The U.S. dairy industry entered 2020 with an optimistic farm milk price outlook that had been largely missing for the previous five years. When the COVID-19 pandemic struck the United States in March and April 2020, some of the more compelling images were of dumped milk on farms and discussion about “broken” supply chains. This paper examines the dairy market disruptions and adjustments related to the pandemic.

While much has been made in recent years of declining fluid consumption, total U.S. dairy product consumption per capita has actually increased—led by increases in cheese and butter consumption. Cheese sales have been steadily increasing for decades. Italian style cheeses, in particular mozzarella, have grown impressively in volume, but recent growth also traces to more exotic, specialty cheeses ranging from Camembert to queso blanco, Grana Padano, and feta. Butter and other cream-rich products have enjoyed more recent growth as health concerns around fat consumption have moderated and many consumers choose to indulge themselves from time to time. Coffee shops have boosted cream sales, and whole milk and full-fat ice cream have gained market share. Until recently, these domestic consumption shifts have fueled increasing prices for the butterfat component of milk relative to nonfat components. Indeed, the primary growth market for skim milk and whey powders has been international markets. While foreign customers have been a welcome source of demand, international markets are highly price competitive around dairy commodities.

A major driver of domestic consumption has been food away from home (FAFH). The growth in mozzarella (pizzas) and processed cheeses (burgers and sandwiches in quick or limited-service restaurants) can be traced to the explosion in “fast food” dining beginning in the 1970s. After long trending to that result, in 2009, expenditures on FAFH exceeded at-home food consumption, although the quantity of food eaten at home remains larger (U.S. Department of Agriculture, 2020b).

People eat differently away from home, both in terms of quantities and types of foods. For dairy products, there are several important differences. First, fluid milk is primarily consumed at home but not in restaurants, although school and other institutional cafeterias are an important outlet away from home. Second, butter is more favored, particularly in full-service restaurants. Third, although ice creams remain a popular dessert in both full service and limited-service formats, as well as for take away consumption, total consumption for these products has been in mild decline. Finally, many cheeses—including mozzarella and other Italian styles, feta, and blue—are more favored in restaurants; others, such as processed or American slices, provolone, and Swiss are popular deli or sandwich cheeses. Anecdotal industry estimates suggest that about 50%–60% of cheese and 45%–55% of butter were consumed away from home prior to the pandemic (Allied Market Research, 2020).

| Month | Food at Home | Food Away from Home | Total Food Sales |

| January | 2.5 | 4.5 | 3.5 |

| February | 3.9 | 2.6 | 3.2 |

| March | 20.6 | -26.2 | -4.0 |

| April | 7.3 | -49.4 | -22.4 |

| May | 9.0 | -35.6 | -14.3 |

| June | 7.0 | -22.2 | -8.4 |

| July | 9.6 | -17.3 | -4.5 |

| August | 5.6 | -16.0 | -5.7 |

| September | 9.3 | -11.5 | -1.5 |

| October | 9.0 | -10.2 | -0.9 |

| November | 6.2 | -16.2 | -5.0 |

| December | 7.5 | -18.2 | -5.2 |

Source: U.S. Department of Agriculture (2020c).

In late March and into early April 2020, as the scope and seriousness of the COVID-19 pandemic became clear, food service establishments shut down in large numbers and U.S. consumers in many states sheltered at home. Table 1 displays the monthly change in 2020 food expenditures compared to a year earlier. FAFH expenditures declined 26% in March and more than 49% in April compared to 2019 before experiencing smaller, but still significant, year-over-year declines in May and June (U.S. Department of Agriculture, 2020b). At the same time, food at home (FAH) expenditures surged by 20.6% in March over 2019 levels with 7%–9% increases in April–June. Total food expenditures declined 4% in March and 22%, in April in part because FAFH includes a higher percentage of taxes and tips. Total food expenditures recovered in late summer but then fell again YOY as COVID cases rose around the holidays. For 2020 as a whole, FAH expenditures were +8.1% over 2019, FAFH expenditures were -18.4% YOY, and total food expenditures were -5.6% compared to 2019.

The sudden decline, and in many cases outright stoppage, of food service sales shifted the products that were consumed, but the results were nuanced and fairly short-lived in some cases. Sales of fluid milk had been declining since 2010. This trend continued in 2020, with January consumption 4.4% below 2019. Fluid milk was one of the major products hit with panic buying, despite being a highly perishable product. By February, the decline had slowed and in March it spiked by +7.5% YOY (year over year). As was true for other “hoarded” products and grocery sales in general, the first wave spike was followed by a decline, but fluid production spiked to 7.3% YOY growth again in June, this time more in response to food donations. The U.S. Department of Agriculture only reports “domestic disappearance,” a proxy for consumer purchases, for two large cheese categories—American cheeses (primarily cheddar and similar styles) and other cheeses (primarily mozzarella but also including all other styles). With such large aggregate categories, it is difficult to discern the larger ups and downs for individual styles. In total, American-style cheeses, which play a big role in food service but also enjoyed lively sales in grocery stores, saw a modest spike in March but retreated almost 10% in April YOY (U.S. Department of Agriculture, 2020b). Other cheeses followed a similar pattern, with an 11% drop in April despite a stronger start earlier in the year. Thus, the net effect of food service closures and higher retail sales proved to be negative for the cheese category, but clearly there were offsets between the two channels. This sector also serves as a good example of the fact that restaurants that had a strong takeout and/or delivery model fared much better among all restaurants, and the perfect example is pizza parlors. Hence, mozzarella sales were unusually strong. Butter also proved to be an example of a product that benefited to a degree from food service closures despite its strong presence in that channel. Sales spiked 18% YOY in March and were unusually high in the summer of 2020 as well (U.S. Department of Agriculture, 2020b).

The varied impacts for different dairy foods also meant very different impacts to processors and their ability to respond. Dairy manufacturing plants tend to be highly specialized, and this extends to packaging equipment. Small-scale plants, including some farmstead processors, who produced specialty cheeses for restaurants suddenly found themselves with no sales whatsoever. Large plants that were designed to produce shredded mozzarella for pizza parlors or bulk processed cheeses for quick-service restaurants typically often do not have the equipment to manufacture consumer packages required for retail sales. Larger companies, including co-operatives, may have a suite of processing plants, but this does not always mean that it is easy or even feasible to move milk from a plant with low product demand to a plant with high product demand. This is especially true during spring flush months, when milk production is seasonally high and plants tend to be running at or near full capacity. Additionally, nutrition labelling and similar packaging requirements for retail do not apply to bulk packages used in food service. This means that even if consumers are willing to buy a 25-kg box of butter or a 5-lb loaf of processed cheese, these packages often cannot be legally sold at retail. FDA did allow some waivers on packaging requirements, but bulk packaging still remained the wrong size for most consumers. Thus, the disruption to food service outlets had consequences that varied by product type as well as by the structure of the processing business.

In recent years, the dairy supply chain, as many others, has focused on efficiency and cost minimization, exemplified by lean manufacturing techniques and just-in-time delivery. Under the assumption that transportation systems are very robust, these strategies seek to minimize operating, procurement, and distribution costs, and a key strategy is minimizing storage of either inputs or outputs. One result of the emphasis on lean, efficient supply chains is that it is difficult to respond to a dramatic and sudden demand shift. The current descriptor is to say these systems are lean but brittle. This was evident in the dairy sector. Nevertheless, very-short-term voids in retail spaces notwithstanding, it is our opinion that the dairy supply chain proved surprisingly resilient.

U.S. farm milk prices have followed a roughly three-year cyclical pattern since the mid-1990s (Novakovic and Wolf, 2016). Following an extreme high in Fall 2014, a host of national and international market factors resulted in farm milk prices being stuck at a relatively low-level equilibrium for about five years, until the second half of 2019. This period resulted in increased farm consolidation and exit while the lack of payments made under the existing 2014 Margin Protection Program for Dairy created a favorable environment to revamp that program in the 2018 Farm Bill. The resulting Dairy Margin Coverage Program, with more generous protection on the first 5 million pounds of covered milk production, has proven to be much more likely to result in significant income subsidies, especially for dairy farms of average size or smaller.

The market characteristic that led to the prolonged period of below average returns—even in 2017, which was a modestly better farm milk price year—was that growth in milk production was slightly above trend and growth in dairy product demand growth was slightly below trend. Growing production accompanied by slowed demand growth resulted in occasions of milk being dumped in certain regional markets that lacked manufacturing to make storable dairy products and balance markets (Novakovic and Wolf, 2018).

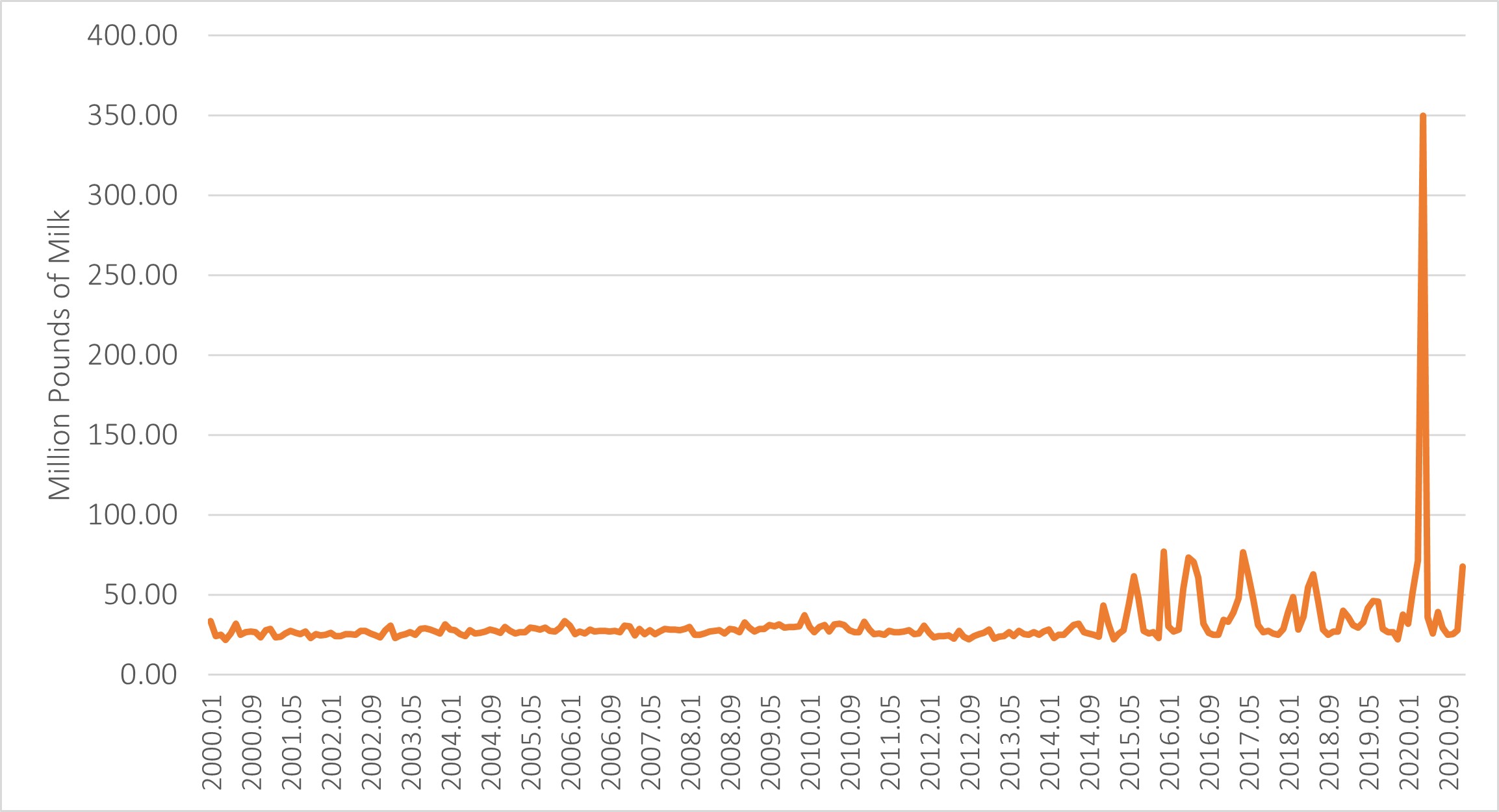

Source: U.S. Department of Agriculture (2020a).

Source: U.S. Department of Agriculture (2020d).

The amount of milk that is dumped, which means that milk was disposed of in a manure lagoon or fed to livestock rather than entering a market outlet, may be reported to and recorded by Federal Milk Marketing Orders (FMMOs). There are pricing advantages to doing this, as the milk earns a price under order regulations rather than having no value, but reporting or “pooling” is by no means automatic or required. A small amount of milk is dumped in each month in every milk marketing order due to weather, plant closures, and other issues (Novakovic and Wolf, 2018). In spring 2020, milk dumping increased across all orders as the aforementioned food consumption and demand shocks occurred. The amount and extent of local milk dumping depended on the market supply and processing situation but FMMO statistics can capture the aggregate picture. Figure 2 displays the amount of milk dumped monthly in all Federal Milk Marketing Orders January 2000 through December 2020. While the past five years witnessed an increase in seasonal dumping, generally during the Spring flush months, nothing compared to the April 2020 amount of 349 million pounds (approximately 40.6 million gallons) dumped nationally. The largest regional quantity dumped was 131 million pounds in the Northeast FMMO.

Typically, 0.2 %–0.5% of milk is dumped. Table 2 summarizes the percentage of milk dumped in each of the 11 FMMOs as the pandemic hit in 2020. In aggregate, the total amount of milk dumped accounted for 2.5% in April, which was the highest amount dumped in 2020 in every order. The table demonstrates that the amount dumped varied widely across orders. In percentage terms, the most dumping occurred in the Florida order (14.3%) with large relative amounts of milk also dumped in the Northeast (5.1%), Southeast (4.2%), Arizona (4.0%), and the Southwest (3.8%) orders. Dumped milk levels in May returned to baseline levels and held at those levels for the remainder of 2020.

| Order | January | February | March | April | May | June | July |

| Northeast | 0.40 | 0.21 | 0.87 | 5.14 | 0.48 | 0.31 | 0.25 |

| Appalachian | 0.65 | 0.65 | 0.56 | 1.47 | 0.50 | 0.67 | 0.57 |

| Florida | 0.53 | 0.57 | 0.51 | 14.31 | 0.52 | 0.49 | 0.53 |

| Southeast | 0.83 | 1.73 | 0.81 | 4.24 | 0.76 | 0.78 | 0.70 |

| Upper Midwest | 0.07 | 0.07 | 0.07 | 1.42 | 0.11 | 0.20 | 0.16 |

| Central | 0.28 | 0.30 | 0.25 | 1.45 | 0.16 | 0.34 | 0.36 |

| Mideast | 0.12 | 0.09 | 0.07 | 1.37 | 0.11 | 0.14 | 0.37 |

| California | 0.10 | 0.13 | 0.13 | 0.80 | 0.30 | 0.10 | 0.73 |

| Pacific Northeast | 0.04 | 0.02 | 0.02 | 0.10 | 0.03 | 0.01 | 0.02 |

| Southwest | 0.30 | 2.83 | 2.75 | 3.82 | 0.40 | 0.44 | 0.42 |

| Arizona | 0.01 | 0.02 | 0.80 | 4.01 | 0.03 | 0.06 | 0.09 |

| All orders | 0.23 | 0.41 | 0.52 | 2.51 | 0.27 | 0.26 | 0.38 |

Source: U.S. Department of Agriculture (2020a).

There are several reasons for the short-lived milk dumping period, although they are not without their own consequences. First, dairy co-operatives, in particular but not exclusively, accepted more “distressed milk” (that is, milk moving from distant locations at discounted prices) that was manufactured into storable products, including bulk cheeses, butter, and milk and whey powders. Cheese and butter production spiked notably in April, and ending stocks relative to monthly domestic use spiked 20%–30% for butter, American cheese, and other cheese. Clearly, the industry chose to produce storable products wherever possible rather than dump milk, even if this meant carrying higher levels of stocks whose final disposition was uncertain. Second, whenever possible, export markets were leveraged to move dairy products. Consistent with historic export patterns, this was especially the case for milk and whey powders, which saw below-average export sales in the first quarter but increased to well above seasonal averages in the second quarter. Third, dairy co-operatives took aggressive actions to either implement existing programs or create new pricing programs to discourage milk production. Farm markets for milk are famously price inelastic in both supply and demand. Rigidity in short-run supply and demand response is a key reason for enduring cyclical behavior with amplitudes of price changes that can have profound impacts on short-term profitability. This characteristic is further compounded by pervasive milk price regulation built around a concept of market pooling, where farmers receive a market average price with adjustments for milk composition. In addition, dairy co-operatives tend to pay price differentials, usually premiums but sometimes discounts, that are also pooled or averaged across all members. The result is a habitual blurring of marginal price information. Dairy co-operatives have increasingly made two decisions designed to achieve greater coordination between member production and commercial sales opportunities. One is that farmers whose milk production is growing beyond a simple trend rate are the ones culpable when supply is long. The second is that such “excess” production should be assigned a price that is punitive, which provides a clear signal that this “excess” is more likely to be unprofitable. Even some co-operatives whose members were not previously supportive of these kinds of “base-excess” or “two-tier” pricing plans were persuaded to at least allow their co-operatives to create the outlines of such a plan during the protracted low milk prices from 2015 to 2019. The anticipated and perceived severe imbalance between current production and commercial demand beginning in late March led many co-operatives to aggressively implement these “base-excess” pricing programs. Whether they did or not hinged entirely on the particular co-operative situation, both in terms of member production growth and the extent of changes in commercial sales and the region of the country.

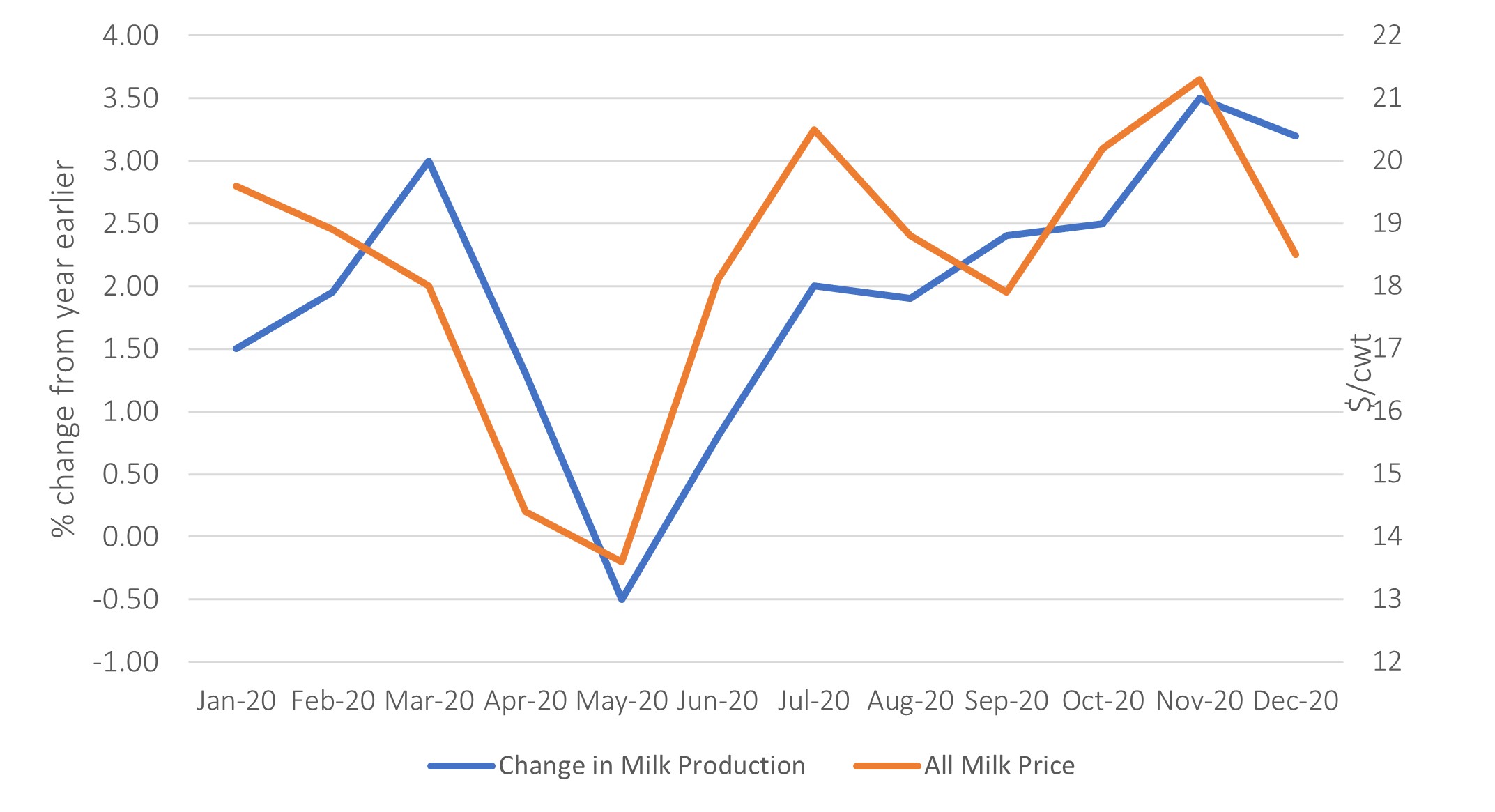

Co-operatives had various parameters to their plans but generally a base level of milk production was set at some farm-specific historic level (a percentage of milk marketed in some recent month or quarter—often 85%–95%). Any milk sold in excess of that amount received a lower “overbase” or “excess” price that was designed to cover the estimated costs of managing the “excess.” Typically, this meant offering the milk to a reluctant customer who needed a deep discount and often also required increased transportation costs. To what extent this restrained growth or even resulted in production declines on specific farms or in total can only be surmised, but the fact is that total U.S. milk production slowed in April, declined in May, and followed higher All Milk prices to increasing production in the second half of 2020 (Figure 2). Normally, monthly milk production change shows virtually no correlation to contemporaneous milk prices. However, as Figure 2 illustrates, they were correlated in 2020 with annual lows in May and strong prices and production increases for the remainder of the year.

Source: U.S. Department of Agriculture (2020e).

Market prices for farm milk were severely impacted as well. Entering the year at around $20 per hundredweight (cwt), a favorable price, the “base” farm price slid in January and February and dropped precipitously in March and April, hitting $13.60/cwt in April. With an “overbase” price applied to milk in excess of the farm-specific adjusted base production level, that was 50% or more below the price paid for “base” milk production; little wonder that there was a significant short-run supply response. The May decline in milk contributed to farm prices, increasing to $18/cwt in June and $20/cwt in July, when industry reports indicate the “overbase” farm milk deduction disappeared or the co-operative supply management plan was suspended.

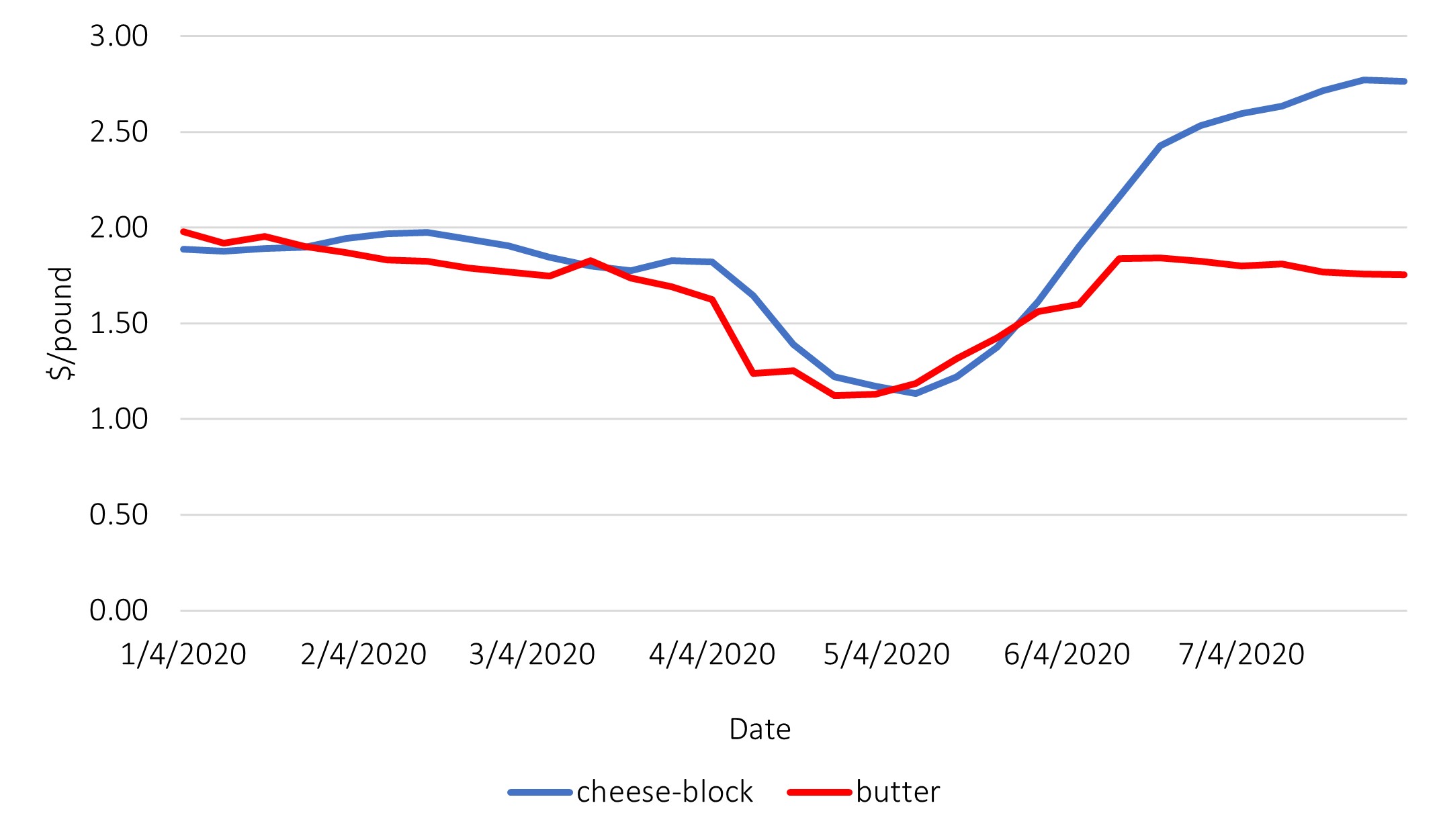

As is generally true, these farm milk price changes were not mirrored in wholesale and retail markets. The result of food service demand destruction was a 39% decline in wholesale cheese price and 36% decline in wholesale butter price from March to May (Figure 3). This has important implications for farm prices as wholesale cheese and butter prices are primary drivers of the farm milk price (Novakovic and Wolf, 2016). At the retail level, prices generally rose and the rate of increase was higher in the second quarter but tended to moderate in the summer months. Increases in retail fluid milk prices were more pronounced (+11% YOY in September 2020), retail butter price changes were more subdued (+1.9% YOY in September), and cheese prices fell in between (+3.8% YOY in September) (BLS, 2020).

| Quarter | All Milk | Net DMC | CFAP |

| Q1 | 18.83 | -0.03 | 6.20 |

| Q2 | 15.37 | 2.38 | 1.20 |

| Q3 | 19.07 | -0.12 | 1.20 |

| Q4 | 20.00 | -0.15 | 1.20 |

Note: DMC assumes signup for coverage at $9.50/cwt minus a $0.15 premium which

would apply to a maximum of 4,167 cwt per month which is about 200 average U.S.

cow production. CFAP includes CFAP2 for the last three quarters assumes that

payment limit of $250,000 per individual or $750,000 per corporation is not exceeded

and is based on the milk production it applies to rather than when payment was

received.

The U.S. federal government reacted to the pandemic with large stimulus investments. Some of this occurred through existing programs. SNAP benefits increased 73% in April YOY, while the Emergency Food Assistance Program (TEFAP) was up 34%. New programs—primarily the Coronavirus Food Assistance Program (CFAP)—also played a role. CFAP had two components. The first offered direct income subsidies to dairy farmers, with payment limitations and income qualification rules. The budgeted payments are considerable and represent a sizable opportunity for the dairy farmer whose farm size does not exceed the payment limitation border. All dairy operations with milk production in the first quarter, as well as all dumped milk in the first quarter of 2020, were eligible for CFAP payments. The initial payment was $4.71/cwt multiplied by first-quarter milk production, funded by the CARES Act. The second CFAP payment was based on an adjusted first-quarter production multiplied by $1.47/cwt, coming from CCC funds. In total, the initial CFAP dairy payment was $6.20/cwt on first-quarter milk production (Table 3). A second version of the program—CFAP 2, with sign-up from September through December—added another $1.20/cwt in payments for the last nine months of 2020 (Table 3). In total, most farms that sign up will have received an average annual income contribution of $2.45/cwt from CFAP payments.

Existing dairy farm programs and crop insurance also provided support for operations that had signed up or purchased these tools. The Dairy Margin Coverage (DMC) program provides a payment when the margin between the U.S. All Milk price and an average U.S. feed cost index falls below trigger levels. The highest margin that can reasonably be protected is $9.50/cwt on the first 5 million pounds of annual production history for each operation (equivalent to the production of about 200 average cows). In 2020, DMC payments for a $9.50/cwt coverage level reached $3.47/cwt for April and $4.13/cwt for May (Table 2). National payments to date, and likely for the year given expected margins, totaled $196 million. Farms that purchased coverage at the $9.50 level will have averaged a net benefit of about $0.67/cwt on their covered annual historic milk production. Unfortunately, expectations of low payouts resulted in only 51% (13,482) of operations with established production history and 36% of all herds participating in 2020. Further, the size coverage limits mean that those payments apply to a relatively small percentage of total milk production. In other words, farms of larger than average herd sizes are receiving payments on only a portion of their overall sales, thereby diluting the average net price benefit as size increases.

Another policy that may have provided significant payments for dairy farmers was the Dairy Revenue Protection (DRP) program, a crop insurance program that offers subsidized bundles of put options for milk price based on Class III milk, Class IV milk, or butterfat and protein prices at the Chicago Mercantile Exchange. Because 2020 milk prices were projected to be relatively high prior to the pandemic, crop insurance contracts purchased earlier would have provided large payments to offset the loss in milk price caused by the pandemic. The results of these programs were an increase in cash flow for dairy farmers and an increase in demand for dairy products, which contributed to a dramatic increase in cheese prices.

Table 3 summarizes net DMC and CFAP payments by quarter along with the U.S. All Milk price to proxy market price. Note that the All Milk price does not deduct promotion or hauling. The table assumes DMC signup for coverage at $9.50/cwt minus a $0.15/cwt premium, which would apply to a maximum of 4,167 cwt/month, which is equal to the production of about 200 average U.S. cows. The CFAP column in Table 3 includes CFAP 2 for the last three quarter assumes that payment limit of $250,000 per individual or $750,000 per corporation is not exceeded and is based on the milk production it applies to rather than when payment was received. With these assumptions, the highest gross farm milk returns since 2014 were achieved in 2020 (Table 3). However, it is important to recognize that the market effects of the COVID pandemic were highly variable both across regions and over time. The result is that actual cooperative and farm returns were also highly variable.

The second component of CFAP is the Farmers to Families Food Box Program. Under this program, the USDA finances the purchase of food items, including dairy products, for direct distribution to needy Americans through local soup kitchens, food pantries, and similar nonprofit organizations. There were four rounds of the program completed in 2020. The first round purchased $1.2 billion of products between May 15 and June 30. The second round purchased up to $1.47 billion between July 1 and August 31. The third round of the program made an additional $1 billion available on August 24, 2020, for deliveries through October 31, 2020. The fourth round, announced on October 23, 2020, will purchase up to $500 million worth of food and deliver between November 1 and December 31, 2020. (U.S. Department of Agriculture, 2020c). To date, this program purchased more than $4 billion in 2020. With more than $600 million spent to purchase dairy products, the Farmers to Families Food Box Program has contributed in particular to strong demand for fresh cheese and fluid milk and is believed to be the primary reason for a dramatic spring rebound of cheese prices to above $2.50/lb (Figure 2).

With the length of the pandemic unknown at this point, it is worth considering some of the lessons that we have learned to date about the U.S. dairy supply chain. Impacts will no doubt continue as long as the pandemic disrupts markets and consumer and producer behaviors. Even after the pandemic emergency can be declared over, there is much speculation about lasting impacts and changes to what had been considered normal dairy business strategies and tactics. Clearly the fundamental effect is in a seriously revised assessment of production and market risks and the need for practices and structures to mitigate those risks. What is entirely uncertain is the extent to which consumers will be able to detect and choose to reward businesses that adopt otherwise costly practices in order to ameliorate potential but uncertain future risks.

Insofar as the pandemic is fundamentally about human health, a primary short-term impact and management challenge was to protect employees and manage the workforce to minimize disruptions from farm to processing plant to delivery. Moreover, the pandemic required employers to consider issues not only within the confines of the workplace but also in the nonwork environment. Unlike the meat industry, there were no widespread outbreaks in dairy processing plants that affected national markets, likely because most dairy plants are much less densely populated by workers. Possible lasting implications may be (i) stricter health protocols in the workplace, including health checks and protective equipment, and (ii) a change in culture that rewards sick workers for staying home as opposed to shaking it off and coming in even if they have a fever or do not feel well.

Another compelling change might be in using greater precautionary inventories to create a cushion for both procurement and sales. This strategy could make for a nimbler operation, or less brittle supply chain, in the event of severe and irregular demand disruption or failures in the transportation system.

With respect to policy, it is tempting to wonder whether the US dairy industry will re-engage in conversation about disaster assistance versus ongoing risk management or insurance programs. The failure in existing programs for dairy was not in their design or execution but rather in dairy farmers’ underutilization of them. The same might be said of food assistance programs. The CFAP food box program had the virtue of targeting farm commodities in particularly dire straits as well as helping food insecure families. Existing programs have different mechanisms and effects. TEFAP distributes food items, but the outlets are more typically food banks as an intermediary distributor. Also, TEFAP is not ordinarily specific about acceptable items. SNAP is entirely different in that it provides cash that can be spent rather broadly on food rather than food items themselves. The CFAP donations program, arguably, created win–win opportunities for hard-hit producers of perishable foods and newly food-insecure consumers, but this came at the expense of a new set of regulations and infrastructure that delayed implementation. In addition, it used new and untested vendors who may well have contributed to price spikes due to their lack of experience in dairy product procurement.

Allied Market Research. 2020. U.S. Cheese Market by Type. Available online: https://www.alliedmarketresearch.com/us-cheese-market.

Bureau of Labor Statistics. CPI Dairy and Related Products in U.S. City Average, All Urban Consumers, Not Seasonally Adjusted. Available online: https://data.bls.gov/timeseries/CUUR0000SEFJ.

Novakovic, A., and C. Wolf. 2016. “Federal Interventions in Dairy Markets.” Choices 31(December).

Novakovic, A., and C. Wolf. 2018. “Disorderly Marketing in the 21st Century US Dairy Industry.” Choices 33(November).

Stephenson, M., and A. Novakovic. 2020. “Making Sense of Your Milk Price in the Pandemic Economy: Negative PPD’s, Depooling and Reblending.” Program on Dairy Markets and Policy Information Letter Series, 20-03. Available online: https://dairymarkets.org/PubPod.

U.S. Department of Agriculture. 2020a. Federal Milk Marketing Order Statistics. U.S. Department of Agriculture, Agricultural Marketing Service. Available online: https://www.ams.usda.gov/resources/marketing-order-statistics.

U.S. Department of Agriculture. 2020b, June 2 (updated). Food Expenditure Series. U.S. Department of Agriculture, Economic Research Service. Available online: https://www.ers.usda.gov/data-products/food-expenditure-series/.

U.S. Department of Agriculture. 2020c. USDA Farmers to Families Food Box. U.S. Department of Agriculture, Agricultural Marketing Service. Available online: https://www.ams.usda.gov/selling-food-to-usda/farmers-to-families-food-box.

U.S. Department of Agriculture. 2020d. Milk Production and All Milk Prices. U.S. Department of Agriculture, National Agricultural Statistics Service. Available online: https://www.nass.usda.gov/Surveys/Guide_to_NASS_Surveys/Milk/index.php

U.S. Department of Agriculture. 2020e. Dairy Market News. U.S. Department of Agriculture,

Agricultural Marketing Service. Available online: https://www.ams.usda.gov/market-news/dairy

Wolf, C., M. Stephenson, and A. Novakovic. 2020. USDA’s New Direct Payments Program for Dairy Farmers. Program on Dairy Markets and Policy Information Letter Series 20-02. Available online: https://dairymarkets.org/PubPod.