins, R., and W. Cochrane. 1996. “The Treadmill Revisited.” Land Economics 72(4):550–553.

U.S. Department of Agriculture. 2014. 2012 Census of Agriculture. Washington, DC: U.S. Department of Agriculture, National Agricultural Statistics Service AC-12-A-51, May.

U.S. Department of Agriculture. 2018a. Assets, Debts, and Wealth. Washington, DC: U.S. Department of Agriculture, Economic Research Service. Available online: https://www.ers.usda.gov/topics/farm-economy/farm-sector-income-finances/assets-debt-and-wealth/

———. 2018b. Returns to Operators, U.S. and State. Washington, DC: U.S. Department of Agriculture, Economic Research Service. Available online: https://data.ers.usda.gov/reports.aspx?ID=17837

———. 2018c. 2018 Farm Sector Income Forecast, U.S. and State. Washington, DC: U.S. Department of Agriculture, Economic Research Service. Available online: https://www.ers.usda.gov/topics/farm-economy/farm-sector-income-finances/farm-sector-income-forecast/

Weber, J., C. Wall, J. Brown, and T. Hertz. 2015. “Crop Prices, Agricultural Revenues, and the Rural Economy.” Applied Economic Perspectives and Policy 37(3):459–476.