4th Quarter 2013

Futures markets offer a means by which commodity producers and users can reduce price risk through hedging. Forward pricing using futures contracts is based on the premise that, over time, the local cash price and futures prices move together. Therefore, adjusting for local conditions, pricing in the futures market is a close approximation to pricing in the cash market. Futures markets then determine the value of many agricultural commodity spot markets and forward contracts. Hedgers are required to make margin deposits with their brokers to insure they can meet their financial obligations. Funds held in margin accounts as a performance bond are assumed to be secure, safely held in segregated accounts at the brokerage firm.

Since 2007, the environment for trading futures and options has changed: prices have become more volatile, futures and cash prices have not converged at historically normal levels, and margin account funds have been misappropriated. This article reports on an analysis used to determine if farmers’ attitudes and behaviors have changed in regards to futures markets given these developments. Participants in Master Marketer, a 64-hour risk management educational program sponsored by Texas A&M AgriLife Extension Service, were surveyed to see if futures and options are still perceived as viable tools of price risk management in today’s turbulent economic environment.

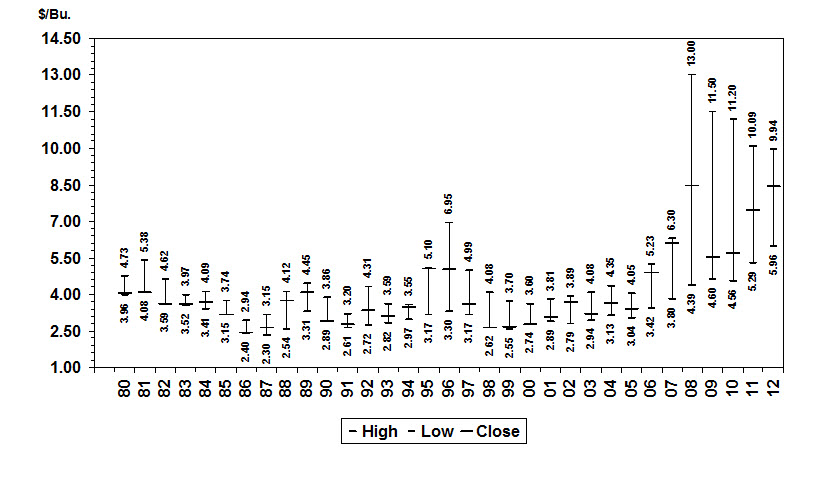

A major feature of the boom in commodity prices since the mid-2000s is the dramatic increase in price volatility (Baffes and Haniotis, 2010; Carter, Rausser, and Smith, 2011; and Karali, and Power, 2013). For example, the average difference between the contract high and the contract low for the July Kansas City Board of Trade (KCBT) wheat futures contract from 1980 to 2006 was $1.17 per bushel (Figure 1). From 2007 to 2012, the average range increased to $5.57 per bushel. During five of the years between 1980 and 2006, the high-low range in prices was less than the current daily trading limit of $0.60 per bushel (1983, $0.45; 1985, $0.59; 1986, $0.54; 1991, $0.59; and 1994, $0.58). Volatile markets increase hedging costs associated with financing margin calls. Maintaining a margin account during a major price move against the trader can exceed the credit limits of many hedgers. The price spike of 2008 caused unprecedented margin calls forcing several large cotton merchant firms and some small- to mid-sized grain elevators to exit the industry (Carter and Janzen, 2009; Hailu and Weersink, 2010).

Another feature of the commodity price boom is the lack of convergence—the futures price at expiration has more recently been beyond any historical norms of comparison to local cash markets (Irwin, Garcia, Good, and Kunda, 2008). Forward pricing using futures contracts is based on the premise that, over time, the local cash price and futures prices move together and that these prices will draw together when the futures contract expires or converge to a predictable level. Therefore, adjusting for local conditions, pricing in the futures market is a close approximation to pricing in the cash market. Cash and futures markets that fail to converge leave hedgers unprotected from price risk (Adjemian, Garcia, Irwin, and Smith, 2013).

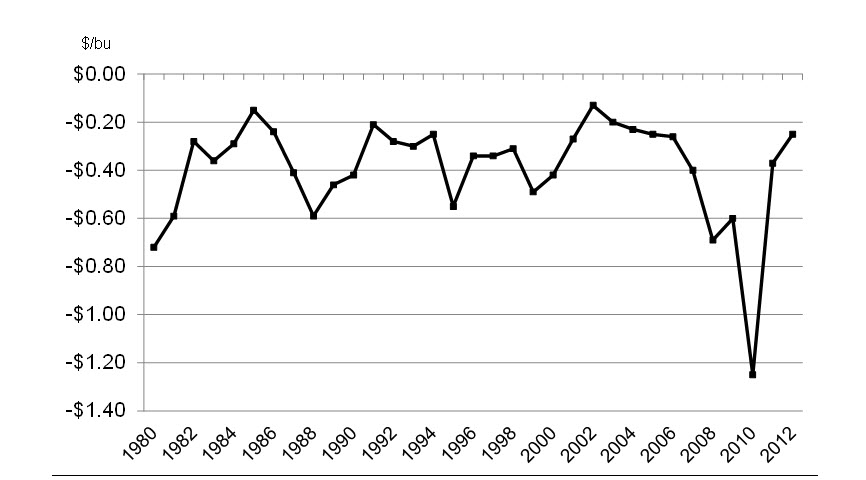

Again using a wheat example, the region of Texas that accounts for the highest concentration of wheat production is identified in market reports as “Area North of the Canadian River” (USDA Market News, 2013). The Canadian River bisects the Texas Panhandle from west to east just north of Amarillo. The harvest basis in this region for the last 30 years has varied by roughly $.40 per bushel, ranging from $0.20 under to $0.60 under the July KC futures (Basis Project, 2013). This basis in 2010 plunged to $1.25 under July KC futures (see Figure 2). With futures prices around $4.85 at harvest, cash wheat prices in the Texas Panhandle fell to around $3.60 per bushel. Some areas in central Texas reported basis levels in excess of $2.00 under July futures—putting cash wheat prices below $3.00 per bushel in the summer of 2010. This lack of convergence to a more average historic level left hedgers exposed to additional price risk.

Compounding the hedging expense and risk exposure associated with volatility and convergence, two futures commission merchants—MF Global and Peregrine Financial Group—about the same time were found to have misappropriated customer funds.

“While companies often make bad decisions and fail, no one expected the violation of one of the foundational principles of the futures markets: the protection of customer money. On Monday, October 31, at 2:30 in the morning, MF Global revealed that an estimated $900 million in customer money had gone missing—unaccounted for. MF Global filed for bankruptcy a few hours later.” --Stabenow, 2011

Then in July 2012, the chief executive officer of Peregrine Financial Group was arrested for fraud in a 20-year scheme in which more than $200 million in customer funds went missing. John Roe, co-founder of the Commodity Customer Coalition, in testimony before the U.S. Senate Agriculture Committee examining the futures markets in response to the failures of MF Global and Peregrine Financial Group, described the problem this way: “An industry which just a year ago prided itself that no customer had ever lost a penny as the result of a clearing member default now hopes customer losses due to broker insolvencies will be limited to hundreds of millions of dollars, instead of billions of dollars.” (2012) The Commissioner of the Commodity Futures Trading Commission, Jill Sommers, added, “…customers correctly understood the risks associated with trading futures and options, but never anticipated that their segregated accounts were at risk of suffering losses not associated with trading.” (2012)

These combined factors have created a climate in which confidence and trust in the use of futures contracts as an effective tool for price risk management may have been lost. Anecdotal evidence from some Texas producers reflected a possible change in their views of hedging due to these factors. In order to assess the degree to which these factors have impacted the risk management strategies of agricultural producers, this study surveys past participants in the Texas A&M AgriLife Extension Master Marketer program. While the group is not representative of all producers in Texas or the nation, it represents a sample of farmers and ranchers, merchandisers, and lenders with training and experience in the use of futures and options for hedging.

In the 1990s, Texas A&M AgriLife Extension Service economists developed an in-depth risk management education program that became known as Master Marketer. The intensive, 64-hour risk management course focuses on marketing plan development and implementation; developing enterprise budgets and breakeven costs; and basic and advanced marketing tools including futures and options, basis, financial risks, fundamental and technical analysis, production risk alternatives (crop insurance, diversification, and integration), agricultural policy, international trade, value added processes, niche markets, and marketing clubs. As of 2013, 25 Master Marketer programs have been conducted in Texas with 1,051 graduates.

With an average age of 45, Master Marketers are younger than the average Texas farmer whose average age is 59 years (U.S. Department of Agriculture-National Agricultural Statistical Service (USDA NASS), 2009. Master Marketers mange an average of 2,422 crop acres, placing them in the 95th percentile of all farms in Texas. Master Marketers have a median gross income of $437,500. According to USDA’s 2007 Census of Agriculture, only 4.2% of farms in Texas reported gross incomes of $250,000 or more. The tendency for Master Marketer graduates—producers who are younger, have larger operations, and have received marketing training—to use futures and options is consistent with other studies that found these characteristics to be important in the use of futures and options for price risk management (Musser, Patrick, and Eckman, 1996; Goodwin and Schroeder, 1994; Makus, Lin, and Krebill-Prather, 1990; Asplund, Forster, and Stout, 1989). A more detailed discussion of the characteristics of Master Marketer participants can be found in Qin et al. (2011)

A key component of the Master Marketer program is a 2.5 year post-program survey of knowledge gains, practices implemented, and economic impact of participation in the program (Qin et al., 2011). Master Marketer graduates report a consistent increase in their understanding and willingness to use marketing concepts ranging from budget analysis and developing a marketing plan to general risk management, and crop and livestock marketing strategies including futures and options (McCorkle et al., 2009).

Some of the important questions addressed by the survey of Master Marketer graduates regarding the current risk environment of using futures and options for hedging included:

Surveys were sent to 911 Master Marketer program graduates still involved with agriculture and for whom there was valid contact information. A total of 127 usable surveys were returned. Demographic characteristics of survey respondents matched closely with the general profile of all Master Marketers in terms of age, farm size, farm revenue, and education.

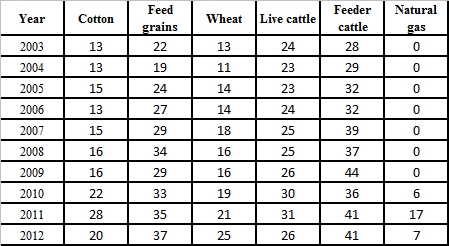

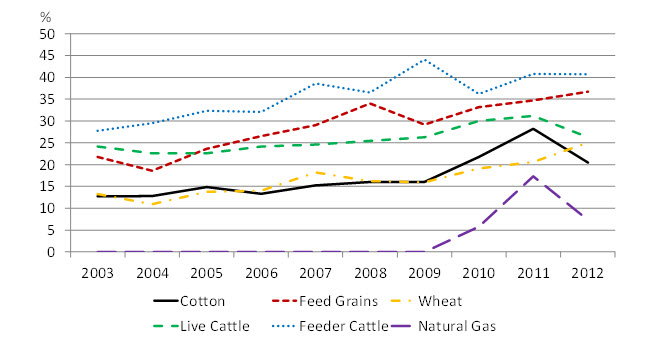

Findings show that, despite increased volatility, convergence issues, and margin fund security, Master Marketer graduates trained in the use of futures and options are, generally, hedging more rather than less. In reporting the percent of total production that was hedged with either futures or options, the average for all commodities from 2003 to 2007 was 18%; this increased to 25% for the 2008 to 2012 time frame. As might be expected the percent hedged varied by commodity (2003 compared to 2012): cotton from 14% to 21%, feed grains (corn and sorghum) from 22% to 36%, wheat from 11% to 25%, live cattle from 25% to 27%, and feeder cattle from 22% to 43% (Table 1 and Figure 3). A 20% increase was shown in the “other” category that represented primarily rice production.

Asked if they used other marketing tools for risk management in addition to or instead of futures and options, 67% reported that they did use other risk management practices. Responses included mostly cash contracts, marketing pools, crop insurance, and grain storage. When asked if they used a marketing advisory service, 53% responded “yes.”

The most intriguing question of the survey, “Have you stopped or will you stop hedging altogether?” was answered “no” by 84% of the respondents. When asked if they had replaced or intended to replace futures/options hedging with some other risk management practices, the leading responses were to increase the use of cash contracting, pool marketing, and crop insurance.

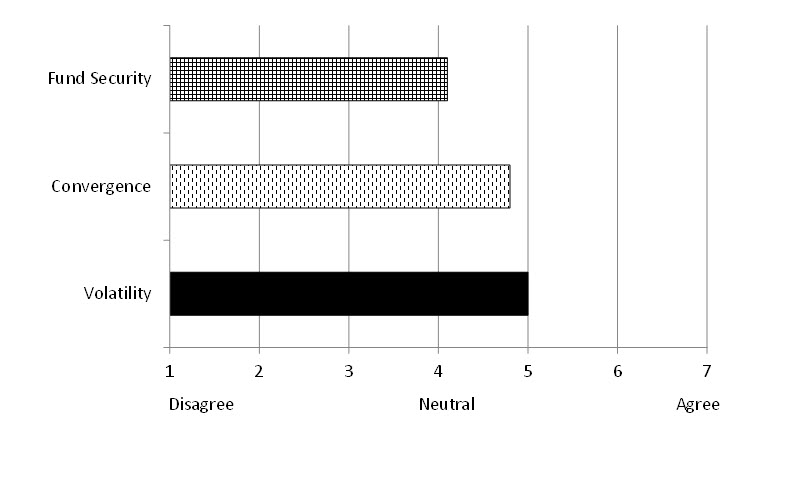

Survey participants were asked to provide a scaled response to survey questions regarding disagreement or agreement (1 to 7, 1 = disagree, 7 = agree) with statements related to volatility, convergence and basis volatility, and margin fund security (Figure 4). When asked if increased futures price volatility and associated margins and options premiums are a serious impediment to the use of futures or options markets for risk management, the average of responses was 5.0 reflecting general agreement with that statement. Of the 122 who responded to that question, 63% responded with a scaled response of five or higher; 25% answered at level 7.

For the statement “More variable basis and less reliable convergence between futures prices and cash prices are a serious impediment to my use of futures and options markets for risk management,” the average response was 4.8, slightly lower than the level of agreement on the volatility statement but still may be seen as expressing general agreement. Of the 122 who responded to this statement, 57% rated their level of agreement 5 or higher, while 18% rated their level of agreement a seven.

Regarding fund security, for the statement “Margin account security with a brokerage house is a serious impediment to my use of futures and options markets for risk management,” the average level of agreement was 4.1, a more neutral response. Agreement was rated 5 or higher by 35% of 123 respondents; 11% agreed at level seven.

Results of this survey indicate that those who have received Master Marketer training are not likely to stop hedging with futures and options in spite of volatility, convergence issues, and fund security. Farmers trained in the use of futures and options continue to use them as viable tools to manage price risk.

Results also suggest that as farm income increases, a farmer is less likely to have stopped using futures and options for hedging. Larger farms have the resources to fund margin accounts and pay higher option premiums relative to smaller farms. Increasingly larger farms may be more professional in their approach to risk management, utilizing a broader range of tools. While farms of all sizes need to manage price risk, large farms may be better able to absorb the risk inherent in the current commodity price environment.

As farmers age there is an indication of an increased likelihood of discontinuing the use of futures and options. Older farmers may view the benefits of risk management using futures and options outweighed by the risk inherent in their use, given either their degree of wealth or goals associated with their business (retirement security versus growth, for example). Older farmers may have a bias towards risk and prices set years ago by previous experience, in that option prices and margin requirements today are “just too high.” These findings are consistent with other studies that have found decreases in risk aversion as wealth increases and increases in risk aversion with advancing age (Martin and Eisenhauer, 2001; and Riley and Chow, 1992). Older farmers may be in a financial position that enables them to ’self-insure’ against price risk.

Many stakeholders in the futures industry—producers, commercial interests, legislators, regulators, the exchanges themselves—have expressed concern that traditional hedgers will abandon the futures market due to the concerns analyzed in this research. While recent developments in the futures markets may have caused some farmers and ranchers to stop hedging with futures and options, the results of this analysis suggest that for a specific population of producers who have received intensive risk management training, the overall trends in utilization of these marketing tools is increasing. In addition, farmers and ranchers who have stopped using futures and options markets report an increased use of other price risk management tools such as cash contracting, crop insurance, and marketing pools. A focus on understanding and using futures and options markets continues to be a viable component of risk management education.

Adjemian, Michael K., Garcia, P., Irwin, S., and Smith, A.. (2013). Non-Convergence in domestic commodity futures markets: causes, consequences, and remedies, EIB-115. U.S. Department of Agriculture, Economic Research Service.

Asplund, N.M., Forster, D.L., and Stout,T.T. (1989). Farmers’ use of forward contracting and hedging. Review of Futures Markets. 8, 24-37.

Baffes, John and Haniotis, T. (2010). Placing the 2006/08 Commodity Price Boom into Perspective. World Bank Policy Research Working Paper Series. Available online: http://ssrn.com/abstract=1646794.

Basis Project. Extension Agricultural Economics, Department of Agricultural Economics, Texas A&M University. Available online:http://agecoext.tamu.edu/programs/marketing/master-marketer-program/basis-website.html.

Carter C.A., Rausser, G.C., and Smith, A. (2011). Commodity booms and busts. Annual Review of Resource Economics 3, 87-118.

Carter, Colin A., and. Janzen, J.P. (2009). The 2008 cotton price spike and extraordinary hedging costs. Agricultural and Resource Economics Update 13, 9-11.

Goodwin, Barry K. and Schroeder,T.C. (1994). Human capital, producer education programs, and the adoption of forward-pricing methods. American Journal of Agricultural Economics. 76(4), 936-947.

Hair, Joseph F. Jr., Rolph E. Anderson, R.E., Tatham, R.L.,and Black, W.C. (1998). Multivariate data analysis, Patparganj, India: Pearson Education.

Hailu, Getu and Alfons Weersink. (2010). Commodity price volatility: the impact of commodity index traders. Canadian agricultural trade policy and competitiveness research network, Commissioned Paper 2010-02. Available online: http://www.uoguelph.ca/catprn/PDF-CP/Commissioned_Paper_2010-2_Hailu+Weersink.pdf.

Halek, Martin and Joseph G. Eisenhauer. (2001). Demography of risk aversion. The Journal of Risk and Insurance, 68(1), 1-24.

Irwin, S.H., Garcia, P., Good, D.L., and Kunda, E.L. (2008). Recent convergence performance of CBOT corn, soybean and wheat futures contract. Choices, 23(2), 16-21.

Karali, Berna, and Gabriel J. Power. (2013). Short- and long-run determinants of commodity price volatility. American Journal of Agricultural Economics. 95(3), 724-738.

McCorkle, D.A., Waller, M.L. Amosson, S. H., Bevers, S.J., and Smith, J.G. (2009). The economic impact of intensive commodity price risk management education. Journal of Extension, 47(2), No. 2RIB7.

Makus, L.D., Lin, B.H., Carlson, J., and Krebill-Prather. R. (1990). Factors influencing producer decisions on the use of futures and options in commodity marketing. University of Idaho Department of Agricultural Economics and Rural Sociology A.E. Research Series 90-09.

Musser, W.N., Patrick, G.E., and Eckman, D.T. (1996). Risk and grain marketing behavior of large-scale farmers. Review of Agricultural Economics, 18(1), 65-77.

Newsom, Jason T. Logistic regression, data analysis II, Portland State University. (2012). Available online: http://www.upa.pdx.edu/IOA/newsom/da2/ho_logistic.pdf.

Peterson, Paul E. Behind the collapse of MF Global. (2013). Choices, (2nd Quarter). Available online: http://www.choicesmagazine.org/choices-magazine/submitted-articles/behind-the-collapse-of-mf-global.

Qin, Xiaoyan,. Nayga, R. M., Ximing Wu, Mark L. Waller, M.L., McCorkle, D.A., Amosson, S.H.. Smith, J.G., and Bevers, S.J. (2011). Master Marketer program: analysis of 9 years of evaluation results. Faculty paper series, FP 2011-5. Department of Agricultural Economics, Texas A&M University, College Station, TX. Available online: http://agecon.tamu.edu/publications/publications_faculty_papers_and_reports.html.

Riley, William B. Jr. and K. Victor Chow. (1992). Institute asset allocation and individual risk aversion, Financial Analysts Journal, 48(6), 32-37.

Roe, John. Statement before the U.S. Senate Committee on Agriculture, Nutrition, and Forestry. (2012, August 1). Available online: http://www.ag.senate.gov/hearings/examining-the-futures-markets-responding-to-the-failures-of-mf-global-and-peregrine-financial-group.

Sommers, Jill. Statement before the U.S. Senate Committee on Agriculture, Nutrition, and Forestry. (2012, August 1). Available online: http://www.ag.senate.gov/hearings/examining-the-futures-markets-responding-to-the-failures-of-mf-global-and-peregrine-financial-group.

Stabenow, Debbie. Opening Statement, Investigative Hearing on the MF Global Bankruptcy, U.S. Senate Committee on Agriculture, Nutrition, and Forestry. (2011, December 31). Available online: http://www.ag.senate.gov/hearings/investigative-hearing-on-the-mf-global-bankruptcy.

U.S. Department of Agriculture Market News. Texas Hi Plains Elevator Grain Bids. (2013). Available online: http://www.ams.usda.gov/mnreports/am_gr110.txt.

USDA National Agricultural Statistics Service. (2007). Census of Agriculture: United States Summary and State Data, Vol. 1, Part 51. Available online: http://www.nass.usda.gov/Statistics_by_State/Ag_Overview/AgOverview_TX.pdf.