3rd Quarter 2013

Crop insurance is widely supported, and the program has expanded to become the primary component of the farm safety net. Yet, the program’s support and growth has engendered significant criticism for its level of subsidization and other aspects. Such a tension, especially during development of a new farm bill, seems natural and appropriate for a program with rapidly growing taxpayer exposure. From our vantage, employed by National Crop Insurance Services, a 501(c)(6) non-profit organization funded by the crop insurance industry, in this article we offer a within-the-industry perspective on the program status and key issues.

1) Is there a public interest in a resilient, financially sustainable and competitive industry that produces the nation’s food and is subject to natural disasters and other shocks?

Without relying on formal empirical support or a social welfare metric, and understanding the vagueness of the term, we believe there is such an interest. An issue of “public interest” usually merits acknowledgement and protective action by the government and is fundamental to government programs across all major essential industries, such as energy, housing, and health care. Based on legislation and the mission and goals of the U.S. Department of Agriculture (USDA), there appears to be a public benefit or, at a minimum, a public interest in maintaining a resilient and financially sustainable national agriculture by assisting producers in need or helping to make available the tools for them to protect their operations. Of course, specific actions taken to serve the public interest should be subject to cost-benefit analysis and standards which may also serve as evidence of a public interest.

2) Should there be taxpayer (government) support for a farm safety net?

If there is a “public interest” in financial stability in agriculture, should there be public support? This is, of course, a normative question. History of most developed nations indicates a socially revealed preference for some form of public economic support for agriculture, specifically for farmers. Critics of farm programs call for reduced, if any, federal support for the safety net, citing interference with the efficiency of free markets and relative farm prosperity. At this juncture in our history, based on recent farm bill actions, some level of substantive support to agriculture, although reduced, appears definite.

3) What is the willingness and ability to spend on the farm safety net?

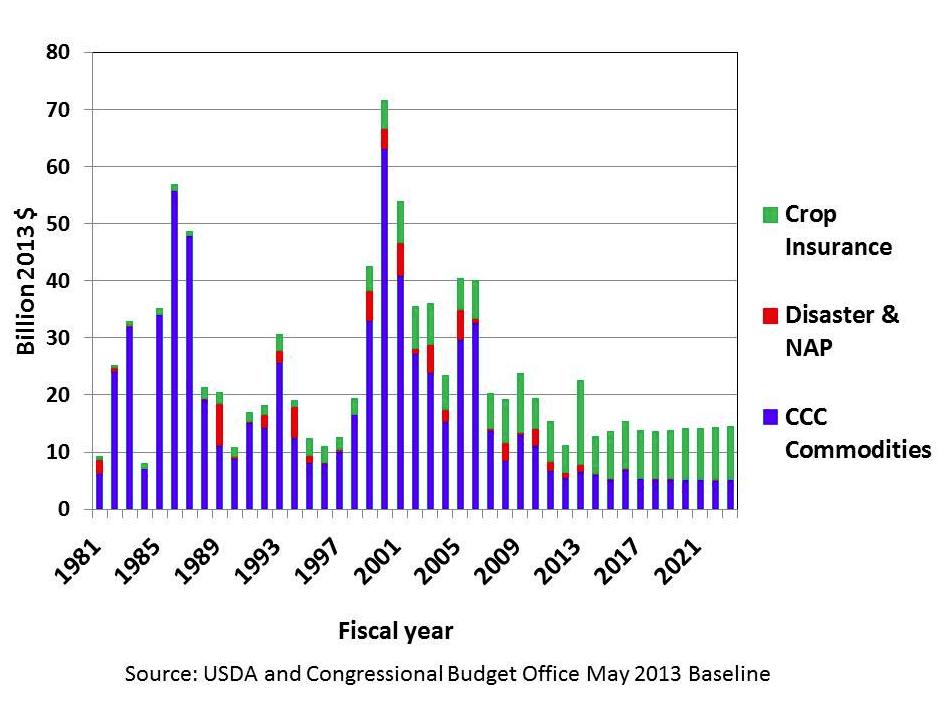

Total taxpayer expenditures on the farm safety net—as measured by a deflated index of prices received for crops—have trended down since the late 1990s (Figure 1). The next major funding cut is expected to be direct payments. Congressional funding targets are measured as cuts from a "baseline" of projected spending. The baseline for the safety net plays out on a couple of levels for the crop insurance program. One level is on the supply side, how much to spend on the delivery system? Recent renegotiations of the Standard Reinsurance Agreement (SRA) between USDA and the approved insurance providers (AIPs) reduced baseline funding for the delivery system. Administrative and Operating (A&O) expense payments have been reduced and capped. Potential underwriting gains for the AIPs have also been reduced. At the same time, the program coverage and complexity has generally expanded. From an industry perspective, this means "more bricks, less straw." However, high commodity prices and low loss ratios in the late 2000s led to unsupportable increases in A&O payments and raised questions as to the true level of industry expected underwriting gains.

On the demand side, how much is the taxpayer willing to subsidize the producer to purchase crop insurance? Beginning with the 1994 Crop Insurance Reform Act, most legislation has increased subsidy levels to encourage greater participation. Critics are challenging these support levels and have proposed alternatives to roll back producer subsidies. Just as funding for AIPs has been reduced in SRA renegotiations and the 2008 Farm Bill, continuing federal budget pressures are likely to result in increasing political interest to reconsider the level and form of premium support. In summary, there is now less willingness and ability to support the safety net.

4) Should the safety net be ex ante or ex post?

The current crop insurance system is ex ante in the sense that all program stakeholders are essentially required to proactively manage their respective risks. Government, via the Risk Management Agency (RMA), along with the AIPs and crop insurance agents, enroll farmers prior to planting of the crop. Liability and premiums are established prior to the determination of indemnities. Because of the contract between the farmer and the AIP, the farmer knows coverage per acre, the policy deductible, and the policy’s insured perils. This stands in stark contrast to ex post ad hoc disaster assistance in which some form of disaster determination must make its way through the political process. The farmer does not know if a loss is payable and the timing of a payment is uncertain. These ex ante features of crop insurance seem attractive from the perspective of both the government and the farmer. Recent literature indicates ex ante crop insurance may be preferred from government’s perspective (Innes, 2003; and Bulut, and Collins, 2013).

5) Is the safety net income support or risk management?

Although the distinction between income support and risk management seems apparent—raising income vs. redistributing income across time—it is useful to contrast a few concepts. Income support programs have been free and the farmer has not necessarily had to experience a natural disaster or even an economic loss to receive a payment. With crop insurance, farmers pay a portion of the premiums and do not receive a payment unless there is a verifiable loss under the terms of the crop insurance policy. The current direction of the 2013 farm bill strongly favors the crop insurance model. It would appear that traditional price and income support programs may ultimately be phased out, although the risk associated with multi-year price declines is not well accommodated in the current crop insurance program.

Considerations 1 through 5 have basically led us to where we are today: a U.S. farm safety net now characterized as a risk-management-based crop insurance system. Given the farm bill debate, we argue that questions 1, 2, 4, and 5 have been answered in the affirmative with a nod toward ex ante risk management. In the case of 3—the budget constraint—we are in the process of determining how much the nation is willing and able to spend on farm support, acknowledging an overall reduction in farm safety net spending as a percent of total crop value, and its division between risk management and direct income support.

The remaining five considerations, in our opinion, are where we think answers to the following questions have the potential to positively contribute to the policy debate in the future.

6) Is current risk sharing optimal?

The U.S. crop insurance program is characterized as a "public-private partnership." The partnership consists of farmers, taxpayers—represented by USDA and RMA—and the private sector insurance industry comprised of crop insurance agents, adjusters, crop insurance company personnel, and the reinsurance community. How do these entities share risk? Descriptively, the current risk-sharing arrangements are set out contractually at several levels: a) the SRA, the risk sharing arrangement between the AIPs and USDA; b) the actual crop insurance policy between the farmer and the AIP; c) the contractual arrangements between the crop insurance agents and the AIPs; and d) the reinsurance treaties between the reinsurers and the AIPs.

The fundamental arguments for risk sharing are: a) government sets rates and underwriting standards, b) government requires a policy to be sold to any producer who desires one, c) private sector risk sharing reduces taxpayer exposure, and d) risk sharing incentivizes companies to reduce losses.

Beyond some assigned risk pool to deal with the risky policies that private companies are forced to take at government-set rates, the choices are: a) all risk borne by the government—as in flood insurance, b) risk shared between the government and private companies, or c) all risk borne by the companies. Under the first choice, if a company could not augment its rate of return through risk sharing under the current program structure, the government would have to pay companies a fee to cover delivery costs plus a reasonable return, a total which may not turn out much different than current total returns, although that is an empirical question. The second choice is the current approach, and the balance of risk held by each party continues to evolve and is subject to change. The third choice is a viable option for an SRA negotiation, which would require greater reliance on more costly private reinsurance markets.

But in what sense is any risk-sharing arrangement "optimal"? There has been some empirical work related to the SRA with an emphasis on program outlays and the underwriting gain or loss potential for the AIPs, but the outcome is a negotiated solution without a clear determination of what constitutes an optimal level of risk sharing between the private and public sectors. With the expectation of further federal budget pressure, the issue of public-private risk sharing should be an area of further investigation.

7) What is the role of area versus individual plans?

Given the advancement of supplemental area plans in the farm bill, it is useful to address some issues about these plans. Area plans do not fall under the traditional definition of insurance. The indemnity paid under an area plan is the result of the area experience, not the experience of the individual. Conversely, a farmer may not receive a payment under an area plan while incurring a large loss on the farm. Our work (Bulut, Collins, and Zacharias, 2012) and others suggest area plans are not necessarily "incentive compatible," and with actuarially fair premium rates, farmers would not demand area coverage relative to individual plans. Currently, there is very little market penetration of area plans relative to individual coverage.

Curiously though, current farm bill alternatives, some policy analysts, and commodity organizations have proposed large scale area plans in lieu of existing farm programs. Perhaps the most compelling reason is program costs, as area plans are less expensive to administer. It has also been argued that area plans are subject to less moral hazard and adverse selection. These are supply-side arguments and beg the question of effective demand. Just as the 2008 Farm Bill’s Supplemental Revenue Assistance Payments program was phased out and the Average Crop Revenue Election program is slated for termination, it will be interesting to observe the development of the large-scale "shallow-loss" area plans and their coexistence with individual coverage.

8) Should the safety net be incentivized?

Use of economic incentives in government programs is a way to achieve efficiency and outcomes that benefit people individually and collectively. The U.S. crop insurance program is incentivized at several, but not all levels. Sales of crop insurance are incentivized through the use of producer premium subsidies and company sales incentives. While producer support has steadily increased, the most recent SRA imposed constraints on overall AIP compensation for delivery expenses and agent compensation. The SRA also reduced the underwriting gain potential of the participating AIPs but also lowered the maximum possible level of underwriting loss. In general, incentivization should be viewed positively, and it can be argued that sales incentives have increased participation and that risk-sharing provides companies the incentive to pay claims accurately, thereby reducing the potential for program fraud, waste, and abuse. If the program is to be national in scope through private delivery, it is also important that the private sector be incentivized to provide delivery in all regions. A key issue going forward will be whether the government budget for a delivery system will provide adequate economic incentives for meaningful, nationwide private sector participation.

9) Can the current incentive structure be improved?

The U.S. crop insurance program is incentivized, in large part, by the use of producer subsidies, sales commissions, and risk sharing, with the incentive structure based on an insurance delivery system model. To be clear, the premise here is on risk management on the part of the farmer, not farm income support. If income enhancement is the primary goal, crop insurance is not the best way to achieve direct income support. A check in the mail, like the lump-sum direct payment, or a negative income tax, are probably more efficient transfers.

Given an incentive-based insurance delivery system, and leaving aside optimal risk-sharing which was previously discussed, the two remaining key elements of the system are producer premium subsidy and A&O producer subsidy of delivery expenses. With respect to producers, how should the subsidy be optimized? Subsidy rates currently vary by plan and unit, decrease by coverage level, and range from 38% of premium to 100%. Subsidy levels remain a function of the premium rate and insured liability; high risk crops receive a higher nominal level of subsidy than low risk crops. Farm Bill proposals seek reductions in the producer subsidy schedule and one proposal specifically calls for the elimination of the producer subsidy for tobacco. Historically, the subsidy schedule has been motivated by the political desire for increased participation and coverage. The future subsidy schedule will likely be guided by the economic impacts of alternative structures and the public willingness to support producers.

A&O payments to AIPs are sometimes misconstrued or misrepresented as an industry subsidy or profit. We argue that A&O delivery payments are another component of farmer subsidy. With regard to the current A&O delivery expense subsidy, should it be re-evaluated in light of the impacts from the present SRA? Caps on payments to agents and the method of distributing A&O payments, which are sensitive to commodity price fluctuations, have created unintended consequences by blunting marketing incentives and arbitrarily reallocating payments across states. It may be time to seriously reconsider the traditional insurance “incentive structure” as we go forward, including alternative approaches.

10) Is crop insurance distortionary?

The incentive structure of crop insurance and the potential for distortionary effects are interrelated. Some literature indicates major farm programs in the past decade or two have had positive but not large effects on overall production and trade. Moreover, some recent literature indicates record-high commodity prices are the primary cause of recent acreage shifts, not subsidized crop insurance. While some impact can be expected from risk reduction and premium support, in aggregate, a program that covers most crops, where farmers pay part of the cost and may not get a payment, and has deductibles that average 20-25%, might not result in land-use distortions or effects as great as the farm programs it is replacing. No doubt economic research will continue to inform this issue on both aggregate and micro levels.

The 10 considerations presented here are by no means exhaustive or presented in depth. Rather, the point is to lay out concerns and issues facing the private and public sectors arising in the farm bill’s development of the farm safety net and in program regulation.

It will be interesting to observe and participate in the direction of agricultural policy in light of the expected increasing prominence of crop insurance. The sway of the political pendulum will determine short-run directional shifts in policy. However, U.S. farm policy appears to be transitioning from direct income support to a risk-management-based system dependent upon both public and private sector participation. Perhaps noted historian Murray Benedict was on to something more than a half century ago when he wrote, “There are indications, however, that crop insurance is gradually emerging as one of the more settled features of American farm policy.” (Benedict, 1953, p. 496). Yet, as we outlined above, key issues remain in play, and particularly the level and use of taxpayer funds in determining a proper balance between the roles of the public and private sector in agricultural risk management.

Benedict, M.R. (1953). Farm policies in the United States, 1790-1950. New York: Twentieth Century Fund.

Bulut, H., Collins, K.J., and Zacharias, T.P. (2012). Optimal coverage demand with individual and area plans of insurance. American Journal of Agricultural Economics, 94(4), 1013-1023.

Bulut, H., and Collins, K.J. (2013). Political economy of crop insurance risk subsidies under imperfect information. Selected paper presented at the Annual Meeting of Agricultural and Applied Economics Association (AAEA), August 4-6, Washington, D.C.

Innes, R. (2003). Crop insurance in a political economy: an alternative perspective on agricultural policy. American Journal of Agricultural Economics, 85(2), 318-335.