Ground beef consumption in the United States accounts for over half of total beef consumption and is included in a variety of products from tacos to chili to hamburgers (Greene 2012; National Cattlemen’s Beef Association 2009, 2012; Peel, 2012). The importance of ground beef to U.S. consumers is reflected in the number of restaurants that include hamburgers on their menus as well as the different types of hamburgers offered. Despite the slow economic recovery that has been occurring over the past few years, quick-service restaurants focusing on serving quality hamburgers have been expanding across the country. This is in addition to better known chains such as McDonald’s and Wendy’s periodically updating their hamburger offerings to boost sales which reflects the latest trends present among consumers.

Although ground beef consumption accounts for over half of total beef consumption, it accounts for approximately a quarter of the beef produced from each steer or heifer carcass (Nold, 2012) and a much larger percentage of harvested cows. Additional ground beef is produced by grinding primal chuck and round cuts, but these are more expensive. Compared to the 1970s, domestic beef demand dropped as consumer demand shifted toward leaner protein sources, namely chicken. Although the number of cattle in the U.S. has declined since the 1970s, increased efficiency has contributed to an increase in total U.S. beef production. The primary source of lean ground beef is not from feedlot finished cattle, but from mature cows and bulls slaughtered and from imported lean beef trimmings. Supplies of mature cows and bulls are limited compared to feedlot finished cattle, as an average of 6.3 million cows and bulls have been slaughtered under federal inspection annually since 2000 compared to 27.4 million steers and heifers.

It is in this environment that lean finely textured beef (LFTB) was developed to increase the percent leanness of relatively fatty beef trim—items after removal of major cuts from carcass. The overall value of a beef carcass was increased due to production of LFTB, which allowed consumers to experience near constant prices of products like hamburgers. Following media stories on LFTB, referred to as “pink slime,” in March 2012, consumers rejected the beef product with immediate implications for the U.S. beef supply chain. This article explores the implications for beef markets as a result of the rejection by some consumers and retailers for LFTB. Discussion is also included on industry reaction to the story.

LFTB has been used since the early 1980s (Rabobank, 2012) although the exact product sold by Beef Products Incorporated (BPI), and which was at the center of media and consumer publicity in March 2012, has only existed since 2001 (Andrews, 2012).

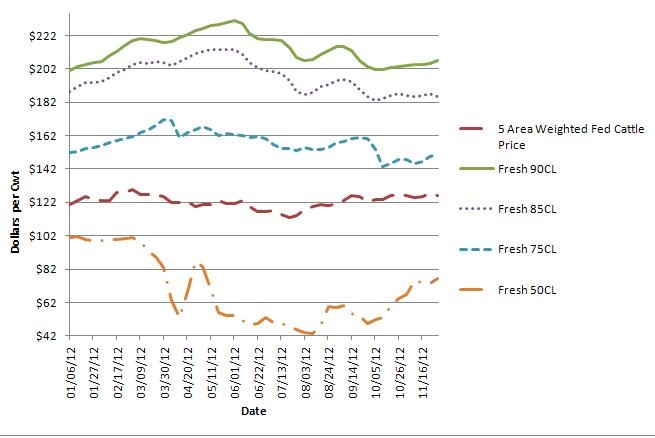

Dramatic public backlash against the use of LFTB—or termed “pink slime,” based on wording from a former USDA scientist—occurred following the airing of an ABC News segment on March 7, 2012 (Avila, 2012a), even though there had been other stories on LFTB in previous years (see Andrews, 2012). Consumer concern was almost immediate with ABC News alerting its viewership to which retail outlets carried LFTB in a follow-up story on March 8th (Avila, 2012b). Price impacts were not immediately apparent in the fed cattle futures and cash markets, but weekly prices for 50% chemically lean (CL) trimmings showed a 2% decline in the first week and increased to a 48% drop by mid-April. Fifty percent (50CL) trim prices would stage a short-lived recovery in late April, but the damage in public confidence was too great to overcome.

Through the end of June, lean trimmings (75CL, 81CL, 85CL, and 90CL) held or increased in their value relative to the first week of March, as 50CL trim prices continued to decline. The loss of LFTB acceptance resulted in a large increase in the supply of 50CL.

BPI was not the only company producing a form of LFTB, and production of this beef product by all companies has slowed since the news stories in March 2012. While this story has huge potential ramifications for the entire meat and poultry industry, the drought that has enveloped much of the United States in subsequent months has become the larger story. The impact of the drought on pasture and range conditions combined with rapidly declining yield expectations for corn and soybeans have had a larger impact on fed and feeder cattle prices than LFTB. Regardless, the fallout from the lack of demand of LFTB reflected in the price for 50CL trimmings continues to lower the value of fed cattle. The decline in demand for 50CL trimmings may be permanent, short of a shift in consumer demand resulting from consumer or retailer re-acceptance of LFTB type products.

Why did the industry adopt LFTB use? Use of LFTB helped to recover approximately 110 pounds of beef trimmings that were less than 50% chemically lean (Rabobank, 2012). Otherwise this product would have been rendered down or would have been incorporated into lower value products on each carcass harvested. The use of 50CL allowed the industry to improve efficiency at the processing level amid a period of declining cattle herd supply in the U.S. and other major beef producing nations. Even though the total U.S. beef herd numbers declined in recent years, total beef supplies had not declined because carcasses were getting larger and the industry was able to more efficiently harvest what was available.

On the consumer demand side, ground beef is typically produced, or ground, into a range of lean-to-fat ratios to meet the requirements of various retail buyers. The ground beef lean-to-fat ratio typically ranges from 50% lean and 50% fat up to 97% lean and 3% fat. The LFTB process allowed lean beef to be taken out of trimmings that contain a high percentage of fat. Extracted LFTB, approaching 100% lean beef, can be blended with other beef to increase the percentage lean which consumers continue to demand.

LFTB never accounts for more than 15% of a ground beef mixture comprised of lean trimmings that range from 94 to 97% chemical lean (94CL, 97CL). Using ground beef in combination with LFTB results in a desired percentage lean ground beef offering to consumers. Table 1 illustrates prices which affect the formation of an 85% lean-15% fat ground beef mixture with and without the inclusion of LFTB. The beef trim prices are reflective of prices at the wholesale level in mid-February 2012, and indicate savings that can be passed on to consumers.

| Ground Beef with LFTB included | Ground Beef without LFTB | |

| Percent Usage of 90CL Ground Beef Trim | 75% | 87.5% |

| 90CL Ground Beef Trim Price ($/cwt) | $212.28 | $212.28 |

| Percent Usage of 50CL Ground Beef Trim | 15% | 12.5% |

| 50CL Ground Beef Trim Price ($/cwt) | $99.84 | $99.84 |

| Percent Leanness of LFTB | 95% | N/A |

| Percent Usage of LFTB | 10% | N/A |

| LFTB Price ($/cwt) | $174.00 | N/A |

| Percent Leanness of Ground Beef Mixture | 85% | 85% |

| Ground Beef Mixture Price ($/cwt) | $191.59 | $198.23 |

The cost savings from use of LFTB in ground beef mixtures may not be large, but helps to explain why an estimated 75% of hamburger patties sold in the United States contained LFTB by mid-2008 (Shin, 2008). In the intensely competitive hamburger market, where margins are razor thin and profits often measured in fractions of a penny, these cost savings are extremely important.

The inability to use LFTB in ground beef mixtures has not dampened the U.S. consumers’ appetite for products requiring ground beef. Sources of lean ground beef are still needed due to U.S. consumer preferences for lean beef. As a result of some consumers and retailers unwillingness to accept LFTB, 13 pounds of beef per animal are no longer being used for human consumption (Cross, 2012). This meat did not disappear, but is being incorporated into lower value products and thus reducing the overall value of cattle to producers.

The processes used in production of LFTB are an illustration of the disassembly process involved in transforming cattle into beef and, ultimately, steaks, roasts, and ground beef (Robb, Lawrence, and Rosa, 2006). Consumer beef demand rests on these products, as beef demand is an aggregation of the demand for each of those products consumers eat such as roasts, ground beef, and steaks. Technologies such as LFTB increased the supply of recoverable lean beef from fat trimmings, allowing for lower priced beef at the retail counter and cattle there were higher in value at the farm gate.

Cross (2012) and Rabobank (2012) argue that the inability to use LFTB will result in the need for an additional 1 to 1.5 million cattle to be slaughtered annually. Loss of the LFTB production process creates an inability to efficiently use all the products available from beef carcasses. An additional 1 million cattle slaughtered would result in more steaks, roasts, and other beef cuts also being produced along with ground beef, which would reduce prices for these beef cuts and the overall value of cattle at the farm gate.

Lack of consumer acceptance of LFTB opens the door to development of technologies that can efficiently harvest all available beef on each animal slaughtered. Without the use of LFTB, more 90CL trim from mature cows and bulls will be needed to increase the leanness of ground beef when mixed with 50CL trim (Peel, 2012). Supplies of 90CL trim come primarily from mature cows and bulls which accounts for approximately 20% of Federally Inspected cattle slaughter. Domestic supplies of 90CL trim are expected to continue tightening in the next few years as the U.S. cattle herd shifts from contraction to expansion resulting in fewer mature cows and bulls going to slaughter.

Not all of the 90CL trim though will come from domestic sources. Additional supplies of 90CL trim will come from a variety of sources including U.S. cattle producers, slaughter cow imports from Canada, and frozen beef imported from Australia and New Zealand. At this point, the question is which source will be quickest to respond and at the lowest cost to consumers in this competitive market?

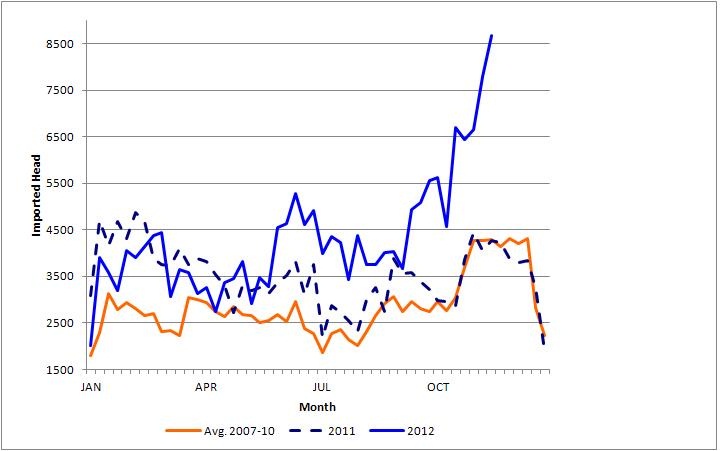

Regardless of the source of the beef, indications are that the concern over LFTB has led to the U.S. importing more beef. This is not trivial, given the increased interest among some U.S. consumers for locally produced food.

In early April, 2012, imports of Canadian slaughter cows and bulls began to increase, partially in response to the inability of U.S. processors to continue to use LFTB in ground beef mixtures.

The increase in cattle imports was likely to occur, given price trends, even without the loss of LFTB, but certainly imports have increased from the negative press coverage surrounding LFTB. Year-to-date imports from Canada are on pace to provide approximately 200,000 head of mature cows and bulls.

Imported lean beef trimmings from Australia and New Zealand can also fill the void in an LFTB-free marketplace, but not without its own set of challenges. Imports from these countries are typically frozen, which work better in the hotel and restaurant industries due to the lack of mandatory country-of-origin labeling (mCOOL) required for retail grocery sales. Additionally, frozen processing beef is more difficult to use in retail packaging due to the increased liquid that results when frozen product is thawed, thereby increasing the chances of leaky packages (Rabobank, 2012). Through May of 2012, U.S. imports of Australian beef trim have increased 85% over last year. The strengthening of the Australian dollar relative to the U.S. dollar during this time period cannot be ignored, but frozen 90CL trimmings from Australia and New Zealand have been trading at a discount to U.S. frozen 90CL trimmings for every month in 2012. The fact that fresh U.S. beef trimmings (90CL) continue to trade at a premium to imported frozen trimmings of similar leanness indicates that the frozen imported product is not a perfect substitute for fresh product.

The issue of LFTB further illustrates the divide in perception of consumers and agricultural producers. Consumers generally find agricultural producers to be credible, hence the recent push by farm organizations to have producers “tell their story” and the development of public relation programs such as the Masters of Beef Advocacy by the National Cattlemen’s Beef Association to help combat misinformation.

While there is room in today’s marketplace for a variety of production methods, consumer knowledge about processing practices used to convert a raw food commodity into the desired food product is lacking. Part of the backlash against LFTB was the use of beef previously rendered into nonfood products and use of ammonium hydroxide to prevent the risk of E. coli and other pathogen contamination. Critics of the way the beef industry and USDA handled media coverage have argued products containing LFTB should have been labeled as such (Ray and Schaefer, 2012; Lean Beef or Pink Slime? It’s All in a Name, USA Today, April 2012).

Questions remain as to what part and to what extent LFTB should have been labeled: low value beef trim being incorporated into higher value beef trim or the fact that ammonium hydroxide was used to kill E. coli and other pathogens? The former has large implications for any meat or poultry product that is ground while the latter has consequences for products ranging from meat to bakery products to confectionery (Greene, 2012). Ammonium hydroxide is widely used as a processing aid in a variety of food products and the Food and Drug Administration views ammonium hydroxide as generally recognized as safe (International Food Information Council Foundation, 2009; Greene, 2012). The use of ammonium hydroxide in LFTB was as a processing aid, and not as an ingredient, which is not required to be labeled per the Food Safety Inspection Service.

Transparency through labeling can reduce information asymmetry, especially at a time when an increasing number of consumers are further and further removed from the realities of agricultural production. However, the effectiveness of transparency is limited when emotions are involved, as is often the case with food production and food safety. Increased transparency would provide consumers with increased knowledge of food production practices, and reduce the “yuck” factor, but there is no guarantee that consumer exposure will eventually lead to consumer acceptance.

Lusk and Briggeman (2009) found that consumers considered food safety the most important of eleven attributes tested. Gimmicky names such as “pink slime” call into question the safety of a product, which can undermine consumer confidence in the attributes of safety, nutrition and taste which were ranked highly by consumers in Lusk and Briggeman (2009).

Social media and the internet have removed a curtain that often separated production agriculture from the average U.S. consumer and ushered in additional opportunities for transparency and for consumer education. Consumers may be more knowledgeable about production practices that are used, but that is not the same as knowing why a practice is employed. The “why” is no less an important question to ask and present to diminish asymmetric information, but it doesn’t always easily translate into a 140 character tweet or blog post. Too much information can also be detrimental if not completely understood or without the proper context. Arguably, the stories by Avila (2012a, b) lacked context due to the repeated use of the pejorative “pink slime” and failure to highlight how LFTB made more efficient use of available domestic lean beef supplies.

Following the timeline set forth by Andrews (2012) demonstrates that opponents of LFTB had been slowly building a case for labeling or removal of LFTB from the food supply since at least 2008. Entities that are not happy with current production practices in modern agriculture have learned to target public opinion. Use of outlets such as the documentary “Food, Inc.” and the New York Times targeted opinion setters. However, public outcry over LFTB did not gain strength until traditional media such as ABC News and other outlets covered the story (Fielding et al., 2012). At that point, no amount of transparency could prevent the downfall of LFTB.

Proponents of transparency in modern agricultural production practices must also remember that while exposure to certain practices may increase consumer acceptance, previous research has shown that “why” doesn’t always matter in the consumer thought process (Lusk, Norwood, and Pruitt, 2006; Tonsor, Olynk, and Wolf, 2009). In both studies, consumers were provided different levels of information prior to completing a questionnaire, only to find that the level of information presented did not lead to differences in results. However, Tonsor, Olynk, and Wolf (2009) found that labeling of pork raised from gestation crates would improve societal welfare more than a ban on gestation crates in pork production. This suggests the possibility that USDA’s action to approve labeling for LFTB to increase transparency was correct.

Norwood (2007) found consumers do realize the impact of their purchasing decisions on aspects of the agricultural supply chain. However, the consequences of those decisions are not always immediately felt. Longer-run price adjustments often result as marketing intermediaries, recognizing income and substitution effects, are reluctant to pass additional costs to the consumer immediately. In the case of LFTB, consumers continue to demand lean ground beef. The majority of ground beef product previously used in LFTB is still being used and consumed as ground beef, but now in a manner that is more expensive and increases costs to consumers and reduces returns to producers. Cost increases such as these are reflective of changes in the underlying production practices. The changes that occur may result in smaller producers exiting the industry due to an inability to capture efficiencies from alternative available technology or the ability to afford the technology.

Another issue may be the name of the product itself. Lean finely textured beef, LFTB, is beef. The descriptors of this beef product do provide the opportunity for individuals to know what it is. Alternatively without sufficient transparency, a product can be rebranded into something seemingly sinister.

The media did no favors to consumers by presenting an unbalanced LFTB story. Consumers are intelligent, but intelligence is different from being knowledgeable. Research that has focused on hot topic animal agriculture issues has not determined the extent of the knowledge base of consumers. This may provide an information void pertaining to their knowledge of what agricultural practices are used, by more importantly why certain practices are used. Knowledge on the “why” may not have made a difference in the case of LFTB, but this can provide a lesson to agriculture related consumer education needs. Providing an improved understanding to consumer’s relating to production practices used at the farm or processing level will help them more reliably assess information provided by the media and other sources.

Labeling and bans on LFTB have been discussed. Labeling provides a degree of information and transparency, but without background knowledge may mislead consumers. Without an educated public, bans could have unintended negative effects on societal welfare, as opposed to the desired result of being welfare-enhancing. The outrage expressed by consumers over LFTB resulted in ABC News providing a lesson for production agriculture that the public must be both educated and informed.

Andrews, J. (2012, April 9). BPI and ‘pink slime’: A timeline. Food Safety News. Available online: http://www.foodsafetynews.com/2012/04/bpi-and-pink-slime-a-timeline/?utm_source=newsletter&utm_medium=email&utm_campaign=120409.

Avila, J. (2012a, March 7). 70 percent of ground beef at supermarkets contains ‘pink slime’. ABC News. Available online: https://www.geekwrapped.com/archive/70-percent-of-ground-beef-at-supermarkets-contains-pink-slime .

Avila, J. (2012b, March 8). Is pink slime in the beef at your grocery store? ABC News. Available online: http://abcnews.go.com/blogs/headlines/2012/03/is-pink-slime-in-the-beef-at-your-grocery-store/.

Cross, R. (2012, April 1). Opposing view: LFTB is 100% beef [Editorial]. USA Today. Available online: http://www.usatoday.com/news/opinion/story/2012-04-01/lean-finely-textured-beef/53933754/1.

Fielding, M., Friedland, D., Gabbett, R.J., Johnston, T. and Keefe, L.M. (2012, May). SLIMED what the hell happened. Meatingplace. Available online: www.meatingplace.com/Print/Archives/Details/4162.

Greene, J.L. (2012, April). Lean finely textured beef: The “pink slime” controversy. Washington, DC: Congressional Research Service R42473. Available online: http://www.fas.org/sgp/crs/misc/R42473.pdf.

International Food Information Council Foundation. (2009). Questions and answers about ammonium hydroxide use in food production. Available online: http://www.foodinsight.org/Resources/Detail.aspx?topic=Questions_and_Answers_about_Ammonium_Hydroxide_Use_in_Food_Production.

Lean beef or pink slime? It’s all in a name [Editorial]. (2012, April 1). USA Today. Available online: http://www.usatoday.com/news/opinion/editorials/story/2012-04-01/pink-slime-lean-beef/53933770/1.

Lusk, J.L, and Briggeman, B.C. (2009). Food values. American Journal of Agricultural Economics, 91(1),184-196.

Lusk, J.L., Norwood, F.B., and Pruitt, J.R. (2006). Consumer demand for a ban on antibiotic drug Use in pork production. American Journal of Agricultural Economics, 88(4),1015-1033.

National Cattlemen’s Beef Association. (2012, August). Average annual per capita consumption, beef cuts and ground beef. Available online: http://www.beefusa.org/CMDocs/BeefUSA/Resources/Statistics/averageannualpercapitaconsumptionbeefcutsandgroundbeef559.pdf.

National Cattlemen’s Beef Association. (2009, May). Beef market at a glance. Available online: http://www.beefusa.org/CMDocs/BeefUSA/Resources/Statistics/factsheet_beefmarketataglance.pdf.

Nold, R. (2012, January 2). How much meat can you expect from a fed steer? Brookings, SD: South Dakota State University Extension. Available online: http://igrow.org/livestock/beef/how-much-meat-can-you-expect-from-a-fed-steer/.

Norwood, F.B. (2007, November 26). lessons abound on animal welfare issue. The Voice of Agriculture-American Farm Bureau.

Peel, D.S. (2012). Getting what you asked for and not liking what you get. Cow/Calf Corner Newsletter; April 2.

Rabobank. (2012, July). LFTB: Beef’s latest battleground for survival.

Ray, D.E., and Schaffer, H.D. (2012). Pink slime: An object lesson for the meat industry? University of Tennessee Agricultural Policy Analysis Center. Available online: http://www.agpolicy.org/weekcol/611.html.

Robb, J.G., Lawrence, A.E., and Rosa, E.L. (2006). Issues related to beef traceability: A discussion of transforming cattle into products. Lakewood, CO: Livestock Marketing Information Center. Available online: http://www.lmic.info.

Shin, A. (2008, June 12). Engineering a safer burger. Washington Post, p. D-1.

Tonsor, G.T., Olynk, N., and Wolf, C. (2009). Consumer preferences for animal welfare attributes: The case of gestation crates. Journal of Agricultural and Applied Economics, 41(3), 713-730.