After a run of low prices for livestock and meat dating back to 2014, 2020 was shaping up to be a bull market for United States livestock interests. African swine fever continued to decimate China’s pig population. As a result, China—the world’s leading meat importer—was poised to increase purchases dramatically through 2020. Moreover, in January 2020 the United States government signed the Phase One trade agreement with China, which promised to end a two-year trade war and dramatically expand China’s imports of United States agricultural products, including pork and beef. At the consumer end of United States meat markets, a strong economy and record low unemployment pointed to increased demand for meat (Badau, 2020). The net result was that, early in 2020, analysts were forecasting increased United States exports of beef and pork as well as high prices for livestock and meat.

Source: Opportunity Insights (2020).

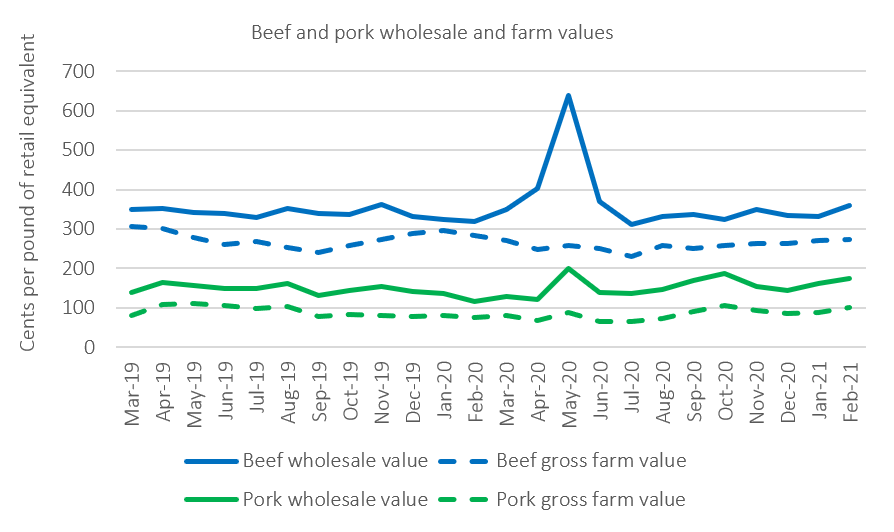

Source: U.S. Department of Agriculture (2020b).

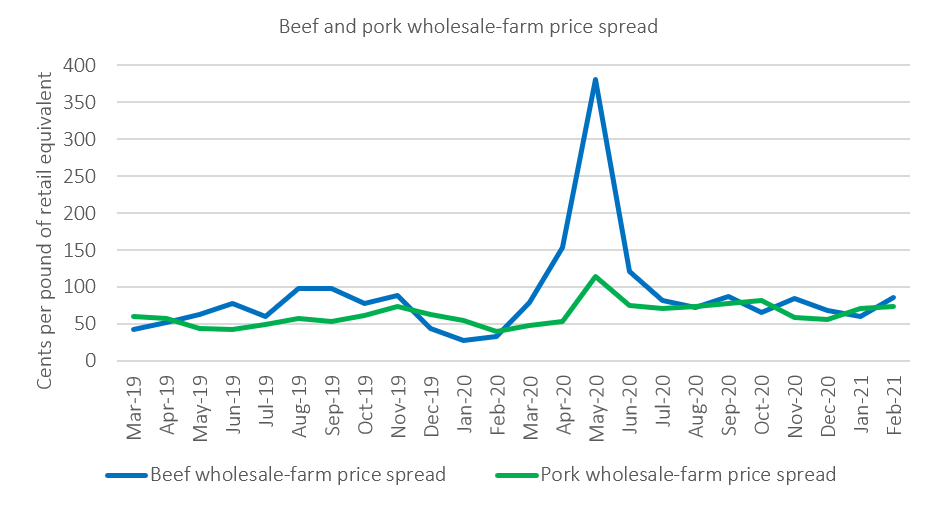

Source: U.S. Department of Agriculture (2020b).

CPI=Consumer Price Index

Data Source: U.S. Bureau of Labor Statistics (2021).

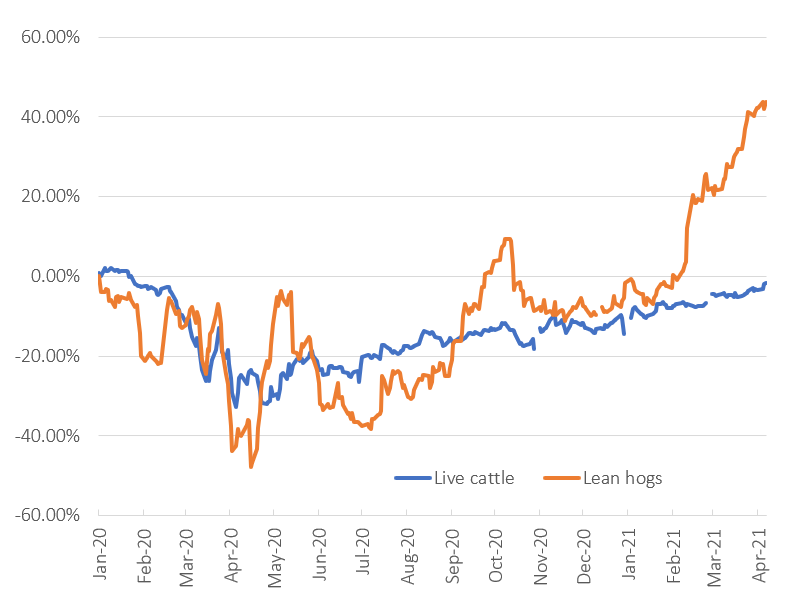

Source: Generic first cattle and lean hogs (live) futures contract,

Bloomberg.

The COVID-19 pandemic started in the Wuhan province of China in late 2019 and eventually spread through the rest of the country. The first known cases of COVID-19 in the United States appeared in Seattle, Washington, in January 2020, and cases were dispersed throughout the country by March 2020. The United States government declared a national emergency on March 13, 2020. The pandemic disrupted United States livestock and meat markets in several ways. First, global merchandise trade fell 14% in the second quarter of 2020 compared to the same time last year (WTO, 2020), and we can surmise that much of this is associated with the economic response to COVID-19. As a net exporter of meat, reduced global trade amounted to a reduction in demand for United States meat exports and downward pressure on prices of United States meat and livestock. Second, although United States pork exports rose in the first half of 2020 compared to 2019, driven by a huge spike in Chinese demand associated with the African swine fever in that country, exports likely would have been even larger if China had not been affected by COVID-19. Through July 2020, year-to-date United States exports of beef were down 8% compared to 2019 (United States Department of Agriculture, 2020a).

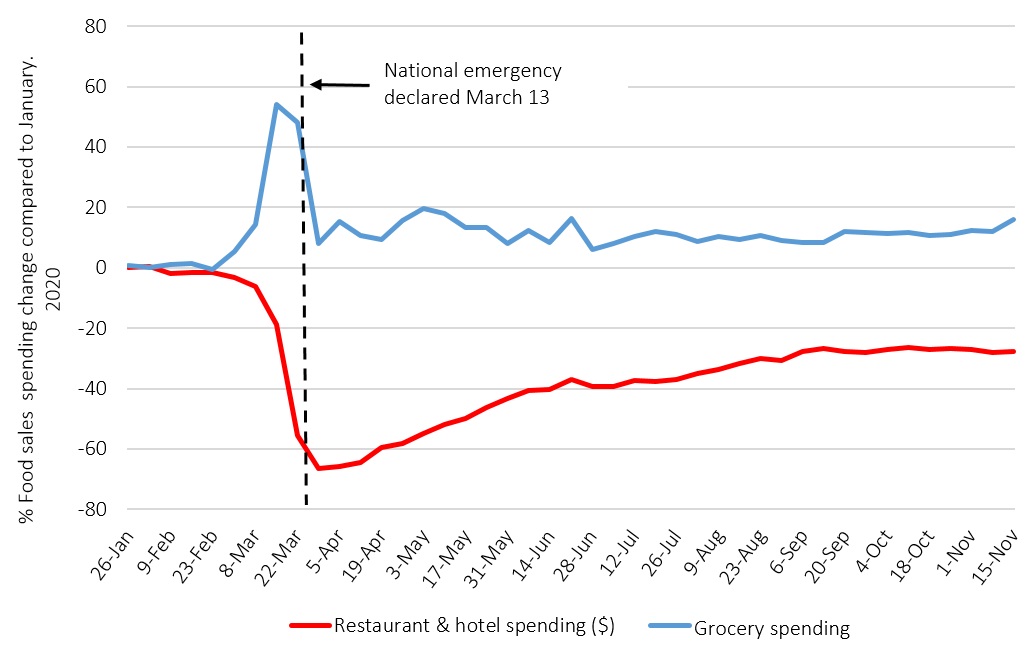

The spread of the virus throughout the United States caused additional, more acute disruptions to livestock and beef markets. Starting in March 2020, private precautions taken by people and firms to protect themselves from the virus, together with mandated closings of schools, businesses, and much of the retail sector, led to a sudden and dramatic reduction in demand for food service meals and an increase in demand for food in grocery stores (see Figure 1). With children staying home from school and workers staying home from work or losing their jobs, fewer people were eating meals at school and work. State and local governments took emergency measures to close retail businesses, including full-service restaurants and bars (fast food restaurants were not permitted to open dine-in facilities but were allowed to continue drive-thru and delivery service). In contrast, grocery stores were designated as essential businesses and remained open through the pandemic.

The combined effect of these events was to dramatically and suddenly alter retail demand for food, reducing demand for food served by commercial food service institutions, known as food away from home (FAFH), and increasing demand for food purchased in grocery stores, known as food at home (FAH). Figure 1 shows that spending in restaurants and hotels fell by more than 60% in March, while grocery spending spiked by more than 50%, as people prepared more meals at home.

The pandemic also affected United States meat supply chains. Starting in early March 2020, meat-packing plants and processors of poultry, pork, and beef were forced to scale back production or temporarily close as COVID-19 spread through the workforce (Bunge, 2020). The resulting illness, or fear of illness, contributed to absenteeism among plant workers (Polansek and Sullivan, 2020). Some plants were forced to temporarily close to prevent spread of the pandemic. Plants remaining open slowed production lines in in order to comply with public health guidelines for reducing COVID-19 spread (Parshina-Kottas et al., 2020; CDC, 2020). As plants were idled or forced to limit operations, daily capacity at cattle and hog facilities declined as much as 45% in May 2020 (Cowley, 2020), with others citing similarly dramatic declines (Muth and Read, 2020; Haley, 2020). Muth and Read (2020) cite estimates of the loss of production capacity because of plant closures ranging up to 25% for beef slaughter plants, 43% for pork slaughter plants, and 15% for chicken slaughter plants. The disruption of meat-packing plants reduced production of meat destined for retail outlets and created a backlog of livestock destined for the closed plants.

On April 28, 2020, President Trump issued an executive order invoking the Defense Production Act to keep meat-packing plants open (United States Department of Agriculture, 2020c). The executive order exempted plants from state and local orders to close nonessential businesses but did not solve plants’ problems with sick workers. COVID-19 outbreaks among the workforce continued to force plants to close and slow down even after the Executive Order.

Meat supply chains also struggled to transition their production lines and distribution networks in response to the pandemic events in the retail sector that reduced demand from food service and increased demand in groceries. FAFH meat is differentiated from FAH meat, and specialized production processes and distribution networks serve these separate marketing channels (Bittle, 2020). The rapid shift of demand from FAFH to FAH, combined with a costly transition of supply chains, contributed to higher prices and at times stockouts for some meat products in grocery stores in the spring of 2020 (Riley, 2020).

As discussed in more detail below, from approximately early April to early June 2020, capacity utilization fell significantly at pork and beef packing plants due to shutdowns and slow downs related to COVID-19. Reduced production capacity meant decreased supplies of meat products entering wholesale and retail markets. At the same time, the packing disruption caused reduced demand by packing plants for live animals. The net effect of these COVID-19 impacts was to increase wholesale and retail meat prices, decrease upstream prices of livestock, and thus increase the price spread between meat and livestock (Figures 2 and 3).

The market disruptions starting in March 2020 are evident in the food consumer price indices (Figure 4). Between February and June 2020, the food at home CPI increased by 3.5%. While CPIs for all food categories in the chart increased over this period, by far the largest increase was the meat CPI, at 9%. The CPI started to fall around June 2020, with the meat CPI falling almost 5% between June and July. Reductions in meat processing capacity associated with COVID-19 outbreaks were a likely cause of the increase in the meat CPI. For example, on April 29, 2020, pork packing plant capacity utilization bottomed out at 54%, compared to 100% in early April (Haley, 2020). By mid-June, capacity utilization in pork processing plants rebounded to near 95%; consumer prices for pork were falling. Other disruptions in the food chain were caused by the precipitous drop in FAFH and the associated increase in FAH, given differences between product types and production and distribution processes targeted at FAFH versus for FAH and the efforts needed to rechannel goods. Overall, even after the decrease in the CPI for food consumed at home from its peak in June, in July it was still 3.5% higher compared to February 2020. In contrast, the headline CPI for all goods—the CPI-U—actually fell from February to May 2020, and as of July was 0.1% lower than in February 2020. The gasoline CPI fell 23% from February to May 2020, likely driving much of that decrease in overall CPI.

| Percentage Change | |||||||

| Jan Proj. | May Proj. | Sept. Proj. | Oct. Proj. | Jan. vs. May | Jan. vs. Sept. | Jan. vs. Oct | |

| Steers ($/cwt) | 117.50 | 104.10 | 107.30 | 108.71 | -11.40% | -8.68% | -7.48% |

| Barrows and gilts ($/cwt) | 54.50 | 43.10 | 39.40 | 43.25 | -20.92% | -27.71% | -20.64% |

| Broilers (cents/lb) | 86.50 | 71.40 | 70.90 | 70.80 | -17.46% | -18.03 | -18.15% |

| Turkeys (cents/lb) | 92.50 | 104.60 | 105.80 | 106.10 | 13.08% | 14.38% | 14.70% |

| Eggs (cents/dozen) | 95.50 | 129.50 | 114.90 | 116.70 | 35.60% | 20.31% | 22.20% |

| Milk ($/cwt) | 19.25 | 14.55 | 17.75 | 18.00 | -24.42% | -7.79% | -6.49% |

Source: USDA, World Agricultural Outlook Board (2020, January and September).

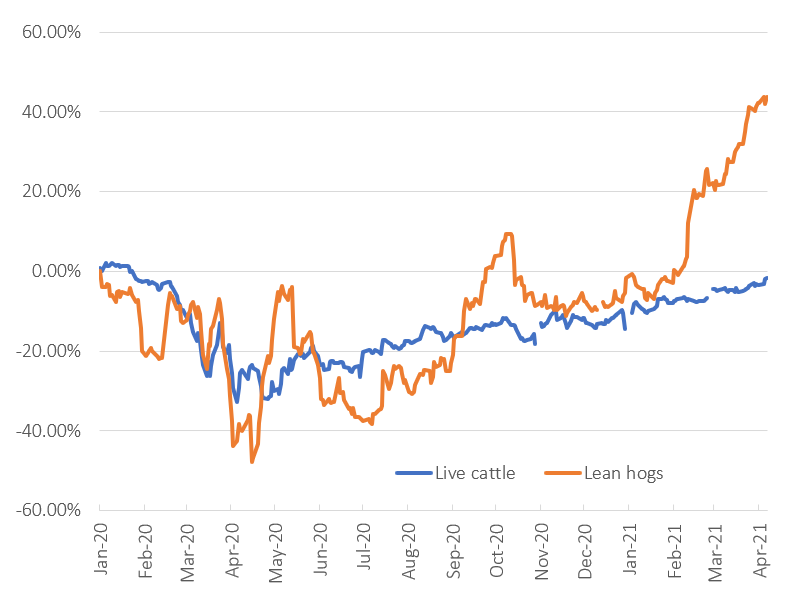

Table 1 reports the USDA’s projections for 2020 average annual livestock prices, as produced in the January, May, and September World Agricultural Supply and Demand Estimates reports (WAOB, 2020). Between January and May 2020, USDA’s projected prices fell by 11.4% for steers and 20.9% for barrows and gilts. Between May and October 2020, prices for steers had begun to rebound, while prices for barrows and gilts were flat. Figure 5 shows a similar pattern in futures contracts for cattle but considerably more fluctuation in hog futures, with the latter rallying considerably higher starting in February 2021.

Source: Adapted from Rhodes, Dauve, and Parcel (2015) and

Marchant (2020, p. 7).

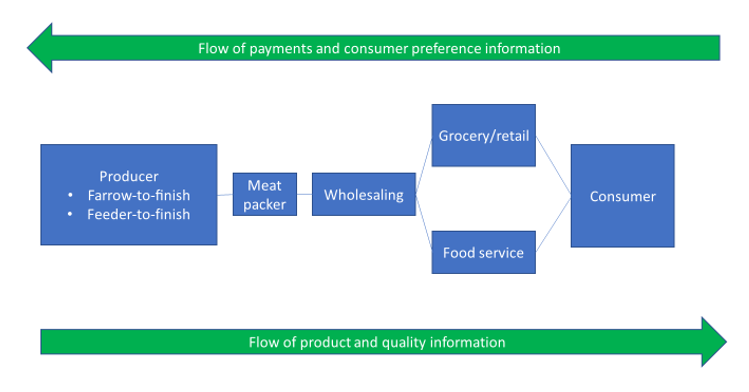

Figure 6 contains a flow chart of a meat marketing channel, using the example of hogs. Payment and consumer preference information move upstream from the consumer, and product and quality information move downstream from the producer.

Lusk, Tonsor, and Schulz (2020) posit a simple theoretical model of a meat supply chain to help illustrate the impact of COVID-19 on meat and livestock markets. In the model, the retail market for meat (e.g., beef) is linked to the market for livestock (e.g., fed cattle) by a “marketing” sector that includes meat processing, wholesale services, and retail services. Under some simplifying assumptions, the demand for livestock is obtained by subtracting the costs of these marketing inputs from the retail demand for meat. Similarly, the retail supply of meat is obtained from adding the costs of marketing inputs to the marginal cost (or supply) of livestock.

The model produces an intuitive equilibrium relationship between meat prices and livestock prices:

(1) Pmeat = Plivestock + M,

where Pmeat is the retail price of meat (in dollars per pound), Plivestock is the price of livestock (in meat-equivalent units), and M is the marketing margin. The simple interpretation of this relationship is that retail meat prices have two components: the packing plants’ cost of the livestock in the meat, Plivestock, and the cost of the marketing input, M. The marketing costs drive a wedge between the price of meat on the animal and the price of the meat at retail.

COVID-19 affects meat-packing plants by raising their costs of production, initially by making the workforce sick and thus less productive, and eventually by forcing processors to incur costs to protect workers from the virus. The effects of higher processing costs are distilled in the equilibrium pricing relationship displayed above, in the form of higher M. Higher processing costs increase the wedge between meat prices and livestock prices, so that meat prices must rise or livestock prices must fall. Higher processing costs cause a decrease in the meatpackers’ demand for livestock and a decrease in the retail supply of meat. As a result, downstream meat prices rise and upstream livestock prices fall.

The magnitudes of these price changes depend on the responsiveness (elasticities) of livestock supply and retail demand. Because both meat demand and livestock supply are quite inelastic in the short term, we expect to see relatively large changes in prices and relatively small reductions in quantity.

While the COVID-19 pandemic continues to play out, livestock and meat markets have begun to recover (Figure 5). But the events of the past 14 months have raised questions about the performance of United States food supply chains generally and of United States meat supply chains in particular. While these questions deserve more careful consideration, we provide some initial reactions based on the data and simple model presented above.

The news media and other observers of agricultural markets have speculated that meatpackers took advantage of COVID-19 to increase margins (e.g., Hagemann, 2020). At issue is meat-packing plants’ ability to exercise market power to earn super-competitive profits. The question arises in part because of the high degree of concentration in meat-packing. The CR4—a common measure of industry concentration of the four largest firms in the industry—was 85% for livestock/beef and 64% for hogs/pork in 2012 (Saitone and Sexton, 2017), up from 36% and 56%, respectively, in 1980 (Crespi, Saitone, and Sexton, 2012). In addition, the industry is characterized by large capital investment that prevents new firms from entering, at least in the short term. Indeed, a large body of empirical work by agricultural economists has investigated the question over the past decades and has tended to find that meat-packing plants do not exercise market power to harm livestock suppliers or consumers. We do not specifically assess market power here and thus cannot rule it out. But we do note that the observed price patterns that are of concern—high retail prices and low livestock prices—are not themselves evidence of market power, as they are consistent with the model described above, which assumes a perfectly competitive meat-packing sector. Also, capacity constraints may reduce the incentives for plants to reduce production; Lusk, Tonsor, and Schulz (2020) found that plants are better off trying to run near full capacity than voluntarily restricting output. They also found that, in general, changes in the stock prices of companies with significant packing operations do not suggest substantial windfalls corresponding to COVID-19.

Another concern related to the industrial organization of meat-packing plants is whether concentration makes the sector less resilient to the pandemic and speculation that localized supply chains have been more resilient to COVID-19. Resilience to a particular risk depends on susceptibility to the risk and the ability to manage the risk if realized (Johansson, 2020). On the question of susceptibility, smaller, more localized meat-packing plants may not have been less susceptible to the pandemic. If smaller plants are less susceptible, then more resilience via smaller and more localized packing plants comes at the cost of efficiency, as larger plants capture economies of scale that result in lower meat prices and higher livestock prices. It is possible there is a trade-off between efficiency in meat-packing and ability to quickly pivot to operating under a pandemic or more quickly changing marketing channels. For instance, at least initially, business was reportedly brisk at some small packing plant in the initial days of the COVID-19 outbreak (Huffsturrer and Nickel, 2020; NPR, 2020).

In early summer 2020, as the COVID-19 pandemic caused high prices and stockouts in the meat section of grocery stores, United States pork producers were expanding exports to China (Braun, 2020), causing some observers to wonder whether trade exacerbated the problems caused by COVID-19 in livestock and meat markets. Some countries restricted agricultural exports in an effort to protect domestic consumers (Reuters, 2020). Similar policies were implemented by some countries during the global commodity price spike of 2008–2011. While such policies may appear to help domestic consumers in the short term, the restriction of trade can actually exacerbate the local shortages that the trade restrictions are intended to prevent (Hendrix, 2020). First, export restrictions reduce domestic prices of restricted goods and thus create a disincentive to increase production and economize on consumption. Moreover, export restrictions disrupt the ability of markets to move product to places most in need. Currently, the United States does not restrict exports of meat or other agricultural commodities.

In this paper we provide an overview of the ways in which the COVID-19 pandemic upset United States markets for meat and livestock. Around the time that the United States government announced a national emergency in mid-March 2020 and state and local officials began to close schools and some businesses, demand for meat and other foods shifted dramatically away from food service and toward retail grocery. The COVID-19 demand shock, combined with some difficulties in reorienting meat supply chains, resulted in a spike in retail meat prices in the spring and occasional grocery store stockouts of some meat products. The pandemic also disrupted meat supply chains in the United States as the virus spread through the workforce in meat-packing plants, causing some plants to temporarily close and all plants to slow production to inhibit the spread of the virus. The resulting reduction in demand for livestock and supply of beef and pork caused lower livestock prices and higher meat prices in the spring and summer of 2020.

By late summer, the public health precautions taken by meat-packing plants appear to have been successful, as the number of COVID-19 cases at meat-packing plants from August through September is considerably lower than in May through July (Douglas, 2020) and steer and hog futures prices have returned to prepandemic levels. Food demand patterns have moved toward normalcy, but in Fall 2020 demand for FAFH remained more than 20% below prepandemic levels and demand for FAH approximately 10% higher than prepandemic levels. By late August 2020, the CPI for meat was declining but remained 10% above prepandemic levels.

The COVID-19 pandemic raises several questions and issues related to meat supply chains that warrant further research. We see a need for economic research into the incentives of meat-packing plants to run at full capacity and the trade-off that they face between profits and costly measures to manage the public health risk. More generally we see resilience, and in particular potential trade-offs between resilience and efficiency, as a fruitful area for additional research.

Badau, F. 2020, September 6. “U.S. Beef and Pork Consumption Projected to Rebound.” Amber Waves. Available online: https://www.ers.usda.gov/amber-waves/2016/september/us-beef-and-pork-consumption-projected-to-rebound/.

Bittle, J. 2020, May 6. “Beef Producers Are Grinding Up Their Nicest Steaks, While Retailers Can’t Meet Demand for Cheaper Cuts.” The Counter Available online: https://thecounter.org/beef-producers-grinding-steaks-ground-beef-coronavirus-covid-19-usda/.

Bloomberg. 2021, April 7. “The Terminal: Bloomberg Professional Services.” Bloomberg Anywhere Available online: https://bba.bloomberg.net/.

Braun, K. 2020, May 5. “U.S. Faces Meat Shortage While Its Pork Exports to China Soar.” Reuters. Available online: https://www.reuters.com/article/us-usa-pork-braun-idUSKBN22H2Q6.

Bunge, J. 2020, April 6. “Coronavirus Hits Meat Plants as Some Workers Get Sick, Others Stay Home.” The Wall Street Journal. Available online: https://www.wsj.com/articles/coronavirus-hits-meat-plants-as-some-workers-get-sick-others-stay-home-11586196511.

Centers for Disease Control and Prevention. 2020. COVID-19 Among Workers in Meat and Poultry Processing Facilities ― 19 States, April 2020.” Morbidity and Mortality Weekly Report 69(18): 557–561. Available online: https://www.cdc.gov/mmwr/volumes/69/wr/mm6918e3.htm.

Cowley, C. 2020, July 31. COVID-19 Disruptions in the U.S. Meat Supply Chain. Kansas City, MO: Federal Reserve Bank of Kansas City, Main Street Views: Policy insights from the Kansas City Fed. Available online: https://www.kansascityfed.org/en/research/regionaleconomy/articles/covid-19-us-meat-supply-chain.

Crespi, J., T. Saitone, and R. Sexton. 2012. “Competition in U.S. Farm Product Markets: Do Long-Run Incentives Trump Short-Run Market Power?” Applied Economic Perspectives and Policy 34(4): 669–695.

Douglas, L. 2020, October 21. “Could the Food System Face a New Covid-19 Wave?” Food and Environmental Reporting Network. Available online: https://thefern.org/2020/10/could-the-food-system-face-a-new-covid-19-wave-ahead/.

Hagemann, K. 2020, May 1. “How'd We Get Here? over the Decades, We Made the Meatpacking Industry ‘Too Big to Fail.’” Des Moines Register. Available online: https://www.desmoinesregister.com/story/opinion/columnists/iowa-view/2020/05/01/covid-19-iowa-how-meatpacking-industry-became-too-big-fail/3055086001/.

Haley, M. 2020. “U.S. Pork Processing Capacity Utilization Rebounds as COVID-19 Infections of Plant Labor Forces Recede.” Washington, DC: U.S. Department of Agriculture, Economic Research Service, Chart of Note. Available online: https://www.ers.usda.gov/data-products/chart-gallery/gallery/chart-detail/?chartId=98682.

Hendrix, C. 2020, March 30. “Wrong Tools, Wrong Time: Food Export Bans in the Time of COVID-19.” PIIE Insider Weekly Newsletter. Available online: https://www.piie.com/blogs/realtime-economic-issues-watch/wrong-tools-wrong-time-food-export-bans-time-covid-19.

Huffstutter, P., and R. Nickel. 2020, May 26. “How about Next June?' Small Meat Processors Backlogged as Virus Idles Big Plants.” Reuters. Available online: https://www.reuters.com/article/us-health-coronavirus-meatpacking/how-about-next-june-small-meat-processors-backlogged-as-virus-idles-big-plants-idUSKBN23217V.

Johansson, R. 2020, October 13. “America’s Farmers: Resilient throughout the COVID Pandemic.” USDA Blog. Available online: https://www.usda.gov/media/blog/2020/09/24/americas-farmers-resilient-throughout-covid-pandemic.

Lusk, J., G. Tonsor, and L. Schulz. 2020. “Beef and Pork Marketing Margins and Price Spreads during COVID-19.” Applied Economic Policy and Perspectives 43(1): 4–23.

Marchant, M. 2020. “Marketing of Agricultural Commodities.” Lecture, Blacksburg, VA: Virginia Tech University.

Muth, M., and Q. Read. 2020, July 7. “Effects of COVID-19 Meat and Poultry Plant Closures on the Environment and Food Security.” Insights Blog. Available online: https://www.rti.org/insights/covid-19-effect-meat-supply-chain.

NPR. 2020, April 30. “Small Meatpacking Plants Thrive as COVID-19 Forced Bigger Ones to Close.” National Public Radio. Available online: https://www.npr.org/2020/04/30/848179283/small-meatpacking-plants-thrive-as-covid-19-forced-bigger-ones-to-close.

Opportunity Insights. 2020. “Economic Tracker.” Cambridge, MA: Harvard University and Brown University. Available online: https://www.tracktherecovery.org/.

Parshina-Kottas, Y., L. Buchanan, A. Aufrichtig, and M. Corkey. 2020, June 12. “Take a Look at How COVID-19 Is Changing Meatpacking Plants.” Chicago Tribune. Available online: https://www.chicagotribune.com/coronavirus/sns-nyt-how-coronavirus-changing-meatpacking-plants-20200612-xxmpecs3ebhppafujpj5wzmw6u-story.html.

Polansek, T., and A. Sullivan. 2020, June 15. “Meatpacking Workers Often Absent after Trump Order to Reopen.” Reuters. Available online: https://www.reuters.com/article/us-health-coronavirus-usa-meatpacking/meatpacking-workers-often-absent-after-trump-order-to-reopen-idUSKBN23M1EQ.

Reuters. 2020, April 3. “Trade Restrictions on Food Exports Due to the Coronavirus Pandemic.” Reuters. Available online: https://www.reuters.com/article/us-health-coronavirus-trade-food-factbox/trade-restrictions-on-food-exports-due-to-the-coronavirus-pandemic-idUSKBN21L332.

Riley, L. 2020, April 14. “The Industry Says We Have Enough Food. Here’s Why Some Store Shelves Are Empty Anyway.” The Washington Post. Available online: https://www.washingtonpost.com/business/2020/04/14/grocery-stores-empty-shelves-shortage/.

Rhodes, J., J. Dauve, and J. Parcel. 2015. The Agricultural Marketing System, 7th ed. Columbia, MO: University of Missouri Publishing.

Saitone, T., and R. Sexton. 2017. “Concentration and Consolidation in the U.S. Food Supply Chain: The Latest Evidence and Implications for Consumers, Farmers, and Policymakers.” Economic Review, Special Issues: 25–59. Available online: https://www.kansascityfed.org/~/media/files/publicat/econrev/econrevarchive/2017/si17saitonesexton.pdf.

U.S. Bureau of Labor Statistics. 2021. Consumer Price Index (CPI) Databases. Washington, DC: U.S. Bureau of Labor Statistics. Available online: https://www.bls.gov/cpi/data.htm.

U.S. Department of Agriculture. 2020a. Livestock and Meat International Trade Data. Washington, DC: U.S. Department of Agriculture, Economic Research Service. Available online: https://www.ers.usda.gov/data-products/livestock-and-meat-international-trade-data/livestock-and-meat-international-trade-data/ - Annual and Cumulative Year-to-Date U.S. Livestock and Meat Trade by Country.

U.S. Department of Agriculture. 2020b. Meat Price Spreads. Washington, DC: U.S. Department of Agriculture, Economic Research Service. https://www.ers.usda.gov/data-products/meat-price-spreads/.

U.S. Department of Agriculture. 2020c, April 28. “USDA to Implement President Trump’s Executive Order on Meat and Poultry Processors.” Washington, DC: U.S. Department of Agriculture, Press Release. Available online: https://www.usda.gov/media/press-releases/2020/04/28/usda-implement-president-trumps-executive-order-meat-and-poultry.

World Agricultural Outlook Board. 2020. “World Agricultural Supply and Demand Estimates.” Washington, DC: U.S. Department of Agriculture, Office of the Chief Economist, World Agricultural Outlook Board. Available online: https://www.usda.gov/oce/commodity/wasde.

World Trade Organization. 2020. Second Quarter 2020 Merchandise Trade. Available online: https://www.wto.org/english/res_e/statis_e/daily_update_e/merch_latest.pdf.