Agriculture in the United States is undergoing a significant change. Grain, oilseed, and land prices have increased significantly, creating a subsequent increase in the income and wealth of many rural Americans—unless you are in animal agriculture. Feed is the largest single cost item for livestock and poultry production, accounting for 60%–70% of the total cost in most years. Although energy, labor, and other inputs have increased, feed costs have increased anywhere from 40%–60% (depending on the species) in the last two years. As price takers in competitive markets, animal producers cannot simply pass their higher costs on to consumers. To date, rising costs have largely been absorbed by livestock and poultry producers, often with significant financial loss. However, higher costs of production will ultimately have to be reflected in higher prices for meat, milk, and eggs at retail counters in the United States and elsewhere. This adjustment process is complex, lengthy, painful, and not without unintended consequences. In this article we attempt to explain what is happening to feed costs, including the likely consequences of the recent ethanol boom on these costs and how the different sectors—beef, dairy, pork, and poultry—are adjusting to higher costs. Importantly, speed of adjustment will vary significantly as industries with shorter production cycles, such as poultry, are able to respond in a matter of months whereas adjustments in industries with longer production cycles, such as beef, can take a period of several years.

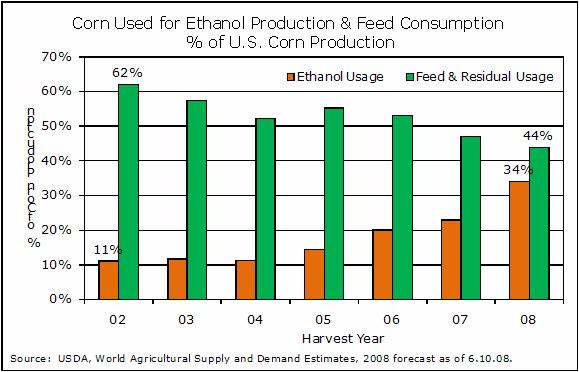

When analyzing the impact of escalating feed costs on animal agriculture, it’s important to consider the causes of these increasing prices as well as overall solutions to the problems resulting from higher feed costs. A variety of factors have contributed to higher feed grain prices. However, unlike most other periods of rising grain prices, recent price increases have been driven primarily by strong demand, not supply shocks. In particular, rapid growth of ethanol production in the United States has been a key factor. Domestic feed usage has historically been the largest use for U.S. feed grains, but ethanol production is taking an ever–increasing amount of corn in the United States (Figure 1). Corn prices have increased dramatically. For example, Omaha corn prices average $1.91/bu in January–March 2006 and were $4.92 for the same period in 2008, a $3/bu, or a 158% increase. Yet, on the last day of May corn in Omaha was priced at $5.45/bu and July 2009 corn futures topped $7/bu, so feed costs continue to rise.

We have had high grain prices before so it’s useful to examine how livestock producers responded in the past to a sharp increase in feed costs. Perhaps the best analogy to our current situation is the price shift that occurred in the 1970s. Corn prices increased from a season average of $1.08/bu for the 1971–72 crop year to $3.02/bu for the 1974–75 crop year, a 179% increase. In response, the U.S. hog breeding herd decreased nearly 15% in two years and U.S. beef cow inventories decreased 19% between 1975 and 1979. Retail prices for pork and beef increased 56 and 46%, respectively, during the same periods. Although the magnitude of the shifts may differ this time, smaller supplies and higher prices are expected.

The current financial losses in most of animal agriculture are not sustainable. Ultimately, higher prices throughout the marketing chain will be required to offset the large increase in production costs. While increased domestic or export demand may help support livestock and poultry prices, higher prices will also come about because quantities supplied to consumers will decline. We’ll offer insight into how the major components of the livestock sector have been impacted by rising feed prices and how each industry is responding to increasing costs and declining profits.

As in all of animal agriculture, production costs have risen sharply in the cattle sector, primarily as a result of rising feed costs. For example, in the cattle finishing sector a monthly survey of commercial cattle feedlots by Kansas State University indicates that the cost of gain increased from an average of about $0.54 per pound in 2006 to $0.74 in 2007 and preliminary estimates indicate feedlot costs of gain will average well over $0.80 per pound during 2008, an increase of 54% in just two years. Cattle feeding returns estimated by Iowa State University indicate cattle feeders experienced the largest loss on record ($167 per head) during April since the series began in the 1960s.

Production costs in the cow–calf sector have also skyrocketed over the last two years. Again, most notable has been the rise in feed costs. Kansas Farm Management Association (KFMA) data documents the shifting cost structure as feed costs per cow increased from $287 in 2006 to $346 in 2007, an increase of 21%. Recent feed grain and protein supplement prices, along with a sharp increase in forage production costs, indicate that total feed costs will rise again during 2008, possibly approaching $450 per cow, an increase of more than 50% in just two years. The same KFMA data indicate that returns in the Kansas beef cow–calf sector still exceeded variable production costs in 2007 by about $50 per cow, but the projected rise in feed costs during 2008 will almost certainly push returns below variable production costs, encouraging some producers to either reduce their herd’s size or to exit the industry.

It’s important to note that the losses experienced in the cattle sector were not associated with large cattle price declines. In fact, prices for slaughter weight cattle in Kansas were record high in 2007, averaging $93 per cwt., 8% higher than in 2006. Increasing feed costs did push calf prices down 1 to 2% in 2007 compared to a year earlier, but annual average calf prices were still the third highest on record. So the reduced profitability was directly attributable to rising costs, especially feed costs.

Higher beef prices in the next few years from stronger domestic demand seems unlikely as beef demand has weakened moderately since 2004. Consumers’ disposable income is a major determinant of consumer demand for beef and slow, or even negative, growth in the U.S. economy during 2008 and 2009 means there will be little likelihood of an increase in domestic beef demand in the short run.

Export demand for beef is improving and will help support beef and cattle prices. Since plummeting in 2004, following the discovery of BSE in the U.S. herd, beef exports have increased significantly. However, U.S. beef exports in early 2008 were still 36% below the same period in 2003. Based on the trend established early this year, U.S. beef exports in 2008 could total 6 to 7% of beef production (still below the 10% of production exported in 2003), which effectively reduces the supply of beef available in the domestic market and hence supports beef and cattle prices. Although current exchange rates will continue to boost U.S. beef exports and discourage imports, the short–run change in domestic supplies resulting from an improving international trade picture is not expected to be large enough to offset the dramatic increase in production costs.

If beef, especially export, demand does not increase enough to yield beef and cattle prices that are high enough to offset the rise in production costs, how will the industry respond? The short answer is that the industry will shrink in size to the point where fewer pounds of beef are marketed to U.S. and international consumers. This shift in the beef supply curve will yield higher prices throughout the beef sector and, over a period of several years, allow producers to cover average total costs. The magnitude of the supply shift that will be required will depend on whether feed grain prices continue to increase or stabilize at their current level and how rapidly beef exports recover, especially to the Pacific Rim countries. Modest herd liquidation is already underway as the U.S. beef cow herd declined by about 1% during 2007. Slaughter data through May 2008 suggests that the liquidation is still underway and might have accelerated somewhat from the 2007 pace. Looking ahead, the U.S. beef industry could be facing several more years of herd reduction before prices rise sufficiently to offset the new production cost regime.

Pork producers enjoyed a nearly unprecedented string of positive returns between February 2004 and September 2007. However, at least part of the prolonged profitability was due to disease problems that increased farm costs but also reduced the supply of market hogs during 2006 and early 2007. An effective vaccine was widely adopted last year which contributed to a nearly 10% year–over–year increase in pork supplies during the fourth quarter of 2007. As a result, hog prices fell to their lowest levels in four years at a time when feed costs reached nearly their highest levels in history, resulting in losses that mounted quickly.

According to Iowa State University’s Estimated Returns, farrow–to–finish hog producer losses for the seven months from October 2007 through April 2008 exceeded the estimated profits of the prior thirteen months. Hog prices during that time did not cover variable costs for producers raising their own grain. Feed costs for farrow–to–finish producers selling hogs in April 2008 were $91.81 per head, 35% higher than April 2007 and 75% higher than April 2006. In late May, corn and soybean meal futures projected an additional $30 per head increase in feed cost by April 2009. If realized, total costs per head in spring 2009 will be nearly $185 per head, 70% higher than in 2006.

The pork industry is reacting to higher costs by downsizing. Breeding herd liquidation is underway in the United States and Canada, and pork supplies are expected to show a year–over–year decrease by the end of 2008 that will continue through 2009. However, small reductions in supply are not likely sufficient to move farm level prices to a level that will sustain the U.S. pork industry.

A simple comparison of prices from 2006 (corn $2/bu and SBM $175/ton) with prices from the first half of the 2007/08 crop marketing year (corn $5/bu and SBM $335/ton) indicates total production costs increased 45%. An elasticity of demand of –.4 suggests that supply will need to decrease by 18% from 2006 levels to offset the cost increase experienced to date. Demand growth, especially in the export markets, will offset some of this reduction. For example, pork exports during January–April 2008 were up over 50% compared to a year earlier. Still, a significant decrease in U.S. pork production, possibly approaching 10%, could be required to push prices back up over average total cost.

The poultry industry has viewed the recent rapid expansion of the ethanol industry with considerable concern. Having few good, commercially viable alternatives to corn as a primary energy feed, the poultry industry responded to the initial surge in corn prices beginning in late 2006 by moving fairly aggressively to rein in production; however, when corn prices began to moderate during the 2007 growing season, poultry integrators ramped production back up. Strong demand for poultry, supported largely by export demand, helped the broiler industry to maintain fairly strong prices in the face of higher production.

The quick response of the industry to escalating feed prices in late 2006, along with fortuitous demand strength, especially exports, has helped soften the blow of higher feed prices on the poultry industry. However, that situation now appears to be changing. Despite prices that appear high by historical standards, poultry producers have begun to feel the pressure of mounting feed costs and significant cutbacks in poultry production are on the horizon, based on the rise in production costs. Feed accounts for about 65% of total live broiler production costs (Dozier, Kidd and Corzo, 2008). The 35% increase in corn prices just since the end of last year suggests a roughly 20% increase in farm–level production costs. The single–sector disequilibrium model described by Lusk and Anderson (2004) can be used to illustrate the potential impact of these higher costs. In that model, a 20% increase in broiler production costs at the farm level would result in a 2% decline in the quantity of broilers offered at the retail level and a 6.1% increase in retail broiler prices.

The dairy industry has had its own unique market situation since this period of increasing feed prices began. Milk prices through this decade can best be described as volatile, going from record high to record low prices and back to new record highs. Class III milk prices were low in 2005 ($10/cwt), but were already increasing in late 2006 because of stronger demand just as corn prices began to escalate. Milk prices peaked in July 2007 at $21.38/cwt, but declined to $16.76/cwt by April 2008. Despite the recent price decline, milk production is still increasing because, unlike the beef industry, output prices are still above production costs.

From 2006 to 2008 milk production costs increased approximately $2.00/cwt according to the Agricultural and Food Policy Center’s representative dairy farms (Anderson, et al. 2008). Feed costs make up approximately 53% of all production costs on the representative dairies. Historically, a $2.00/cwt increase in costs might set in motion a production decline of 2% or more. However, given the current state of milk product demand, milk production remained profitable for most producers despite the cost increase and expansion in the industry is continuing.

The strength in milk prices was largely driven by strong export and domestic demand for milk products which kept milk prices above production costs, despite the increase in feed costs. U.S. milk product exports have increased for a variety of reasons. Drought in Australia, and reduced production in the EU as subsidies decline strengthened the U.S. position as an exporter. The combination of reduced competition in export channels and a weaker U.S. dollar is largely responsible for the growth in U.S. dairy product exports.

The dairy industry also continues to undergo structural changes. More large dairies enter production or expand from existing operations, small dairies continue to exit the industry, and production shifts regionally. Various areas of the United States have experienced rapid growth, like New Mexico, Idaho, and, more recently, the Texas Panhandle. So, dairy production in some regions of the U.S. will decline, while other regions continue to experience growth. Looking ahead, it will take more time for increased milk production to push prices below production costs, although any further increases in feed costs will accelerate that process. Still, strong demand growth, especially in export markets, has so far enabled the dairy industry to avoid the large financial losses attributable to rising feed costs that have hit other livestock species.

A few short years ago, most analysts and policy makers contemplating a four– or five–fold increase in ethanol use would probably have envisioned an array of related external benefits: a reduction in harmful automobile emissions, a lessening of dependence on foreign petroleum, a boost in corn prices for farmers, and an abundance of cheap by–product feeds for livestock producers. While increased ethanol production has certainly yielded some benefits, it has also carried with it a number of unintended consequences, particularly for the livestock sector.

Growth in ethanol production has made carryover feed grain supplies very tight by historical standards exposing livestock producers to more feed price risk than in the past. In turn, tight carryover supplies not only push average prices up, but also contribute greatly to corn price variability. Thus, increasing ethanol production means that livestock producers face far more feed cost risk than in the past.

One of the more dramatic consequences of the ethanol boom has been its impact on by–product prices. As corn prices have risen to historic levels, prices of substitutes for corn in livestock rations have increased sharply as well. Anderson, Anderson, and Sawyer (2008) note that the price of major corn by–product feeds expressed as a percentage of corn price trended lower over the last twenty–five years, suggesting that by–products have gotten a little cheaper relative to corn. However, with corn prices at record levels by–products, in absolute terms, are more expensive than ever before.

If the market for by–products is efficient, by–products will be priced competitive with corn, based on their feeding value. In the long run, then, the advantage to feeding by–products will be mostly for those producers of ruminant animals that are situated close enough to an ethanol plant to realize a transportation cost advantage. In the cattle industry, this suggests a shift of comparative advantage towards Northern Plains and Corn Belt feeders with better access to wet ethanol by–product feeds than Southern Plains feeders.

With respect to the competitive position of various livestock species, prior to the ethanol boom, conventional wisdom held that increased availability of by–products would favor cattle, since ruminants are well–adapted to using these feeds. Additionally, the beef industry has the opportunity to use more forages to feed cattle and, while forage values are rising, the cost increase so far has been smaller than for grains and proteins. Longer term, however, if by–product feeds and forages are priced more competitively with corn, the beef industry’s advantage could erode. With higher feed prices across the board, efficiency of gain again becomes the key determinant of comparative advantage. Thus, it is possible that, in the long run, the ethanol boom may actually enhance the poultry industry’s comparative advantage derived from its greater feed efficiency.

What has been a boon to crop prices has had serious unintended consequences for livestock producers. In fact, the livestock industry has absorbed all of the costs of ethanol and the consequences of those costs are still to be felt in the rest of the economy. For example, through mid–year 2008, all major milk and meat supplies were still higher than during the same period in 2007. But as production of animal proteins decline in response to higher costs, consumer prices will increase and rural communities where livestock and poultry are produced and processed will experience downsizing and loss of economic activity that these sectors created. The new equilibrium in agriculture will have both livestock and renewable fuels. The challenge for animal agriculture is to survive the transition from the old equilibrium based on grain prices driven by the demand for domestic livestock feed and exports to the new equilibrium where demand for grain is driven by government policy and energy prices, which is expected to result in an industry providing a smaller supply of higher priced animal proteins to consumers.

Anderson, D.P., J.L. Outlaw, H. Bryant, J.W. Richardson, D.P. Ernstes, J.M. Raulston, J.M. Welch, G.M. Knapek, B.K. Herbst, and M. Allison. “The Effects of Ethanol on Texas Food and Feed.” AFPC Research Report 05–08. Texas A&M University, Texas AgriLife Extension, and Texas AgriLife Research. April 2008.

Anderson, D.A., J.D. Anderson, and J. Sawyer. (2008). “Impact of the Ethanol Boom on Livestock and Dairy Industries: What Are They Going to Eat?” Journal of Agricultural and Applied Economics 40,forthcoming.

Dozier III, W.A., M.T. Kidd, A. Corzo. (2008). “Dietary amino acid responses of broiler chickens: A Review.” Journal of Applied Poultry Research 17,157–167.

Lusk, J.L. and J.D. Anderson. (2004). “Effects of Country–of–Origin–Labeling on Meat Producers and Consumers.” Journal of Agricultural and Resource Economics 29,185–205.

United States Department of Agriculture. “World Agricultural Supply and Demand Estimates.” Various issues, 2002–2008.

The authors gratefully acknowledge helpful comments from three anonymous reviewers and from Jim Robb, Director of the Livestock Marketing Information Center, Lakewood, CO.