The noncitrus tree fruit industry is a vital part of the U.S. agricultural sector, with $21.6 billion in revenues representing nearly 14% of the value of the country’s agricultural production in 2017 (U.S. Department of Agriculture, 2019a). But value of production tells only part of the story of the industry’s importance. Fresh fruit is a fundamental input into other segments of the food economy such as food processing and manufacturing. And since fruit production is typically a highly labor-intensive activity, with wages accounting for more than 25% of production costs in 2017 (U.S. Department of Agriculture, 2020b), the livelihoods of many farm workers are reliant on the industry. Further, U.S. exports comprise roughly 27% of world cherry trade, 13% of apple trade, 8% of plum trade, and 6% of peach and nectarine trade (Food and Agriculture Organization of the United Nations, 2020), making the United States one of the world’s largest exporters of fruit.

National-level statistics on the industry’s importance mask the extent to which the agricultural sectors of many states depend on fruit production. In California, the country’s largest agricultural producer and exporter, noncitrus fruits accounted for more $10.6 billion of revenues (more than 25% of the state’s crop production value) and nearly $3 billion dollars in export sales (U.S. Department of Agriculture, 2020a). Similar figures for Washington ($3.4 billion in total revenues), Oregon ($473 million), Michigan ($415 million), and other states reflect the industry’s fundamental role in the farm sectors of large fruit-producing states (U.S. Department of Agriculture, 2020a).

Despite its importance, the industry has in recent years been beset by significant ongoing challenges and structural changes. In this article, we describe these trends in the noncitrus tree fruit industry (focusing on apples, cherries, peaches, pears, and plums, the top five noncitrus tree fruits by total value of production), detailing how stagnant or falling production of many fruits, declines in acreage, consolidation of production, labor supply issues, changing demand patterns, and trade competition have shaped the current situation in the sector. We further discuss potential policy responses that could be undertaken to ensure the viability of the sector.

Table 1 documents the phenomenon of declining production of several major tree fruits over time (we also include grapes because growers of several major tree fruits frequently convert their orchards to grape production). After declining for most of the past two decades, apple production has only recently reattained levels seen in the late 1990s. Fruits such as peaches, pears, and plums have been afflicted by protracted declines in production. As an exception, cherry production has increased noticeably, but cherries are not produced in the same quantities as other major fruits.

| Average Annual Production (1,000 tons) | % Change | ||||

| 1997-2001 | 2002-2006 | 2007-2011 | 2012-2017 | 1997-2017 | |

| Apples | 5,106.0 | 4,720.8 | 4,712.4 | 5,297.8 | 3.8 |

| Cherries | 370.3 | 354.4 | 454.8 | 487.6 | 31.7 |

| Grapes | 6,831.0 | 6,883.0 | 7,289.0 | 7,873.0 | 15.3 |

| Peaches | 1,244.0 | 1,206.0 | 1,117.2 | 872.6 | -29.9 |

| Pears | 1,021.3 | 873.4 | 896.0 | 823.2 | -19.4 |

| Plums | 762.7 | 630.6 | 547.4 | 417.2 | -45.3 |

While many factors have influenced these declines, the principal outcome of this phenomenon has been substantial reductions in the amount of land devoted to fruit production. As of 2018, total U.S. acreage devoted to major noncitrus fruits stood at roughly 1.5 million acres (compared to a high of roughly 1.9 million acres in 2000), lower than at any point in the previous four decades (U.S. Department of Agriculture, 2019a).

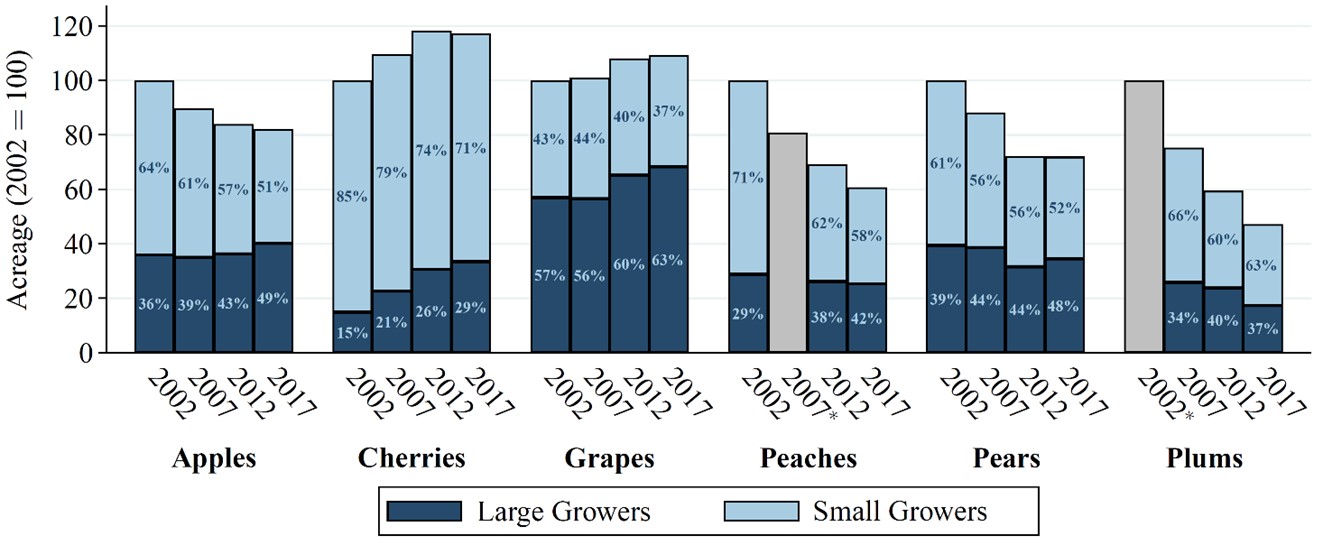

Notes: Data from the U.S. Department of Agriculture (2020b).

Bar labels indicate the percentage share of acreage accounted

for by large versus small growers. The cutoff for small versus

large growers is defined here as 250 acres, with the exception

of pears, for which we define the cutoff as 100 acres due to

data availability issues. For disclosure reasons, complete data

on operation size is not publicly available for some fruits/years.

Figure 1 shows total bearing acreage for several major fruits. The trends in acreage largely mirror those in production. The amount of apple-bearing acreage declined by nearly 20% from 2002 to 2017 (in seeming contrast with total apple production, which actually rose slightly over this period, largely due to technological advances and farm consolidation), while peach and pear acreage decreased even more precipitously, with declines of around 40% and 30%, respectively. For plums, acreage in 2017 was less than half of its 2002 level.

Several factors have influenced these broad changes in U.S. noncitrus fruit production, including consolidation of production, rising labor costs, and increased competition from foreign fruit growers. And to a large extent, the decline in production of many fruits has coincided with landowners and operators substituting toward the production of other more lucrative fruits, a practice stemming from changes in the relative profitability of certain fruits—for example, many of California’s apple orchards have been repurposed as vineyards because of the much higher prices fetched by grapes relative to apples (Bland, 2011).

While these changes might simply reflect fruit producers’ rational supply decisions, the perennial nature of fruit production entails substantial switching costs and long-term investments that must be made years before profitable production can be realized. This particular feature of the noncitrus tree fruit sector means that changes in land use and supply have long-lasting impacts and significant implications for producers and consumers.

In line with broader trends in the agricultural sector (MacDonald, Hoppe, and Newton, 2018), fruit production has increasingly consolidated toward fewer (but larger) growers. Figure 1 shows that this trend is not specific to any particular fruit. Focusing first on apples, roughly half of bearing acreage is on large operations of 250 acres or larger, compared to around a third of total bearing acreage 15 years prior (U.S. Department of Agriculture, 2020b). Similar trends (although not as stark) are evident for peaches, pears, and plums. Clear from this portrait of fruit production is that the decline in acreage for many fruits has occurred largely through a significant contraction in the number of small growers. In contrast, cherries have exhibited an upward trend in acreage and production because of growing domestic and foreign demand and declining overseas competition.

Fundamentally, however, the declines in acreage for most commodities have been caused by a dramatic contraction in the number of small operations. Statistics on the number of apple-growing operations in the United States make this clear. Between 2002 and 2017, the number of operations between 5 and 250 acres in size shrank from 8,151 to 4,710, while the number of operations of at least 250 acres largely held steady, only declining from 283 to 269 (U.S. Department of Agriculture, 2020b). While larger operations are likely to reap efficiency gains from their large scale, the increasing degree of consolidation threatens smaller growers’ ability to compete. The concentration of production in the hands of fewer, but larger, growers exacerbates this threat to small growers and the diminished level of competition has further negative implications for consumer welfare.

As one of the most labor-intensive areas of agriculture, ongoing issues with the farm labor supply have put many fruit growers in an uncomfortable position. Growers have acutely felt the impact of rising farm wages and reduced migration rates among farm workers (Taylor, Charlton, and Yúnez-Naude, 2012; Fan et al., 2015; Charlton and Taylor, 2016). Because of this, the share of labor in fruit production has declined slowly but steadily. Since peaking in 2001 at around 33%, labor costs as a share of gross farm income fell below 25% in 2016 (U.S. Department of Agriculture, 2020b).

Mechanization has not taken hold in much of the fruit sector the way that it has in other food and agriculture sectors. This is due in part to the barriers to adoption of technologies unique to fruit production (Gallardo and Sauer, 2018) and to the potential of mechanical harvesting to cause aesthetic damage to fresh fruits intended for retail consumers (Huffman, 2012). Even today, nearly all such fruit is harvested manually, with mechanical methods largely confined to fruits destined for processing. Despite this current limitation, labor-saving technological advances have the potential to drastically reduce demand for farm labor and thereby lower labor costs. The continued development and adoption of such technology will be essential for the industry to maintain its competitiveness in the future.

Also fundamental to the viability of the U.S. fruit sector is the continued presence of H-2A guest workers, who account for a substantial portion of the country’s farm-labor force. While the Trump administration went to great lengths to limit legal immigration under other programs (such as H-1B visas for skilled workers), in the wake of the COVID-19 pandemic the administration took steps to expand and streamline the H-2A program by waiving interview requirements for H-2A applicants (Mohan, 2020). Maintaining a streamlined H-2A program will be crucial for the survival of the fruit industry while the pandemic endures. In addition to such steps, the administration also sought to lower minimum wage rates for H-2A guest workers (Ordoñez, 2020), with the thought that paying farm workers less will help solve the labor supply issues facing producers. Ensuring an adequate supply of labor is of crucial importance for the sector, and a well-functioning H-2A program—one that continues to incentivize guest workers to come and work in the United States—is an essential aspect of this. One of the first acts of the Biden administration was to freeze pending H-2A rules introduced in the waning days of the Trump administration that would have lowered the reimbursement employers are required to provide for migrant workers’ travel to the United States, a sign that the new administration intends to adopt a different approach from its predecessor to farm labor issues.

In line with declines in production, U.S. consumption of many fruits has also fallen steadily. The quantity of apples, cherries, peaches, pears, and plums on grocery store shelves is lower now than it has been in decades. For comparison, annual per capita retail availability of these fruits (a proxy for consumer demand) averaged 28.4 lb per U.S. resident in the 1990s, 25.7 lb in the 2000s, and 24.4 lb over 2010–2017 (U.S. Department of Agriculture, 2019b). These declines have been particularly stark in fruits such as peaches, nectarines, pears, and plums.

The origins of these trends are manifold. Other types of fruit (such as strawberries, pineapples, and mangoes) have become increasingly available to consumers, which causes households to demand less of the traditionally consumed varieties. Consumers might have adjusted their expenditures on fruits because of price or income effects or U.S. consumers’ underlying preferences might simply have evolved such that fruit has become a less important component of food expenditures. Regardless of what drives declining consumption, these patterns represent a threat to the industry’s long-term viability.

Source: United Nations (2020).

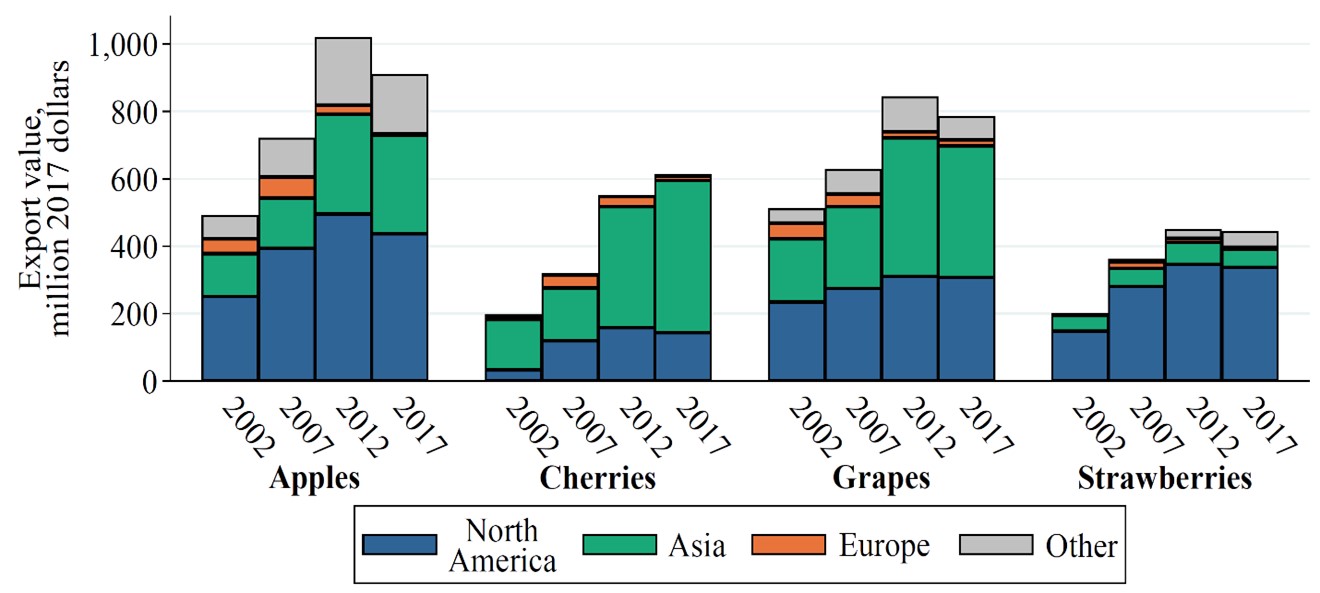

Because of plateaued or declining consumption of many fruits, access to export markets has been an enormous boon for American growers and has generated billions of dollars in revenues. Figure 2 illustrates the extent to which international markets have expanded U.S. fruit sales. For each of the depicted commodities (the top three noncitrus tree fruits by export value, and (for comparison) strawberries, the most exported noncitrus fruit), the real value of sales to foreign markets more than doubled (and in the case of cherries, tripled) from 2002 to 2017.

Most of this growth has come through expanded trade with Canada and Mexico, facilitated by their proximity to and low barriers to trade with the United States. The United States also exports substantial quantities of fruit to Asian markets—not only to traditional trading partners such as South Korea ($486 million of fresh fruit exports in 2017), Japan ($424 million), and China ($320 million), but also to markets that have only recently begun to engage in substantial trade with the United States, such as India ($103 million), Indonesia ($84 million), and Vietnam ($76 million) (United Nations, 2020). These high numbers have risen despite significant import barriers in many of these markets, such as ad valorem tariff rates of 30% on most of India’s fruit imports (United Nations Conference on Trade and Development, 2020). The contraction in U.S.–China trade resulting from the ongoing trade dispute has also dramatically affected exports of U.S. fruit to the region.

While exports to Asia and other North American markets remain large, it is apparent that export growth is rising less quickly than it was 10 years ago; in fact, exports generally stagnated or declined between 2012 and 2017. Also clear is that other markets account for only a tiny part of U.S. fruit exports: Europe, despite its relative accessibility, high incomes, and similar preferences for fruits, imports only limited (and shrinking) quantities of U.S. fruit. Other markets such as South America, the Middle East, and Africa likewise account for small (but growing) export shares.

Source: United Nations (2020).

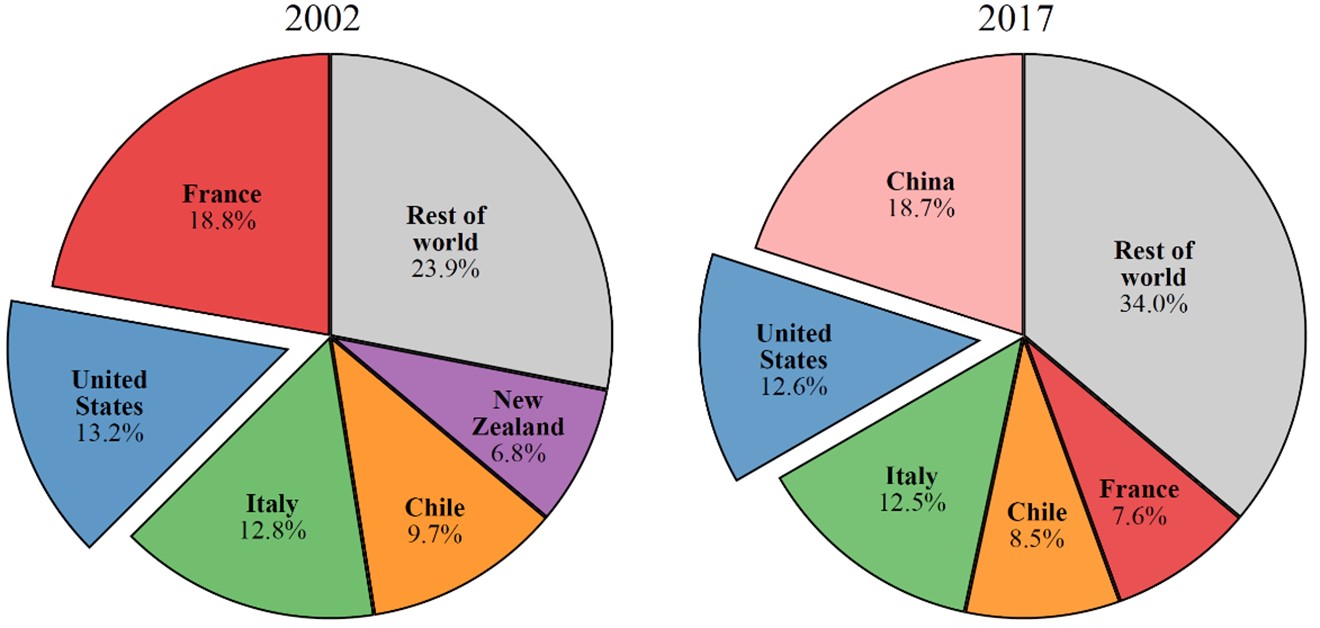

Stagnation in export markets is directly related to the ever-rising degree of competition in international markets. For apples, the most exported U.S. fresh fruit by value, Figure 3 makes clear how the global trade picture has evolved. The U.S. share of world apple trade has diminished slightly, but China’s rapid entry into world fruit markets has been a seismic shock to global fruit supply: Between 2002 and 2017, China’s annual exports of apples increased by approximately 560% (from $208 million to $1.37 billion in 2017 dollars); likewise, China’s exports of pears increased more than 300% (from $136 million to $567 million), and its exports of peaches a staggering 1,800% (from $5 million to $95 million) (United Nations, 2020).

U.S. growers face heightened competition from other producers as well. European apple producers—such as those in Poland—have expanded exports considerably, with the real value of Poland’s apple exports growing by more than 550%, from $72 million to $475 million, between 2002 and 2017 in the wake of its entry to the European Union (United Nations, 2020). Apple producers in other countries (such as Chile and New Zealand) have also seen their international sales increase. Such is also the case in global markets for other fruits—for example, Chile expanded its cherry exports from $51 million to $610 million over the 2002–2017 period, a 12-fold increase, and Turkey’s peach exports expanded from $11 million to $86 million over the same period, a 684% increase. The current international market environment has only added to the pressure faced by U.S. producers; declining consumption and processing demand for many fruits means that U.S. growers rely more than ever on export markets.

The U.S. fruit sector faces challenges on several fronts—declining production and acreage, consolidation, labor shortages, changing consumer preferences, and ever-rising international competition. These challenges have no single origin, nor does a single remedy exist with which to address them. However, there are several strategies that policy makers can emphasize to encourage the long-term sustainability of this vital part of American agriculture.

With the supply of farm labor in the United States continuing to decline, the long-term competitiveness of the sector will depend on process innovation and investment in labor-saving technologies. For growers, this could include introducing new varieties, planting high-density orchards with more efficient layouts, and increasing their use of harvesting machinery.

The problem suggests a clear role for policy makers in incentivizing research and development and technology adoption. Technological innovation and substitution from labor to capital has the potential to enhance the global competitiveness of U.S. fruit growers and to increase the productivity of the workers that remain in agriculture, which could lead to higher wages and reduce the physical impacts of fruit picking on workers. Gallardo and Sauer (2018) note that the main promise of automation is not that it will displace labor but that it will offer farm workers the opportunity to take on high-skill occupations higher up in the agricultural value chain. Simplifying and reducing the cost of H-2A visas could also be a boon in the medium run while labor-saving technology is being developed and adopted.

While American fruit growers face ever-rising competition from foreign producers, the opportunities promised by international markets suggest that the long-term viability of the sector will continue to hinge on export opportunities. Policy makers should make every effort to expand foreign-market access, both by strengthening ties with existing partners and by gaining concessions in markets that U.S. fruit does not reach in large quantities. Along these lines, future presidential administrations would be wise to reconsider the country’s abandonment of the Trans-Pacific Partnership (the TPP, rechristened and enacted without the United States as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership, to which many of the original signatory countries are party) and exert more effort toward concluding the currently stalled negotiations on the Transatlantic Trade and Investment Partnership (T-TIP) with Europe.

The nature of perennial production implies that the trends in the noncitrus tree fruit sector that we highlight will have long-lasting, hard-to-reverse impacts on the supply and demand for fruit. But while the U.S. noncitrus fruit sector faces several headwinds, there are many reasons for optimism about the industry’s future. On the consumer side, fruits such as apples and cherries continue to be enduringly popular with American consumers and have become well-established in many foreign markets. For producers, technological advances in production and harvesting and the continued development of new fruit varieties and production practices will continue to ensure that American fruit growers are among the most efficient and innovative in the world. And if steps are taken to address the challenges faced by the industry, the U.S. fruit sector will be able to maintain its cornerstone position in American agriculture.

Bland, A. 2011, November 1. “California’s Disappearing Apple Orchards.” Smithsonian Magazine.

Charlton, D., and J.E. Taylor. 2016. “A Declining Farm Workforce: Analysis of Panel Data from Rural Mexico.” American Journal of Agricultural Economics 98(4): 1158–1180.

Fan, M., S. Gabbard, A. Alves Pena, and J. Perloff. 2015. “Why Do Fewer Agricultural Workers Migrate Now?” American Journal of Agricultural Economics 97(3): 665–679.

Food and Agriculture Organization of the United Nations. 2020. FAOSTAT Statistical Database.

Gallardo, R.K., and J. Sauer. 2018. “Adoption of Labor-Saving Technologies in Agriculture.” Annual Review of Resource Economics 10: 185–206.

Huffman, W. 2012. “The Status of Labor-Saving Mechanization in U.S. Fruit and Vegetable Harvesting.” Choices 27(2).

MacDonald, J., R. Hoppe, and D. Newton. 2018. Three Decades of Consolidation in U.S. Agriculture. Washington, DC: U.S. Department of Agriculture, Economic Research Service, Economic Information Bulletin EIB-189, March.

Mohan, G. 2020, March 27. “State Department Eases Coronavirus Bottleneck for Foreign Farmworkers.” Los Angeles Times.

Ordoñez, F. 2020, April 10. “White House Seeks to Lower Farmworker Pay to Help Agriculture Industry.” National Public Radio.

Taylor, J.E., D. Charlton, and A. Yúnez-Naude. 2012. “The End of Farm Labor Abundance.” Applied Economic Perspectives and Policy 34(4): 587–598.

United Nations. 2020. Comtrade Statistical Database. Available online: https://comtrade.un.org/.

United Nations Conference on Trade and Development. 2020. Trade Analysis Information System (TRAINS) Database. Available online: https://databank.worldbank.org/reports.aspx?source=UNCTAD-~-Trade-Analysis-Information-System-%28TRAINS%29 .

U.S. Department of Agriculture. 2019a. Fruit and Tree Nuts Outlook, September 2019. Washington, DC: U.S. Department of Agriculture, Economic Research Service.

U.S. Department of Agriculture. 2019b. Food Availability (Per Capita) Data System. Washington, DC: U.S. Department of Agriculture, Economic Research Service.

U.S. Department of Agriculture. 2020a. Farm Income and Wealth Statistics Database. Washington, DC: U.S. Department of Agriculture, Economic Research Service. Available online: https://www.ers.usda.gov/topics/farm-economy/farm-labor.

U.S. Department of Agriculture. 2020b. QuickStats Database. Washington, DC: U.S. Department of Agriculture, National Agricultural Statistics Service. Available online: https://quickstats.nass.usda.gov/.