The Eurozone problem is the long-term consequence of using a common currency for a set of countries which do not have a common monetary and fiscal system. Its manifestation is sovereign debt crises, rising interest rates on country debt, slow or negative growth, and high unemployment in affected countries. While this could have major implications for the United States economy, our analysis suggests that even under the most adverse situations considered, total U.S. agricultural exports are likely to increase over time.

While the global financial crisis which started with the recession of 2008-09 did not cause the Eurozone problem, it did precipitate the crisis by focusing attention on the unsustainable current account imbalances associated with growth in government and private bank debt, and the shortfall in tax revenues in the EU deficit countries. The potential problem of having a European monetary union without political and financial integration of the member countries was pointed out by a number of authors (see Arestis and Sawyer, 2001, Feldstein, 1999, Feldstein, 2008, Holmes, 1997, and Kelch and Stallings, 1992). The Eurozone was formed despite these warnings. When the worldwide recession of 2008-09 occurred, it undermined government revenues, exposing countries with high debt payment burdens and reducing their short- to intermediate-term growth prospects. The Eurozone’s sovereign debt problem emerged in 2010 first in Greece but was followed by problems in Ireland, Portugal, Spain (Münchau, 2010), and Italy. Once the magnitude of these problems became known, interest rates for government bonds increased for all euro-denominated debt, including German bonds. The EU policy response was to provide a fund for the problem countries to guarantee debt repayments. However, as a condition for borrowing from that fund, major austerity programs were required for indebted countries to bring their government expenditures more closely in line with receipts. The longer term outcome of these policies is likely to reduce growth and investment in the indebted Eurozone countries for some years to come (Eichengreen, 2009; European Central Bank, 2010; International Monetary Fund, 2011; Jones, 2009; Reinhart and Rogoff, 2009; Rodrigues, 2010; Tumpel-Gugerell, 2010; and Wolf, 2008).

The major consequences of the current situation will be largely felt by the Eurozone countries themselves, who are forced to go through significant structural adjustments over the coming years. The adjustment process could generate a range of alternative macroeconomic outcomes among these countries—including differences in growth, real exchange rates and investment—which could have significant implications for U.S. agriculture and agricultural trade. U.S. exports are expected to remain robust across the full range of potential outcomes explored. Because the EU has represented an increasingly smaller share of U.S. agricultural exports, the direct impact of changes in European demand affects U.S. agricultural exports less than the secondary effects of changes in exchange rates and global investment patterns associated with alternative EU outcomes.

The Eurozone sovereign debt problem could undermine the euro’s role as a reserve currency leading to a capital flight out of the Eurozone resulting in:

Our analysis suggests that continued strong income growth in developing countries will be more important for the future of U.S. exports than the increasing competition from EU exports. This is consistent with previous research by Shane et al. (2008), where the study showed that long-term growth in U.S. exports is driven by GDP growth in our export market countries.

Once a set of countries adopts a single currency, individual members lose the ability to devalue their own currency as a means to increase trade competitiveness and overcome current account deficits. While changes in the exchange rate of the euro relative to other currencies would be expected, it will represent an average change reflecting the conditions in the currency union as a whole. Since a single country is only a small part of the currency union, conditions in that country will only marginally affect the currency’s value, particularly if the country has a small Gross Domestic Product (GDP) relative to the aggregate. In the event of imbalances, policy options for countries with current account deficits entail adjustments in monetary policy to reduce inflation and fiscal policies that reduce government expenditures, income transfers, and increase tax collections. By inducing slower growth and less aggregate demand, these policies are expected to put downward pressure on prices of non-internationally traded goods and services and wages. These adjustments will increase the country’s relative global competitiveness and, thus, reduce current account deficits. Negative GDP growth over a number of years can reduce import demand significantly and, therefore, also help correct current account deficits despite being very painful.

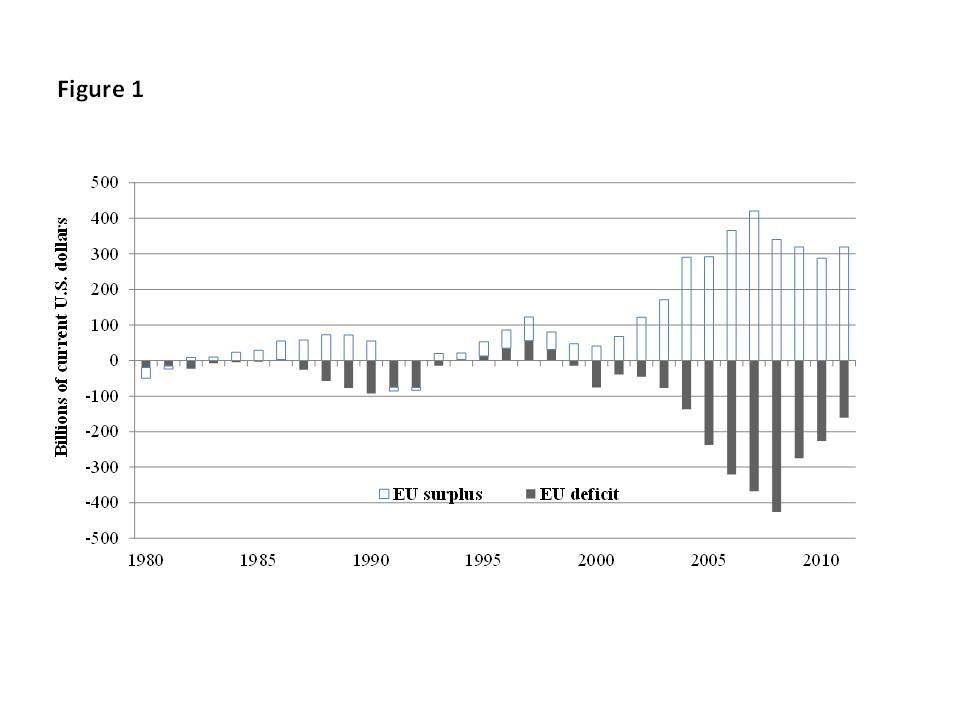

Divergent current accounts between countries in the Eurozone demonstrate the growing degree of disequilibrium within the zone before the crisis. Figure 1 aggregates current account surplus and deficit countries in the EU. The outstanding surplus countries are Germany, the Netherlands, and Sweden (an EU member but not in the Eurozone). The countries with the largest deficits are Spain, Italy, Greece, France, Portugal, and Ireland. The offsetting nature of European deficits and surpluses is evident from the figure. More indicative of why there was a crisis are the widening surpluses and deficits evident since the formation of the common currency in 1999. This suggests the fundamental policy discordance between the surplus and deficit Eurozone members, and that rebalancing current accounts in the deficit countries will likely entail rebalancing the current account of surplus countries as well. Resolution of that policy discordance is a difficult and time-consuming process involving harmonizing macroeconomic policy in all Eurozone countries. Action taken so far by the EU through the European Central Bank (ECB) to create a fund for deficit countries will provide some time for rebalancing fiscal and trade accounts and for the EU to begin the process of creating an institutional structure for a unified EU financial system and resolve the underlying policy discordance. The difficulty of overcoming the imbalances in this manner and the potential for continuing imbalances will continue to provide the conditions for future crises. The Eurozone problem is now in its third year. The evolving pattern in Figure 1 suggests that the deficit countries have been reducing their current account deficits, an indication of at least some movement towards a positive resolution of the problem.

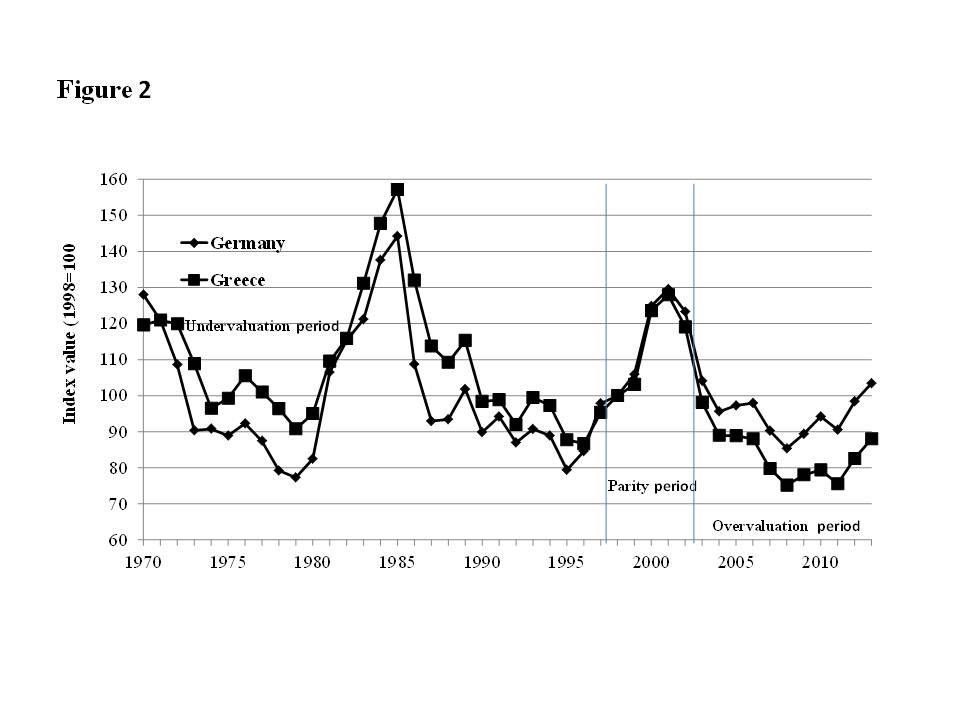

Although the Eurozone fixes the nominal exchange rate between countries, it does not fix the real exchange rate. Policies and factors which change the relative costs and prices, and thereby competitiveness, change the real exchange rate. However, the inability of countries within the zone to adjust to changes in their real exchange rate from higher inflation or lower productivity growth by simply changing the nominal exchange rate leaves them with much less attractive options to correct trade imbalances. These unpalatable options include reducing costs, wages, and prices within specific industries, or macroeconomic retrenchment policies that reduce overall incomes and imports. One indication of the cause of the growing imbalances since the formation of the Eurozone has been the relative real appreciation of the euro evaluated by the inflation in Greece relative to that of Germany (Figure 2). Before the Greeks adopted the euro in 2001, they maintained a relatively undervalued real currency compared with Germany. Between 1996 and 2000, there was relative parity in the value of the two currencies. Since 2000, there has been a widening divergence in the underlying real value of the two countries’ currencies leading to the imbalance in their current accounts (USDA, ERS, 2013a).

What, then, would it take to forestall future government indebtedness problems under a single currency system? Using the individual states in the United States as an example, the longer term solution to the Eurozone problem—if a single currency is to be maintained—is for members to unify their fiscal and monetary policies and reduce barriers to the free flow of factors of production—primarily labor—throughout the zone.

The euro problem can have significant implications for U.S. agricultural exports since the macroeconomic conditions of countries around the world can be affected—directly or indirectly—by the Eurozone problem. The primary factors that affect U.S. agricultural exports are income growth outside the U.S. and changes in exchange rates. The global consequence of the Eurozone problem is driven by the changes in the euro relative to the U.S. dollar, EU gross domestic product (GDP) growth, and GDP growth of developing economies. Given the declining importance of the EU as a destination, the slowdown in EU growth and the depreciation of the euro relative to the dollar should have fairly modest impacts on the future growth in U.S. agricultural exports.

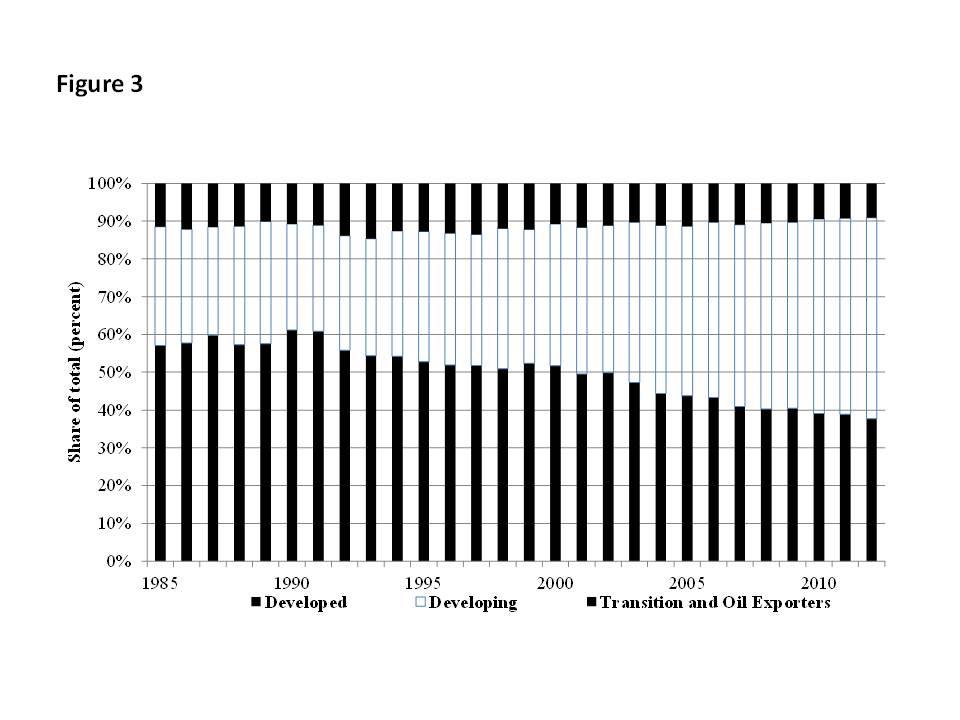

One feature of world growth since around 1980 has been the increasing importance of developing countries as major destinations for U.S. agricultural and merchandise exports (Figure 3).

Developing countries have gone from being the destination for around 20% of U.S. exports in the late 1980’s to around 40% by 2010. As a source for imports, their growing importance has even been greater. The United States imports almost 60% of its merchandise from developing countries compared with only around 20% in the late 1980s. The extremely high real economic growth in China and India, which has now spread to most of the developing world, suggests strong, new demand for imported goods in developing countries relative to developed countries (USDA, 2013b). Between 1985 and 2010, the compound growth rate for China and India was 9.28 and 6.16%, respectively, while the compound growth rate for all developing countries was 4.74%. This compares with a compound growth rate for developed countries over the same period of only 2.32%.

The importance of this growth in the present situation is that developing countries have been much less affected by the 2008-09 world financial crises and the euro crisis than developed nations. One of the major implications of the differentials in growth before and after the 2008 financial crises is that world GDP has been and continues to be demonstrably shifting toward developing countries (USDA, 2013c). While it is likely that the EU’s trading partners in Africa will be affected by the euro problem to some degree, the effects will be muted relative to countries in Europe and other developed economies. Growth prospects in all developed countries have declined since the financial crisis. It is a characteristic of financial crises historically that affected countries take a long time to resume growth at full potential rates and this appears to be the case in the aftermath of the present crisis (Reinhart and Rogoff, 2009). The combination of the growing importance of developing countries and the fact that they have been much less impacted by the crisis implies that the share of developing countries as a destination for U.S. exports will get larger. It appears likely that developing country growth will more than compensate for the slower growth in EU imports and a more competitive, devalued euro.

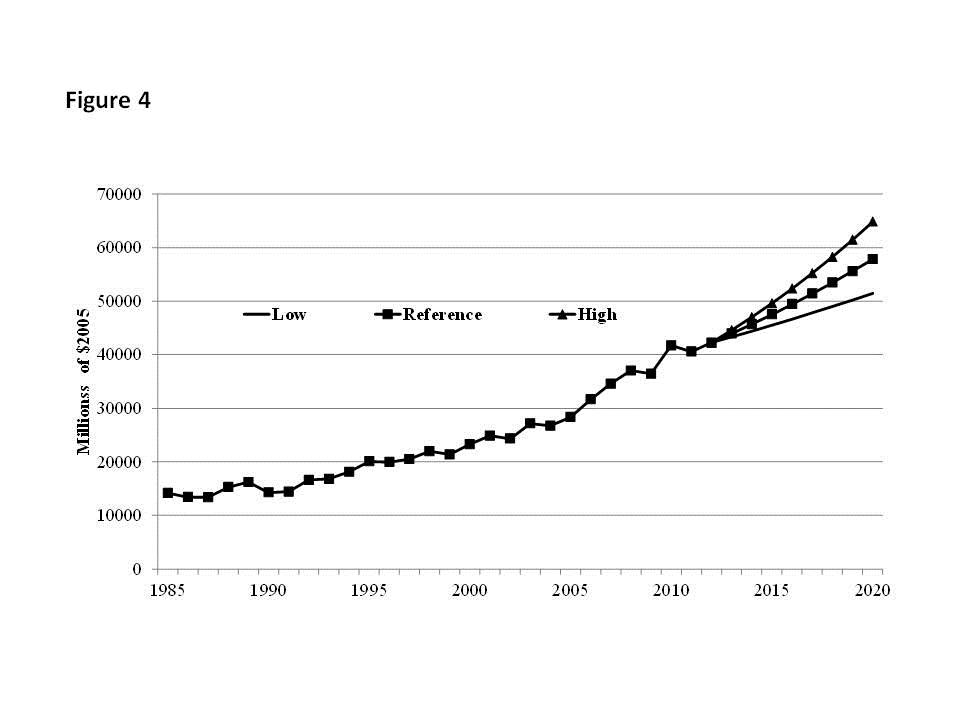

In previous work (Kelch and Shane, 2011; Peters et al., 2009; and Shane et al., 2009), an analysis was conducted of the implications of alternative macroeconomic scenario assumptions using a composite of economic models to provide a range of plausible outcomes for U.S. agricultural trade and its components. The detailed results of that analysis go beyond the scope of this paper. However, the charts below show that, even under the most dire of Eurozone scenarios where the euro falls back to parity with the dollar and GDP growth in the Eurozone goes to zero for five years, U.S. agricultural exports continue to increase. Under the more likely middle scenario which seems to be emerging, U.S. agricultural exports continue to expand at a rather robust rate.

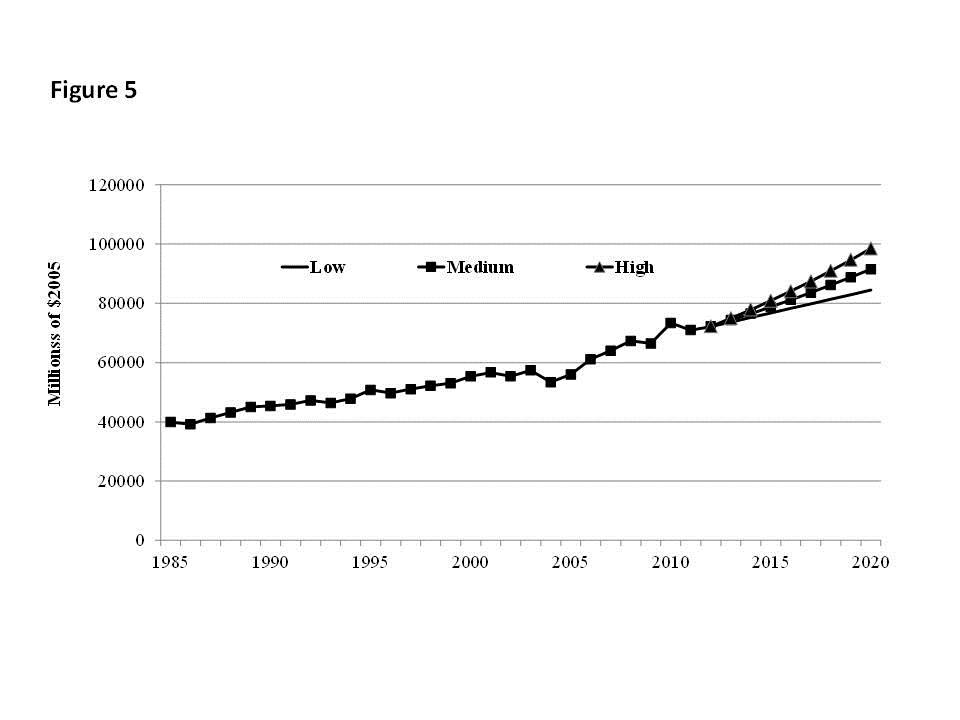

There is a big difference between the United States’ growth experience with the developed countries and with the developing countries (Figure 4). While U.S. agricultural exports to the EU remain stagnant except for some modest growth in the high scenario, rapid growth in developing countries drives higher U.S. exports under all scenarios. Thus U.S. exports are likely to continue to increase, although by a substantially lower amount, under the euro crisis scenario with a devalued euro and stagnant net investment in the EU, the low scenario (Figure 5). The difference in U.S. real agricultural exports between the high and low outcomes is around $18 billion 2005 dollars, or about 20%. The high, low, and medium scenarios represent alternative assumptions about the impact of the euro crisis on the value of exchange rates and economic growth in the Eurozone countries and derived impacts on other countries around the world. In the low scenario, we assume that the euro goes to parity with the dollar and economic growth in the Eurozone goes to zero for an extended period of time. In the high scenario, we assume that the euro is unaffected by the euro problem and continues as if the crisis never happened. In the middle scenario, we assume that there are both some exchange rate depreciations and slower growth in the Eurozone with derivative consequences to other countries exchange rates and growth.

This paper examines the consequences of the euro zone problem for U.S. agricultural exports. Yet the nature of this problem, while present since the beginning of the formation of the euro, only became a major issue in 2010.

Model-generated projections of the effects of the euro problem on the prospects for U.S. agricultural exports based on various scenarios and assumptions are presented. The results of the analysis shows that even under some rather strong assumptions about impacts of the euro problem, U.S. agricultural exports are likely to continue to increase based on growing demand in developing countries. Even substantial impacts to the exchange rates and GDP of EU countries are not likely in and of themselves to change the long term pattern of U.S. agricultural export growth. The composition of global growth is increasingly focused on growth in developing countries, particularly in Asia. Developing countries have benefitted from high investment rates based on domestic savings, but also from substantial increases in foreign direct investment which has resulted in transfers of capital, technology, market capacity, and access. U.S. agricultural exports only increase modestly in the low scenario as indirect impacts of EU stagnations have global effects.

Arestis, Philip, and Sawyer, Malcolm. 2001. Will the Euro Bring Economic Crisis to Europe? Jerome Levy Economics Institute Working Paper No. 322, Annandale-on-Hudson, N.Y.

Eichengreen, Barry. 2009. “The Crisis and the Euro,” Real Instituto Elcano International Economy and Trade. Working Paper No. 23, Elcano Royal Institute, Madrid, Spain.

European Central Bank. 2010. Euro Area Fiscal Policies and the Problem. Occasional Paper Series No. 9. April 2010.

Feldstein, Martin. Finance: The Euro Risk. Time New York. January 25, 1999.

Feldstein, Martin. 2008. “Will the Euro Survive the Current Crisis?” Project Syndicate. Available online: http://www.nber.org/feldstein/projectsyndicate_eurosurvive.html/

Holmes, Martin. 1997. From Single Market to Single Currency: Evaluating Europe's Economic Experiment. The Bruges Group, Paper No. 20.

International Monetary Fund. 2011. World Economic Outlook, September 2011: Slowing Growth, Rising Risks, Washington, D.C.

International Trade Commission, 2011. ITC Dataweb: dataweb.itc.gov.

Jones, Erik. 2009. “The Euro and the Financial Crisis.” Survival, Vol. 51:2, pp. 41-54.

Kelch, David and Stallings, David. “EC Monetary Union and the CAP: The Hidden Connection.” Atlantic Economic Society. Vol.2 No. 2. July 1992.

Kelch, David;, Shane, Mathew, Torgerson, David, and Somwaru, Agapi. 2011. European Financial Imbalances: Implications of the Eurozone Sovereign Debt Problem for U.S. Agricultural Exports. Economic Research Service, U.S. Department of Agriculture. Outlook Report No. WRS-11-02, May 2011.

Münchau, Wolfgang. 2010. “The Irish Contagion.” Financial Times, London, November 21, 2010

Peters, May, Shane, Mathew, and Torgerson, David. 2009. What the 2008/2009 World Economic Crisis Means for Global Agricultural Trade. Economic Research Service, U.S. Department of Agriculture, Outlook Report No. WRS-09-05, Washington, D.C., August 2009.

Reinhart, Carmen M. and Rogoff, Kenneth S. (2009). “The Aftermath of Financial Crises” presented at the American Economic Association meeting in San Francisco, January 3, 2009.

Rodrigues, Maria Joao. 2010. The Eurozone Crisis and Reforming Economic Governance. Foundation for European Progressive Economic Studies, May 2010.

Shane, Mathew, and Stallings, David. 1987. The World Debt Crisis and Its Resolution, USDA, Economic Research Service, AER-231.

Shane, Mathew, Roe, Terry, and Somwaru, Agapi. 2008. “Exchange Rates, Foreign Income, and U.S. Agricultural Exports,” Agricultural and Resource Economics Review, Vol. 37, No. 2 (Oct. 2008), pp. 160-175.

Shane, Mathew, Liefert, William, Morehart, Mitch, Peters, May, Dillard, John, Torgerson, David, and Edmondson, William. 2009. The 2008/2009 World Economic Crisis: What It Means for U.S. Agriculture, WRS-09-02, USDA, Economic Research Service. March 2009.

Tumpel-Gugerell, Gertrude (member, European Central Bank Executive Board). 2010. “The ECB’s actions during the recent problem and the policy elements needed for a sound recovery.” Speech at the Shanghai Expo Conference on “How can the EU and China Contribute to a Sound and Sustainable Global Economic Recovery?” Shanghai, China, July 3, 2010.

U.S. Department of Agriculture, Economic Research Service. 2013a. Exchange rate data set. Available online: http://www.ers.usda.gov/data/exchangerates/.

U.S. Department of Agriculture, Economic Research Service. 2013b. Global Agricultural Trade System, Foreign Agricultural Service of the U.S. Dept. of Agr. Available online: http://www.fas.usda.gov/gats/default.aspx/.

U.S. Department of Agriculture, Economic Research Service. 2013c. International macroeconomic data set. Available online: http://www.ers.usda.gov/data/macroeconomics/.

Wolf, Martin. 2008. Fixing Global Finance. Baltimore, MD: Johns Hopkins University Press.