Milk production in the United States has become increasingly concentrated among fewer herds. This consolidation has, as in other on-farm agricultural sectors, long been recognized (e.g., Drabenstott, 1994; MacDonald, Cessna, and Mosheim, 2016). According to USDA milk production reports (LMIC, 2018), the number of licensed dairy herds in the United States declined from 45,344 in 2014 to 40,219 in 2017, a 4% annual rate of decline over the period.

Large and small farms are, in aggregate, different in their output, production costs, and quality metrics. Significant scale economies exist in dairy production (Mosheim and Knox Lovell, 2009): larger herds are generally better positioned to attain quality standards as reflected by somatic cell count indicators (Norman, Walton, and Dürr, 2018) and technical inefficiency is a factor in exit decisions (Dong et al., 2016). Given the obstacles faced, smaller dairy farms generally have difficulty competing with larger farms unless they receive higher prices in specialty milk markets or have low opportunity costs of operator time.

Less well understood are the investment dynamics that precede both exit and expansion. In this article, we provide a snapshot of the dairy industry based on a survey of dairy farmers in a market environment of multiple continuous years of low milk prices and low milk profit margin. The survey allows us to analyze how farm size relates to dairy farmers’ views of industry outlook and their decisions regarding expansion or contraction of herd size, labor, and capital as the industry adjusts to market pressures and emerging technological opportunities.

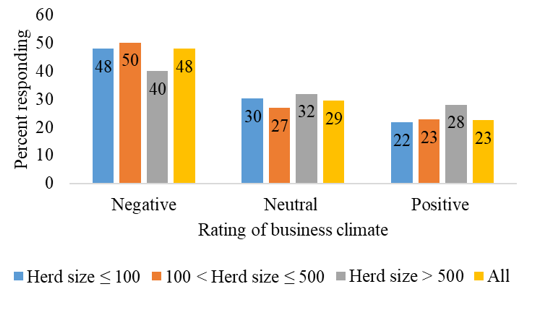

Notes: Negative includes those responding “negative” or “very negative” on the survey.

Positive includes those responding “positive” or “very positive.”

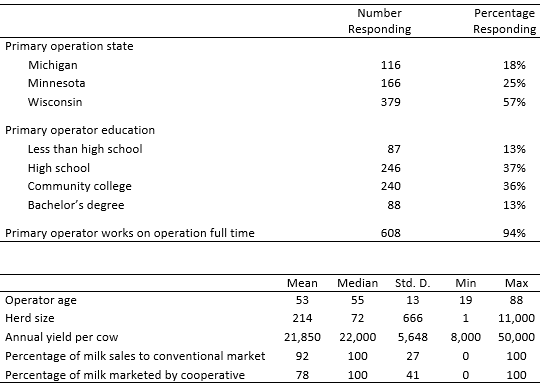

We conducted a dairy producer survey between May and September 2017 that targeted three U.S. Great Lakes states: Michigan, Minnesota, and Wisconsin. In 2017, these states accounted for 24% of U.S. milk production (5% Michigan, 5% Minnesota, and 14% Wisconsin) and 23% of the U.S. milk cow herd (LMIC, 2018). We designed the survey, which was administered by Michigan State University’s Office for Survey Research. The survey generated 710 completed questionnaires, of which 660 (112 web and 548 mail) were usable for this analysis. To put these numbers in perspective, there were about 16,300 registered dairy farms in the three states. Table 1 reports summary statistics for our sample.

Consistent with the relative sizes of the dairy industries in each state, 57% of the sample was from Wisconsin, 25% from Minnesota, and 18% from Michigan. Average herd size was 214 cows, but data were positively skewed, with a maximum of 11,000 cows. The majority of respondents, 66%, had herds with fewer than 100 cows, while 26% of herds had 101–500 cows, which we define as a medium-size herd. Only 8% of respondents fell in our large herd category, which we define as more than 500 cows. Most milk marketed from the sample went to conventional commoditized milk markets, but 55 farmers stated that most of their milk was sold in the organic market. Nearly 80% of the milk produced by our sample was marketed through a co-operative. Average yield per cow was 21,850 lb, 5.8% smaller than the U.S. 23 state average of 23,204 (LMIC, 2018).

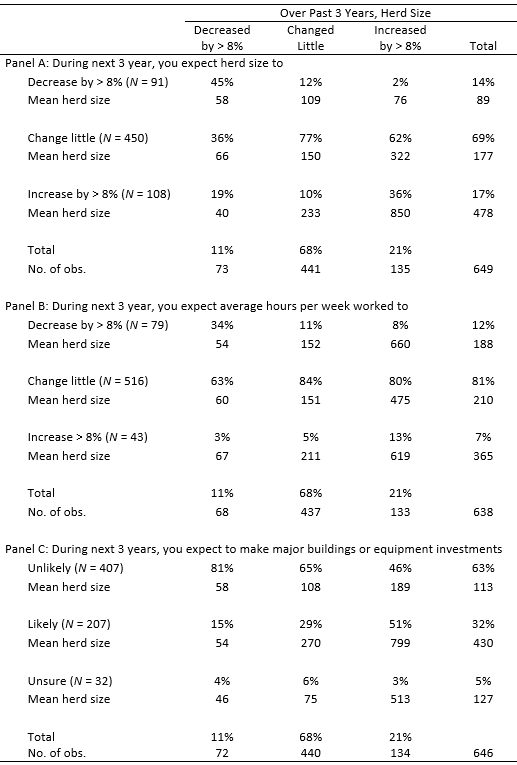

One question in the survey asked, “How would you assess the current business climate for milk production in your state?” Not surprisingly, given prices received at the time, views were generally pessimistic, with nearly half of respondents indicating negative views (Figure 1). Overall, respondents with small and medium-sized dairy herds were more pessimistic than those with larger herds. Nearly 30% of the sample stated they were neutral on the current business climate for milk production in their state, while less than one-fourth were positive. Further questions asked about herd size choices over the previous 3 years, intended herd size, enterprise employment, and building/equipment investment intentions over the next 3 years. Table 2 summarizes the responses.

Despite a challenging milk price situation and overall negative outlook, 21% of farmers among our survey respondents had increased herd size by more than 8% during the previous 3 years, while 17% expressed an intention to increase herd size by more than 8% during the subsequent 3 years. More responding farmers had increased herd size than had decreased herd size during the previous 3 years (21% vs. 11%). Of course, survivorship bias, in the form of nonresponse by recently exited farmers, inflates the first and deflates the second of these numbers. Looking forward, more farmers intended to expand than to contract herd size during the ensuing 3 years (17% vs. 14%). In general, expanding operations are usually larger (Table 2). There is a strong positive temporal autocorrelation in herd expansion/contraction choices (Panel A). Few farmers expect to expand hours worked, but the connection between these expectations and herd size trajectories is weak (Panels A and B). However, intended investments in buildings and equipment correlate strongly with herd size trajectories (Panel C). Overall, it appears that those farmers expanding herd size are underpinning this expansion through further capital investments and not through increased use of labor (Panels B and C).

As reported in Panel A, we interpret those who have contracted or intend to contract as very likely to leave dairy farming. Of the five categories in which the producer indicated either past or future intentions to decrease herd size (first column and first row of Panel A), only one category has mean herd size in excess of 100 cows. Respondents in this category saw little change over the prior 3 years and also expected to decrease in the 3 years to follow.

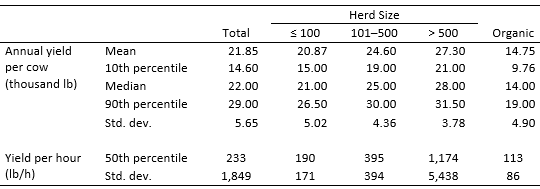

Table 3 shows that farmers with larger herd sizes were significantly more efficient (as measured by production per cow and by production per hour of labor). Median annual production per cow was 21,000, 25,000, and 28,000 lb for farms with small, medium, and large herds, respectively. We also considered output per unit of labor input. Specifically, we divided total annual milk production by total annual labor input. The operator and operator’s family provide most of the labor on smaller operations, while labor was mostly hired on large operations. Table 3 also indicates that median quantity of milk per unit of labor on large farms was about 5 times that of small farms. These production efficiency advantages are a driving factor in the continued consolidation of the industry.

Tables 2 and 3 point to two trends: One is diverging trajectories for different dairy herd scale categories in the three Great Lakes states. Data in Table 2 presage the eventual exit of most operations with smaller herd sizes, stasis among most operations in the middle, and future expansion concentrated among larger operations. Those middle-tier farms may not be safe, however. While we cannot find evidence that Earl Butz, the controversial former Secretary of Agriculture under Richard Nixon and Gerald Ford, ever asserted, “Get big or get out”—a phrase indelibly linked to him—he held firmly to the belief that farms that were not growing would eventually exit. Possible constraints on expansion for dairy farms of all sizes vary by location and can take many forms, including limited access to feed and forage, constricted local processing capacity, and manure disposal challenges. All else equal, however, as unit costs decline with scale, medium-sized operations may be unable to generate cash flow or access the loans needed to expand and lower cost structures.

The other trend is bias toward capital, rather than labor, in intended investments. To understand this tilt, some reflection on the investment environment is in order. One point, made previously by Sumner (2014) but still true as of writing, is that real capital costs are at historic lows, whereas all-inclusive labor costs have stagnated. Furthermore, production agriculture has become an increasingly technical field, requiring protracted human capital investments in skill development. Forming enduring employment connections with hired help interested in and well-positioned to acquire the requisite skills has been a continual source of woe for many operators.

A related point, also made by Sumner (2014), is the growing need for technical managerial skills increasingly similar in form to those valued in general economy businesses. In the case of dairying, larger enterprises require the financial, logistics, personnel, information technology (IT), and marketing skills associated with supporting what amounts to a small manufacturing plant. Beyond that, strong technical understanding of such matters as genetics, animal physiology, nutrition science, and microbiology present operators with further challenges. Table 4 reports community college or higher degree attainment by operation scale for different principal operator age cohorts. Those operating larger herds have generally had more extensive formal education. If the occupation is to compensate for the educational investments made and compete with available alternative occupations, then these managerial skills need to span an adequate breadth of resources.

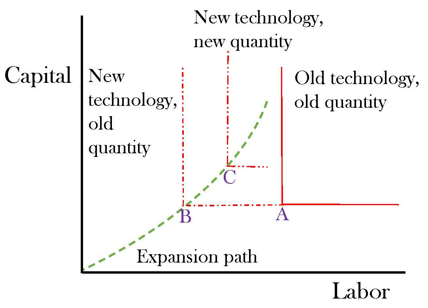

We turn now to the tilt in investments made. Figure 2 illustrates a stylized characterization of the assembled evidence. For simplicity, we assume in the figure that labor and capital combine in fixed proportions (i.e., as a Leontief technology). That is, for each capital investment level, there will be one corresponding amount of labor input to cost-effectively generate a milk production level. In an initial technology, the optimum (labor, capital) combination is given as point A, where the equilibrium profit-maximizing output is given as “old quantity.” Then a new labor-saving technology shifts the vertical arm inward to intersect the horizontal arm at point B. For reasons that we will elaborate on shortly, the expansion path (i.e., the green dashed line) for the new technology is assumed to bend from the origin toward the capital axis so that the capital-to-labor ratio increases as a firm expands production. Given lower costs upon moving from input combination A to combination B, the producer will find it optimal to expand along this path, and equilibrium settles at point C. As depicted, this point involves greater capital use and less labor use than at point A, although nothing precludes point C from being above and to right of point A. Our survey data reveal that for the three Great Lake States, production expands with use of more capital but no more labor.

Unit labor costs in milk production come in many forms. In recent times, insurance, administration and documentation cost categories have assumed increased importance as costs of employment. While smaller farms may retain comparative advantages in some cost categories, larger farms will likely be better able to gain favorable terms when providing insurance and can more readily justify the administrative costs of hiring and retention. Nonetheless, the increasing costs of labor in general combined with the growing availability of less physically challenging jobs have led producers to substitute capital for labor.

The history of agriculture is replete with labor-saving innovations, but labor has retained its worth in large part because it is more flexible than capital inputs when dealing with weather and biological uncertainties. The advent of confinement and developments in animal physiology, pharmacology, and genetics have gradually promoted process controls in ways similar to that in which technology developments led the blacksmith’s forge to be replaced first with foundries and then with factories. When inputs are uniform then stationary, pre-set machines can more readily be used to meet animal needs and harvest produce. Farmers sought cows with similar genetics and fed them common rations so that housing, feeding, and manure management investments were well-adapted to all and labor-substituting investments could expand more deeply into production operations. Similarly, investments that limit nature’s encroachments into production also favor the substitution of capital for labor, whose advantage in addressing these encroachments has assumed reduced value. We will discuss shortly how more recent innovations may have changed this demand for uniform inputs.

By and large, capital investments have significant fixed cost components. Sources of these fixed cost components include installation costs and the human capital investment that accompanies a new technology. To the extent that uniformity-enhancing technologies generate opportunities for on-farm capital investments, they will also tend to increase production scale (Hennessy and Wang, 2012). To the extent that more uniform on-farm inputs generate more uniform farm-gate outputs in terms of milk constituents, uniformity-promoting technologies may have similar effects in processing. Consistency in farm-gate milk outputs will generate higher yields during downstream physical and biochemical processing. Lower unit costs in processing will in turn enhance incentives to append further processing steps and to articulate product markets. As demand grows for highly processed dairy products, investment signals will guide firms toward adopting more of these uniformity-enhancing on-farm technologies at the expense of labor, possibly increasing farm-level fixed costs.

A wrinkle in this line of thought is that recent IT innovations have allowed for adaptation even in the face of non-uniformities, as in individualizing feeding regimes and adjusting for weather conditions. The expanding role of information in capital intensive animal agriculture has long been recognized (see, e.g., Boehlje, 1996), but penetration has been steady and not drastic. For certain applications, our view is that, as of 2018, adoption thresholds are being reached that suggest thicker markets, lower prices, and more reliable performance for many technological advancements in dairy. Many of these will become essential technologies on competitive dairy farms. Critical technologies to substitute for the non-uniformities that humans so capably manage are fast computing, laser guidance, electronic sensors, and cheap chemical diagnostics suitable for rough conditions. Robotic milking machines, for instance, provide low-stress, cow-specific udder washing and milking and also real-time analysis of milk before it enters bulk tanks. The machines are animal-welfare friendly in the sense that the cow partly chooses her own milking schedule.

Interestingly, and by contrast with the automated feeding systems that are now entering use on larger farms, robotic milking machines first found a niche among smaller farms in continental Northern Europe and only began to gain acceptance among larger farms around 2017. The more enthusiastic adoption for smaller herds may be because the hired labor input comes with scale economies and also because, in comparison with paid laborers, smaller owner–operators have the capacity and incentives to work with the robotic machine. Furthermore, versions of the technology are portable and readily scale up or down. This scaling observation underscores a cautionary note about the presumption that capital investments universally promote larger production scale. As an innovation matures, thoughtful innovation and, even more so, reliability can lead to smaller, more flexible equipment, just as the personal computer replaced the mainframe in most office uses. Many smaller operators in food and beverage markets, including brewing, have found opportunities to scale down capital inputs to efficiently produce the volumes that a highly differentiated market will bear.

As Sauer and Latacz-Lohmann (2015) noted, the wealth of information that such sensor-intensive milking, housing, and feeding system instruments generate warrants emphasis. While this class of machines substitutes for adaptable physical labor, it also generates potential premiums for adaptable management inputs. Furthermore, the information becomes more valuable in large herd settings because cows bear electronic tags. In larger herds, individual records can be more reliably compared with reference benchmark records for such purposes as feed adjustments, lameness detection (e.g., through monitoring hoof fall data on a metal plate), mastitis detection and precise diagnosis (e.g., through monitoring quality and flow from each quarter), estrus detection, and culling decisions. As has also become true with precision field-cropping technologies, informal experimental approaches to evaluating production practices are enabled and producers are accumulating privately held knowledge banks for the purposes of developing operational rules of thumb. These producers generally use formal research findings as just one, typically minor, point of guidance for their decisions.

In light of its deepening role in production and service sectors, macroeconomists are increasingly concerned about the economy-level impacts of automation on labor demand. One recent insight by Acemoglu and Restrepo (2018) is to replace factor-augmenting views of how IT innovations affect factor productivity with a task-focused view that better reflects empirical evidence on how labor demand is affected by automation. They model labor and capital as perfect substitutes in completing specific tasks but allow how these tasks aggregate to determine factor interactions. When more menial tasks are more amenable to programming, then these will be automated first, labor share in output will decline, and demand for capital will increase. The approach emphasizes automation’s value in factor-saving and also readily admits insights on bias in how factors are saved. The framework resonates well with much of what is happening on dairy farms. However, the models are silent on how these technologies shift demands for managerial cognition. Measurement and real-time adaptation activities are less necessary, but opportunities have opened up for assessing and processing the emerging large volumes of data recorded during production. A gap in the literature is that current economic models omit roles for automation in dynamic learning about production processes. As currently posed, this class of models can provide only a limited set of insights into how automation is reshaping dairy milk production.

When margins are tight in a commoditized market with innovative input providers, the need to be cost competitive is intense. Given cash flow realities and technological scale economies, a point may come when the competitiveness problem resolves to either expanding or exiting. We report survey findings on the views of U.S. Great Lakes state milk producers regarding their difficult production environment and how they are struggling to adapt. Many are in the process of exiting, while others have committed to expand as a cost management strategy. The expansion will favor capital inputs over labor inputs so that employment on the remaining farms will not notably increase and overall on-farm employment in the sector will decrease. In many senses, features of this trajectory should be familiar. For instance, 18th-century textile manufacture was a very labor intensive, rural, small-scale activity. The processes involved lent themselves to automation, and indeed the Jacquard loom’s control system inspired the first rumblings of computational science. On-farm milk production is only partly down the path on which a reductionist scientific analysis of its parts may generate technologies that both reduce costs and open possibilities for further innovation. To quote Disney’s Peter Pan, “All this has happened before, and it will all happen again.” But this time it is happening in milk production.

Acemoglu, D., and P. Restrepo. 2018. “Modeling Automation.” American Economic Review 108(May):48–53.

Boehlje, M. 1996. “Industrialization of Agriculture: What Are the Implications?” Choices 11(1):30–33.

Dong, F., D.A. Hennessy, H.H. Jensen, and R.J. Volpe. 2016. “Technical Efficiency, Herd Size, and Exit Intentions in U.S. Dairy Farms.” Agricultural Economics 47(5):533–545.

Drabenstott, M. 1996. “Industrialization: Steady Current or Tidal Wave?” Choices 9(4):4–8.

Hennessy, D.A., and T. Wang. 2012. “Animal Disease and the Industrialization of Agriculture.” In D. Zilberman, J. Otte, D. Roland-Holst, and D. Pfeiffer, eds. Health and Animal Agriculture in Developing Countries. New York, NY: Springer, pp. 77–99.

Livestock Marketing Information Center (LMIC). 2018. “MilkProdnInv_Annual.xls” and “CATINV.xls” [Spreadsheets]. Available online: http://www.lmic.info

MacDonald, J.M., J. Cessna, and R. Mosheim. 2016. Changing Structure, Financial Risks, and Government Policy for the U.S. Dairy Industry. Washington, DC: U.S. Department of Agriculture, Economic Research Service, Economic Research Report 205, March.

Mosheim, R., and C.A. Knox Lovell. 2009. “Scale Economies and Inefficiency of U.S. Dairy Farms.” American Journal of Agricultural Economics 91(3):777–794.

Norman, H.D., L.M. Walton, and J, Dürr. 2018. Somatic Cell Counts of Milk from Dairy Herd Improvement Herds during 2017. Bowie, MD: Council on Dairy Cattle Breeding, CDCB Research Report SCC19, February.

Sauer, J., and U. Latacz-Lohmann. 2015. “Investment, Technical Change and Efficiency: Empirical Evidence from German Dairy Production.” European Review of Agricultural Economics 42(1):151–175.

Sumner, D.A. 2014. “American Farms Keep Growing: Size, Productivity, and Policy.” Journal of Economic Perspectives 28(1):147–166.

U.S. Department of Agriculture (USDA). 2018. Milk Cost of Production Estimates. Washington, DC: U.S. Department of Agriculture, Economic Research Service. Available online: https://www.ers.usda.gov/data-products/milk-cost-of-production-estimates/ [Accessed 20 Aug. 2018].