Access to agricultural credit for young and beginning farmers is shaped by lenders’ perceptions of the trade-off between risk and returns. Strong returns are generated when loan repayment rates are consistently high. Although the 2008 financial crisis caused repayment rates to dip somewhat, rising commodity prices following the crisis drove farm incomes higher, boosting repayment rates and keeping returns at agricultural banks relatively high.

Young and beginning farmers, however, present greater risk to commercial lenders because of lower farm equity and fewer assets. Lower equity levels lead to greater risk because of the lack of assets that could be liquidated, if necessary, to meet loan obligations. Fewer assets can also limit farm incomes, possibly accentuating the risk. Farmers presenting greater risks to loan portfolios are often required to provide higher levels of collateral when securing farm loans. These requirements, when combined with surging farmland prices, lead to higher fixed costs and cash outlays for young and beginning farmers trying to purchase land, which may serve as a barrier to entry into land-ownership agricultural production.

By balancing risks and returns, credit markets are operating as expected. Bankers typically perceive young and beginning farmers as greater risks and are responding by requiring more collateral, making land purchases more difficult. Many farmers aspire to own the land they operate. However, given the higher capital requirements and the more stringent lending standards, high levels of land ownership may not be a viable model for young and beginning farmers, raising the question of whether facilitating land purchases is the best approach for transitioning to a new generation of farmers.

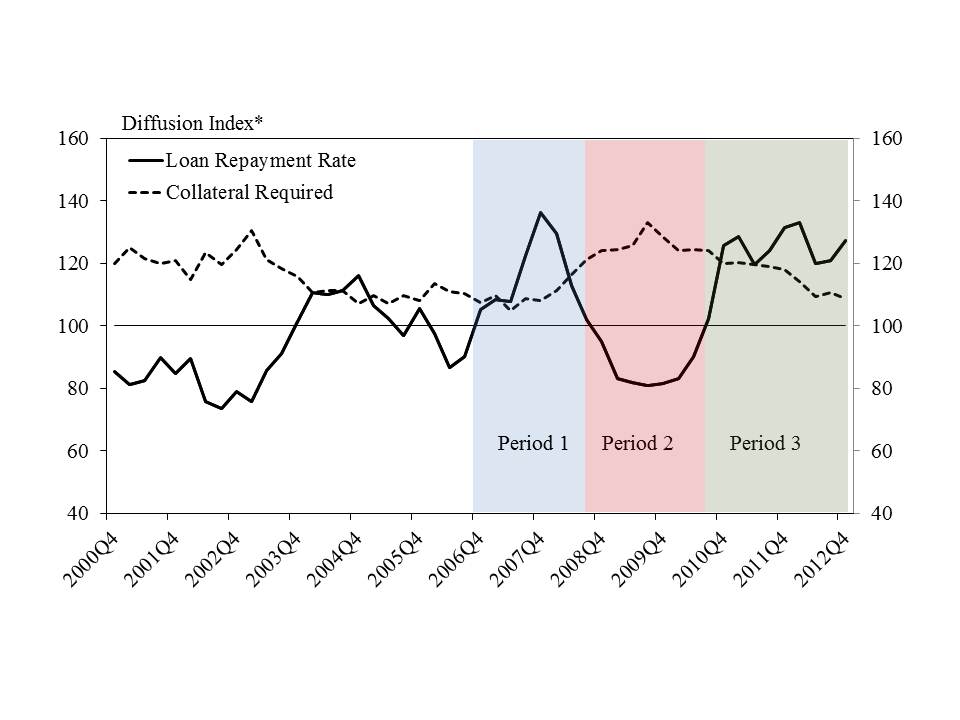

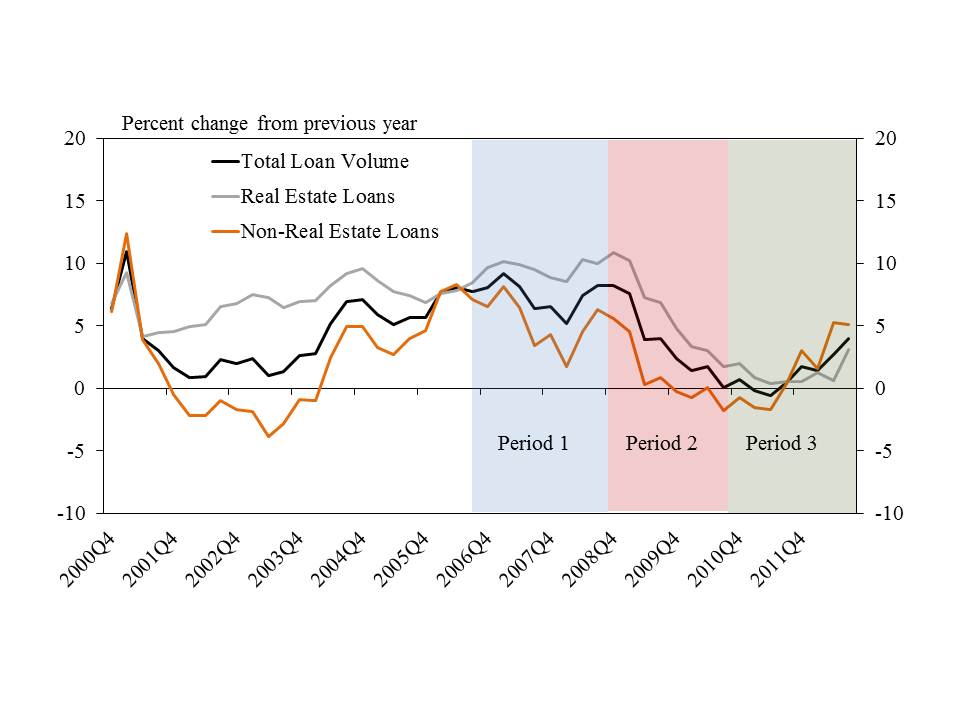

Agricultural credit markets over the past seven years can be separated into three distinct time periods in relation to the 2008 financial crisis. Prior to the crisis, conditions had improved significantly with surging agricultural commodity prices and land values. In the wake of the financial crisis and ensuing recession, loan standards tightened as repayment rates began falling with sharply lower commodity prices. This period of deteriorating conditions, beginning at the end of 2008, lasted until the end of 2010. With the crisis and recession over, credit conditions have rebounded once again with loan repayment rates following commodity prices and land values higher. In contrast to the period before the crisis, however, loan demand has remained relatively soft despite record low interest rates and adequate fund availability.

It can be argued that agricultural finance entered a new era beginning in late 2006. Sharp rises in ethanol production and burgeoning export demand, particularly from China, pushed agricultural commodity prices higher. Higher commodity prices boosted farm incomes. As shown in Figure 1, the loan repayment capacity of farm enterprises improved dramatically with higher incomes as the farm sector began building significant equity in their operations. Figure 2 indicates that after a prolonged period of weak loan demand in the early 2000s, particularly for non-real estate purposes, volumes of both real estate and non-real estate loans began to accelerate in 2006. Year-over-year growth in real estate loan volumes hovered around 10% between 2006 and 2008.

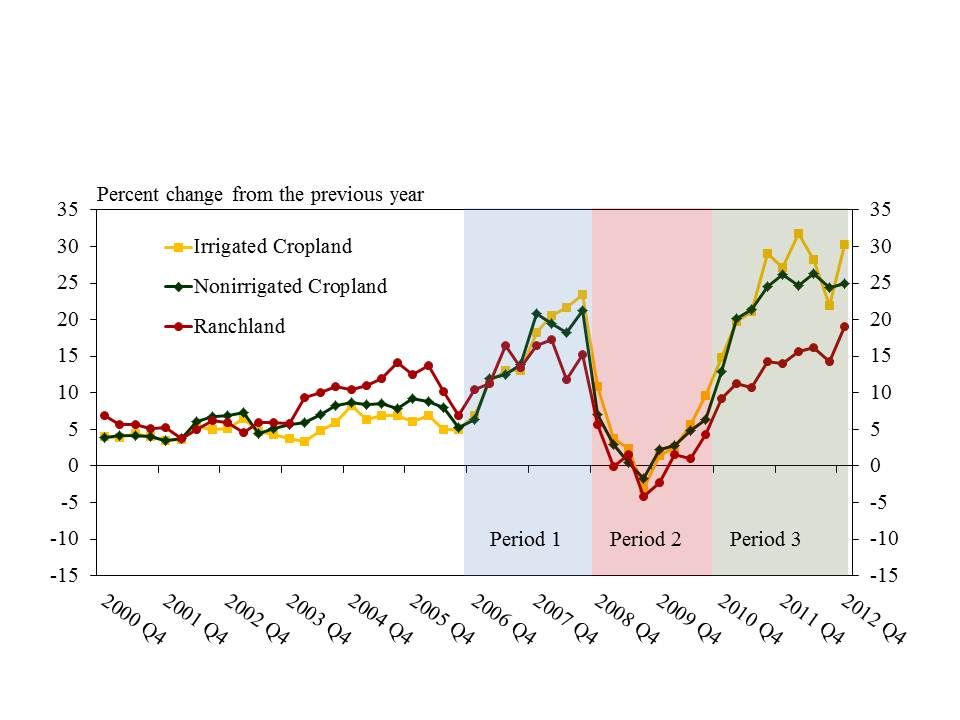

Land values shown in Figure 3 began a sharp ascent between 2006 and 2008, strengthening farm balance sheets. From 2000 to 2007, year-over-year cropland value gains for the 10th Federal Reserve District (which includes Colorado, Kansas, Nebraska, Oklahoma, Wyoming, and portions of western Missouri and northern New Mexico) did not reach double digits in any given quarter. From 2007 until the fourth quarter of 2008, both non-irrigated and irrigated cropland values rose by an average of about 17%. Other districts with a heavy agricultural composition experienced similar rises in farmland values. This surge in farmland values generated significant appreciation in wealth for farming operations that owned land. Commercial banks with sizable agricultural loan portfolios benefited from strong repayment rates.

Commercial banks also benefited from a jump in non-real estate lending activity prior to the financial crisis. In 2007, combine and four-wheel-drive farm tractor sales rose 15% and 22%, respectively. The trend continued in 2008, with further gains of 19% and 21%, respectively.

The 2008 financial crisis, however, significantly impacted agricultural credit markets. From the third quarter to the fourth quarter in 2008, average corn prices plummeted 35%. Average soybean prices fell 33% over the same time period. Weaker commodity prices caused farm incomes to drop 26% from 2008 to 2009. Whereas rising commodity prices and incomes drove loan repayment rates higher prior to the financial crisis, falling incomes drove repayment rates substantially lower throughout the crisis and recession. Growth in farmland values in the 10th District also slowed considerably and average values even contracted somewhat in the third quarter of 2009 for all types of farmland.

Deteriorating economic conditions and regulatory concerns throughout the 2008-2009 recession caused banks to tighten lending standards. Lower farm incomes created cash flow difficulties for some agricultural enterprises, causing loan repayment rates to fall. In an effort to maintain strong loan portfolios and ease heightened concerns of bank regulators, commercial banks began tightening lending standards by raising collateral requirements. As a result of tighter standards and weaker incomes, agricultural lending activity slowed throughout this recessionary period. After rising more than 20% each of the previous two years, farm tractor sales rose only 2% in 2009.

With the post-financial crisis recovery well underway in late 2010, the last three years have seen a tremendous boom in the U.S. agricultural sector. Despite some concerns about how long the boom will last, crop prices and farmland values have soared over the past three years. U.S. farmers have enjoyed near-record incomes during the latest boom, although livestock producers have recently endured steep losses due to persistently high feed and forage costs following periods of drought. Loan repayment rates have rebounded from their post-recession pace, particularly for crop producers, and have been hovering at historically high levels.

Despite dramatic improvements in agricultural credit conditions and relatively strong profits in agricultural bank loan portfolios, loan demand has remained soft. Accommodative monetary policy has pushed short-term interest rates nearly to zero. Federal Reserve large-scale asset purchases and quantitative easing have also driven long-term interest rates to record lows. These lower interest rates have led to record-low farm loan interest rates and strong competition for high quality farm loans. Flush with cash and high levels of wealth supported by surging farmland values, however, farmers have been reluctant to finance their operations with debt, even as commercial banks compete aggressively for new loans with plenty of funds available.

Surging commodity prices and farmland values appear to have accentuated a gap in agricultural credit markets between experienced farmers and young and beginning farmers. With less experience, typically smaller farms, and lower levels of overall net worth, young and beginning farmers present greater risks to commercial banks that balance risk with the potential for long-term returns. Higher volatility in agricultural commodity markets over the past several years may have compounded these risks. Rising land prices, combined with the need to provide high levels of collateral to compensate for greater risks, make the purchase of farmland difficult for young and beginning farmers. However, small businesses in other sectors of the economy also face difficulties financing large capital purchases, raising the question of whether a high percentage of land ownership is a tenable model for young and beginning farmers.

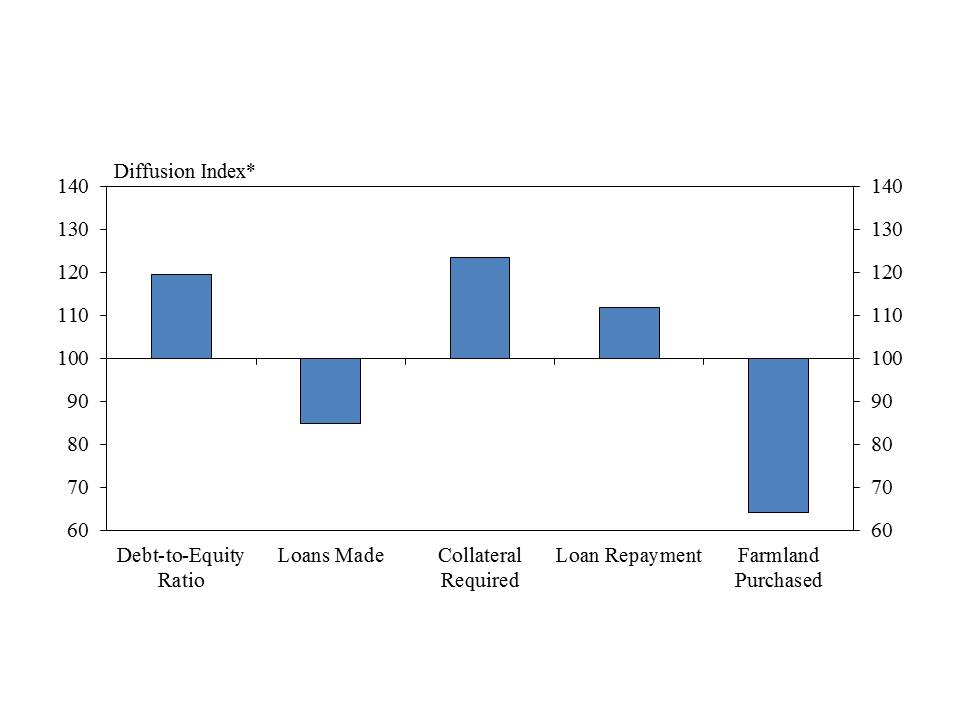

Along with less experience, young and beginning farmers typically have less farm equity. In 2011, farmers under the age of 35 held more than 20% less equity per farm than the average across all farms (U.S. Department of Agriculture (USDA), 2012). As a share of total assets, farm liabilities of these younger farmers were more than twice those of all farmers in 2011. As indicated in Figure 4, a recent survey of banks in the 10th Federal Reserve District shows that commercial bankers have also reported higher debt-to-equity ratios for young and beginning farmers compared with those of other farmers. Non-real estate debt is a primary contributor, and is about three times higher on average for younger farm operators when compared with other farms. Real estate debt presents younger farmers with higher debt burdens as well.

With lower levels of equity and fewer assets, young and beginning farmers are a greater risk for lenders. One of the primary concerns with respect to loan portfolios at commercial banks is the risk of default. Since 2010, farm incomes have been historically high. However, incomes are more limited for young and beginning farmers with fewer assets, making economies of size or scale difficult to achieve. Moreover, incomes are projected to decline over the next 10 years. The USDA currently projects net farm incomes in 2022 to be 26% below the forecast for 2013. Since they have less capacity to repay loans in the event of a downturn in incomes, it is not surprising that young and beginning farmers are perceived as a more risky group on average. A risk premium, in the form of higher interest rates or increased collateral, is consequently required from borrowers who present greater risks to compensate for potential losses through default.

Since 2006, grain markets have become significantly more volatile. From 1994 to 2006, there was just one quarter (the fourth quarter of 1996) when average corn prices swung in either direction by more than 30% from the previous quarter. Since then, there have been four such occurrences in half the time. Daily price volatility has also been 50% higher since 2006 compared with the average of the previous 12 years. Higher volatility—characterized by greater price fluctuations—results in more risk. This new era of greater volatility compounds the risk that young and beginning farmers already present to their lenders.

Credit markets and bankers are responding rationally by requiring higher levels of collateral and taking greater precautions when originating new loans. With large fixed costs involved in agricultural production, high collateral requirements present young and beginning farmers with a significant barrier to entry. As land prices continue rising, this barrier to entry is becoming even more pronounced. Many sources, including contacts at the Federal Reserve Bank of Kansas City (FRB KC), have indicated that young farmers often require assistance from family members to get started.

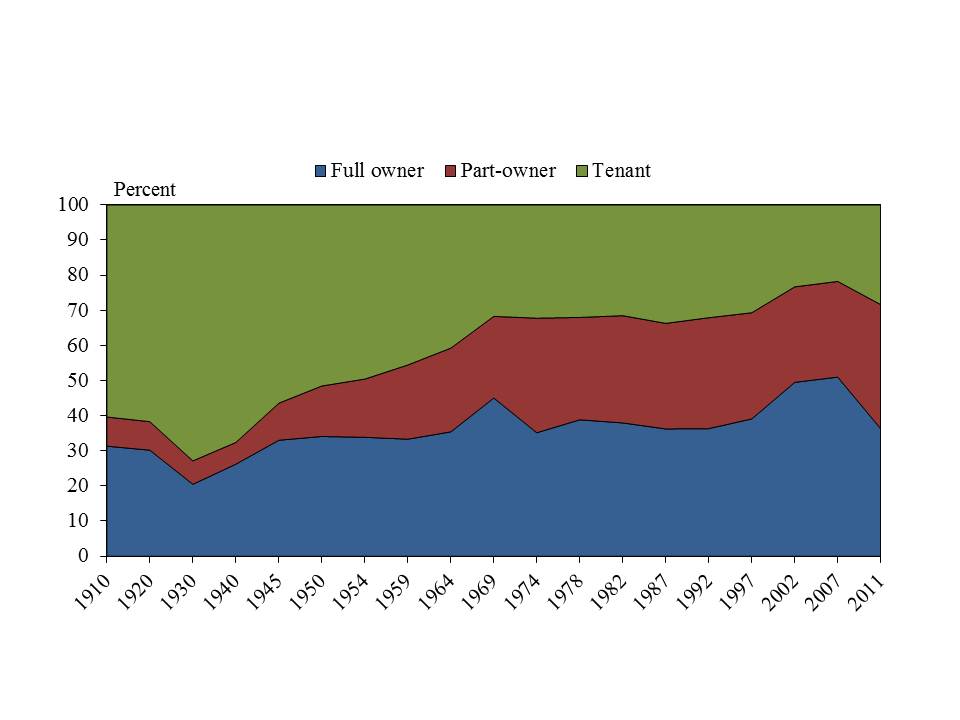

According to FRB KC contacts, young and beginning farmers struggle to compete in today’s farmland real estate market and are choosing to lease instead. The run-up in farmland values has made land unaffordable for many of these farmers, with fewer young and beginning farmers purchasing farmland. In contrast to the previous decade, an increasing share of young farmers is choosing partial ownership or lease arrangements when evaluating potential farm management strategies. As recently as 2007, 51% of farmers under the age of 35 fully owned the farms they operated (USDA, 2012). Throughout most of the 20th century, only 30% to 40% were full owners, as shown in Figure 5. By 2011, full ownership had dropped back to 36%. Renting assets, including land, could be emerging as a more important component of the business model for young and beginning farmers.

It should be noted that it is possible the share of land rented, rather than owned, by farmers under the age of 35 differs from the share of farmers who rent. In particular, large commercial farms may be renting a higher percentage of operated farmland, which would keep the share of land rented relatively lower.

In addition to high farmland prices, farm consolidation and delayed retirement compound the difficulties young and beginning farmers face. Although relatively stable over the past 20 years, the number of U.S. farms has fallen from more than six million a century ago to just over two million today. Farm operations have become significantly larger on average, taking advantage of economies of size and scale. Thus, today’s new farmers face the additional challenge of needing to acquire even more land to be competitive in modern agriculture. However, many older farmers are delaying retirement. Not only are they often reluctant to sell their land, but ageing farmers are also frequently reluctant to pass on farm management responsibilities, limiting the availability of land for either purchase or rent.

Similar to young and beginning farmers, small businesses in other sectors of the economy also face tight credit conditions. In a recent survey of small businesses conducted by the Federal Reserve Bank of New York, only 13% of loans were approved for the full amount requested (Federal Reserve Bank of New York, 2012). Moreover, insufficient levels of collateral accounted for 28% of loan denials. In a 2012 survey conducted by the National Small Business Association (NSBA), 31% of respondents indicated a reliance on friends and family for financing. These examples of tight credit and a reliance on family members in small businesses echo the comments of agricultural bankers in surveys conducted by FRB KC.

Although many farmers seek to own the land they operate, leasing may be a more viable option for young and beginning farmers. The Equipment Leasing and Finance Association reports that approximately 80% of U.S. companies lease some or all of their equipment (Entrepreneur Magazine, 2012). With farm incomes expected to drop in 2014, and with some concerns about the sustainability of soaring farmland prices, leasing a larger share of land might also be a less risky proposition for young and beginning farmers, notwithstanding the perception of risk from a creditor’s perspective. Today’s young and beginning farmers may need to recognize the tools and strategies being used in other sectors of the economy and adopt those that have proven effective. Although various federal and state policies currently offer support for young and beginning farmers to purchase land, these policies may also be better geared toward leasing, particularly if fixed costs in agricultural production continue rising.

Agricultural credit terms and conditions for young and beginning farmers are different from those for experienced farmers. Terms of credit are different because this group of new farmers presents greater risks to commercial lending institutions. As might be expected, banks are responding by requiring higher levels of collateral. In addition to greater collateral requirements, soaring farmland values make entry more difficult for young and beginning farmers, challenging the conventional business model of land ownership in agricultural production.

Greater risk, higher land prices, and tighter credit markets for young and beginning farmers point to the reality that owning a high percentage of the land operated may not be a tenable path in transitioning to a new generation of farmers. Similar to small businesses in other sectors of the economy, leasing assets may be a more viable option. A shift in farm management strategies toward leasing farmland will require refocusing and refining the skill set needed to compete in modern agriculture. This skill set includes various aspects of long-term planning, marketing, and negotiating in rental markets. For family farms, stronger communication surrounding plans for succession and including younger farmers in management responsibilities earlier would help foster these valuable skills. Federal, state, or local policies could also be designed with these skills in mind, recognizing the need for a smooth transition to a new generation of U.S. farmers.

Agricultural Finance Databook. 2013. Federal Reserve Bank of Kansas City. Available online at http://www.kansascityfed.org/research/indicatorsdata/agfinance/.

Entrepreneur Magazine. March 3, 2013. Available online at http://www.entrepreneur.com/article/225959

Federal Reserve Bank of New York. 2012. Small Business Borrowers Poll. Available online at http://www.newyorkfed.org/smallbusiness/2012/

National Small Business Association (NSBA). 2012. Small Business Access to Capital Survey. July, 2012.

Survey of Agricultural Credit Conditions. 2013. Federal Reserve Bank of Kansas City. Available online at http://www.kc.frb.org/research/indicatorsdata/agcredit/.

U.S. Department of Agriculture (USDA). 2012. Agricultural Resource Management Survey. Available online at http://www.ers.usda.gov/data-products/arms-farm-financial-and-crop-production-practices.aspx#.UcnhitijFWM

U.S. Department of Agriculture, Census of Agriculture. Available online at http://www.agcensus.usda.gov/Publications/index.php.