Once dominated by traditional and small-scale production systems with little regulation, Mexico's pork industry now includes modern, vertically integrated production systems and federal inspection of packing and processing plants. Recent structural changes have resulted in three distinct segments within the production and processing sectors as the industry works to adjust to international and domestic demand for better product quality, stricter sanitary practices, and increased supplies yet continue to meet the needs of low-income consumers. As the structural changes continue, the industry faces several challenges that will affect its ability to become both internationally and domestically competitive. To meet these challenges, the Mexican government is faced with decisions about implementing and enforcing regulations and providing incentives to encourage continued development and best serve domestic consumers. Background

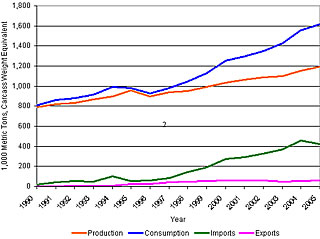

The structure of Mexico's pork industry has changed significantly in response to the implementation of the North American Free Trade Agreement (NAFTA), changes in consumer demographics, and the industry's desire to increase pork exports. The trade liberalization allowed under NAFTA has played a major role in spurring the rapid expansion of pork imports into Mexico to help keep pace with steadily growing demand (see Figure 1). Many of the structural changes to Mexico's pork production and processing sector have taken place since the phase-in period of NAFTA began in 1994. During this period, Mexican pork producers have worked to meet increasing domestic demand for pork and better pork quality and to meet competition from imported pork and the poultry meat products that substitute for pork in many processed products. Processed products are popular in Mexico because of flavor; convenience; the range in quality and price that makes them affordable to many consumers; and the perception of many consumers that cooked, processed products are safe. Imports of live U.S. slaughter hogs have also been an important component of Mexico's pork industry trade, although numbers have been highly variable. Between 1996 and 2005, exports of U.S. slaughter hogs to Mexico ranged between a low of 14,700 head (1997) and a high of 201,500 head (1998); in 2005, exports totaled 130,100 head.

Pork has always been an important part of the Mexican diet, but a growing middle-income class, greater urbanization, overall population growth, and the greater availability of imported pork due to NAFTA have helped drive the sharp increase in pork demand. In 2005, per capita pork consumption reached 33.1 pounds, a 30.4% increase since 1995 (SAGARPA, 2006). Between 1990 and 2005, domestic pork production increased by 50%, but total consumption increased even more rapidly (see Figure 1). Along with the increase in pork demand, a growing number of Mexican consumers are demanding higher quality and greater safety in pork products. At the same time, a significant portion of Mexico's population does not have access to retail outlets that sell pork produced under sanitary conditions and can afford only the lowest-quality, lowest-priced pork.

During this period, the Mexican pork industry has worked to increase exports, although this trade is relatively small compared with import volumes (Figure 1). Although Mexico is a net pork importer, the Mexican pork industry is competitive in providing some labor-intensive cuts that require trained labor to produce and some high-value-added cuts to export markets. Japan and Mexico signed a free-trade agreement in 2004, and exports under this agreement began in April 2005. During 2005, Mexico exported 46,906 metric tons (carcass weight) of pork to Japan, the largest export market for Mexican pork (USDA, 2006). In contrast, Mexico exported a mere 11,663 metric tons (carcass weight) of pork to the United States.

Meeting international standards for the product quality and sanitary practices required to export pork has further encouraged greater integration and efficiencies in the production and processing sectors. But, as a large net importer of pork, Mexico must increase production and/or imports to replace any exported pork if domestic demand is to be met. To increase domestic production and compete with imported pork, the industry will need to continue to expand production from its vertically integrated systems.

The desire to export has also required that the Mexican industry improve sanitation practices in the segments of the production and processing sectors involved in exporting. Sanitary and phytosanitary (SPS) standards in the United States and elsewhere have limited live hog and pork exports from Mexico. For example, U.S. food safety import regulations require that pork and pork products imported from Mexico meet all the same food safety standards applied to similar products produced in the United States. The efforts to upgrade slaughter and processing facilities to meet these standards are discussed in the following section. Another important effort has been the attempt to eradicate export-limiting swine diseases.

Classical swine fever (CSF) prevented live animal and pork exports until Mexico was able to regionalize CSF-free states. Under regionalization, the Mexican government recognizes 13 Mexican states as CSF-free. In addition to CSF-free areas, Mexico has two other CSF zoo-sanitary areas: eradication areas and control areas. In the eradication areas, located in Central Mexico, vaccination for CSF is prohibited; producers rely instead on depopulation and restrictions on movement of live animals should an outbreak occur. In contrast, CSF is considered endemic in the control area of Mexico, located in southern Mexico. Here, vaccination is used continuously to reduce pig production losses. Movement of live hogs and meat between zones is regulated or restricted, which has influenced industry development and limited export potential for producers and processors in some states.

The need to meet international sanitary standards and competition from imported pork has helped shape government policies that are resulting in improved pork quality and safety. However, government and industry resources are limited and modernization has not reached all segments of pork production and processing. As the production and processing sectors continue to modernize, the Mexican pork industry faces significant challenges because of differences in the product quality required by a more modern pork distribution system and export markets, in contrast to that accepted and preferred by many domestic consumers.

Production and Processing Systems

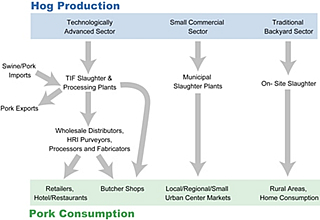

Production and processing of hogs and pork products in Mexico are undergoing important structural changes, driven by adjustments in the domestic market and international rules of trade. Modern, technologically advanced production and processing systems have emerged, and rapid urbanization has shifted opportunities toward more integrated marketing channels. However, the modern sector coexists with a more traditional domestic sector, and today three distinct sectors exist in the Mexican pork industry. Technology, resources, and location differentiate the three live animal production systems and the unique pork product distribution and marketing channels supplied by each (see Figure 2).

Live Hog Production

Hog production systems in Mexico can be separated into three types: technologically advanced, small commercial (semi-technically advanced), and traditional backyard. These systems are differentiated by the level of technology employed, degree of vertical integration, and quality of hogs produced (see USDA, 1999, for more details; see Batres-Marquez et al., 2006, for full references on all data).

Firms that operate technologically advanced production systems raise hogs at specialized sites, use advanced breeding methods, and implement strict animal health regimes, such as vaccination against disease and multi-site production systems. Most of these vertically integrated firms control the entire process, from hog production through pork distribution. The hogs are fed milled feeds and balanced rations, and this production system consistently produces the highest quality hogs of the three systems. These operations have shown the greatest expansion in response to increased pork demand in Mexico, and this expansion is expected to continue in response to an overall increase in demand, as well as demand for better quality and greater safety.

Small commercial operations produce fewer pigs per unit than do the technologically advanced producers. The small commercial producers may use breeding stock similar to that of the technologically advanced firms but lack the animal health controls and marketing systems used by the technologically advanced producers. These producers are less likely to feed balanced rations and cannot consistently produce hogs of uniformly higher quality. In response to the need for increased efficiencies to increase pork supplies and to compete with the increase in inexpensive imports allowed under NAFTA, many of these small commercial producers have exited the industry because of their inability to produce animals more efficiently and to meet increased quality standards, such as weight ranges, that are required by many live hog buyers. As a result, the scale of production has increased and the industry has become more highly concentrated and integrated, and this trend is expected to continue.

The reduction in small commercial production and the expansion of technologically advanced production have taken place alongside continued production using traditional backyard methods. Traditional backyard production is still quite common and found throughout the rural and semi-urban regions of the country. These traditional hog production systems are used in areas where there are few or no formal commercial channels. The hogs normally are fed low-quality feedstuffs and are of the lowest quality among the production systems. This production segment has declined, but economic and geographic limitations that prevent a large number of domestic consumers from obtaining pork from the other segments mean that this segment will remain part of the pork industry for the foreseeable future.

Pork Slaughter and Processing

As with live hog production facilities, slaughter and processing systems can be separated into three types: federally inspected, or "Tipo Inspección Federal" (TIF), plants; municipal plants; and traditional on-site slaughter. The facilities differ mainly by the degree of technology used, the size of capital investment, and the services the plants offer.

The TIF slaughter and processing plants use state-of-the-art technologies and have the highest sanitary standards and most advanced technological processing levels in Mexico. These plants are certified and federally inspected by the National Service of Health, Innocuity, and Agro-alimentary Quality (SENASICA) of the Agricultural, Livestock, Rural Development, Fishery, and Food Secretariat (SAGARPA). In addition, some of Mexico's TIF plants are HACCP-certified by the USDA Food Safety and Inspection Service, and some are individually approved by the Japanese government to export pork to Japan. TIF plant services include slaughtering, carcass handling, packaging, refrigerated storage, and fabrication of processed products (for example, hams and salamis) for both domestic and imported pigs and pork. An individual TIF plant may provide slaughter services only, slaughter and fabrication/processing services, or fabrication/processing services only.

TIF slaughter plants generally obtain hogs from technologically advanced, vertically integrated production systems that produce animals raised to meet high quality standards for the higher-end domestic market and for international markets. Also, the slaughter of imported hogs is restricted to TIF plants. TIF fabrication/processing plants use raw materials from TIF slaughter plants and imported products. The products from TIF slaughter and fabrication plants are mainly sold in large urban areas, and a small percentage is exported. Only pork slaughtered in TIF plants can be exported, once the importing country has accredited that the TIF plant complies with its sanitary controls.

TIF plants have existed in Mexico since 1947, but use of these plants has been increasing. A 1994 law on animal health requires that all new slaughter and meat plants built in Mexico be TIF plants. In addition, many companies are renovating existing plants in order to obtain TIF certification. In 2005, there were 95 TIF slaughter plants in Mexico. TIF pork plants processed 5.1 million pigs, a 25.9% increase over the number of hogs processed in 1998. TIF pork slaughter operations are concentrated in four states. In 2004, 43% of all hogs slaughtered in TIF plants were slaughtered in the state of Sonora, 21% in the state of Mexico, 14% in Guanajuato, and 11% in Yucatan. Eight other states accounted for the remaining 12% of TIF slaughter (Conferacion Nacional de Organizaciones Ganaderas, 2005).

As the number of TIF plants has increased, so has the share of hogs slaughtered in these plants with respect to total hogs slaughtered in Mexico. In 1991, only 11% of all slaughtered hogs were slaughtered in TIF plants, whereas in 2005, about 36% of all hogs were slaughtered in these plants. However, despite the general shift of production to the more modern processing sector, many TIF plants are working below their capacity levels—about 55% to 60% capacity according to one estimate. Because imported live hogs must be slaughtered in TIF plants, the underutilization of slaughter and processing capacity in Mexico encourages more live hog imports when market conditions such as U.S. hog prices and currency exchange rates are favorable.

Despite the incentives to use TIF facilities, several factors limit their use and segregate the market between the TIF plants and municipal slaughter plants, especially with regard to small commercial producers. First, shipping of meat in refrigerated containers makes meat transported from TIF plants to retail and consumer markets relatively more expensive than meat produced, processed, and marketed through local market channels. A second factor that limits the use of TIF plants is their geographical location. Even though TIF plants are located near major hog production areas, they are inaccessible to many producers dispersed throughout the country because of high transportation costs and other logistical problems. Third, many small producers do not meet the animal quality standards of the federally inspected slaughter plants.

In contrast to TIF plants, municipal slaughter plants offer limited services, namely, slaughtering and carcass handling (cutting). These plants do not follow strict sanitary controls such as appropriate refrigeration, yet they are the main processors of hogs in nonmetropolitan areas of the country. According to some estimates, there are 866 municipal slaughter plants located throughout Mexico. Most of these plants are old and have not received proper maintenance. They lack the equipment and resources necessary to dispose of by-products properly and therefore are a source of contamination, particularly groundwater contamination (Lastra Marin and Peralta Arias, 2000). This segment of the slaughter industry is expected to decline as more producers use TIF plants for slaughter and processing, but the decline likely will be slow. Mexico's small commercial operators have traditionally sent their animals to municipal and/or private slaughterhouses where slaughter costs are about 30% to 40% lower than those of the TIF slaughter plants. These lower costs are passed on to consumers, at least in part, through lower prices of meats sold in local, regional, and small urban center markets.

A sizeable proportion of producers in Mexico still use traditional on-site slaughter. These slaughter practices correspond to a traditional/ancestral slaughtering system practiced even before the Spanish colonization of Mexico. Although the share of hogs slaughtered under this system has fallen, about 36.1% of hogs were slaughtered on site in 1997, mainly in rural areas. The pork harvested under this system is used mainly for family (subsistence) consumption, although some is sold fresh for local domestic consumption. This system remains an important source of pork for many consumers because of its low production cost, low price, and the preference by some consumers for freshly slaughtered meat.

Government Incentives for TIF Production

As noted, slaughter and fabrication in TIF plants are more expensive than in municipal plants or on-site slaughter. To support the modernization of the meat industry, the Mexican government has provided subsidies to producers to encourage slaughter and processing at TIF plants and at registered plants in the process of becoming certified as TIF plants. In 2003, for example, producers received approximately $7 per head (on average) for hogs slaughtered in TIF plants to cover the higher cost of meeting hog quality standards of TIF plants. In 2004, producers received about $4.63 per animal to cover the cost differential. Hogs slaughtered under the subsidy program must be five to six months of age, weigh 85 to 120 kilograms, and be produced in Mexico. Programs like this are designed to promote the use of TIF plants, a key component to expanding Mexico's export of pork and to improving the quality and safety of fresh pork in the domestic market.

Challenges to the Industry

Both expanded domestic production and imports have been used to meet the rapid increase in Mexico's consumer demand for pork. Rising consumer incomes, more consumer information about food safety, and more efficient distribution will help drive demand for pork produced in TIF plants and increase consumer willingness to buy packaged (rather than freshly butchered) meats. These changes will, in turn, continue to drive ongoing structural changes in the domestic pork production, slaughter, and processing sectors.

Key to the continued development of a more modern and integrated production and processing sector is the increased domestic movement of live pigs (brought about through improved animal health and disease control), as well as channeling more pigs and pork through the modern sector. Such changes will require improvements in infrastructure (for example, new and improved roads and cold chains) to expand the use of TIF plants and to encourage the development of marketing channels that support high-quality products. Such changes will also require continued government regulatory and financial support.

The Mexican government's scarcity of financial resources relative to the country's needs will force the government to make choices about the most effective use of scarce resources for future development of the pork sector. The three levels in the industry's production and processing systems are likely to remain a part of Mexico's pork industry, although the proportion of hogs produced and slaughtered in each will gradually change. In the near term, Mexico's industry can take advantage of different consumer markets through exports of high-valued cuts. However, given that Mexico's export market for pork is small and importing countries certify only a portion of TIF plants for export, policies that encourage increased exports may limit the overall industry's potential to increase quality and safety in the domestic market. Government policies that encourage industry-wide improvements in quality and safety could reasonably be expected to help bring about the long-term changes necessary to support a pork industry that benefits all consumers.

Acknowledgment

The authors thank all the reviewers for helpful comments, and are especially grateful to one reviewer for suggestions on the organization of material.

For More Information

Batres-Marquez, S.P., Clemens, R., & Jensen, H.H. (2006). The changing structure of pork trade, production, and processing in Mexico. MATRIC Briefing Paper 06-MBP 10, Midwest Agribusiness Trade Research and Information Center, Iowa State University. Available online: http://www.card.iastate.edu/publications/DBS/PDFFiles/06mbp10.pdf (Accessed 11/29/06).

Conferacion Nacional de Organizaciones Ganaderas. (2005). Informacion economica pecuaria. Numero 14, Mexico. Available online: http://www.cnog.com.mx/Estudios/Indicadores/INFOPECO14.pdf.

Lastra Marin, I. de J., & Peralta Arias, M. de los A., eds. (2000). La producción de carnes en Mexico y sus perspectivas 1990-2000. Available online: http://www.sagarpa.gob.mx/Dgg/estudio/carne.pdf (Accessed 8/31/06).

Secretaria de Agricultura, Ganaderia, y Desarrollo Rural Pesca y Alimentación (SAGARPA). (2006). Situación actual y perspectiva de la producción de carne de porcino en Mexico 2006. Available online: http://www.sagarpa.gob.mx/Dgg/estudio/sitpor06.pdf (Accessed 9/26/06).

United States Department of Agriculture (USDA). (1999). Mexico's pork industry structure shifting to large operations in the 1990s. Agricultural Outlook. Washington, DC: Economic Research Service.

USDA. (2006). Mexico Livestock Annual. MX6068. Washington, DC: Foreign Agricultural Service. Available online: http://www.fas.usda.gov/gainfiles/200608/146208819.pdf (Accessed 11/29/06).

|

|

Other articles in this theme:

|

|