Source: Statista. Available online: https://www.statista.com/stati

stics/379112/e-commerce-share-of-retail-sales-in-us/ and

https://www.statista.com/statistics/534123/e-commerce-share-o

f-retail-sales-worldwide/

Source: USDA-ERS Food Expenditure Series (Monthly sales of

food, with taxes and tips, for all purchasers); Available online:

https://www.ers.usda.gov/data-products/food-expenditure-serie

s/food-expenditure-series/#Archived%20Food%20Expenditure%

20Tables

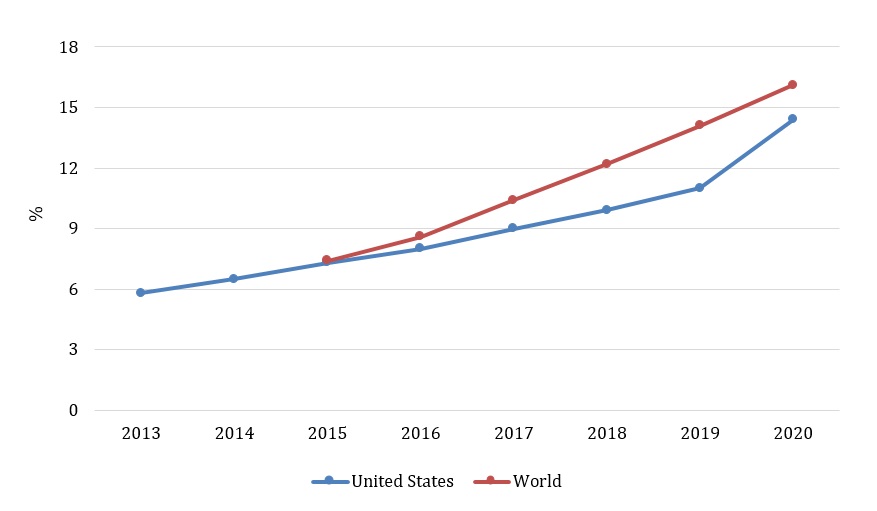

The U.S. e-commerce sector has expanded steadily since the beginning of the twenty-first century. In 2020, this sector accounted for 14.4% of total retail sales, nearing the global average of 16.1% and representing a 30.9% increase over 2019 (Figure 1). A significant component underpinning this momentum is the growth of online food retailers and ordering services. The COVID-19 pandemic wreaked an unprecedented havoc in the agriculture and food sector and highlighted vulnerabilities along the supply chain. Pervasive, disruptive changes resulted in supply shortages, panic buying and stockpiling behaviors among consumers, increased food price volatility, and widespread restaurant closures (Chenarides et al., 2021; Cosgrove, Vizcaino, and Wharton, 2021). Meanwhile, this global crisis has also resulted in lingering consumer fear over safety in public spaces (including grocery stores and restaurants) and growing preferences for convenience and time saving due to work-life schedule changes (Chenarides et al., 2021; Grashuis, Skevas, and Segovia, 2020; Kelso, 2020; Stuckey, 2020; Mercatus and Incisiv, 2020). These factors, in turn, have significantly magnified and accelerated the expansion of e-commerce in the food sector, changing consumers’ food acquisition patterns.

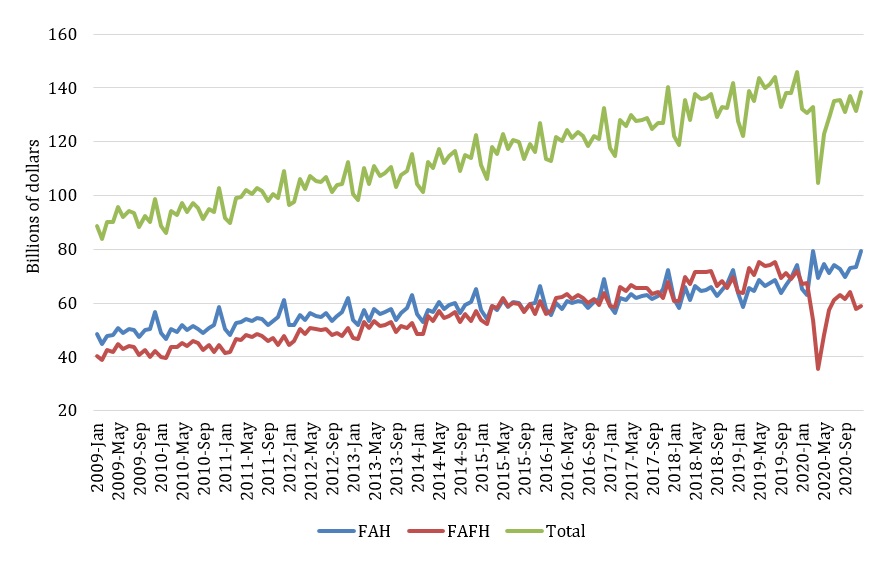

Food consumption usually includes two components: (1) food-at-home (FAH) consumption, targeting food purchased from a grocery store, convenience store, or supercenter for use in home production, and (2) food-away-from-home (FAFH) consumption, focusing on food bought from a food service provider, such as a full- or limited-service restaurant, for on- and off-premise consumption. (Davis, 2014; Elitzak and Okrent, 2018). After years of growth in FAFH expenditures, FAH regained the majority share of expenditures in 2020 (Figure 2). FAFH consumption plummeted at the onset of the COVID-19 pandemic due to sudden disruptions such as mandated social-distancing measures and massive restaurant closures. Consequently, consumers shifted to preparing more meals at home, driving an 8.5% increase in total FAH expenditures compared to 2019. Although restaurants began to reopen after May 2020 and prior patterns began to return gradually, FAFH expenditures remained lower than FAH expenditures through the end of the year. The COVID-19 crisis not only changed FAH and FAFH patterns dramatically but also transformed consumers’ food acquisition patterns, with e-commerce approaches dominating. As a result of concern over contracting coronavirus, as well as limitations on entry into physical stores, many people sought online alternatives to physical visits to grocery stores and dining inside brick-and-mortar restaurants. While previous research has focused on consumers’ online grocery shopping behaviors, little is known about how e-commerce has evolved in both FAH and FAFH markets since the pandemic. By focusing on two innovative e-commerce-based food acquisition methods in both the FAH and FAFH markets (featuring grocery stores and restaurants, respectively), this article seeks to (1) understand how digitalization evolutions reshape the food retailing and food service landscape, (2) analyze opportunities and challenges of online food acquisition in the post-pandemic era, and (3) suggest directions for future research.

U.S. e-commerce shares in total grocery sales rose to 10.2% in 2020—a 200% increase relative over 2019—further accelerating a long-term trend of growth (Statista, 2021a). Consumer data show that many consumers tried online grocery shopping for the first time and those who were already regular users tended to rely on it more (Food Marketing Institute, 2019, 2020). Behind these changes are two major factors. The primary factor is coronavirus-related safety concerns. Data show that a high level of coronavirus concern among consumers contributed to approximately 50% more usage of online grocery shopping channels, compared to a low level of concern (Statista, 2021a). The other factor is new work-from-home lifestyles, which led consumers to seek convenient and time-saving ways of managing household chores (Mercatus and Incisiv, 2020; Kats, 2020).

In addition to growing market penetration, diversified omnichannel services also characterize the e-commerce boom in the food retailing sector (Statista, 2021a), leading to two major models. The fastest-growing model is third-party vendors (such as Instacart and Shipt) that employ shoppers to handpick groceries at the store of choice for customers and offer same- or next-day home delivery. Instacart’s growth, for example, has been fueled by the pandemic, leading it to become the third-largest online grocery shopping venue after Walmart and Amazon (Statista, 2021a). Moreover, the growing customer base allowed these third-party vendors to diversify existing delivery services by teaming up with nonfood local merchandisers, such as apparel and cosmetic stores, generating new revenue sources and further enlarging the customer base.

The second model is free curbside or in-store pickup or delivery services with extra fees/charges supported by individual brick-and-mortar grocery stores. The largest player using this model is Walmart, which has been offering online ordering and free pickup services for several years. It made same-day home-delivery service extensively available in 2019 and upgraded the service to a two-hour time window through the Express Delivery program in 2020 (McGrath, 2020).

Another model of online grocery shopping that has grown in recent years and accelerated by the pandemic involves “ghost” grocery stores, also called dark or virtual grocery stores, that exclusively fulfill online orders from a warehouse or fulfillment/distribution center rather than a brick-and-mortar store. While these ghost grocery stores all lack in-person shopping experiences, they differ in product range. Some ghost grocery stores, such as Thrive Market and Boxed, only supply shelf-stable goods. Others—order-based Fresh Direct, subscription-based Misfits Market, and AI technology-based Farmstead—are either virtual versions of full-service brick-and-mortar grocery stores or smaller stores specializing in perishables such as fresh produce or meats. Responding to increased demand for online grocery shopping during the pandemic, some independent grocers (such as Amazon, Kroger, and Giant Eagle) closed existing grocery stores and converted them into ghost grocery stores that exclusively fulfill online orders with pickup or delivery services (Thakker, 2020; Wells, 2020a,b).

Benefits of ghost grocery stores include reduced costs associated with operating a brick-and-mortar store, increased flexibility and capacity to fulfill online orders from remote consumers, enhanced safety measures for employees and the community amid the pandemic, unique convenience of allowing consumers to repeat a previous order with a simple click, and extended market opportunities to local farmers and food producers. However, challenges also exist in each of the three models. First, although the rise of on-demand third-party grocery delivery vendors offers flexible earning opportunities to those who have lost full-time jobs due to the pandemic, labor-related conflicts are occurring. For instance, Instacart associates and shoppers walked out for greater pay, access to paid leave, and more disinfectant supplies (Scheiber and Conger, 2020). Second, for brick-and-mortar grocers with delivery services, the optimal strategy between managing an in-house delivery team and contracting with third-party delivery company is unclear, especially when the pandemic-driven demand for delivery in general has made driver recruitment and retention more challenging. Third, besides the added complexity of reassigning employee roles and additional costs of setting up online assortment systems, converting an existing grocery store to a ghost store is not a one-size-fits-all solution. Both feasibility and profitability hinge on a comprehensive evaluation of the local food environment and e-commerce demand density (Wells, 2020c).

As consumers become accustomed to and more confident in online grocery shopping, grocery shopping through a mobile app or website rather than in person is expected to become more common (Brewer and Sebby, 2021; Chenarides et al., 2020). However, the extent to which the virtualization of grocery stores will become a long-term trend in the post-pandemic era remains an open question. A key element to consider is consumer technical and economic access to online grocery shopping. For example, additional delivery fees make online grocery shopping less economically accessible to consumers living paycheck to paycheck. The USDA launched a pilot program allowing Supplemental Nutrition Assistance Program (SNAP) participants with Electronic Benefit Transfer (EBT) cards to purchase groceries online. Practically, efforts to help lower-income consumers access online grocery shopping tools also help to improve food environment and access to healthy foods. In addition, policy interventions might be necessary from the perspective of decentralizing the market structure of the food retailing industry. As online grocery shopping continues to grow, while grocery store virtualization opens potential opportunities for smaller local stores, major retailers’ lead in this trend might further consolidate their market power, threatening small local grocers’ resilience. It could also bring dynamic changes to the local food environment, which has been documented to impact consumers’ dietary patterns and even health outcomes (Volpe, Jaenicke, and Chenarides, 2018). Last, when the coronavirus threat dwindles, several questions are worth investigating to better understand how online grocery shopping will continue to emerge and impact consumers’ food consumption patterns:

Note: Forecast data are highlighted with dented outlines.

Source: Statista, based on IMF, World Bank, UN and Eurostat;

https://www.statista.com/outlook/dmo/eservices/online-food-deli

very/worldwide

Source: Statista, based on IMF, World Bank, UN and Eurostat;

https://www.statista.com/outlook/dmo/eservices/online-food-deli

very/worldwide

Source: National Restaurant Association

(https://restaurant.org/research/state) and The Kitchen Door

https://www.thekitchendoor.com/kitchen-rental/states);

aggregated/sorted by authors.

Frost and Sullivan projected that global online food delivery (OFD) will be a $200 billion industry by 2025, almost double the size of 2018 (Singh, 2019). In the prepandemic era, the annual growth of the global OFD industry was less than 20% (Figure 3). When the COVID-19 pandemic set in, disruptive changes in the food sector significantly accelerated the adoption and expansion of OFD and pickup services (Shead, 2020), resulting in an annual growth rate of 27% (Figure 3). Driving forces include, for example, restaurant closures, limited-capacity dine-in restrictions guided by social distancing measures, seeking solutions to home-cooking fatigue, and increased preferences for food diversity. As the second-largest market in the world following China, the U.S. OFD sector is projected to reach a volume of $32 billion by 2024, after adjusting for the COVID-19 impacts (Figure 3).

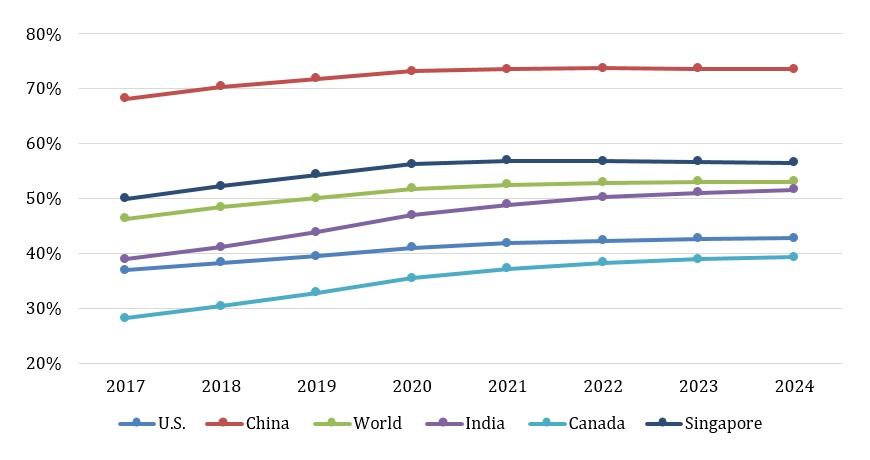

The U.S. OFD sector usually employs two major methods: platform-to-consumer (P2C) and restaurant-to-consumer (R2C) (Statista, 2020a; Niu et al., 2021). P2C is characterized by third-party food delivery platforms and companies such as DoorDash, Grubhub, Uber Eats, and Postmates. R2C is also called self-logistics (Niu et al., 2021), which are independently operated by restaurants through an in-house delivery team, such as pizza delivery restaurants Domino’s and Papa John’s. Statista’s data show that, among leading OFD markets by volume and user penetration worldwide, the market share of the P2C segment has been steadily increasing (Figure 4). In markets with the largest revenue (China) and the highest user penetration rate (Singapore), more than half of OFD sales are generated through third-party delivery platforms.

Before the onset of the pandemic, the three-year average user penetration rate of P2C segment in the U.S was 13.6%, 33% lower than that of the R2C segment (Statista, 2021b). In the wake of the COVID-19 pandemic, P2C user penetration increased to 17.8%, further shrinking the gap with R2C (Statista, 2021b). Recent studies indicate that the P2C segment is expected to be the dominant driver of the OFD sector in the post-COVID era (Annaraud and Berezina, 2020; Niu et al., 2021). This conclusion is supported by explicit signs that third-party food delivery platforms and companies—such as DoorDash, Uber Eats, and Grubhub in the United States and Just Eat and Deliveroo in the United Kingdom—have grown enormously and actively initiated significant acquisitions and mergers (Yeo, 2021). Additional evidence of OFD’s development is the rapid proliferation of ghost kitchens, which grow in tandem with the P2C segment. As P2C delivery platforms provide accessible marketplaces and contracted delivery services for ghost kitchens, the latter contributes to the former’s customer base and revenue sources.

Unlike traditional restaurants, which receive customers in physical storefronts and brick-and-mortar dine-in spaces, ghost kitchens are professional food preparation spaces that are usually operated in shared commercial kitchens optimized for delivery services (Lee, 2020). Note that ghost kitchen operations are characterized by delivery, and the takeout option is rarely offered (Lee, 2020); thus, this paper focuses on delivery-based ghost kitchens. Ghost kitchens go by many names—including virtual, dark, enlightened, cloud, or shared kitchens—depending on the context. Without establishing physical storefronts or dine-in areas, which come with considerable overhead costs and commitments, ghost kitchens provide a much lower entry point for restaurateurs and chefs to test out new business ideas and generate new sales.

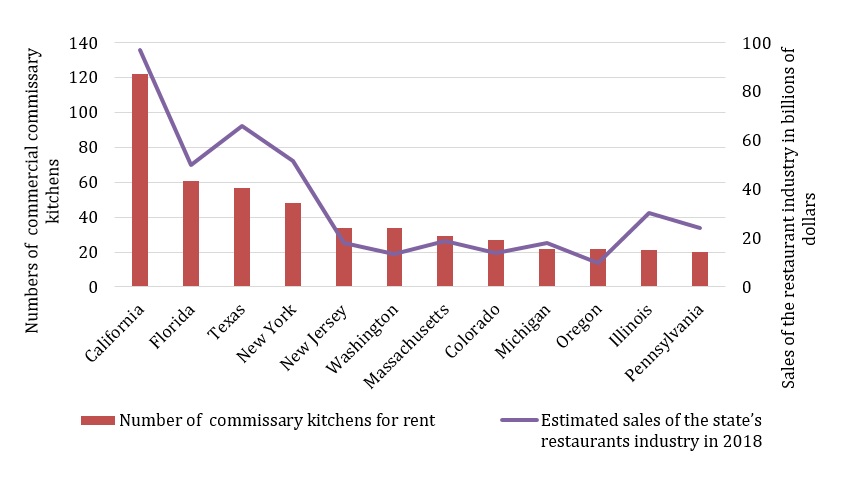

Currently, ghost kitchens generally follow two different models. The most common model is the rent-a-kitchen model, referring to renting a kitchen space at a commercially licensed multikitchen facility and partnering with OFD platforms for ordering and delivery services. The number of these shared-use kitchen facilities—also called “commissary kitchens”, “central kitchens”, “commercial kitchens”, or “rent-a-kitchens”—has grown nationwide in parallel with OFD platforms for the past few years. As of February 2021, there are nearly 800 commissary kitchens in the United States listed The Kitchen Door, a website directory of commercial kitchen spaces available for rent. As illustrated in Figure 5, although the number of commissary kitchens is not perfectly aligned with restaurant industry sales, states with more commissary kitchens and ghost kitchen operations tend to have larger restaurant industries. However, it is worth noting that the commissary kitchen count listed on The Kitchen Door does not perfectly represent the size of the ghost kitchen industry state-by-state for a couple of reasons. First, The Kitchen Door does not provide an exhaustive list of commissary kitchens. It excludes those owned by individual corporations such as DoorDash, CloudKitchens, and Virtual Kitchen Co. Virtual eateries allowing consumers to mix-and-match food items across restaurants located within the same facility and fulfilling the orders in one delivery drop, such as Zuul and Kitchen United, are also excluded. Second, besides renting kitchen spaces in commissary kitchen facilities, ghost kitchen operations have a second model that involves collaborating with existing kitchens.

Due to the reliance of ghost kitchens on third-party food delivery services, P2C giants have ventured into the ghost kitchen market, resulting in a different model: ghost-kitchen-within-a-physical-kitchen (Filloon, 2018, calls this a “virtual-brand-within-an-actual-restaurant”). For example, Uber Eats, the fastest-growing OFD platform in the United States, adopted this approach to collaborate with brick-and-mortar restaurant owners to develop an additional set of menus and brands optimized exclusively for delivery as a second line. Confronted by safety concerns about eating out amid the coronavirus pandemic, several major brands in the restaurant industry also joined the ride of the ghost kitchen revolution by launching a second, virtual brand that operates out of their existing kitchen spaces or partnering with other restaurant operators as host kitchens. Examples of this model include It’s Just Wings (which operates out of its mother kitchen Chili’s within the same company, Brinker International), Wow Bao (which uses its fast-growing partner kitchen program to facilitate delivery-only food), and Famous Dave’s (which uses existing restaurant kitchens within the same company, Granite City, as well as other host kitchens) (Littman, 2021). This type of ghost kitchen is not designed to compete with their “mother kitchens” or “host kitchens” but to complement the in-store business volumes, diversify revenue sources, and save on operational costs. To this end, this model emerges as a cost- and labor-effective strategy in a slim-margin industry.

Before the pandemic, the ghost kitchen trend was driven by two major forces: diminishing margins in the brick-and-mortar restaurant industry (such as rising real estate price and minimum wage) and consumer behavioral shifts leading to digitalization. Major brands’ experiments with storefront-free and delivery-only operations by partnering with commissary kitchens (such as Chick-Fil-A in Nashville and Louisville and Panera in Chicago) have polished the concept of ghost kitchens. A third force that supercharged the ghost kitchens trend is undoubtedly the COVID-19 pandemic. While restaurant closures, government-mandated social distancing measures and in-door dining restrictions, and lurking consumer concerns about coronavirus have challenged the restaurant industry, they have also driven restaurateurs and chefs to seek virtualization opportunities.

Abundant evidence shows that consumer demand for the convenient OFD services has surged in 2020 (Kelso, 2020; Brewer and Sebby, 2021). The ghost kitchen boom fills the influx of online orders, especially in densely populated areas. Not surprisingly, this rapid expansion is largely powered by major brands, which have adequate capital support and operational flexibility to seamlessly generate additional revenue streams through delivery-friendly virtual brands operating out of existing kitchens. Another pivotal component of ghost kitchens’ momentum, however, cannot be overlooked. Through a preliminary interview with a professional chef in New York City who started a ghost kitchen operation amid the pandemic, we learned that a significant number of chefs and line cooks who lost their jobs during the pandemic embarked on testing culinary ideas and business plans through ghost kitchens and OFD platforms (personal communication, March 3, 2021).

As growth in the OFD sector and especially the P2C segment is expected to continue in the near future when online food ordering becomes an ordinary component of consumption habits, ghost kitchens are likely to become a bigger player. The optimism persists that ghost kitchens can become a common e-commerce tool for restaurateurs and chefs to adjust development and growth strategies and thereby reshape the restaurant industry’s landscape in the post-COVID era. To established restaurants, ghost kitchens offer an efficient approach to scale up revenues and introduce off-premises opportunities. To individual chefs, start-ups, and pop-up restaurants, ghost kitchens are a flexible and low-cost solution for sculpting and promoting their business ideas.

However, despite widespread optimism, skepticism about the long-term viability of this approach remains. First, given the concern that ghost kitchens could potentially threaten brick-and-mortar restaurants’ survival and that small businesses already bear hefty regulatory burdens (Jennings, 2020), it is difficult to determine balanced regulations and policies about them. Second, the ghost kitchen model comes with a unique set of challenges, such as heavy dependence on third-party delivery platforms, unavoidably hefty commission fees (usually 15%–30% per transaction), and unpredictable outcomes and limited control over delivery service that could tamper with food quality. Third, even successful ghost kitchens unequivocally face the scale hurdle. As ghost kitchens grow, the pressure to have a physical presence increases. For example, the owner of a successful ghost kitchen brand, It’s Just Wings, has started considering a nonvirtual version within a few months since it was launched as a virtual brand based in Chili’s kitchens (Maze, 2020). Last, potential system-wide spillovers brought by ghost kitchen proliferation, such as paradigm shifts in commercial real estate and strengthened market powers of major brands, need to be addressed.

From a broader perspective, in the post-pandemic era when eating out becomes less of a concern, how consumers allocate FAFH dollars between online ordering (and takeout) and eating out should be further studied. It is unclear whether consumers will rush to return to in-person dining when COVID-related restrictions are lifted and whether any such rush will be permanent or if the introduction to online options will change the landscape of restaurant dining permanently. OFD platforms will need to determine how to compete for market share as the industry matures and becomes saturated, how consumer segments and profiles differ due to COVID-related changes (such as changes of work-life balance and consumer attitudes toward food purchasing), and how conventional restaurateurs will adapt. These questions await updated answers from economic and marketing research.

From a narrower perspective, while restaurateurs have discussed the ghost kitchen concept widely, consumer perspectives about this trend have not yet been studied. In economies with advanced e-commerce penetration, there have been discussions on consumer awareness of where their meals come from and related food safety issues (Sun and Buijs, 2018; Limon, 2021). To better understand the mechanism supporting this growing market and fill the regulatory vacuum, in-depth research focusing on consumer perspectives (such as awareness, attitudes, and satisfaction) and consumption patterns of ghost kitchen operations, as well as market structures and competitiveness, need to be conducted in a timely manner.

E-commerce has infused the food retailing and food service sectors with innovative business ideas and off-premises growth opportunities, and the COVID-19 pandemic only accelerated this momentum. It is worth noting that as consumers become more accustomed to ordering meals from restaurants for at-home consumption, the definitions of FAH and FAFH may become obscured. In future study contexts, one might need to clarify whether online food ordering belongs to the FAFH rather than FAH component for both survey takers and research purposes. Whether FAH and FAFH’s dynamic patterns will return to the pre-COVID time remains uncertain because (1) consumers’ lifestyle and food-related behaviors have changed and (2) in addition to increased convenience and diversity, e-commerce’s impacts on consumers’ ways of acquiring both FAH and FAFH have yet to be evaluated precisely. What’s certain is that with high-quality logistics, the virtualization of grocery stores and restaurants could benefit all walks of consumers, including those who live in remote areas with limited access to fresh produce and those looking for convenient weekday meals, for example. On the other hand, high-quality logistics suppliers are major players as well as winners in the e-commerce evolution. For instance, Uber dabbles in grocery and alcohol delivery markets (Drizly), and Instacart continues to partner with nonfood shopping and delivery.

Annaraud, K., and K. Berezina. 2020. “Predicting Satisfaction and Intentions to Use Online Food Delivery: What Really Makes a Difference?” Journal of Foodservice Business Research 23(4):305-323. https://doi.org/10.1080/15378020.2020.1768039

Brewer, P., and A.G. Sebby. 2021. “The Effect of Online Restaurant Menus on Consumers’ Purchase Intentions during the COVID-19 Pandemic.” International Journal of Hospitality Management 94:102777. https://doi.org/10.1016/j.ijhm.2020.102777

Cosgrove, K., M. Vizcaino, and C. Wharton. 2021. “COVID-19-Related Changes in Perceived Household Food Waste in the United States: A Cross-Sectional Descriptive Study.” International Journal of Environmental Research and Public Health 18(3):1104. https://doi.org/10.3390/ijerph18031104

Chenarides L, C. Grebitus, J.L. Lusk, and I. Printezis. 2021. “Food Consumption Behavior during the COVIDâ€19 Pandemic.” Agribusiness 37:44–81. https://doi.org/10.1002/agr.21679

Davis, G.C. 2014. “Food at Home Production and Consumption: Implications for Nutrition Quality and Policy.” Review of Economics of the Household 12(3):565-588. https://doi.org/10.1007/s11150-013-9210-0

Elitzak, H., and A. Okrent. 2018. “New U.S. Food Expenditure Estimates Find Food-Away-from-Home Spending Is Higher Than Previous Estimates.” Amber Waves. Available online: https://www.ers.usda.gov/amber-waves/2018/november/new-us-food-expenditure-estimates-find-food-away-from-home-spending-is-higher-than-previous-estimates/ [Accessed February 15, 2021].

Filloon, W. 2018, October 24. “Uber Eats’ Path to Delivery Domination: Restaurant Inception.” Eater. Available online: https://www.eater.com/2018/10/24/18018334/uber-eats-virtual-restaurants [Accessed March 4, 2021].

Food Marketing Institute. 2019. U.S. Grocery Shopper Trends 2019 [webinar presentation]. Available online: https://www.fmi.org/docs/default-source/webinars/trends-a-look-at-today's-grocery-shopper-slides-pdf.pdf [Accessed January 10, 2021].

Food Marketing Institute. 2020. U.S. Grocery Shopper Trends: The Impact of COVID-19 [webinar presentation]. Available online: https://www.fmi.org/docs/default-source/webinars/trends-covid-19-webinar.pdf [Accessed January 10, 2021].

Grashuis, J., T. Skevas, and M.S. Segovia. 2020. “Grocery Shopping Preferences during the COVID-19 Pandemic.” Sustainability 12(13):5369. https://doi.org/10.3390/su12135369

Jennings, L. 2020, February 28. “Third-Party Delivery, Ghost Kitchens Face Scrutiny in San Francisco.” Restaurant Hospitality. Available online: https://www.restaurant-hospitality.com/owners/third-party-delivery-ghost-kitchens-face-scrutiny-san-francisco [Accessed March 22, 2021].

Kats, R. 2020, November 17. “Online Grocery Sales Will Increase by Nearly 53% This Year.” Insider Intelligence. Available online: https://www.emarketer.com/content/online-grocery-sales-will-increase-by-nearly-53-this-year [Accessed March 5, 2021].

Kelso, A. 2020, October 5. “How the Pandemic Accelerated the US Ghost Kitchen Market ‘5 Years in 3 Months’.” Restaurant Dive. Available online: https://www.restaurantdive.com/news/how-the-pandemic-accelerated-the-us-ghost-kitchen-market-5-years-in-3-mont/585604/ [Accessed March 4, 2021].

Lee, W.K. 2020, December 11. “Ghost Kitchens: Reasons to Adopt This Type of Food Delivery Model.” Forbes. Available online: https://www.forbes.com/sites/forbesbusinesscouncil/2020/12/11/ghost-kitchens-reasons-to-adopt-this-type-of-food-delivery-model [Accessed March 4, 2021].

Limon, M.R. 2021. “Food Safety Practices of Food Handlers at Home Engaged in Online Food Businesses during COVID-19 Pandemic in the Philippines.” Current Research in Food Scienc 4(63-73). https://doi.org/10.1016/j.crfs.2021.01.001

Littman, J. 2021, January 26. “Wow Bao to Reach 1K Locations through Its Host Kitchen Program.” Restaurant Dive. Available online: https://www.restaurantdive.com/news/wow-bao-to-reach-1k-locations-through-its-host-kitchen-program/593978/ [Accessed March 22, 2021].

Maze, J. 2020. “Chili’s Owner Has Some Big Plans for It’s Just Wings.” Restaurant Business. Available online: https://www.restaurantbusinessonline.com/financing/chilis-owner-has-some-big-plans-its-just-wings [Accessed March 22, 2021].

McGrath, K. 2020. “How to Use Walmart Grocery Pickup and Delivery.” Offers. Available online: https://www.offers.com/blog/post/walmart-grocery-pickup-and-delivery/ [Accessed March 4, 2021].

Mercatus and Incisiv. 2020. E-Grocery’s New Reality- The Pandemic’s Lasting Impact on U.S. Grocery Shopper Behavior. Available online: https://www.incisiv.com/hubfs/ebook/Mercatus%20-%20eGrocerys%20New%20Reality/Mercatus_Report_eGrocery-Shopper-Behavior-FINAL.pdf?vgo_ee=UoO%2FTD%2B7wydRG%2BSDUnx%2BsIvy7T5YEJ8ohjC9vauJg30%3D [Accessed March 25, 2021].

Niu, B., Q. Li, Z. Mu, L. Chen, and P. Ji. 2021. “Platform Logistics or Self-Logistics? Restaurants’ Cooperation with Online Food-Delivery Platform Considering Profitability and Sustainability.” International Journal of Production Economics 234:108064. https://doi.org/10.1016/j.ijpe.2021.108064

Scheiber, N., and K. Conger. 2020, March 30. “Strikes at Instacart and Amazon over Coronavirus Health Concerns.” The New York Times. Available online: https://www.nytimes.com/2020/03/30/business/economy/coronavirus-instacart-amazon.html [Accessed March 15, 2021].

Shead, S. 2020, December 3. “Covid Has Accelerated the Adoption of Online Food Delivery by 2 to 3 Years, Deliveroo CEO Says.” CNBC. Available online: https://www.cnbc.com/2020/12/03/deliveroo-ceo-says-covid-has-accelerated-adoption-of-takeaway-apps.html [Accessed February 24, 2021].

Singh, S. 2019. “The Soon to Be $200B Online Food Delivery Is Rapidly Changing the Global Food Industry.” Frost and Sullivan. Available online: https://ww2.frost.com/frost-perspectives/the-soon-to-be-200b-online-food-delivery-is-rapidly-changing-the-global-food-industry/ [Accessed February 25, 2021].

Statista. 2020a. eServices Report 2020 - Online Food Delivery. Available online: https://www.statista.com/study/40457/food-delivery/ [Accessed February 23, 2021].

Statista. 2020b. Online Food Delivery Report - United States. Available online: https://www.statista.com/outlook/dmo/eservices/online-food-delivery/united-states [Accessed February 23, 2021].

Statista. 2021a. U.S. Consumers: Online Grocery Shopping - Statistics & Facts. Available online: https://www.statista.com/topics/1915/us-consumers-online-grocery-shopping/ [Accessed March 5, 2021].

Statista. 2021b. Platform-to-Consumer Delivery User Penetration (United States). Available online: https://www.statista.com/outlook/dmo/eservices/online-food-delivery/platform-to-consumer-delivery/united-states#analyst-opinion [Accessed February 25, 2021].

Stucky, B. 2020, October 2. “Online Grocery Shopping Will Continue Post-COVID Says Data from Online Grocer Good Eggs.” Forbes. Available online: https://www.forbes.com/sites/barbstuckey/2020/10/02/online-grocery-shopping-will-continue-post-covid-says-data-from-online-grocer-good-eggs/ [Accessed Feb 28, 2021].

Sun, J., and J. Buijs. 2018. “Online Food Regulation in China: The Role of Online Platforms as a Critical Issue.” European Food and Feed Law Review 13(6):503-513.

Thakker, K. 2020. “Giant Eagle to Open 2nd Pickup and Delivery-Only Store.” Grocery Dive. Available online: https://www.grocerydive.com/news/giant-eagle-to-open-second-pickup-and-delivery-only-store/575911/ [Accessed March 15, 2021].

U.S. Department of Agriculture. 2021. Food Expenditure Series. Washington, DC: U.S. Department of Agriculture, Economic Research Service. Available online: https://www.ers.usda.gov/data-products/food-expenditure-series/food-expenditure-series/ - Current Food Expenditure Series [Accessed February 20, 2021].

Volpe, R., E.C. Jaenicke, and L. Chenarides. 2018. “Store Formats, Market Structure, and Consumers’ Food Shopping Decisions.” Applied Economic Perspectives and Policy 40(4):672-694. https://doi.org/10.1093/aepp/ppx033

Wells, J. 2020a, March 26. “Kroger Converts Store to Pickup-Only Service.” Grocery Dive. Available online: https://www.grocerydive.com/news/kroger-converts-store-to-pickup-only-service/574952/ [Accessed March 15, 2021].

Wells, J. 2020b, April 13. “Amazon's Woodland Hills Supermarket Is Now a Dark Store.” Grocery Dive. Available online: https://www.grocerydive.com/news/amazons-woodland-hills-supermarket-is-now-a-dark-store/575953/ [Accessed March 15, 2021].

Wells, J. 2020c April 3. “Should Grocery Stores Go Dark?” Grocery Dive. Available online: https://www.grocerydive.com/news/should-grocery-stores-go-dark/575374/ [Accessed March 22, 2021].

Yeo, L. 2021, April 14. “Which Company Is Winning the Restaurant Food Delivery War?” Second Measure. Available online: https://secondmeasure.com/datapoints/food-delivery-services-grubhub-uber-eats-doordash-postmates/ [Accessed April 5, 2021].