As with other farm commodities, fresh fruits and vegetable (produce) crops faced demand and supply impacts from the COVID-19 pandemic that plagued the world in 2020. Shifts in the demand for produce have affected where, how, and which food is purchased and consumed. Supply-side shocks, especially for availability and cost of labor, have affected costs of produce production and distribution.

This paper summarizes the impact of the pandemic on the supply and demand situation and outlook for fruit and vegetables typically shipped as fresh produce. These farm commodities and their markets have some distinguishing features. First, they tend to be labor-intensive: Many are hand-harvested or have other cultural practices that employ labor services that are costly relative to crop value. Second, perishability often implies significant marketing and distribution costs and vulnerabilities. Third, retail packing in the field and direct marketing relationships between farms and retailers shorten the supply chain for many of these commodities. Fourth, in some cases relatively few farms supply a significant share of the market, although, as in other industries, there are many small farms that supply niche or local markets.

The bulk of this paper compares the pattern of produce shipments and prices during the pandemic relative to prior years. To preview results, the data show normal flux similar to what we find in many agricultural markets. We see some evidence of what may be pandemic impacts, but these are relatively isolated and it is hard to assign causation definitively. The data do not reveal strong evidence for a major impact of the COVID-19 pandemic on quantities or prices of fresh fruit and vegetables during 2020 compared to a normal season. That is, given the normal variability, the prices and quantities observed in 2020 are consistent with year-to-year variations in these markets in the recent past. These data are suggestive, but measuring causal impacts is beyond the scope of the data analysis presented. Before digging into those data, we consider first some farm labor market relationships and data.

Much of U.S. agriculture has replaced hired labor with mechanized production processes. That is less true for fresh fruits and vegetable industries, where harvest and several other operations are still conducted by hand. This fact has had significant implications for adjustments to the COVID-19 pandemic.

| Crop | Labor Share of Operating Costs |

Labor Share of Total Costs |

| Apples | 63% | 41% |

| Broccoli | 26% | 21% |

| Celery | 39% | 33% |

| Cherries | 61% | 49% |

| Grapes | 60% | 50% |

| Iceberg lettuce | 52% | 42% |

| Peaches | 73% | 46% |

| Bell peppers | 53% | 43% |

| Spinach | 24% | 20% |

| Strawberries | 43% | 39% |

Source: Author calculations from University of California Cost and Returns Studies,

https://coststudies.ucdavis.edu/en/current/.

Table 1 summarizes hired farm labor shares of operating costs and total costs for a range of fresh fruit and vegetable products. These data come from recent cost estimates for fruit and vegetable farms that are considered to be “typical, well managed” commercial operations in California. The labor share of costs includes direct farm hires and employees of labor contractor firms that supply labor services to the farms. Costs range from more than 70% of operating costs for peaches to about 25% for broccoli, iceberg lettuce, and spinach, which rely on mechanization for some operations. The importance of farm labor costs for these crops means that the cost and availability of hired labor has the potential to measurably affect produce costs and, therefore, the price of these products.

Hired farm labor in produce industries tends to be low wage and seasonal. Most employees are immigrants, and a significant share do not have full immigration documentation. These conditions affect the supply and availability of hired farm labor. Despite concerns by employers of a “shortage” of labor, wages remain relatively low. Some employers claim that labor supply is inelastic; therefore, they claim that, higher wages do not attract additional workers. Compelling econometric evidence remains scarce on this point.

The pandemic has had several effects on the market for hired farm labor supply facing produce industries. Most important, locking down segments of the economy reduced nonfarm employment opportunities (for example, in food service and janitorial and cleaning services) that compete for low-wage workers. Some farms found more workers available when nonfarm employment became scarcer. The magnitude of this impact has not been adequately measured, however, and several factors push in the opposite direction.

First, unemployment insurance benefits for those laid off from nonfarm jobs exceed potential farm earnings. The traditional assumption has been that those that have held nonfarm jobs never enter (or re-enter) farm work. In that case, there are no potential recipients that might shift to farm work, so larger unemployment benefits would be irrelevant. Second, school closings and difficulties with childcare reduce availability of workers that would normally work on farms. Third, potential danger and some serious outbreaks of disease in farm worker communities have reduced worker availability. Finally, farm costs of addressing disease prevention and care for ill workers raise costs that do not appear in wage rates, but do affect the cost of production of labor-intensive produce. Unfortunately, measuring the magnitudes of these impacts is still difficult and data sources have not kept up with the pandemic.

On the demand side, several major drivers have affected produce markets. First, government shutdowns of food supply channels, especially of the food service sector, meals at school and work, and many dine-in restaurants, caused severe, immediate disruptions. In addition, some buyers chose to avoid away-from-home food venues and many employees worked from home and thus did not use at-work food service venues. These shifts caused a massive and rapid shift in where, and to a lesser extent which, produce was demanded. The result was an immediate loss of perishable products that could not be repackaged or repositioned rapidly enough, say from salads bagged for institutional cafeterias to packages suitable for grocery store sales.

The other demand-side disruption was sequestration requirements that meant lack of commuting and travel, more time with family, and other changes in patterns of consumption. For example, home baking and “comfort food” became more common in the early days of the pandemic. There were, however, no pervasive behavioral changes affecting produce consumption. The still-incomplete transition back to more consumption of produce away from home has been more gradual than the initial disruption but remains uncertain and depends on both progress in reducing COVID-19 impacts and opaque government choices about what will be allowed. We also do not yet know the extent to which consumption will return to the pre-COVID “normal.”

Finally, the sudden and severe recession reduced consumption of most products. However, most food products, including produce items, are less sensitive than most goods to income declines (a small income elasticity of demand for food). The gradual return of employment and income will cause more consumption; however, the magnitude of the impact on consumption is expected to be small for standard produce items but may be larger for high-priced luxury produce. Even this effect could be muted if luxury meals at home, with exotic fruits and vegetables, substitute for expensive meals away from home.

Weekly quantities of produce shipped and average prices (at the shipping point) are available from the USDA Agricultural Marketing Service (AMS). We gathered quantity data on labor-intensive fruits and vegetables and melons for January 2018 through the second week of September 2020. Fruits include apples, avocados, cherries, grapes, nectarines, peaches, and strawberries. Vegetables and melons include broccoli, cantaloupes, carrots, cauliflower, celery, iceberg lettuce, romaine lettuce, bell peppers, tomatoes, and watermelons. AMS reports weekly shipment and price data on the Saturday ending each week. We selected the week ending March 21, 2020, as the first week of the COVID-19 period. The week ending March 23 is the closest match in 2018, and the week ending March 24 is the closest match in 2019.

The broad magnitude of market-wide differences in the period of the COVID-19 pandemic are derived by comparing shipments and prices of each fruit and vegetable commodity from mid-March through the end of August 2020 with the comparable periods in 2018 and 2019. We consider both season long and week-by-week impacts, and examine individual commodities and sector-wide averages.

To calculate average impacts, we calculate the difference between quantity shipped and price for each commodity in each week in 2020 and the comparison year as a percentage of 2020. We ask if the data in the period starting with the week of March 14–20, 2020 has been measurably different across a variety of fresh fruit and vegetable quantities and prices relative to the prior two years. We use 2020 as the base to make sure we capture all data available for 2020, even if there were zero shipments in the prior years for a week in which there were shipments of that commodity in 2020.

The quantity and price data for each commodity are specific to shipping district. We use California for all these produce items except apples and cherries, for which we use Washington State as the shipping district. California and Washington have large shares of total shipments in national markets. A broader array of shipping districts adds substantial complexity in data interpretation with little gain for understanding the markets. In particular, concerns about mostly local consumption, differences in product characteristics, short seasons, and small quantities would have made comparisons even more complicated.

Every produce crop is different and markets are complicated. For example, some crops—such as cherries—are highly seasonal, with seasons that start and end on slightly different dates each year. This complication may cause some large percentage difference in weekly quantities from year to year at the beginning and ends of seasons. Crops also differ by revenue, with the value of shipments of lettuce, strawberries, apples, and grapes much larger than, say, peaches or watermelons. Perishability is high for lettuce or cherries, but much less of an issue for apples. These complications suggest caution in generalizations.

With the exception of strawberries, the fruits are all perennial tree and vine crops with limited harvest seasons. Some, such as apples, are storable and ship year-round. Others, such as peaches and cherries, have relatively short shipment seasons of four or five months. Strawberries are grown commercially as an annual crop and ship from California every week of the year, although shipments are noticeably smaller in December through February. Some vegetables and melons are planted and harvested once per year, others vegetables allow two or three crop cycles per year. Strawberries and several of the vegetable crops are planted several times during the year and shipped year-round. These crop-specific features affect supply flexibility and how readily growers may adjust quantities within the year. For example, because apples are storable, those shipped in the spring of 2020 were harvested in 2019. For many perishable vegetables (for example, broccoli or lettuce), growing seasons are short, so that planting adjustments in the spring affect summer shipments, which allowed them supply flexibility in response to COVID-19.

Examining the patterns of shipments and prices for our sample produce commodities helps determine if the COVID-19 period of 2020 has been different from earlier years, in more than just a random way.

| Crop | Percentage Difference from 2018 |

Percentage Difference from 2019 |

Percentage Difference from Average of 2018-2019 |

| Apples | 7% | 7% | 7% |

| Artichokes | -25% | 7% | -9% |

| Avocados | 6% | 42% | 24% |

| Blackberries | 16% | 17% | 17% |

| Blueberries | 44% | 25% | 35% |

| Broccoli | -4% | 6% | 1% |

| Brussels Sprouts | 51% | 46% | 48% |

| Cantaloupes | -73% | -39% | -56% |

| Carrots | 0.2% | 3% | 1% |

| Cauliflower | -4% | 8% | 2% |

| Celery | 8% | 13% | 11% |

| Cherries | -23% | -5% | -14% |

| Grapes | -12% | -5% | -8% |

| Lettuce, Iceberg | -4% | 2% | -1% |

| Lettuce, Romaine | -4% | 2% | -1% |

| Nectarines | 24% | -7% | 8% |

| Peaches | -23% | -44% | -34% |

| Peppers, Bell Type | -3% | -7% | -5% |

| Raspberries | -4% | -5% | -4% |

| Spinach | -20% | 4% | -8% |

| Strawberries | -7% | 1% | -3% |

| Tomatoes | -43% | -23% | -33% |

| Watermelons | -58% | 4% | -27% |

Source: Author calculations from USDA Agricultural Marketing Service: Custom Reports for

2018, 2019, and 2020 Seasons. Available online:

https://www.ams.usda.gov/market-news/custom-reports.

| Mean (2020-2018)/2020 |

Mean (2020-2019)/2020 |

|

| Mid-March through December | ||

| Shipments | ||

| All | -12.78% | 2.09% |

| (4.24) | (1.65) | |

| Fruits | -10.42% | 2.61% |

| (9.67) | (3.38) | |

| Vegetables | -5.56% | 3.51% |

| (1.82) | (1.37) | |

| Melons | -92.71% | -13.87% |

| (12.02) | (7.91) | |

| Prices | ||

| All | 9.58% | -5.79% |

| (1.44) | (2.41) | |

| Fruits | 5.52% | 2.53% |

| (2.26) | (2.32) | |

| Vegetables | 6.80% | -16.68% |

| (1.80) | (3.57) | |

| Melons | 57.14% | 53.16% |

| (5.32) | (6.10) |

All shipments, 821; fruit 341; vegetable 431; melons, 49; All prices 707; fruit 237; vegetables

425; melons 45. Standard errors of the estimates are provided in parentheses for testing

hypotheses.

Source: Author calculations from USDA Agricultural Marketing Service: Custom Average

Pricing: Shipping Point Average Prices Custom Reports for 2018, 2019, and 2020 seasons.

https://www.ams.usda.gov/market-news/custom-reports.

Table 2 compares 2020 shipments to those of prior years for each of the commodities. The entries in Table 2 show a wide range of differences in shipments between 2020 and the prior two years across commodities. Ten of 23 commodities had larger shipments in 2020 compared to the average of 2018 and 2019. However, three of those were only up one or two percent. Of the 14 commodities with declines, five had declines of 5% or less. Produce shipments in 2020 were larger than both the prior two years for seven commodities, smaller than both the prior two years for seven commodities, and split for nine commodities.

Shipment quantity was up slightly for broccoli, carrots and cauliflower, and down slightly for iceberg and romaine lettuces, raspberries and strawberries. Shipments were up by 11% for celery, and down by 8% for spinach and 5% for bell peppers. These are commodities for which quantities are more flexible within a year. Shipments are up among four of the six tree and vine crops, where supplies are hard to adjust and shipments depend mostly on weather, unless disruptions have impeded harvest or shipments. Cherry shipments are down, but the spring forecast was for a smaller Washington cherry crop in 2020. It is not clear that these impacts have been driven by COVID-19. In general, Table 2 reports little evidence of large systematic COVID-19 pandemic impacts.

Table 3 reports estimates of the means (averages) of relative differences in shipments and prices by week for all available weeks for the produce commodities, along with the estimated standard errors. For example, the first entry in Table 3 shows that from mid-March to the end of the year, the average quantity of weekly shipments in 2020 was 12.78% smaller than 2018 shipments, with an estimated standard error of 4.24. A sample of 821 weekly commodity-specific shipments was used in those calculations of means and standard errors. An estimated mean twice as large or more than its estimated standard error is typically considered an indication of statistical significance and high confidence in the precision of the estimated mean. With these data, there is less than a 5% chance that the true difference is outside the range of about -20.5% and -4.3%, so we reject the hypothesis of a nonnegative difference.

The mean size of vegetable shipments each week (with a sample of 431 observations) was also smaller in 2020 than in 2018 (-5.56%), and the difference has a high degree of statistical significance. However, the difference in mean shipments for fruit (-10.42%), based on a sample of 341 observations, is only slightly larger than its standard error (9.67), so a typical confidence interval would include zero. The estimated means of weekly shipment differences between 2020 and 2019 are all small and small relative to their standard errors. Thus, we have very little confidence that anything other than randomness accounts for the estimated differences between 2020 and 2019 being more or less than zero. The outlier in the shipment data is melons for which shipments were very low in 2020 compared to both the prior years.

The bottom half of Table 3 reports estimated mean price differences between 2020 and the earlier years. Produce producers have flexible price contracts with buyers and some produce continues to trade on spot markets. These individual produce prices are often variable from year to year, and even from week to week within a year. Relative prices across produce commodities items move up and down in ways that are consistent with the then current supply or demand conditions. Romaine lettuce may be expensive one week, and a week later celery or broccoli prices have jumped and romaine prices may have dipped. We commonly see price differences of 50% or more between the price in one week to the price a few weeks later for the same commodity. Such variations indicate the importance of using large samples of prices to develop any inferences.

The mean price difference of 9.58% between 2020 and 2018, for the full sample of 707 fruits and vegetables prices, is large and highly significant statistically. So, just as weekly shipment quantities were lower in 2020 than in 2018, the prices have been higher in 2020. The comparison of 2020 with 2019 shows the opposite: Prices are 5.79% lower in 2020 compared to the very high prices of 2019. The average prices for vegetables are where the big differences occur. The 2020 average vegetable prices are 6.808% above 2018 and -16.68% below 2019. For fruit, prices in 2020 are above 2018 and 2019, but the difference compared with 2019 is small.

Based on the patterns in 2018, 2019, and 2020, we cannot make a definitive statement about whether 2020 was an abnormal year for produce shipments and prices, at least compared to the most recent two years. We see large differences from one year to the next, but 2018 and 2019 seem to be more different from each other than either are from 2020.

Note: The shaded bar around the third week of March

represents the beginning of the COVID-19 period.

Source: USDA Agricultural Marketing Service: Custom Reports

for 2018, 2019, and 2020 Seasons (California).

https://www.ams.usda.gov/market-news/custom-reports.

Note: The shaded bar around the third week of March

represents the beginning of the COVID-19 period. Week 21

2019 was removed due to the concerns about data accuracy.

Source: USDA Agricultural Marketing Service: Custom Reports

for 2018, 2019, and 2020 Seasons (California).

https://www.ams.usda.gov/market-news/custom-reports.

Source: USDA Agricultural Marketing Service: Custom Reports

for 2018, 2019, and 2020 Seasons (Washington State).

https://www.ams.usda.gov/market-news/custom-reports

[Compiled September 14, 2020].

Note: Prices are pre carton. The shaded bar around the third

week of March represents the beginning of the COVID-19

period.

Source: USDA Agricultural Marketing Service: Custom Average

Pricing: Shipping Point Average Prices (California).

https://www.ams.usda.gov/market-news/custom-reports.

Note: Prices are per "flats 8 1-lb containers with lids." The

shaded bar around the third week of March represents the

beginning of the COVID-19 period.

Source: USDA Agricultural Marketing Service: Custom Average

Pricing: Shipping Point Average Prices (California).

https://www.ams.usda.gov/market-news/custom-reports.

Note: Prices are per pound.

Source USDA Agricultural Marketing Service: Custom Average

Pricing: Shipping Point Average Prices (Washington State).

https://www.ams.usda.gov/market-news/custom-reports

[Compiled September 14, 2020].

To dig a bit more deeply into shipments and prices for 2020 compared to prior years, we turn to data from three representative commodities. Iceberg lettuce and strawberries are high-volume produce items that are shipped throughout the year. They are also significant users of hired farm labor and are staple foods in the diets of many consumers, whether for meals at home or away from home. Sweet cherries represent a major labor-intensive, perishable, and seasonal fruit, and Washington accounts for the majority of shipments.

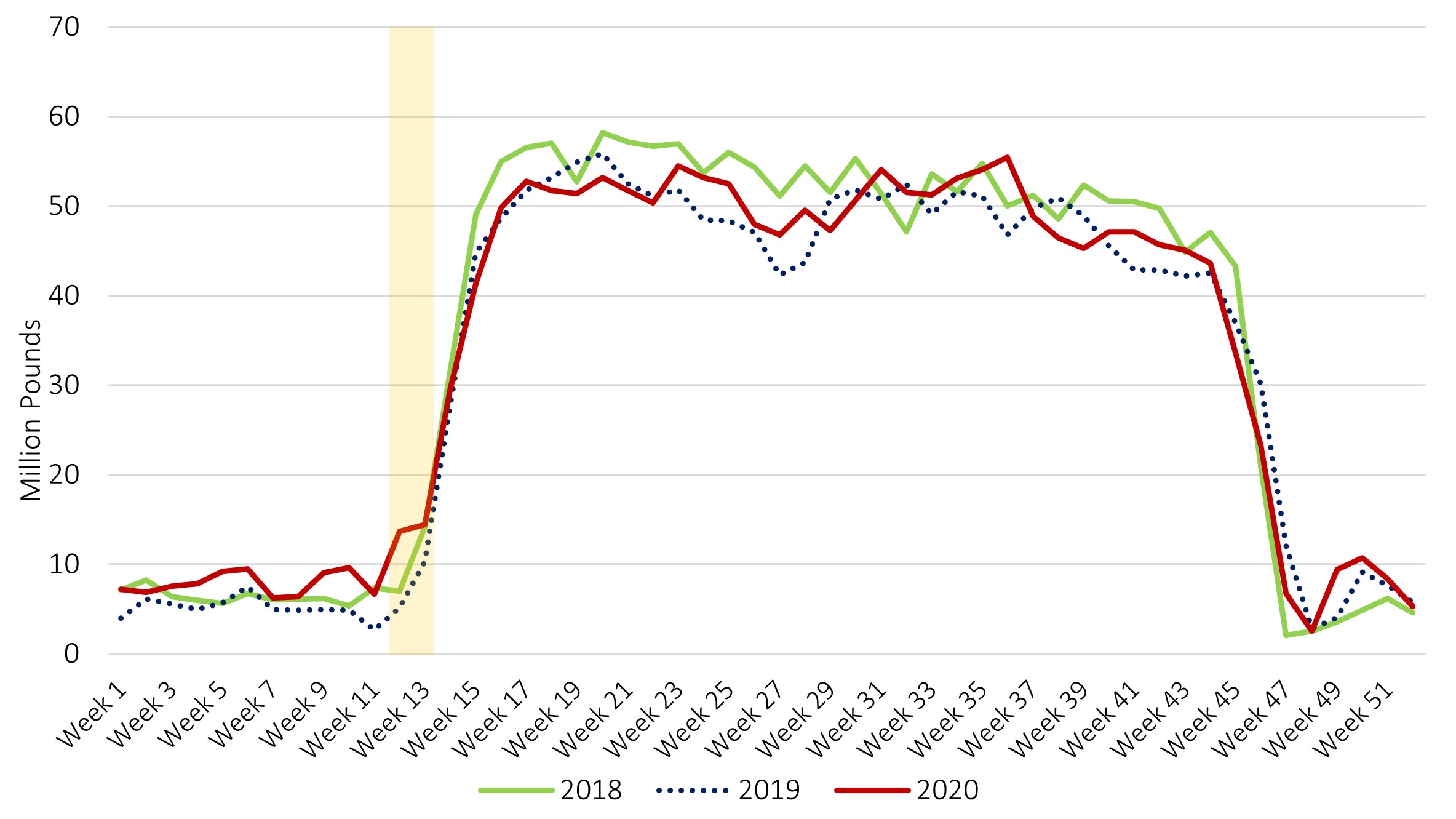

Figure 1 shows the pattern of weekly shipments of iceberg lettuce. Shipments are less than 10 million pounds per week for the first 10 weeks of the year and then ramp up rapidly to exceed 40–50 million pounds starting around week 15 of each of the three years represented. The five-week ramp up begins in the middle of March and is complete by the end of April each year. (Thus, the typical expansion begins just about the time the economic impacts of the pandemic were being imposed on the economy.) From the beginning of May to through the middle of end of October shipments bounce around in a range of about 10% up or down each year. Shipments are very low at the end of the year.

A quick test of the impact of the COVID-19 pandemic on lettuce shipments might be to ask: If there were no labels in Figure 1, could the observer correctly identify which line was 2020? I could not. Data for 2020 (the dark red line) are sometimes above and sometimes below the other two, but mostly the pattern is very similar. Perhaps the pandemic caused shipments to take off a little more quickly in late March than usual and then expand slightly less rapidly than usual from the middle of April through early May. However, that pattern is quite similar to what occurred in 2019 (the dotted blue line) compared to 2018 (the light green line). We know from Table 2 that season-long shipments have been 1% smaller for iceberg lettuce than the average of the prior two years.

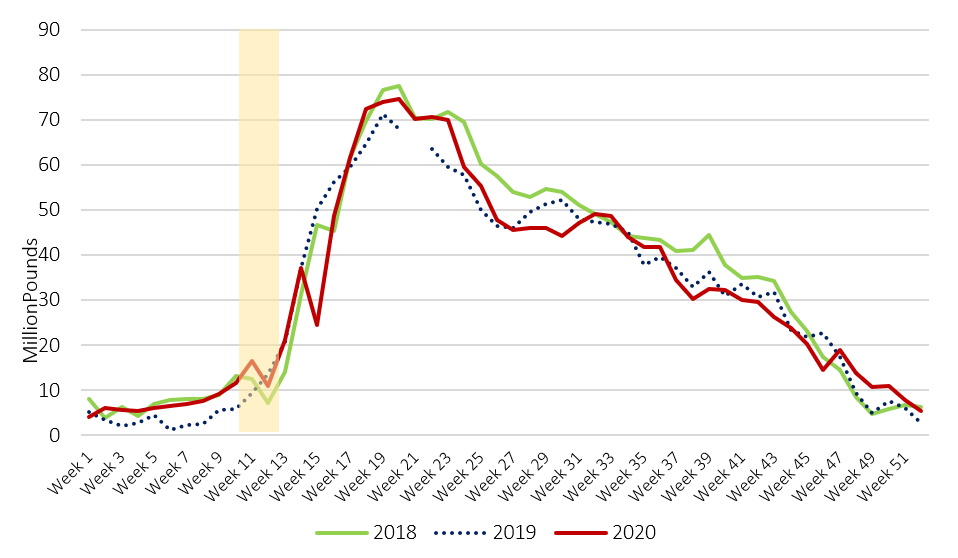

The first four months of Figure 2, representing strawberry shipments, are similar to the early months in Figure 1, representing iceberg lettuce. For strawberries, relatively small weekly shipments through the middle of March begin to ramp up, through somewhat more gradually than for lettuce. There is some observable up and down flux in shipments compared to 2019 that occurs during the beginning of the COVID-19 period, shown by shading around the middle of March. However, the 2020 pattern is, in fact, similar to what occurred in 2018. Once again, 2020 shipping patterns are visually not much different from the patterns of 2018 and 2019.

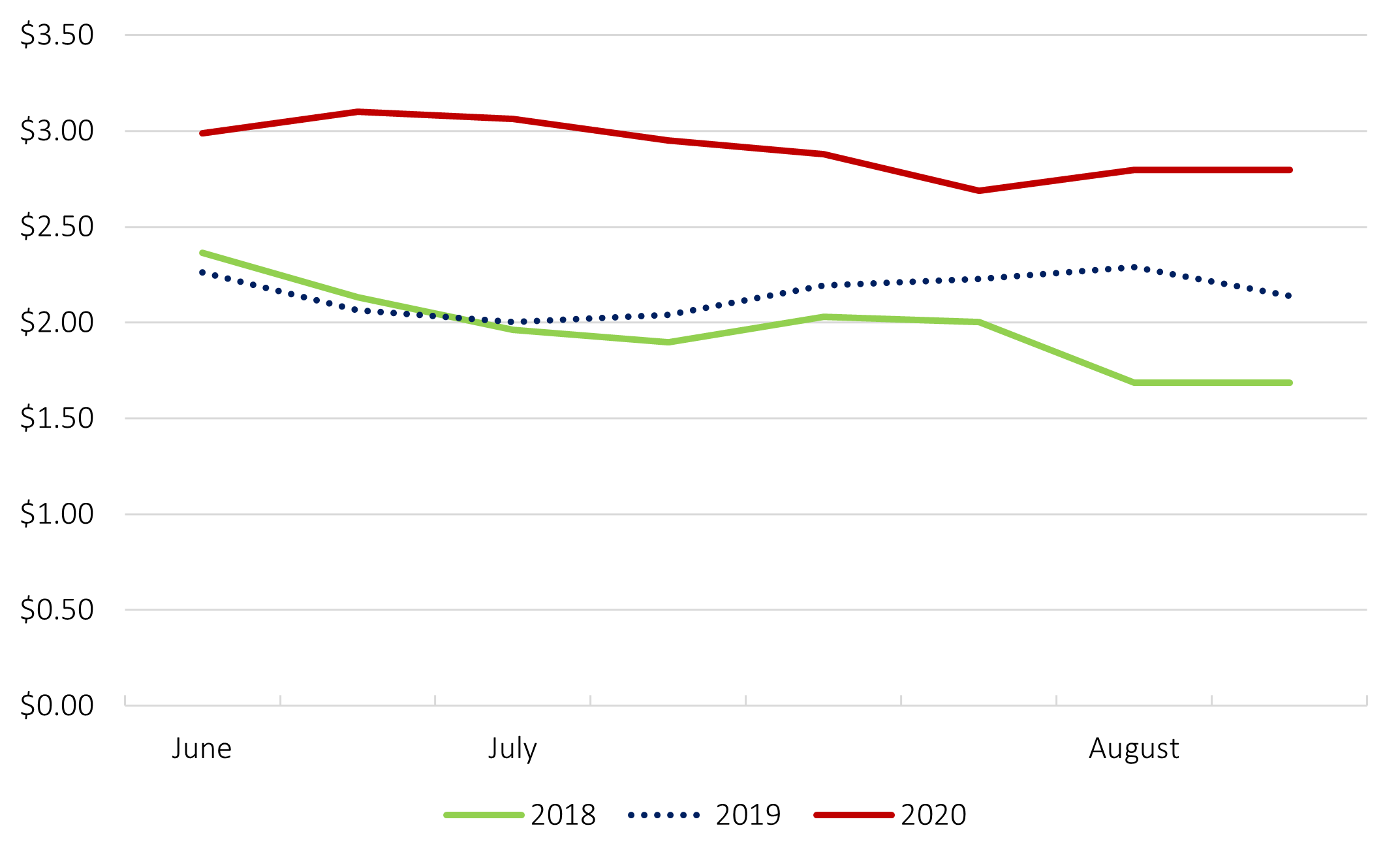

For cherry shipments (Figure 3), the shipping season begins at the first or second week of June and is almost finished by the end of August. Most shipments occur from the middle of June through the beginning of August each year. Figure 3 shows that fewer cherries were shipped over the whole season; from Table 2 we know the total in 2020 was 13% lower than in 2018 and 5% lower than in 2019. The 2018 and 2020 seasons started one week earlier than did the 2019 season. However, 2020 expanded more slowly and, after hitting the same peak of about 75 million pounds in week five of the season, the shipment quantities dropped more rapidly in 2020 and mostly remained below the prior two years. Shipments were below 2018 for just about every week of the season and below 2019 for most of the season, especially during the peak shipment weeks from mid-June through mid-July.

Washington State was hit with a serious and sustained outbreak of COVID-19 among cherry harvest workers that disrupted harvest in several counties. The disease occurred among local residents but was reported to have been severe among immigrant “guest workers,” for which the federal government requires employers to provide housing. Several cherry harvest workers died and hundreds were infected, as reported in local and national news outlets. These terribly sad events concerned everyone in the region and led to adjustments in employment and housing. The timing of the disease outbreak and labor supply disruption is also consistent with low 2020 cherry shipments during what is normally a peak period in July (Figure 3). However, we do not have data to establish how much farm labor health concerns affected the quantities of weekly shipments in July.

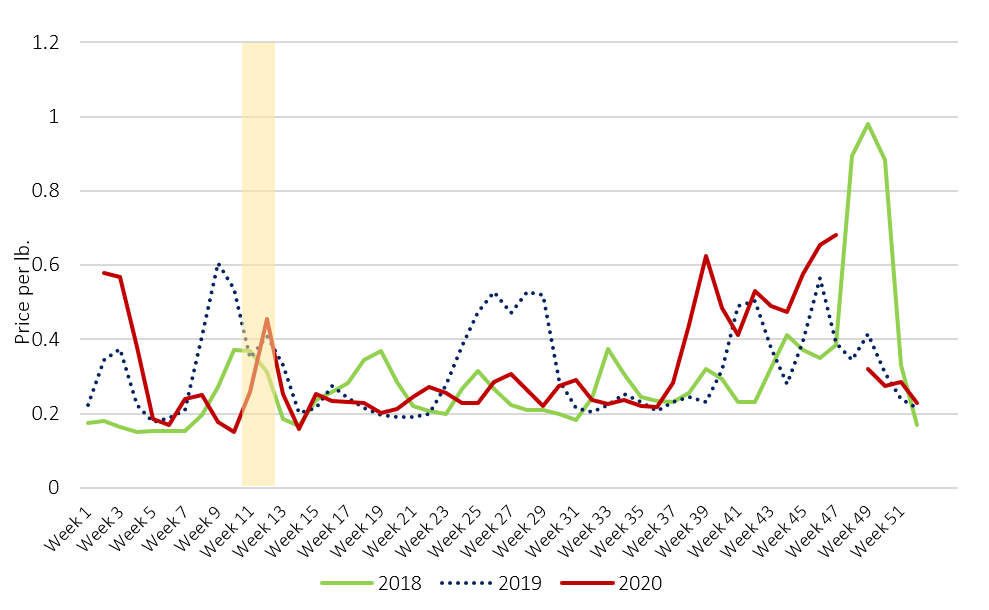

Weekly fresh fruit and vegetable prices are often highly variable in response to disruptions in supply or demand. Figure 4 shows the volatile path of iceberg lettuce prices. There is no obvious seasonal pattern to prices in 2018, 2019, and 2020, other than generally higher prices during parts of March in all three years, but even in March the highest prices are in different weeks. The prices in 2020 peak during the first weeks of the pandemic, but that is also a high-price period in the prior two years. Prices dropped severely in April 2020, but again, that is a low-price period in the prior years too. In the early fall (week 37) lettuce price jumped in 2020 and stayed high relative to the prior years. The 2020 prices did not match the bump in prices that occurred at the end of the year in 2018. Recall these volatile prices occur when, as shown in Figure 1, shipments of lettuce are low. Nothing about the 2020 price path stands out relative to 2018 and 2019.

Strawberry prices (Figure 5) follow the classic high-low-high price pattern through the season with lower prices during the peak shipment period of May and June and higher prices during the winter, summer and fall. Prices are usually high in weeks when shipments are low and would likely be even higher but for substantial imports during such periods. For example, the dip in shipments in early August (Figure 2) is accompanied by higher prices during those weeks (Figure 5). Nonetheless, it is hard to see a pattern related to COVID-19 in the time path of strawberry prices in 2020 relative to the prior years.

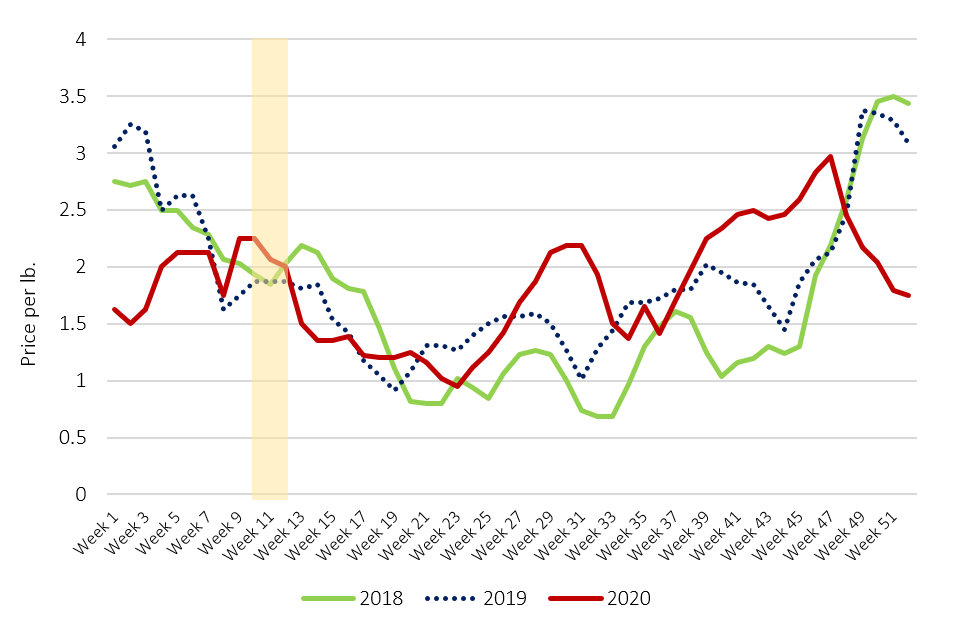

For cherries, a smaller crop in 2020 was accompanied by substantially higher prices throughout the relatively short short season (Figure 6). Perhaps the dip in shipments during some weeks in July, which may have been related to disease among farm workers, caused prices to remain a little higher than otherwise and avoid the slight dip in prices experiences in the prior two years, but the impact seems modest at best.

The domestic U.S. market accounts for the large majority of fresh, labor-intensive produce shipments, and most U.S. fresh vegetable exports go to Canada, which is also the major destination for fresh fruit exports. Table 4 shows export quantities and unit values by month relative to the average of the prior three years. Table 4 includes data for apples, table grapes, strawberries, and lettuce. The years are split into two periods, the pre-COVID-19 period (January–March) and the COVID-19 period (April–December). Given monthly data and the somewhat long lead-times for exports, April is the appropriate starting point for pandemic influences.

These export data are total U.S. shipments to Canada and, while most shipments come from the domestic shipping locations examined above, the data include exports from all U.S. production districts. For lettuce, exports include all lettuce, not just iceberg lettuce and romaine lettuce. The export data used for comparison includes 2017. The export data are thus not strictly comparable to the U.S. domestic shipments.

| Lettuce | Strawberries | Table Grapes | Apples | |

| Volumes | ||||

| January–March | 1.04 | 1.07 | 0.61 | 1.16 |

| April–June | 0.87 | 0.98 | 0.52 | 1.06 |

| July–September | 0.88 | 0.79 | 0.93 | 1.01 |

| October–December | 0.86 | 0.86 | 0.94 | 1.04 |

| Units Values | ||||

| January–March | 1.01 | 1.04 | 1.42 | 0.87 |

| April–July | 0.95 | 0.92 | 0.98 | 0.86 |

| July–September | 1.17 | 1.27 | 1.09 | 0.93 |

| October–December | 1.25 | 1.10 | 1.02 | 1.04 |

Source: Author calculations from U.S. Department of Commerce, U.S. exports,

available from U.S. International Trade Commission. 2020. DataWeb.

https://dataweb.usitc.gov/.

Shipments in the pre-COVID-19 periods in 2020 are up for apples, strawberries, and lettuce and down substantially for table grapes. For the April–December period, 2020 shipments are up for apples and down for the other three four commodities. The January–March shipments of apples are likely to have been harvested in the prior year, and that may also be true for most shipments through the spring months as well. For grapes, 2020 domestic shipments were relatively low, but export shipments are even lower compared to prior years. Notice that exports are more than 90% of the prior years for July-December when most of the 2020 crop is being shipped. For strawberries and lettuce, the export data show that the COVID-19 period had lower shipments despite normal shipments in the domestic market. This may indicate some diversion of product from exports to domestic buyers.

Apple export prices are slightly lower in the pre-COVID-19 period, consistent with higher volumes. Apple prices in the April–September period are lower than in prior years and prices are up during the last month of the year despite slightly higher volumes. For table grapes, export prices are much higher in the pre-COVID-19 period of 2020 when export shipments were very low and roughly equal to the average of prior years in the April–December period. Prices for strawberries higher than prior years except in the April–July period. For lettuce, export prices are down in the April–July period despite lower export volumes in 2020. Overall, more export data are needed to reveal clear patterns of pandemic influence, if any, on export volumes or prices.

This article has reviewed the ways the pandemic has influenced fresh produce shipments and prices with an emphasis on how farm workers have been affected by the pandemic and may affect produce supplies. Temporary disruptions caused by the rapid shift from food consumed away from home to food consumed at home were widely reported and caused some perishable produce to be lost. Some farms and shippers certainly experienced losses during the transition, and some of those that had specialized in supplying restaurants experiences sustained losses. Nonetheless, the major conclusion is that it has been hard to isolate broad and compelling evidence that markets in 2020 are distinctly different than produce quantities and prices in prior years. There is always lots of volatility in produce markets, so even if the COVID-19 pandemic had some significant, specific market impacts, it would be hard to see those impacts in available data. Overall, consumers, producers and shippers were able to transition rapidly from purchasing produce in food service settings away from home to purchasing produce for home consumption. As with other food markets, we do not know how much of this change will be long-lasting as the direct effects of the pandemic fade.

In this situation, specific commodity profiles and case studies are especially effective tools. For example, the COVID-19 outbreak among cherry harvest workers in Washington State was devastating for workers and their families, with loss of life for several workers and loss of livelihood for many more. Hired farm workers are especially vulnerable to disease and to income loss, and the events of July 2020 were terrible for many. That said, the data are not clear that widespread or lasting market impacts were a result.

One bottom line is that shipment and price data do not document clear market differences between 2020 and earlier years. But that does not mean that individual workers did not suffer losses or that the individual farms or industries have not experienced higher costs or lower revenues due to the pandemic.

Beatty, T., A. Hill, P.L. Martin, Z. Rutledge. 2020. “Covid-19 and Farm Workers: Challenges Facing California Agriculture.” ARE Update 23(5): 2–4. https://giannini.ucop.edu/filer/file/1587396051/19625/.

Bernton, H. 2020, August 15. “Mexican Workers Who Left Mid-Harvest Describe a COVID-Ridden Cherry Season in Okanogan County: ‘It Was Like We Were Disposable’” Seattle Times. Available online: https://www.seattletimes.com/seattle-news/northwest/mexican-workers-who-left-mid-harvest-describe-a-covid-ridden-cherry-season-in-okanogan-county-it-was-like-we-were-disposable/.

Bruno, E.M., R.J. Sexton, and D.A. Sumner. 2020. “The Coronavirus and the Food Supply Chain.” ARE Update 23(4): 1–4. https://giannini.ucop.edu/filer/file/1587396051/19625/.

Newman, J. 2020, July 6. “ Coronavirus Hits Nation’s Key Apple, Cherry Farms.” Wall Street Journal. Available online: https://www.wsj.com/articles/coronavirus-hits-nations-key-apple-cherry-farms-11594027802.

Song, Y., M. Bolda, O. Daugovish, and R. Goodhue. 2020. “How Is the Strawberry Industry Weathering the Pandemic?” ARE Update 23(5):10. https://giannini.ucop.edu/filer/file/1587396051/19625/.