4th Quarter 2012

On March 7, 2012, ABC News aired a report on the use of lean, finely textured beef (LFTB), or “pink slime” as its reporters dubbed it. Although this was not the first time LFTB had been the subject of negative criticism on a national scale, the attention is no longer just coming from traditional media outlets (television, radio, and newspaper), but also from social media sources (Facebook, blogs, and Twitter). Of particular importance is the influence this reaction has had on the financial performance of agribusiness firms in the food supply chain. If image is everything and perception is reality, particularly as it relates to food safety, then agribusiness firms might be in for some challenges. Food and agribusiness firms will need to be prepared to react every time a food safety issue receives attention in social media irrespective of how these images and perceptions are generated.

As early as 2008, the documentary Food, Inc. provided many Americans with their first exposure to LFTB. In December 2009, the New York Times questioned the technology for producing LFTB, particularly the safety of the ammonium hydroxide process (Moss, 2009). The next major mention of LFTB occurred in April 2011, when chef and TV personality of the television show “Food Revolution”, Jamie Oliver, blasted the production process. His rant was witnessed by approximately 5.4 million viewers. Oliver, a celebrity chef and food activist, criticized the process used by Beef Products Incorporated (BPI), when he placed beef trimmings in a washing machine and doused them with an ammonia-cleaning product so he could demonstrate his perception to consumers of what they were consuming. Many of those viewers took to their blogs and twitter accounts to condemn the process, based upon Oliver’s actions that night. The “Oliver event” might be deemed ground zero as it relates to LFTB and agribusiness; it marks one of the largest uses of social media to condemn a food practice determined to be safe by the United States Department of Agriculture (USDA). Agribusiness companies, particularly fast food companies known for their use of ground beef, took notice. McDonald’s, Burger King, and Taco Bell responded to the “Oliver event” by indicating through company media releases that they would no longer be using LFTB in their products. Both Burger King and McDonald’s indicated their decision to remove Beef Products Incorporated (BPI) beef—the seller of LFTB—from their lists of suppliers of ground meat had nothing to do with the “Oliver event” and everything to do with keeping with corporate strategy. The “Oliver event” should serve as a lesson that the tension between the food supply chain and its consumers will likely increase as consumers are further removed from agriculture and the processes needed to ensure a safe food supply.

The report from ABC News (Avila, 2012) created a flurry of activity along the food supply chain. First on March 15, 2012, the USDA announced it would allow school districts the option of excluding ground beef containing LFTB from its food program. Approximately two weeks after ABC News’s initial report, retail grocery stores issued statements on the use of LFTB in their ground beef offerings. Some publicly traded companies indicated they never offered ground beef that contained LFTB—for example, Whole Foods and Costco; others such as Kroger, Safeway, and SuperValu indicated that they would no longer offer ground beef that included LFTB, and Wal-Mart indicated that it would give its consumers a choice between ground beef with and without LFTB. This list is not inclusive, as there were also many privately owned grocery chains that made similar declarations about LFTB. The commonality between the public and private companies was that they all seemingly affirmed their belief in the safety of LFTB, but were responding to the market demand for ground beef that did not contain LFTB. The announcements did not stop with the grocery sector, as Wendy’s and Red Robin each issued statements saying they had never used LFTB, McDonald’s reiterated that it had long since removed LFTB from its ground beef, and Tyson announced that it would make accommodations for customers who did not want LFTB in their ground beef (Bartlein and Geller, 2012; Food Safety News, 2012). At the same time the restaurant industry was making its statement on LFTB, three of the largest packaged food companies in the United States—ConAgra Foods Inc. (Chef Boyardee, Slim Jim, and Hebrew National), Sara Lee Corp. (Jimmy Dean, Ball Park, and Hillshire Farm), and Kraft Foods (Oscar Mayer)—each announced that none of their products contained LFTB.

Because public and private companies in the retail food supply chain create value only by satisfying their consumers’ needs and wants, they must satisfy those demands. In the LFTB case, the decline in demand resulting from negative publicity led to a loss of revenue for its producers. This loss in business had a devastating effect on BPI. On March 25, 2012, BPI announced the suspension of operations in its Iowa, Kansas, and Texas plants, which reduced the production of LFTB by 900,000 lbs. a day and left the jobs of 650 people in limbo. Following BPI’s announcement, AFA Foods, a ground beef processing company, declared bankruptcy and cited media coverage surrounding “pink slime” as the cause for a significant decline in demand for its products. Although firms reacted to demand, there is relatively little research related to what extent these reactions are warranted. Therefore, the decision-makers of the firms located in the retail food supply chain cannot accurately judge how consumers will react to these pressures. That is, should they announce that they are removing a potentially safe product from their offerings, do nothing at all, or offer their customers a choice? If the market readily values these practices, then those food companies and agribusinesses that have not made statements about LFTB would be wise to do so. If the market does not value either knowing if a company is going to remove LFTB from its offerings and/or offer alternatives, those managers who have reacted to the aforementioned pressures may have acted prematurely. Thus, this article aims to assess how different reactions of publicly traded food supply agribusiness firms—restaurants, grocery stores, and food processors—to the ABC News report on LFTB influenced the market’s assessment of that firm.

Using the previously mentioned publicly traded food supply companies who issued statements regarding LFTB, excluding Burger King because its stock was taken off the New York Stock Exchange (NYSE) in 2010 and only returned in 2012, we employ the event study methodology to assess the short-term impact of the ABC News report on firm value. By examining stock price behavior around the announcement of an event, we can begin to understand the influence it has on shareholder value (Binder, 1998). A market model (Ordinary Least Squares (OLS)) is estimated by regressing stock returns for a firm on the rate of return for the market for 250 days surrounding the LFTB event (Armitage, 1995). This allows for the identification of abnormal returns during the event period—dates surrounding the event window. The event window involves small intervals surrounding and including the event date. In particular, the two-day event window is used because the event can be determined with certainty (Armitage, 1995). We utilize an 11-day event window, which begins 5 days prior to the announcement date to account for information leakage (Senchack and Starks, 1993).

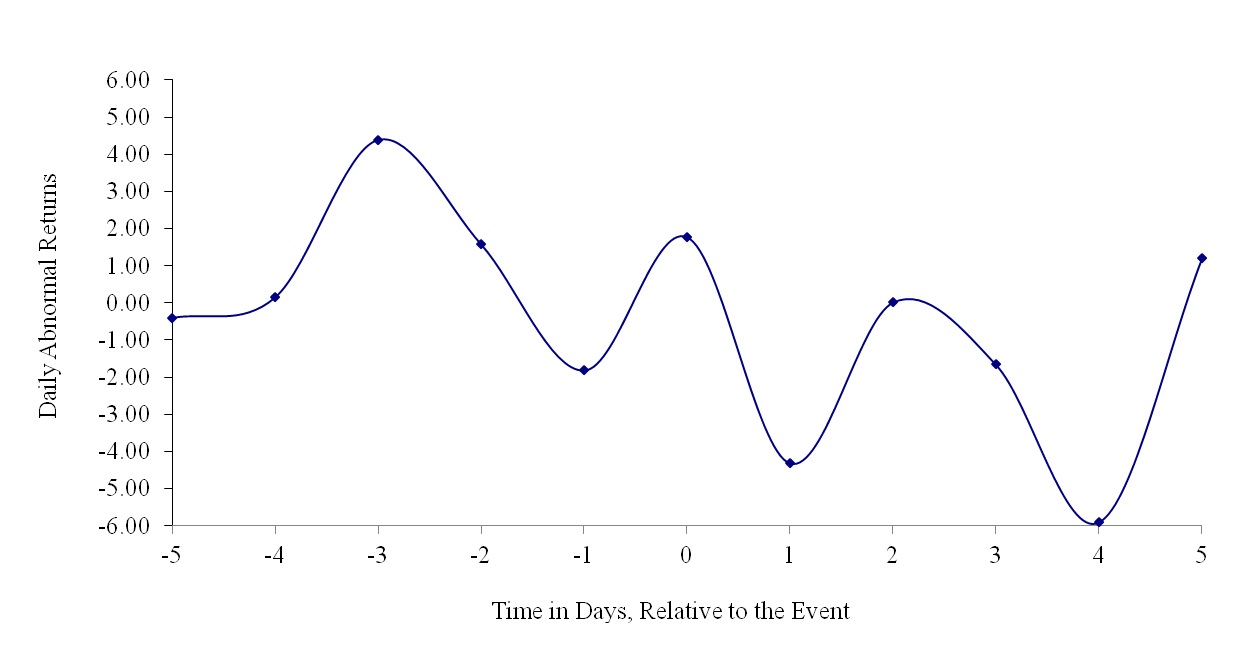

Results of the event study analysis show no statistical significance for the average abnormal returns for the tested publicly traded food supply agribusiness firms’ share values on the day the report aired on ABC nor for any of the 5 days before or after the airing of the report. Figure 1 contains a graphical representation of the daily average abnormal returns during the 11-day event window. The lack of significance indicates that the ABC News report, at least in the short-run, had no influence (positive or negative) on agribusiness returns for any single day in the 11-day event window—the returns behaved as if there had been no report by ABC News. In particular, this means investors, at least in the short-run, did not feel that the LFTB event would influence the agribusinesses’ abilities to continue to generate profit in a manner consistent with recent history.

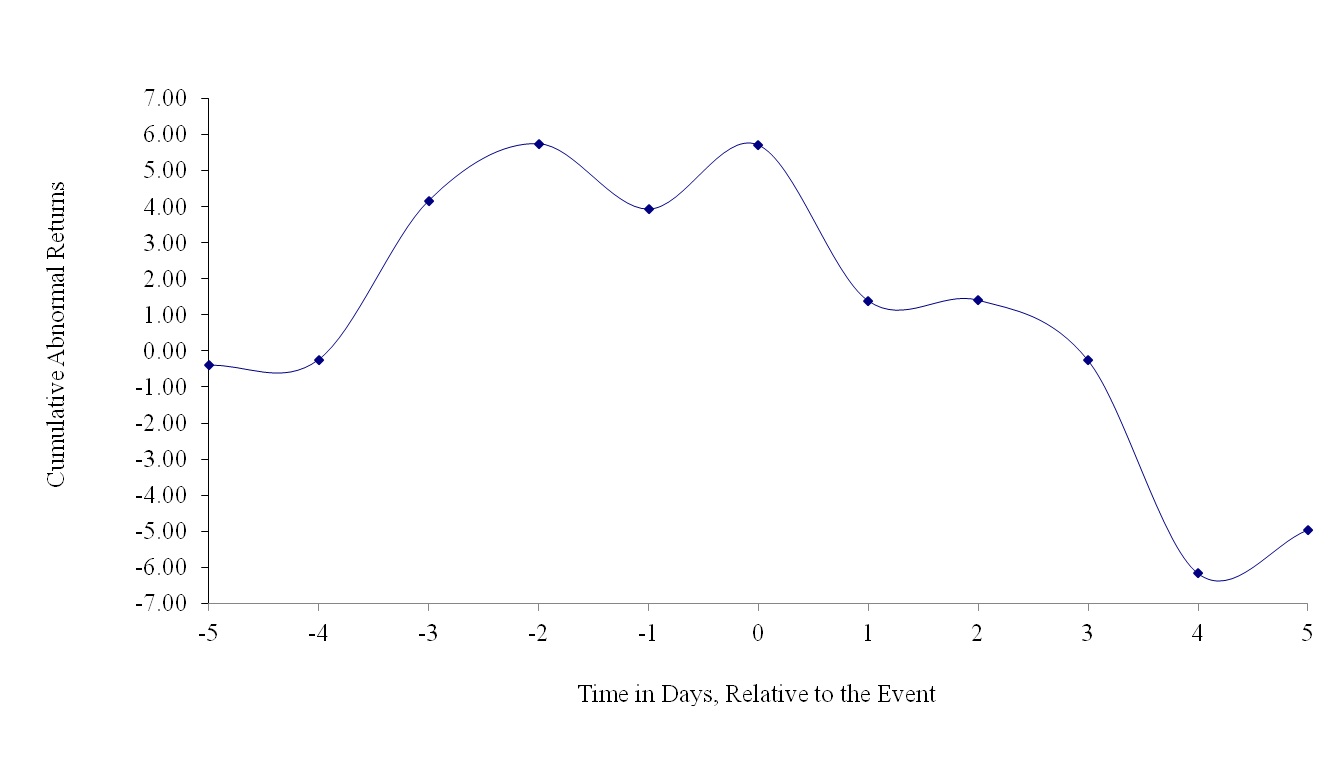

Cumulative abnormal returns allow us to capture the reaction of returns to the agribusinesses over a specified period, relative to the event—ABC News’s report on LFTB, which is important because the market may not react instantaneously, nor at the same time for each agribusiness firm. Figure 2 contains the graph of cumulative returns for the [-5, +5] window. When we look at cumulative abnormal returns for the estimation window, we observe no significant effect. The longer announcement window allows the analysis to capture reactions by agribusiness firms to the report, but is not so long as to allow outside influences unrelated to the event to affect share prices. It is interesting that the agribusinesses in this study issued media releases stating that their products did not contain LFTB, they would remove products with LFTB from their menus, and/or they would offer alternative products that did not contain LFTB. Thus, over the days subsequent to the ABC report, those agribusinesses issuing media releases hoped that they would have an influence on investors. If the hope was that these releases would boost share value, the announcements were not effective; however, if they were to prevent negative public reaction, they could be deemed successful, as these firms did not experience statistically significant negative cumulative abnormal returns.

While the event study measures short-term market reaction to an unexpected event, it does not capture the medium- and long-term effects an event can have on a company. For the LFTB event, the time elapsed has not been sufficient to measure these effects which will require analysis of several quarters of the aforementioned firms’ financial statements. In particular, ratio analysis can provide useful insight into the influence of LFTB. Cash flow per share is not only a good predictor of a firm’s financial stability and financial health, but it is much more difficult for companies to manipulate than earnings per share (EPS). The second financial ratio, return on equity (ROE) measures a firm’s profitability. ROE is defined as net income divided by average stockholder’s equity and measures how effectively the stockholder’s investment is being used to produce profit.

If firms begin to experience a decline in cash flow per share, it likely reflects the first signs the firms are dealing with rising prices of ground beef. McDonald’s, Yum Brands, and Red Robin—large users of ground beef companies that have said they do not use LFTB in their ground beef—must now operate in a market where other firms and entities are no longer using and/or are offering alternatives to LFTB—for example, the USDA. The removal of LFTB from the ground beef supply chain means that the available supply of lean beef has declined, which in turn has caused an increase in lean beef prices and this ultimately reduces cash for some agribusinesses. For a detailed discussion of the LFTB event impact on the U.S. beef supply, see the Pruitt and Anderson article in this issue of Choices.

When examining ROE, declines are typically caused by either decreasing or stagnating firm earnings, which can be attributed to increasing costs and/or lost sales. Thus, for the aforementioned firms it will be crucial to examine how much their ground beef procurement costs have changed and the proportion of these costs to the firm’s total costs. It is likely that those firms that operate in the retail sector as opposed to the processing and manufacturing sectors will be the first to feel the initial effects of rising beef prices first from the loss of LFTB. These costs are likely to be higher than they otherwise would be, in part due to cattle inventory in the U.S. being at its lowest level in more than 60 years thanks to record high corn prices and droughts in states that produce much of the U.S. beef cattle. While cost management from the supply side is extremely important, agribusinesses are more concerned about consumers purchasing their products; otherwise, cost control measures are irrelevant. Loss of sales can have a devastating impact on financial performance, because if people quit eating at a restaurant or purchasing meat from a grocery store, ROE will go down. To get a more complete picture of the effects of the removal of LFTB from a company’s ground beef supply and its ultimate influence on ROE, it will require making earnings comparisons between companies that utilize LFTB and those that do not over a longer time span. Such analysis will allow determination of whether consumers really demand LFTB-free ground beef or are they content with ground beef that contains LFTB.

As the safety of the food supply chain continues to be debated in social media, it will likely become commonplace for agribusiness to react to these debates. This reaction may be in the form of media releases or the removal of products that are proven safe by USDA standards but condemned by the general public because of a lack of understanding the standards. The results from this analysis show that, in the short-term, the market put no value on the pink slime event, as share prices exhibited no abnormal returns. This means that shareholders are unsure whether or not removing LFTB from an agribusiness firm’s offerings will provide the firm with any long-term competitive advantage relative to those that do remove LFTB. In light of the non-reaction in the market in the short-run, it is tempting to say that agribusinesses should not have reacted to public outcries against agribusiness companies; however, we do not fully understand what the medium- to long-term impacts of the pink slime event will be. Consequently, we cannot say whether those firms that reacted immediately will see long-term benefits that outweigh their increases in costs—higher prices of ground beef. To be able to understand the long-term influence of removing LFTB from the beef supply will require a detailed analysis of subsequent quarters of the financials for companies that have and have not removed LFTB from their offerings. While BPI has suffered as the primary producer of LFTB, the final impact on agribusinesses and the retail food-supply chain is not yet known. However, what is evident is that agribusiness will likely need to develop strategic management plans for monitoring and reacting to the social media landscape as it relates to consumer food production.

Armitage, S. (1995). Event study methods and evidence on their performance. Journal of Economic Surveys, 9(1), 25–52.

Avila, J. (2012, March 7). 70 percent of ground beef at supermarkets contains ‘pink slime’. ABC News. Available online: http://abcnews.go.com/blogs/ headlines/2012/03/70-percent-of-ground-beef-at-supermarkets-contains-pink-slime/.

Bartlein, L. and Geller, M. (March 30, 2012). Wendy's jumps into "Pink Slime" public relations war. Reuters, Available online: http://www.reuters.com/article/2012/03/30/us-food-slime-idUSBRE82T1F120120330.

Binder, J.J. (1998). The event study methodology since 1969. Review of Quantitative Finance and Accounting, 11(2), 111–137.

Food Safety News. (September 17, 2012). BPI and pink slime: An updated timeline. Food Safety News, Available online: http://www.foodsafetynews.com/2012/09/bpi-and-pink-slime-an-updated-timeline.

Moss, M. (October 3, 2009). The burger that shattered her life. The New York Times, Available online: http://www.nytimes.com/2009/10/04/health/04meat.html?pagewanted=all&_r=0.

Pruitt, J.R., and Anderson, D.P. (2012). Assessing the impact of LFTB in the beef cattle industry. Choices, this issue.

Senchack, A.J., and Starks, L.T. (1993). Short-sale restrictions and market reaction to short-interest announcements. Journal of Financial and Quantitative Analysis,

28(2), 177–194.