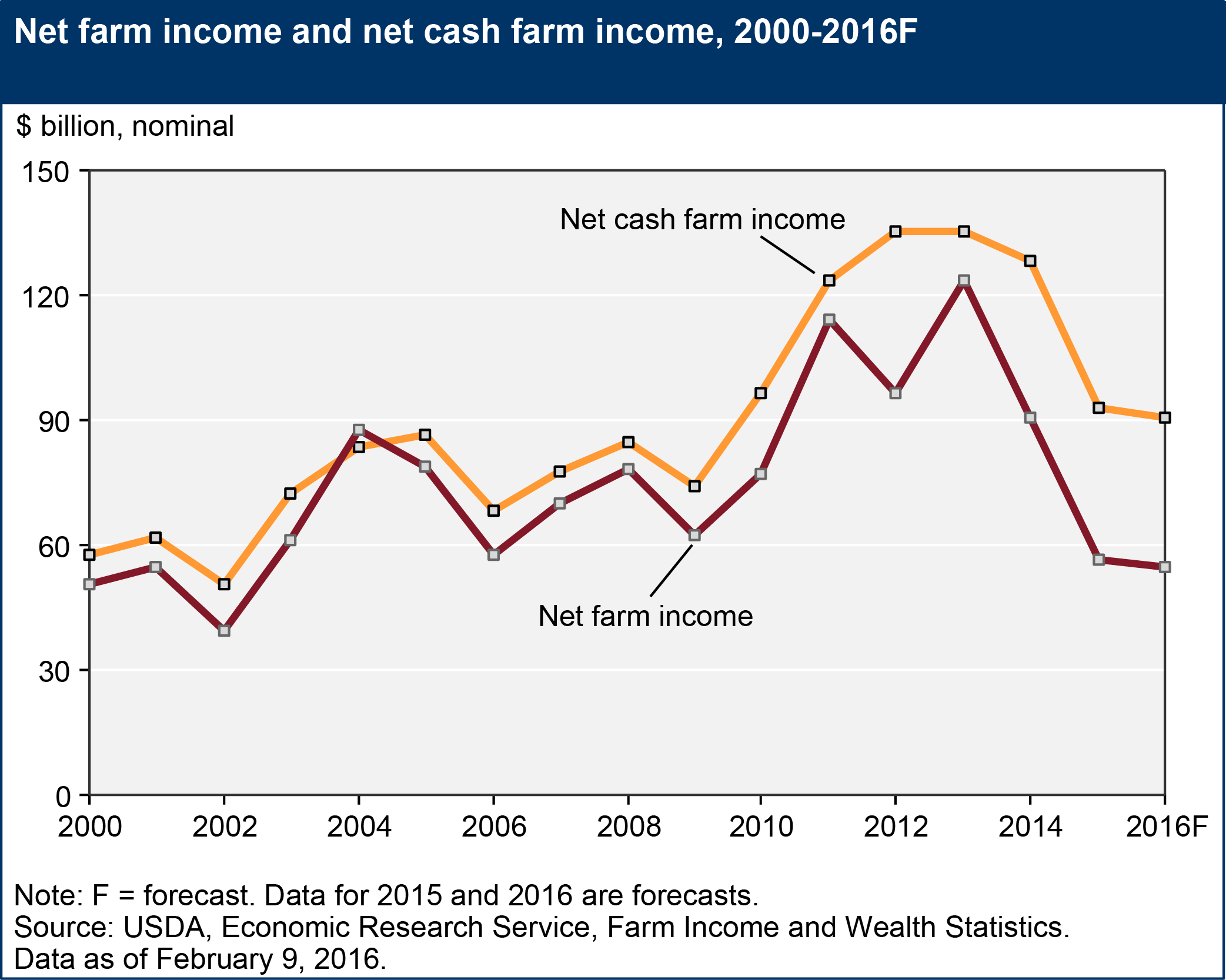

Net farm income has fallen dramatically from its recent high in 2013 due to lower grain and cotton prices (Figure 1), setting the stage for a contentious debate over the next Farm Bill. With lower prices and continued record-setting corn yields in the Midwest, the discussion will likely shift to issues of price risk rather than revenue. For example, if corn prices remain at current levels below the Reference Price, triggering 2018/19 Agriculture Risk Coverage (ARC) payments on corn will require a Marketing Year Average (MYA) Price below $3.18 per bushel, assuming the actual 2018 county yield is equal to the 5-year Olympic average county yield (Barnaby, 2016a). An Olympic average eliminates very high and very low values, before averaging and the ARC program uses Olympic averages. The Office of Management and Budget's (OMB) 10-year budget line assumes most ARC enrolled farmers will switch to Price Loss Coverage (PLC) in 2019-2020 after the current commodity title ends. Farmers had a choice of programs under the 2014 Farm Bill and, given their price and yield expectations, many chose ARC over PLC.

Source: USDA-ERService, Farm Income and

Wealth Statistics. Data as of February 9, 2016.

Note: Data for 2015 and 2016 are forecasts.

In addition to price risk, much of the debate focus for the next Farm Bill will be on crop insurance. Besides the status quo, three policy options are being proposed by supporters and critics of current crop disaster policy:

Some agricultural economists have proposed a dramatic shift away from privately-delivered crop insurance to a county-triggered disaster program administered by the FSA (Babcock and Hart, 2005a; Babcock and Hart, 2005b; Collins and Bulut, 2011). These public sector disaster protection delivery plans assume savings by eliminating premium subsidies on individual plans, eliminating private sector delivery and individual field level lost adjustment costs, and assume the public sector can deliver an area based disaster program with no additional public employees and operation costs. These savings are assumed to be large enough to eliminate any need for farmer paid premiums. Therefore, a proposed area-based disaster program would be free to the farmer in the sense that it would not have a premium, but relative to the current crop insurance program, it could involve substantial costs to farmers in other ways and may run into serious practical difficulties.

A free, area-based alternative to crop insurance would be different from individual, privately-delivered crop insurance in several ways. The program likely wouldn’t provide any individual farm coverage because this policy would require individual farm loss adjustment and reduce any savings claims for public sector crop disaster aid delivery. Individual farm level loss adjusting would require contracting private loss adjusters or a dramatic increase in FSA personnel. The proposed disaster program would be similar in structure to ARC, except that it likely wouldn’t have the 10% stop loss (Barnaby, 2016a). Like ARC, payments under this program would likely come a year after harvest since payments would be based on county yields and MYA prices. Due to its lack of an individual loss adjustment, an area-risk disaster program would likely be less expensive from the taxpayer’s point of view than the current crop insurance program, especially if the producer is required to pay a share of the premium cost.

One important function of crop insurance is to provide collateral for farmers’ operating loans. The difficulty in forecasting county yields—similar to ARC—would likely preclude the use of disaster program payments as collateral for individual farm loans. Furthermore, the program would be of limited use in guaranteeing bushels to offset forward crop sales or replacing a feed supply for crop-livestock producers. Both of these issues would likely weigh more heavily on smaller, younger producers with limited equity. Unlike current crop insurance policy, disaster payments would be subject to means testing, payment limits, and sequestration cuts, which would increase farmers’ exposure to political risk. Additionally, farmers would have no recourse if an FSA employee made a mistake that reduced their payment. By contrast, private crop insurance agents carry errors and omissions insurance to cover liability exposure for errors in farmers’ crop insurance contracts.

Significant data problems would face any move to an area-based disaster program. USDA's National Agricultural Statistics Service (NASS) is currently missing county yield estimates for many counties (Barnaby, 2016b). When practices such as irrigation are considered, the data problems are even more severe. Without individual farmer-reported crop insurance yield data from RMA, the USDA would not be able to fill in the gaps in the NASS county data as readily.

Since farmers would pay no premium under the area-based FSA disaster program, adverse selection—the greater likelihood of choosing more insurance when you know you face greater risks—would be an even bigger issue than it is for crop insurance. Since area coverage would have no premium, farmers would likely choose maximum coverage. This would result in the greatest benefits flowing to high-risk counties that have a large amount of yield variability.

An area-wide insurance product for upland cotton, the Stacked Income Protection Plan (STAX) is similar to the area-based FSA disaster program. Even with its large premium subsidy, however, only 30% of upland cotton acres were covered by STAX. It is important to note that this product, in addition to the Supplemental Coverage Option (SCO) and the Yield Exclusion (YE) were intended to function in the place of ARC and PLC commodity programs. Except for hail coverage, all private insurance coverage would likely be crowded out in the case of a free disaster program.

ARC has demonstrated many limitations of area crop insurance-disaster programs. Nearly all Iowa counties had NASS county yields used by FSA to determine the ARC payments. Outside of Iowa, county yield based disaster programs run into problems with administration due to limited data availability. Many counties have no NASS yields or the yields are not split between irrigated and non-irrigated acres for counties that split the ARC county yield by practice.

Determining county yields for ARC is even more difficult for wheat. When NASS wheat yields are not available the next best alternative is the RMA’s published county yields for SCO if provided by irrigated compared to non-irrigated production practices. RMA offers SCO by practice for Washington, Idaho, and Oregon wheat, but it is the same guarantee offer for both irrigated and non-irrigated. RMA reported the same county yield to settle SCO claims for irrigated, non-irrigated, spring wheat, winter wheat, and soft white wheat. As a result, RMA’s county yields for Washington, Idaho, and Oregon wheat are of little use for estimating FSA county yields that are split into irrigated and non-irrigated practices. With no published RMA SCO insured acres by practice, there is no method for using RMA county yields to estimate FSA county yields that are used to settle ARC claims in counties split by FSA between irrigated and non-irrigated. For example, Yakima County, Washington’s five-year Olympic average FSA 2015-2016 benchmark county wheat yield was 112 bushels for irrigated and 17 bushels for non-irrigated wheat. RMA published a final SCO county yield of 30.8 bushels for all practices and types of wheat for the 2015 crop. FSA will publish their 2015 county wheat yield for Yakima County, Washington in the fall of 2016, but it is obvious this single RMA published county yield is not correct for irrigated or non-irrigated wheat as required by ARC.

Many Corn Belt farmers were very surprised to learn ARC paid nothing, but paid the maximum in the county across the road. There are many causes for this result. If a county had suffered multiple yield losses in the five years prior to 2014, then they started with a low ARC guarantee. In a five-year Olympic average yield, if two of those historical yields are bad, then one of the bad yields will be in the three-year average, after excluding the high and low yield. The order of the yields makes a difference, too. It is more advantageous for farmers to have low yields in 2009 and 2010, and higher yields in 2012 and 2013 (Barnaby, 2016a).

However, Iowa Senators Grassley and Ernst publicly released a letter sent to Agriculture Secretary Tom Vilsack concerning the yield data used to calculate ARC payments. The letter is evidence that Iowa corn growers are questioning why, with the same prices, contiguous counties have large differences in corn ARC payments. The Senators note in their letter that there are “several instances of significant discrepancies in payments between adjacent counties.” Historical yields used to set the Olympic average yields are one of the main reasons for this discrepancy (Barnaby, 2016b). If a county has a crop disaster in 2 or more years of the five-year history, it really lowers the benchmark yield and the resulting ARC guarantee. For example Ringgold County, Iowa had multiple year county yield losses prior to 2014 resulting in a reduced benchmark yield of 110 bushels that is lower than the long run average yield as compared with the crop insurance T-yield of 133 bushels. Using such a short history can produce Olympic average county yields below the expected county yield and limit the effectiveness of ARC as a risk management tool. This method can also inflate Olympic average county yields if there are multiple historical county yields that were above trend yield.

In addition, there is basis risk between county yields and farm level yields. Many farmers have already discovered they can have a loss and the county does not trigger a payment. That is no surprise in the Great Plains where it can rain on one side of the road and not the other side.

Replacing crop insurance with an FSA-administered area disaster program is unlikely, but it is expected in the 2019 Farm Bill debate critics will again make this same argument that the public sector can deliver area based coverage for less taxpayer costs than the current privately delivered crop insurance program. There is no doubt the critics will point to FSA’s successful delivery of ARC, which is an area based disaster program. Most farmers like the service they receive from their crop insurance agent because if the service is poor they can simply change agents. Farmers can’t change FSA offices. The ARC program was the first experience most farmers have had with an area disaster and crop insurance programs and it was not a good experience for some farmers. A common complaint was why "the county across the road received a maximum ARC payment, while my county received no payment" (Grassley and Ernst, 2016). As a result of that experience, farmers will now better understand area based crop insurance and disaster program proposals.

In cases where farmers are required to pay part of an area crop insurance premium, participation has been far below the expected participation forecasted by the experts. An example is the low STAX participation that replaces the ARC and PLC programs for cotton farmers, but requires cotton farmers to pay 20% of the premium. Even with an 80% subsidy rate, only 30% of insured acres were covered by STAX in 2015. Participation may have been higher if individual coverage had not been improved with the yield exclusion option, but it is difficult to determine whether or not this is the case. Historical performance has demonstrated it will require a 100% subsidization of an area disaster program to achieve politically acceptable participation levels. Agricultural economists seem to like area-based disaster/crop insurance programs better than farmers and lenders.

Those critics who want to replace private delivered crop insurance with a "free" area based FSA-administered disaster program will find the debate more difficult after farmers’ experience with ARC. Farmers will remember when they were paid nothing and the county across the road was paid the maximum. We should point out that ARC worked exactly the way it was intended to work. Even if the major farmer complaints are addressed, many farmers would still not be willing to pay any of the “premium” cost for an ARC program.

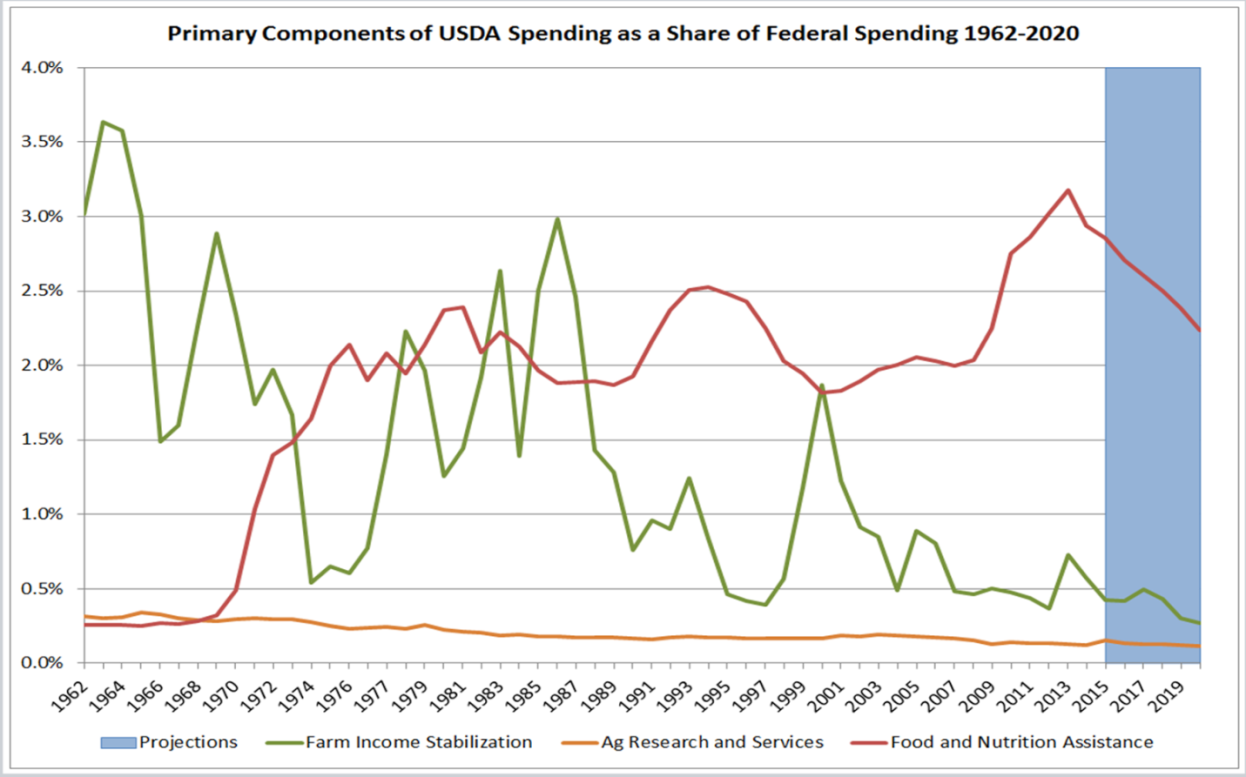

Source: Office of Management and Budget,

Historical Tables

Many of the modifications to the crop insurance program that are likely to be proposed in the context of the next Farm Bill were included in bills introduced in the House and Senate in late 2015 but which failed to become law. In November 2015, Senator Jeff Flake (R-AZ) and Representatives Jim Sensenbrenner (R-WI) and Ron Kind (D-WI) introduced the AFFIRM Act in both Houses of Congress which proposed several changes to crop insurance that would directly impact farmers and Approved Insurance Providers (AIP). The impetus behind the bill was curtailing federal government spending, but cuts to agricultural spending are unlikely to have much of an effect on the federal budget (Figure 2). The bill would limit RMA’s premium share—often referred to as a subsidy—to $40,000 per person, shifting a larger share of the total premium to farmers. The bill would also eliminate the government’s share of paid premiums for all farmers with an adjusted gross income (AGI) over $250,000 per person. AIP’s Administrative and Operating (A&O) costs would be limited to $900 million per year—currently $1.3 billion—which would likely cause a cut in agent commissions.

These limits would likely result in the creation of “paper farms” that would allow more farmers to get under the Adjusted Gross Income (AGI) limit, similar to the response in the commodity programs that have payment limits. These additional “paper farms” would create no new insured acres, but they would create additional paper work for all involved. More “paper farm” contracts would clearly impose additional costs on AIPs and independent crop agents, but would provide no new revenue. Farmers would also have additional costs for accountants and lawyers required to set up these paper entities. In addition, farmers would have additional administrative cost tracking these multiple entities. However, these limits on farm size would create additional paper work for RMA and that would likely create the need for more Federal employees to track and audit these additional “paper farms”.

Finally, the bill would eliminate RMA’s share of the premium on the Harvest Price Option (HPO). This provision accounts for $19 billion of the $24 billion of the total budget savings and would apply to all farmers regardless of AGI. In addition, AFFIRM would also reduce the rate of return to the AIPs.

The elimination of the HPO subsidy could have serious consequences for farmers. Once farmers plant their crop, they are long the market! All farmer marketing plans including feeding their crop to livestock or dairy cows, storing the crop for later sales, deferred price contracts, forward cash contracts, minimum price contracts, hedge to arrive contracts, selling futures, buying put options, buy puts-sell calls, cash sales off of the combine at harvest, etc. assume production. At some point all farmers will liquidate their long position, even if it only means selling cash grain off of the combine.

The Revenue Protection (RP) that includes the HPO is the only crop insurance contract that will replace lost production at its current market value (less the deductible) and maintain the “hedge” on the long position for all farmers’ marketing plans. The other crop insurance contracts do not provide a full hedge on the insurable production. RP is similar to paying an indemnity at “replacement value” in a homeowner’s insurance policy. Although the elimination of the RMA’s premium share for HPO doesn’t eliminate HPO directly, it will increase farmer paid premiums by more than 50% in many Corn Belt counties, potentially pricing HPO out of the market. HPO covers a price increase and it also covers the yield loss that is not covered by Revenue Protection-Harvest Price Excluded (RP-HPE) when prices increase. Unsubsidized HPO coverage adds to the farmer paid premium because it eliminates subsidy on some of the yield risk in addition to the price risk.

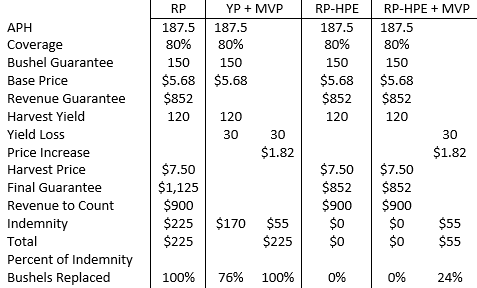

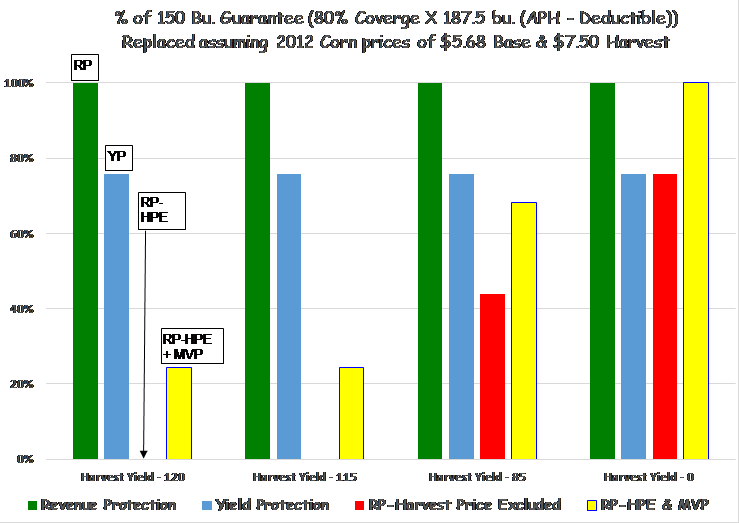

Source: Authors’ calculations

A real example of a 2012 Corn Belt farm was created to demonstrate the “yield coverage hole” in RP-HPE that occurred on 2012 corn. The Corn Belt was in a drought in 2012 when the base price for corn was $5.68 and the harvest price was $7.50 (USDA-RMA, 2016). Assume a corn farm has an approved 187.5 bushel Actual Production History—APH, “farm’s proven 10-year average yield”—insured with 80% coverage under the current RMA-approved individual farm coverage contract (Table 2 and Figure 3). The Yield Protection (YP) contract is the replacement for the original Multiple-Peril Crop Insurance (MPCI) contract that has undergone a number of name changes. YP is a yield triggered contract, but it only guarantees bushels at replacement value if the price forecast is correct. Under short crop scenarios combined with a price increase, like crop year 2012, YP will not provide enough indemnity dollars to replace those lost bushels that are needed to fill a forward contract, replace the feed supply, offset a futures hedge, or provide expected bushels needed for cash sales “off of the combine.” Crop insurance, futures, options, and commodity programs are all in some way tied to production. If production didn’t matter then there would be no need to farm. Trading the commodity markets would be sufficient for these products and programs to operate.

The example farm in 2012 lost 67.5 bushels below its expected production of 187.5 bushels. The first 37.5 bushels of the 67.5 bushel loss is the deductible and farmers must cover that loss from their equity. The next 30 bushels of the 67.5 bushels lost are indemnified at a fixed price of $5.68 set prior to planting corn in 2012 under YP. The example YP insured farm will receive an indemnity payment equal to $5.68 times 30 indemnity bushels that is equal to $170 before the premium was deducted. However, the 2012 corn harvest price increased to $7.50 and the indemnity payment only replaced 22.7 bushels or about 76% of the lost production. Farmers had to replace those bushels that are not replaced by YP from their equity to offset their automatic long position. Effectively this is a second deductible in the YP contract.

Very few corn farmers insure with YP. Nationally 92% of the insured corn acres were insured under one of the revenue plans in crop year 2015. The revenue plans account for 97% of corn premiums. Among the revenue products RP and RP-HPE account for 90% of the insured corn acres and 94% of the corn premium. Less than 1% of RP insured acres have the harvest price excluded, accounting for less than half of a percent of the premium (USDA-RMA, 2016.)

Farmers have voted with their pocketbook and it is clear they prefer RP policies that include the HPO. The AFFIRM Act is targeted at the very product that famers prefer and there are solid risk management reasons why farmers prefer RP over RP-HPE. If a policy similar to AFFIRM would have passed in to law, Corn Belt farmers would face a premium increase of more than 50% on corn. In that scenario, will there be a significant number of farmers drop their coverage or switch from RP to YP, rather than pay the higher premiums? If a large number of farmers are uninsured or under-insured, would a future Congress provide ad hoc disaster aid for a drought similar to 2012? The elasticity of demand for crop insurance is the key to these questions and is under some debate by some agricultural economists (Woodard, 2016).

The original argument for the HPO was based on the 1989 Kansas wheat drought losses and the price increased eliminating winter wheat farmers’ deficiency payments. In some cases farmers had winter wheat yields near zero and they argued that YP type crop insurance did not cover their loss. YP paid the loss at a below market price at harvest, while the deficiency payment was determined by the post-harvest price that eliminated the 1989 deficiency payment—deficiency payments are similar to the current PLC payments. As a direct result, Congress passed an ad hoc disaster program in 1989 to cover the winter wheat losses that were not covered by crop insurance under a short crop and a price increase. Congress passed a similar ad hoc disaster program in 1988 to cover spring crop losses due to drought, but the legislation did not cover winter wheat losses for a winter wheat crop planted in the fall of 1988 during the same drought.

Under the scenario of a short national crop and market price increases, farmers will have less protection under RP-HPE than was the case under YP (MPCI) on the 1989 winter wheat crop or the 2012 corn crop. Under this scenario, policy experts will often show that farmers are better off because the USDA aggregate farm sector income is often near record highs. While some farmers will have major crop losses, other farmers in other states with no crop losses will sell their crop at the drought-induced higher prices. Because of the inelastic demand for grain, it is not uncommon for the price to increase by a greater percentage than the percentage reduction in yield, resulting in a record aggregated farm income.

The problem with this argument is that farmers do not farm in the aggregate, no farm is the "average" farm. Farmers that happen to be in the state with major losses will not have record incomes. This is the difference between macroeconomics and farm-level economics. Under a scenario of the Western Corn Belt being in a drought while the Eastern Corn Belt has record yields, Eastern Corn Belt farmers will have record incomes while farmers in the Western Corn Belt will have little or no production to sell at higher prices. If our example farm is in the drought area and suffers a 67.5 bushel loss, the farm will collect no indemnity payment if the farm manager has excluded the HPO by selecting RP-HPE (Table 2, Figure 3). In fact under the scenario of 2012 corn prices that increased from $5.68 planting price to a $7.50 harvest price, the example RP-HPE insured farm at the 80% coverage level will need a yield loss greater than 113 bushels to trigger any indemnity payments. It will require a farm yield equal to zero for the RP-HPE indemnity payment to equal the YP indemnity payment.

The RP-HPE provides little risk protection for the farmer-feeders who will need to replace their feed supply. Even if a farmer sells a crop “off of the combine,” the manager will have fewer bushels to sell for cash and the indemnity payment will not make up the difference. Often economists don’t include the deductible and the farmer paid premiums when evaluating the net farmer position provided by RP-HPE when a major crop loss occurs.

The argument has been made that HPO is not needed because the private sector will offer the coverage. The example cited is the Market Value Protection (MVP) that was released in 1991 as an endorsement to the MPIC, renamed YP, coverage and provided a yield replacement contract. Notice that the farm’s yield has to reach zero before RP-HPE plus MVP would replace 100% of the insurable lost bushels (Figure 3). For example, with yield loss of 67.5 bushels, the RP-HPE triggers no payment and MVP would have paid $55 that only covers the price increase. The RP-HPE has a hole in the yield coverage of $170 that would have been paid by YP or RP (Table 3).

RP will cover the hole in the yield coverage that is not covered by RP-HPE and also covers the price increase. Because of this, there would be a large increase in farmer paid premium costs if the subsidy were removed from the HPO. The premium increase will likely double if the HPO risk were covered privately because the AIPs will need to load for expenses and catastrophic risk, too.

RP combines revenue coverage and yield replacement in one convenient product. If prices fall, RP will pay the same as RP-HPE. If prices fall far enough it is possible the yield deductible will disappear in both the RP and RP-HPE contract. If this happens it will require an actual harvest yield that is greater than the APH—no yield deductible—to eliminate indemnity payments. If prices increase the RP will replace lost bushels at current market cost after the deductible is met. When prices increase, the RP deductible never shrinks, but the RP-HPE deductible increases and requires a larger yield loss to trigger any indemnity payments.

If a price option or its subsidy must be eliminated from RP for budget reasons, it should be the “put.” Lower market prices are covered by PLC or in some cases ARC from the FSA program. Therefore, it is at lower prices where, under some conditions, the crop insurance and commodity programs will overlap. The harvest price option included in RP is a complement to FSA’s commodity program since higher prices reduce or eliminate PLC and under some conditions the ARC payments, too.

Other costs associated with the provisions in the AFFIRM Act would fall on insurance companies and the RMA. For example, farmers electing to exclude the harvest price in RP may cause underwriting losses, unless one assumes actuarial soundness. For example, in Iowa, eliminating the HPO on corn may cut premiums more than it has historically cut claims but the public data is limited to years after 2011. For the five-year period 2011-2015, the Iowa five-year average RP corn loss ratio was 1.66 on $566 million of premium versus an RP-HPE loss ratio of 2.27 on $7 million of average premium over the same period (USDA-RMA, 2016).

An alternative to the elimination of the HPO premium share paid by RMA is to give producers the option of eliminating the subsidy on either the “put” or “call” built into RP. Producers who use marketing tools or who have strong downside price protection from the commodity program might prefer the harvest price over the insurance “put.” Another alternative to reduce taxpayer cost would be to cut RMA’s share of the premium by five percentage points across all crop insurance contracts, including CAT. Unlike altering specific contracts, this wouldn’t bias farmers’ decisions.

Several economists have published papers advocating for the elimination of ARC, PLC, and crop insurance and replacing them with a free market policy (Smith, 2012; Bakst, 2014; and American Enterprise Institute, 2016). If the farm safety net were completely eliminated as a number of groups have advocated, would Iowa still be planted to corn? The answer is “yes,” but many other aspects of the farm economy would change. Over time, land prices and cash rents would adjust to an agricultural economy without USDA support. Farmers’ rates of return would eventually normalize. However, there would likely be fewer producers. Young farmers with limited equity would lose the most were this policy implemented. The elimination of the safety net may make U.S. farmers less competitive on a global scale because foreign governments will likely continue a preference for local production. For example, refusing importation of GMO corn for safety concerns, foreign central banks’ influence on currency exchange rates to benefit their own exporters, and expanded EPA regulations on commercial agriculture will likely disadvantage U.S. producers.

It’s unlikely that a free market crop insurance industry would form unless all government subsidies were eliminated. Few farmers would be willing to pay the higher premiums required by a fully-private market as long as the USDA infrastructure is in place for some future Congress to provide ad hoc disaster aid or other cash transfers to farmers. Congress would need to close all forms of support including commodity program payments, disaster payments, and conservation payments. If not, producers would be reluctant to pay unsubsidized premiums for fully-private insurance and would instead push for the reinstatement of disaster payments using the existing infrastructure.

It is very unlikely that the current crop insurance program will be replaced with a free, FSA-administered disaster program. Most farm groups would oppose this change, in addition to the independent crop insurance agents, agricultural lenders, and AIPs. As a result, a return to an FSA-administered disaster program is not likely. The structure of the current crop insurance program was passed into Law in 1980 to replace an FSA standing disaster program.

Though some agricultural economists and other groups would like to see a more free market policy implemented, given the expected political opposition from the crop insurance coalition, it is unlikely the current farm safety net will be eliminated and replaced with a free market policy. Assuming some parts of the country will have private insurance offers for selected perils, the private premiums paid by farmers will be much higher. Private premiums would have to cover the operating expenses, likely more expensive re-insurance premiums because USDA would no longer provide any re-insurance, and cover the entire current premium subsidy. Since premiums will likely double, it will be necessary to remove the USDA delivery infrastructure; otherwise a future Congress could provide an ad hoc disaster aid program. As long as the USDA delivery infrastructure is in place, few farmers will be willing to pay private crop insurance rates as most will continue to assume government will provide support when there is a disaster, until proven otherwise.

For the foreseeable future, the risk management policy will likely remain as it is with some “minor tweaks” to crop insurance. In the last Farm Bill, the conservation coalition was able to add the conservation requirement to crop insurance and other critics were able to secure cuts to the AIPs and agents. Many of the same groups will be back to attack the harvest price, propose means testing, subsidy limits or payment limits, more cuts to agent commissions, and cuts to the AIP’s rate of return. Crop insurance critics’ success will likely depend on how well the crop insurance coalition holds together. Some of these proposals are more damaging to producers than others and may lead to some unintended consequences. While it is easy to see the financial interest of those who favor the current system, who have a financial interest in the crop insurance and commodity programs, many of the critics also come with conflicts of interest. Though it is not easy to do, one needs to follow the money to identify conflicts of interest in the crop insurance debate.

American Enterprise Institute. 2016. Solutions 2016 for Agriculture. Available online: http://solutions.heritage.org/regulatory-overreach/agriculture/.

Babcock, B.A. and C.E. Hart. 2005a. “Judging the Performance of the 2002 Farm Bill.” Iowa Ag Review 11.

Babcock, B.A. and C.E. Hart. 2005b. “Safety Net Design for the New Farm Bill.” Iowa Ag Review 11.

Bakst, D. 2014. “10 Guiding Principles for Agriculture Policy: A Free-Market Vision.” Heritage Foundation Issue Brief #4213 on Agriculture. Available online: http://www.heritage.org/research/reports/2014/05/10-guiding-principles-for-agriculture-policy-a-free-market-vision

Barnaby, G. A. 2016a. “Corn ARC is Expected to Provide ‘Little’ Coverage in the Final Year of the ‘Farm Bill.’” AgManager.info. Available online: http://www.agmanager.info/crops/insurance/risk_mgt/rm_pdf16/AB_ARC_ReducedCoverage.pdf

Barnaby, G. A. 2016b “Some FSA and RMA County Yields used to Determine Claims Don’t Agree.” AgManager.info. Available online: http://www.agmanager.info/crops/insurance/risk_mgt/rm_pdf16/AB_ARC-LowPay.pdf.

Collins, K., and H. Bulut. 2011. "Crop Insurance and the Future Farm Safety Net". Choices. Quarter 4. Available online: http://choicesmagazine.org/choices-magazine/submitted-articles/crop-insurance-and-the-future-farm-safety-net - See more at: http://www.choicesmagazine.org/choices-magazine/submitted-articles/crop-insurance-and-the-future-farm-safety-net#sthash.aD5fnQAJ.dpuf

Grassley, C. and J. Ernst. 2016. Grassley, Ernst Seek Information from Agriculture Secretary on USDA Payment Formula. May 9. Available online: http://www.grassley.senate.gov/news/news-releases/grassley-ernst-seek-information-agriculture-secretary-usda-payment-formula

U. S. Department of Agriculture, Risk Management Agency (USDA-RMA). 2016a. Price Discovery Reporting. Available online: http://www.rma.usda.gov.

U. S. Department of Agriculture, Risk Management Agency (USDA-RMA). 2016b. Summary of Business Reports and Application. Available online: http://www.rma.usda.gov,

Shurley, D. 2015. “Modifications in STAX are Forthcoming for 2016 Crop.” Southeast Farm Press, December.

Smith, V.H. 2012. “The Grim Reapers of Crop Insurance.” American Enterprise Institute.

Woodard, J.D. 2016. “Estimation of Insurance Deductible Demand Under Endogenous Premium Rates.” Selected Paper, 2016 AAEA Annual Meeting in Boston, MA