Pork is important around the world as evidenced by reactions as recently as 2012 when bacon lovers nearly took to the streets with rumors of global shortage. Even heads of state like Cristina Kirchner, president of Argentina, understand the importance of pork. While Argentina has the highest per capita beef consumption, Kirchner publicly lauded the sexual benefits of pork consumption. In China, where pork has become a staple food, the consumer price index is often referred to as the China Pork Index (Rabobank, 2012). With global pork consumption at more than 100 million metric tons (MT), pork is the No. 1 consumed meat in the world (USDA PSD, 2012; FAO-Animal Production and Health: Sources of Meat, 2012).

Only a small number of countries/regions account for over 90% of global pork production. China leads all nations, producing over 52 million MT, over half of global production, followed by the European Union (EU) at 22 million MT, the United States at 10.4 million MT, Brazil at 3.3 million MT, Russia at 2.1 million MT, and Canada producing 1.8 million MT (FAS-Livestock and Poultry: World Markets and Trade October 2012, 2012). Now a good deal of the world’s demand falls outside the borders of these producers, and many countries must import pork to satisfy demand. Today, the United States is supplying a large portion of this demand.

Over the years the U.S. pork industry has adopted a number modern production practices and technologies and numerous biosecurity measures. As a result, the U.S. pork industry has become one of the lowest cost producers of safe, healthy pork, which, in part, has led to the United States becoming the number one pork exporting country in the world. Others have claimed this title, but those claims have since faded.

Today, U.S. pork exports generate significant value for the U.S. pork industry and the U.S. economy. In 2012, U.S. pork exports reached a record level of over $6.3 billion. According to the U.S. Department of Agriculture (USDA), each $1 billion of exports in animal production supports approximately 17,200 U.S. jobs (USDA ERS, 2012). At 2012 levels, U.S. pork exports supported nearly 110,000 U.S. jobs. In addition to U.S. jobs, U.S. pork exports have a positive impact on pork producer’s bottom-line, adding $55 of value to U.S. live hog prices in 2012. Recent analysis shows U.S. pork exports account for $10.6 billion dollars of agricultural output and $1.8 billion dollars of national income (Hayes, 2012). The fact that over 95% of the world’s population resides outside of U.S. borders, and U.S. pork consumption has remained flat, further confirms the growing importance of exports to the U.S. pork industry.

Becoming the world’s largest pork exporter did not happen overnight. It has taken an aggressive trade policy agenda that fights for the reduction of tariffs and nontariff barriers though free trade agreements (FTA). Simply, you cannot sell where you don’t have access.

In 1995, for the first time, the United States became a net exporter of pork and since then it has not looked back. The U.S. pork industry’s early export success came in large part from both the North American Free Trade Agreement (NAFTA) and the Uruguay Round Agreement on Agriculture.

In the early 1990s, NAFTA was a controversial issue, and still today some cast doubts on its overall success. However, for the U.S. agricultural sector NAFTA has been a resounding success. Since 1993, the year before implementation of NAFTA, the value of U.S. agricultural exports to Canada have increased by 287%, while exports to Mexico have seen an increase of over 400%. Under NAFTA, the U.S. pork sector, that obtained a ten-year phase out of tariffs and a significant reduction in nontariff barriers, has achieved high levels of exports to Canada and Mexico. Once an inconsequential market for U.S. pork, Mexico now ranks, in 2012, as the second largest value market for U.S. pork exports, valued at $1.13 billion, and the largest volume market, over 600,000 MT exported, a rate increase of 530% since implementation. Mexico alone now accounts for over 20% of total U.S. pork exports and approximately 4% of U.S. pork production. U.S. pork exports to Canada, as part of NAFTA and previously under the United States-Canada FTA, have grown to over 230,000 MT from just under 7,000 MT in 1989, placing Canada among the top five pork markets.

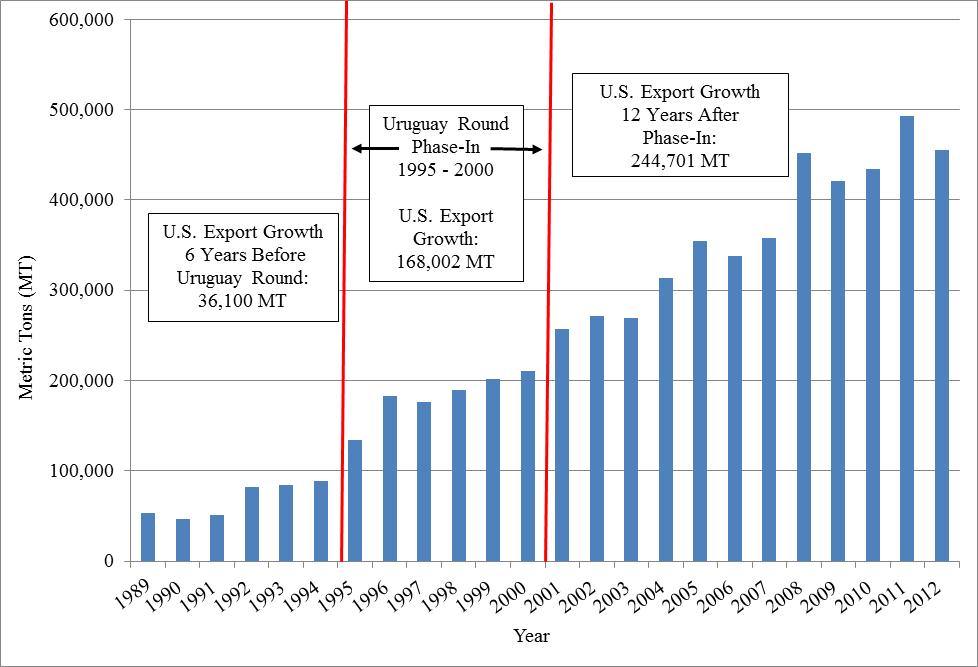

In tandem with NAFTA, the Uruguay Round provided significant market access for U.S. pork products to many new markets, like Japan, now the number one value export market for U.S. pork, by addressing more than simply tariffs. In the case of agriculture, the Uruguay Round addressed market access issues ranging from permitted levels of domestic subsidies to new rules on sanitary and phytosanitary (SPS) measures—actions taken by governments to protect human, animal and plant health. At the core of these new SPS rules was the requirement that SPS measures be supported by sound science (WTO, 2012). Often governments, in lieu of tariffs, turn to non-science-based SPS measures/barriers, a form of nontariff barriers, to limit imports of sensitive products to protect domestic industries. As part of the Uruguay Round Agreement on Agriculture, countries were to remove trade restrictive non-science-based SPS barriers and set bound tariff rates—maximum level of tariffs—along with a phase-in period, ranging from six to ten years, depending on the defined level of development of a certain country, to gradually reduce tariff levels (FAS-FACT SHEET: Sanitary and Phytosanitary Measures and the World Trade Organization, 2006). As a result, the U.S. pork industry saw steady growth in pork exports during the phase-in period, 1995 to 2004.

The Uruguay Round and its six-year phase-in period provide a strong example of what the reduction of trade barriers can do for exports. In the six years prior to the implementation of the Uruguay Round, U.S. pork exports to Japan, for example, grew by a little over 36,000 MT, then during the six-year phase-in period, U.S. pork exports increased by more than 168,000 MT. Since the end of the phase-in period, U.S. pork exports to Japan have increased by an outstanding 245,000 MT. U.S. pork exports to Japan, in 2012, reached over 455,000 MT, valued at over $1.9 billion.

By 2004, NAFTA had eliminated all Mexican and Canadian tariffs on U.S. pork, and the Uruguay Round had significantly reduced tariffs on U.S. pork, globally. Also at this time the United States began implementing a number of new FTAs. Of the 20 countries the United States has FTAs with today, 13 entered into force between 2004 and 2011. During this eight-year period U.S. total pork exports as a percentage of production jumped from around 10% to 27%

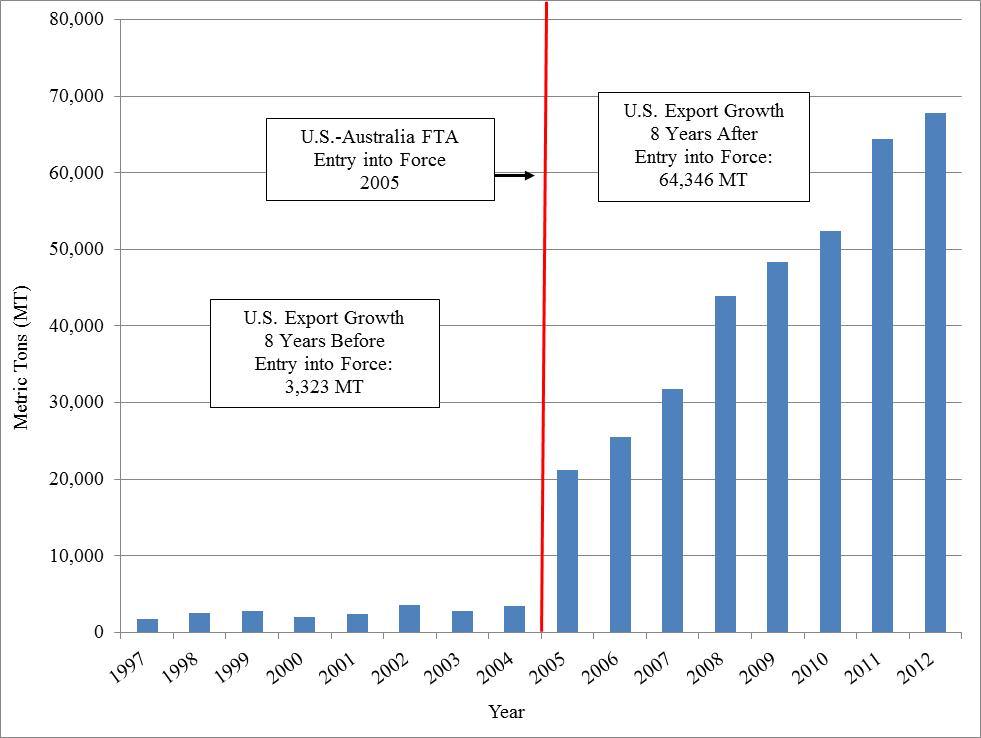

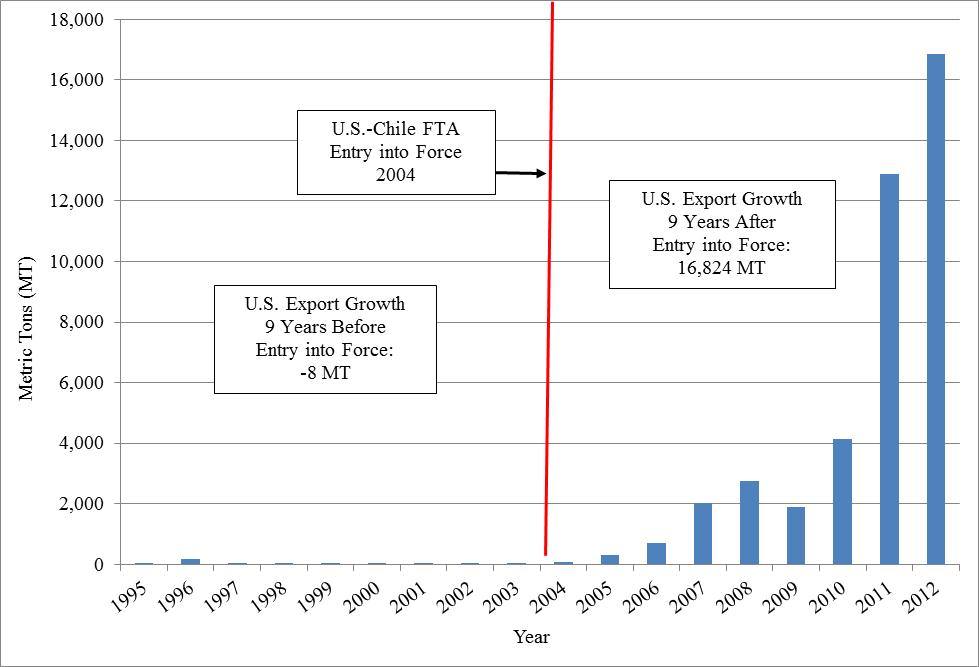

Like under NAFTA, U.S. pork exports expanded rapidly to 10 of these new markets. Among these markets with the most significant U.S. pork export growth was Australia, which in the eight years following implementation saw U.S. pork exports grow by over 64,000 MT. This compared to the small growth of a mere 3,300 MT in the eight years prior to implementation. For the Chilean market the U.S. actually saw negative growth before entry into a FTA. In the nine years since, the United States-Chile FTA has taken an insignificant market, in terms of export volume, and increased them by almost 17,000 MT.

FTA negotiations were completed and agreements signed with South Korea, Colombia, and Panama in 2006 and 2007. Unfortunately, these agreements were destined to remain stalled for almost five years when the United States could not come to an agreement on a path toward implementation. Passage of these FTAs would not come until 2011, and only after lingering issues of autos, labor rights, and tax havens were ironed out.

While the United States delayed implementation of the South Korea, Colombia, and Panama FTAs, other competitor nations were actively pursuing FTAs with these countries. In the past, proponents of FTAs expressed the benefits of trade in potential increased exports and new domestic jobs, however, this time around there was a new message. It was one of urgency that free trade agreements are not only essential to expand market access and stimulate an economy, but also to remain competitive and maintain market share. To stand idle is to move backwards, many would say. The U.S. pork industry and the South Korean market provide a good example of what could have been lost by inaction.

The United States and South Korea had developed a strong trade and investment relationship in the absence of a bilateral free trade agreement. South Korea had become a top market for U.S. pork largely due to the Uruguay Round and the U.S. pork industry’s position as the low-cost producer. In 2010, the United States exported nearly $190 million in pork products accounting for 30% of South Korea’s pork import market share. Though the countries had extensive ties, South Korea’s robust trade agenda kept it moving forward. In 2011, South Korea had already concluded or was negotiating FTAs with Chile, Australia, New Zealand, Canada, China, and the European Union, among many others.

As the U.S. pork industry’s top competitor, the EU was the greatest threat to maintaining established market share. In a scenario that assumed implementation of an EU-Korea FTA coupled with an unimplemented United States-Korea FTA, Iowa State University economist Dermot Hayes projected U.S. market share to fall by 3% per year, ultimately eliminating the U.S. from the Korean market within 10 years. The employment and financial costs of such a loss to the U.S. pork industry would have been severe, not to mention to the negative impact to the U.S. economy. Similar scenarios were projected for the Colombian market with respect to the Canada-Colombia FTA. Fortunately, in 2012, these potential crises were averted when all three FTA entered into force.

For pork producers the market access obtained in the United States-Korea FTA made it by far the most significant FTA since NAFTA. Prior to implementation of the U.S.-Korea FTA, the majority of U.S. pork exports, frozen pork and processed pork, were subject to tariff rates of 22.5% and 25%. Typically, FTAs have phase-in periods for tariff reduction, but under the United States-Korea FTA a date specific tariff reduction was negotiated. In 2016, regardless of the implementation date, all tariffs on frozen pork and some processed pork products will be eliminated. As a result of increased market access, the United States-Korea FTA is projected to generate, within 10 years, an additional $687 million in U.S. pork exports, annually, increase U.S. live hog prices by $10 and create over 9,100 U.S. jobs.

A ten year projection for the Panama FTA, the smallest of the three FTAs, but no less important, has U.S. pork exports reaching $16 million, annually.

Favorable market access terms in the Colombia FTA will enable U.S. pork exports to reach $160 million, annually, within 10 years, including $50 million alone due to the removal of one non-science-based SPS barrier. This $50 million impact reveals just how costly SPS barriers have become. Addressing these SPS barriers has become of key importance to the U.S. pork industry, especially as the United States continues negotiations with the countries of the Trans-Pacific Partnership and enters into trade talks with the European Union.

Continuing its expansion of FTAs and exports, the United States has now turned its focus to the Asia-Pacific region and the European Union. For the U.S. pork industry these markets hold enormous potential for increased exports. Many Asia-Pacific countries are now experiencing rapid growth, and as incomes rise, so will the demand for pork and other meats, some of which we have already seen in recent years. The European Union represents a market of 450 million mostly affluent consumers with domestic pork consumption in excess of 20 million MT (PSD, 2012). Unfortunately, U.S. pork exports are inhibited to these regions by tariffs and numerous SPS barriers. FTAs with these regions represent the best opportunities to remove all barriers.

The Trans-Pacific Partnership (TPP), touted as a high-standard 21st-century agreement, is an Asia-Pacific regional trade negotiation that includes the United States, Australia, Brunei, Canada, Chile, Malaysia, Mexico, New Zealand, Peru, Singapore, and Vietnam. Although the United States has completed FTAs with six of the negotiating countries, and tariff reductions are already underway, the real payout for the U.S. pork industry will come from the elimination of all non-science-based SPS barriers on U.S. pork. Of the participating countries, Vietnam offers the most potential for expanding U.S. pork exports. To put this potential demand into perspective, Vietnam’s domestic pork consumption is 1.8 million MT a year, greater than Mexico, which is currently the largest volume export market for U.S. pork. (USDA PSD, 2012)

This year, the United States and the European Union are set to begin negotiations on a transatlantic free trade agreement. Fortunately, both sides have agreed that agriculture will be included in negotiations, which is a welcomed change as the vast majority of the EU’s trade agreements exclude agriculture. An agreement that includes agriculture, however, does not assure significant new access for U.S. pork and other U.S. agricultural products. Tariffs and nontarriff barriers must be addressed and removed for the U.S. pork industry to benefit. The United States and the European Union have drastically different philosophies when it comes to agriculture production and regulation. These differences have led to a laundry list of barriers to U.S. pork, restricting exports to fewer than 8,000 MT, less than total U.S. pork exports to some small Central American countries. In addition, these differences in philosophy have led to a contraction in agriculture production and have increased the cost of food within the European Union. The inclusion of agriculture and the successful reduction in current barriers will open the second largest pork consuming market to high-quality, low-cost U.S. pork products.

There is a clear and strong correlation between the increase in U.S. trade agreements and increased U.S. pork exports, adding value to the overall U.S. economy and the pork producer’s bottom-line. Just as important as the economic benefits trade agreements provide, will be the role they play in providing healthy affordable U.S. agricultural products, like pork, to a growing world population. If the U.S. pork industry is to remain the low-cost producer and meet world demand for affordable high-quality protein, it must continue to be vigilant in maintaining a level playing field through past and future trade agreements.

AFP. (2010). Eat pork, spice up your sex life: Argentina's Kirchner. Buenos Aires, Argentina. Available Online: http://www.google.com/hostednews/afp/article/ALeqM5j1P9hICJnPnj5MFLXQQRL3YYLnOQ

Food and Agriculture Organization of the United Nations (FAO). (2012). Animal Production and Health: Sources of Meat. Rome. Available Online: http://www.fao.org/ag/againfo/themes/en/meat/backgr_sources.html

Hayes, Dermot. (2012). Economic Importance of Pork Exports to Soybean Growers and the U.S. Economy. Ames, Iowa.

Rabobank International. (2012). Is the CPI the ‘China Pork Index’? Utrecht, The Netherlands.

United States Department of Agriculture Economic Research Service. (2012). Agricultural Trade Multipliers. Available Online: http://www.ers.usda.gov/data-products/agricultural-trade-multipliers/calculator.aspx

United States Department of Agriculture Foreign Agriculture Service. (2006). FACT SHEET: Sanitary and Phytosanitary Measures and the World Trade Organization. Available Online: http://www.fas.usda.gov/info/factsheets/sps.asp

United States Department of Agriculture Foreign Agriculture Service. (2012). Livestock and Poultry: World Markets and Trade October 2012. Available Online: http://www.fas.usda.gov/psdonline/circulars/livestock_poultry.pdf

United States Department of Agriculture Production, Supply and Distribution Online (PSD). (2012). Available Online: http://www.fas.usda.gov/psdonline/psdQuery.aspx

World Trade Organization. (2012). Legal Texts: The WTO Agreements. A Summary of the Final Act of the Uruguay Round. Available Online: http://www.wto.org/english/docs_e/legal_e/ursum_e.htm#aAgreement